Employee State Insurance (ESI) and PF is Provident Fund (PF)

Out of all the schemes and laws, the EPF and ESIC are the most sought after. In both the schemes a predefined percentage is deducted from employee’s salary and proportionate amount is added to it by employer and then aggregate amount is deposited to the account of concerned employee. Both the Schemes are concerned with the employee welfare. Two such important social protections are ESI registration & EPF registration.

The Employees Provident Fund Organization (EPFO) is a statuary body which assists Central Board in administering compulsory contributory Provident Fund Scheme, Pension Scheme and Insurance Scheme for the workforce engaged in the organized sector in India.

The Employees' Provident Fund came into existence with the promulgation of the Employees' Provident Funds Ordinance on the 15th November, 1951. It was replaced by the Employees' Provident Funds Act, 1952. The Act is now referred as the Employees' Provident Funds & Miscellaneous Provisions Act, 1952 which extends to the whole of India. The Act and Schemes framed there under are administered by a tri-partite Board known as the Central Board of Trustees, Employees' Provident Fund, consisting of representatives of Government (Both Central and State), Employers, and Employees.

The Central Board of Trustees administers a contributory provident fund, pension scheme and an insurance scheme for the workforce engaged in the organized sector in India. The Board is assisted by the Employees’ PF Organization (EPFO), consisting of offices at 135 locations across the country. The Organization has a well equipped training set up where officers and employees of the Organization as well as Representatives of the Employers and Employees attend sessions for trainings and seminars. The EPFO is under the administrative control of Ministry of Labor and Employment, Government of India.

The Board operates three schemes - EPF Scheme 1952, Pension Scheme 1995 (EPS) and Insurance Scheme 1976 (EDLI).

New companies under incorporation will get EPFO Registration number on MCA Portal at the time of incorporation. Such companies will have to comply under (Employees Provident Funds and Miscellaneous Provisions Act, 1952) EPF & MP Act, 1952, and ESI Act, 1948 only when they cross threshold limit of employment.

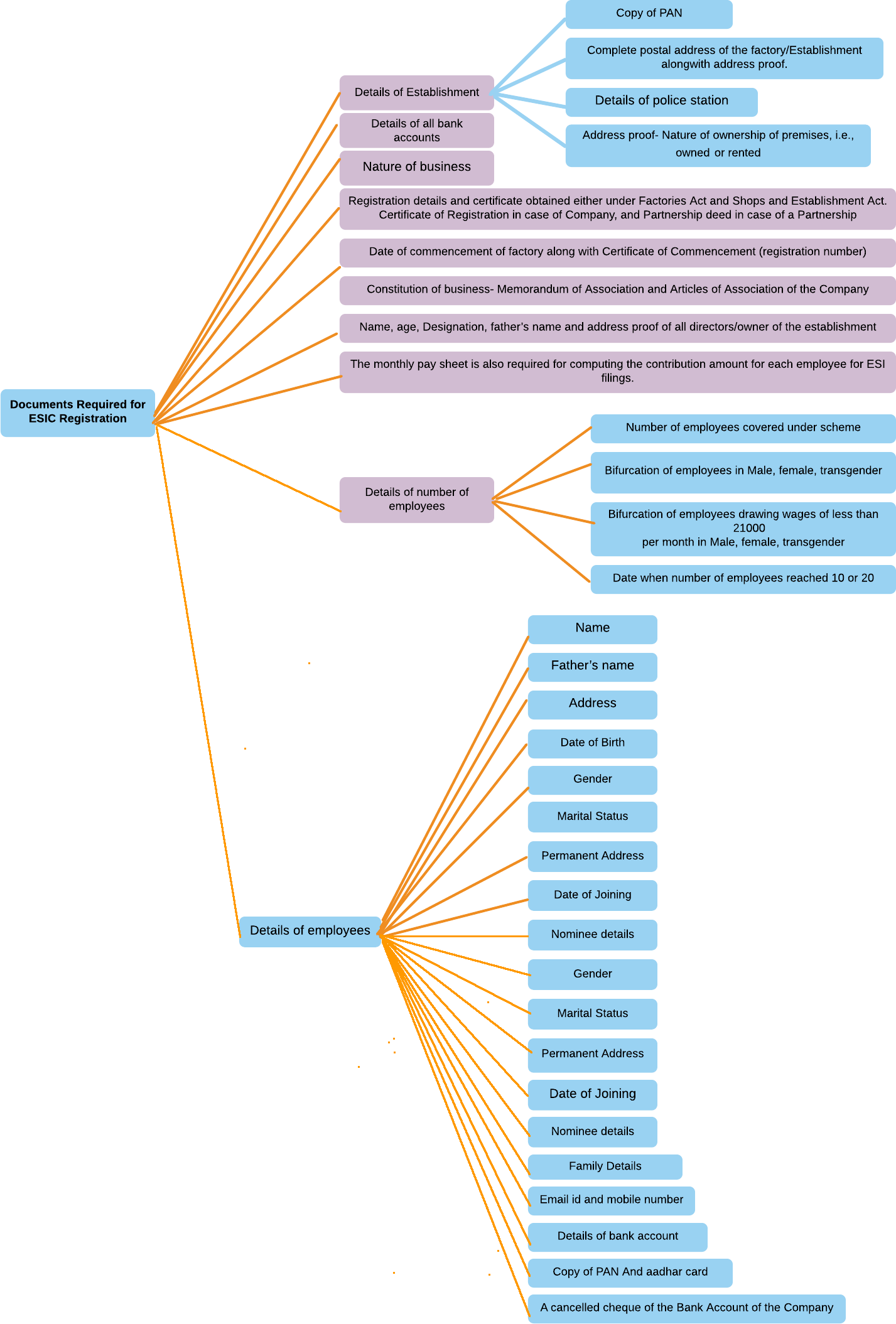

No physical documents are to be submitted to EPFO and ESIC office for registration and also no physical visit is required. All the documents are to be uploaded online only at the time of filling application for registration.

The promulgation of Employees' State Insurance Act, 1948(ESI Act), by the Parliament was the first major legislation on social Security for workers in independent India. The ESI Act 1948 encompasses certain health related eventualities that the workers are generally exposed to; such as sickness, maternity, temporary or permanent disablement, Occupational disease or death due to employment injury, resulting in loss of wages or earning capacity-total or partial. Social security provision made in the Act to counterbalance or negate the resulting physical or financial distress in such contingencies, are thus, aimed at upholding human dignity in times of crises through protection from deprivation, destitution and social degradation while enabling the society the retention and continuity of a socially useful and productive manpower.

The ESI Scheme applies to factories and other establishment's viz. Road Transport, Hotels, Restaurants, Cinemas, Newspaper, Shops, and Educational/Medical Institutions wherein 10 or more persons are employed. However, in some States threshold limit for coverage of establishments is still 20. Employees of the aforesaid categories of factories and establishments, drawing wages upto 15,000/- a month, are entitled to social security cover under the ESI Act. ESI Corporation has also decided to enhance wage ceiling for coverage of employees under the ESI Act from 15,000/- to 21,000/-.

Categories of unorganized workers covered are construction workers, domestic workers, migrant workers, agriculture workers, gig and platform workers and other unorganized workers.

ESI Corporation has extended the benefits of the ESI Scheme to the workers deployed on the construction sites located in the implemented areas under ESI Scheme w.e.f. 1st August, 2015.

The ESI Scheme is financed by contributions from employers and employees. The rate of contribution by employer is 4.75% of the wages payable to employees. The employees' contribution is at the rate of 1.75% of the wages payable to an employee. Employees, earning less than 137/- a day as daily wages, are exempted from payment of their share of contribution.

However, there are certain procedures to be followed in order to legally safeguard the company, such as:

Employees’ Provident Fund (EPF) Fund (PF)

The Employees’ Provident Fund (EPF) is a savings scheme introduced under Employees’ Provident Fund and Miscellaneous Act, 1952. It is managed by the central board of trustees consisting of the government, employer and employees; it is assisted by The Employees’ Provident Fund Organization. EPFO works under the direct jurisdiction of the government and is managed through the Ministry of Labor and Employment.

EPF is commonly known as PF in India and is a scheme through which a portion of employee’s income is set aside for use during any emergency or post-retirement. The employer and employees deposit a certain percentage towards PF every month. The percentage of money to be deducted from the employee’s salary and percentage to be contributed by the employer is predefined under EPF Act.

For EPF, both the employee and the employer contribute an equal amount of 12% of the monthly salary of the employee.

Employees can contribute more than 12% of their salary voluntarily; however the employer is not bound to match the extra contribution of the employee.

For PF contribution, the salary comprises of fewer components: All Allowances paid as part of salary are subjected to PF contribution

- Basic wages,

- Dearness Allowances (DA),

- Conveyance allowance and

- Special allowance.

As per PF law, ‘Basic wages’ means

“all emoluments which are earned by an employee while on duty or (on leave or on holidays with wages in either case) in accordance with the terms of the contract of employment and which are paid, or payable in cash to but does not include:

- the cash value of any food concession;

- any dearness allowance (that is to say, all cash payments by whatever name called paid to an employee on account of a rise in the cost of living), house-rent allowance, overtime allowance, bonus, commission, or any other similar allowance payable to the employee in respect of his employment or of work done in such employment and

- any presents made by the employer.”

‘Basic wages’ and are hence liable for contribution under the PF law.

PF contribution is not attracted where the Employee is eligible to receive any additional amounts including incentives, bonus, over-time allowance etc. Allowances not earned by all Employees are not subject to PF contribution.

Cap on Provident Fund contributionThe employer’s monthly contribution is restricted to a maximum amount of 1,800. Even if the employee’s salary exceeds 15,000, the employer is liable to contribute only 1,800 (12% of 15,000). Details of EPF

The statutory compliance associated with PF contribution has some lesser known facts associated with it. The contributions by the employee and employer are divided into two separate funds:

- EPF (Employee Provident Fund) and

- EPS (Employee Pension Scheme).

The breakup happens as follows: The Employee contribution is completely allotted to Employee Provident Fund (‘EPF’) while the Employer contribution is bifurcated between EPF (3.67%) and Employee Pension Scheme (‘EPS’) (8.33%).

Employee |

Employer |

|

| Total contribution | 12% of monthly salary | 12% of monthly salary (subject to a maximum of 1,800) |

| Employee Pension Scheme (EPS) | 0 | 8.33% (of the 12%) |

| Employee Provident Fund (EPF) | Full amount | 3.67% (of the 12%) |

| Example Monthly Salary: 12,000 | ||

| Total Contribution | 12,000 * 12% = 1,440 | 12,000 * 12% = 1,440 |

| EPS0 | 0 | 12,000 * 8.33% = 999.60 |

| EPF | 1,440 | 12,000 * 3.67% = 440.40 |

In general, the contribution rate for the employee is fixed at 12%. However, the rate is fixed at 10% for the below-

mentioned organizations:

- Organizations or firms employing a maximum of 19 workers.

- Industries declared as sick industries by the BIFR

- Organizations suffering an annual loss much more as compared to their net value.

- Coir, guar gum, beedi, brick and jute industries.

- Organizations operating under the wage limit of 6,500.

Eligibility Criteria for Registration under Provident Fund

- Any organization or factory with at least 20 employees needs to get them registered under EPF Scheme.

- Establishment with less than 20 employees may get themselves voluntarily registered.

- Liability to deduct and deposit EPF arises for all employees with wages of Less than 15,000 per month,

- Employees of an organization, which are already registered under EPF Scheme, are directly eligible for getting their Provident Fund account opened from date of their joining.

- Employees need to become an active member of the scheme in order to avail of benefits under this scheme.

- Employees of an organization are directly eligible for availing Provident Fund, insurance benefits as well as pension benefits since the day they join the organization.

- Any organization employing a minimum of 20 workers is liable to give EPF benefits to the workers.

- This scheme does not cater to the needs of people residing in Jammu and Kashmir.

There are many benefits of registering to the EPF scheme, some of these are:-

Amount deposited in EPF Account is a savings that can be withdrawn at any

time for any purpose such as Education, Marriage, Medical emergency or same

can be obtained post retirement.

If you withdraw the PF amount and interest on its maturity or after 5 years of

completion of continuous employment, then its entire amount will be exempted

from any Income tax liability.

If the employee leaves the organization then he/she can withdraw 75% of the

balance lying in EPF account on completion of one month of continuous

unemployment. Balance 25% can be withdrawn post continuous employment

period of 60 days.

Unlike before, EPF accounts are created and maintained completely online and

the employees can have access to their EPF funds anywhere in the world

with universal account number.

In case of death of the employee the nominee will get the PF amount and

interest accumulated over the period.

Just like the ESI scheme, the Employees Provident Fund (EPF) is a Contributory fund with contributions from both the employee and their employers.

While the focus of the ESI scheme is healthcare, Provident Fund is focused towards post Retirement Income and Benefits.

EPF is a compulsory and contributory fund for Indian organizations under “The Employees’ Provident Fund and Miscellaneous Provisions Act 1952”.

EPF registration is mandatory for all establishments-

- Which is a factory engaged in any industry having 20 or more persons, and

- To any other establishment employing 20 or more persons or class of such establishments which the Central Government may, by notification specify in this behalf.

Central Government may apply any establishment employing less than 20 employees after giving not less than two months’ notice for compulsory registration

Where the employer and majority of employees have agreed that the provisions of this act should be made applicable to the establishment, they may themselves apply to the Central PF Commissioner. The Central PF Commissioner may apply the provisions of this Act to that establishment after passing the notification in the Official Gazette from the date of such agreement or from any subsequent date specified in the agreement.

Some establishments having less than 20 employees would also be required to obtain PF registration but that is voluntary registration. All the employees will be eligible for a PF from the commencement of their employment and the responsibility of deduction & payment of PF lies with the employer.

| Contribution Rate (%) | Employee’s Contribution Rate (%) | Employer’s Contribution Rate (%) |

| A/c No. 1: PF Contribution Account*) | 12.00 | 3.67 |

| A/c No. 2: PF Admin Charges Account | – | 0.50 |

| A/c No. 10: EPS Contribution Account | – | 8.33 |

| A/c No. 10: EPS Contribution Account | – | 8.33 |

| A/c No. 21: EDLIS Contribution Account | – | 0.50 |

| EPS0 | 0 | 12,000 * 8.33% = 999.60 |

| Total Contribution | 12.00 | 13.00 |

Monthly payable amount under EPF Administrative charges is rounded to the nearest rupee and a minimum of 500/- is payable.

Note: - If the establishment has no contributory member in the month, the minimum administrative charge will be 75/-

- The contributions are payable on maximum wage ceiling of 15000/-

- The employee can pay at a higher rate and in such case employer is not under any obligation to pay at such higher rate.

- To pay contribution on higher wages, a joint request from Employee and employer is required [Para 26(6) of EPF Scheme]. In such case employer has to pay administrative charges on the higher wages (wages above 15000/-).

- For an International Worker, wage ceiling of 15000/- is not applicable.

The most primary advantage of the EPF registration is that you can cover the monetary risks of your employees along with their dependents that might occur owing to retirement, ill-health or their decease. As it is one person, one account: another key benefit is that the PF account that it’s firm and movable. It may be easily carried forward by your employee at another place of employment.

Achieving Long-term objective: Numerous long-term aims such as children’s wedding or their upper education that have need of the critical availability of finances. Now, here the accrued PF amount will prove useful on such occurrences.

An amount of deposit in provident fund is eligible for tax exemption under Section 80C of Income Tax Act,1961. The government has raised the threshold limit of tax-exempt contributions to the Provident Fund (PF) to 5 lakh (from 2.5 lakh announced in Budget 2021), subject to certain conditions. This increased tax-exempt limit is applicable to only those PF contributions where there is no employer contribution. In the case of government employees, there is such a fund called General Provident Fund where the government does not contribute. Rather, the government's contribution goes to the pension fund of the employees. As there is no contribution by the employer (i.e., the government), employees of the government sector can contribute a maximum of 5 lakh into their PF accounts in a financial year to earn tax-exempt interest.

However, the limit for private-sector employees shall continue to be 2.5 lakh (EPF + VPF) as the employer needs to contribute towards Employee Provident Fund.

Benefits of EPF Scheme for employees

EPF scheme is among one of the largest and biggest saving schemes available to Indian employees. The key benefits of the scheme are mentioned below:

Tax Benefits

- The interest rate earned on the EPF account is eligible for tax exemption under Section 80C of the income tax act upto 1.5 lakh. Also, even multiple transactions from the EPF account would not lure any taxes for five years unless the employee voluntarily opts to resign from the job or terminate his/her tenure. Any contribution towards the EPF account doesn’t attract any tax liabilities.

Easy transferability

- With Universal Account Number (UAN) at the disposal, the employees would have access to their PF account through the online portal of EPF. This would let them coordinate their EPF account with different employees during their service life.

Long-Term Financial Security:

- Funds deposited in this account cannot be withdrawn easily and hence, helps in ensuring savings.

Retirement Period:

- The accumulated fund under this scheme may be used at the time of retirement of the employee. This provides relief to the retired employee in the form of monetary security.

Unseen circumstances:

- The accumulated fund can be used by the employee in case of any kind of emergency. The employee may choose to withdraw his/her fund prematurely. The scheme provides for such pre-term withdrawals in certain special cases.

Unemployment/Income Loss:

- In case, where the employee loses his/her current job owing to any reason, then these funds may be used to meet expenses.

Resignation/Quitting of Job:

- The employee post-resignation is free to withdraw his/her 75% of the EPF fund after one month of the date of having quit the job and remaining 25% after 2 months of unemployment.

Death:

- In case of death of the employee, the collected amount along with the interest is given to the employee’s nominee thus helping the family tide through difficult times.Accumulation plus interest upon retirement, resignation, death.

Disability of the employee:

- If the employee is no longer in the position to work then he/she may use these funds to help him/her get over the difficult time.

Lay-off:

- In cases of sudden layoffs or retrenchment from the job, this fund may be used by the employee until the time he/she gets another suitable job.

Pension Scheme:

- The employer not only contributes towards the PF fund but also makes the necessary contributions towards the employee’s pension which can be later used by the employee post-retirement.

Insurance Scheme:

- The act also provides for certain provisions whereby, the employer is required to make certain contributions towards an employee’s life insurance where group insurance cover is not present. This scheme ensures that the employees are properly insured.

Accessible All Over:

- With the help of the Universal Account Number (UAN), employees can easily get access to their PF account via the EPF member portal. They can transfer their accounts whenever they make a shift in their current jobs.

Partial withdrawals

- Partial withdrawals allowed for specific expenses such as house construction, higher education, marriage, illness etc.

Employee Provident Fund (EPF)

The Employee Provident Fund (EPF) is a scheme in which both the employee and employer of an organization contribute certain amount for retirement benefits of the employee.

Every organization having 20 or more employees is required to register with the Employee Provident Fund Organization (EPFO). Both the employee and employer are required to contribute 12% of the basic pay to the EPF account. The entire 12% of employee’s basic pay is contributed to EPF account. The employer’s contribution is also 12% of the basic pay but only 3.67% of it is directed towards the EPF and the remaining 8.33% is contributed in the Employee Pension Scheme. The money contributed by employee and his employers is used as retirement funds for the employee. The employee can also withdraw this amount partially before his retirement.

Employers will not be able to generate the Electronic Challan cum Return (ECR) or EPF challan online in case the establishment is not registered. The employer will also need to register to create the User ID and password in order to access the details on the EPFO portal. Hence it is mandated for the employer to register online. All new registrations must be made online as the offline registration process has been done away with.

The Employee Provident Fund Organization allots a unique Universal Account Number i.e. UAN to every employee. This UAN is linked to their EPF account. This UAN is valid throughout the employee’s life. An employee doesn’t need to change his UAN or transfer his EPF account in the event of job change. He just needs to update the employer details.

Rate of interest on EPFThe rate of interest on EPF is decided by EPFO on yearly basis. The Central Board of trustees of EPFO has recommended 8.50% of rate of interest for EPF accounts for the financial year 2020-21. Interest will continue to accrue of EPF accounts till the account becomes inoperative. The account becomes inoperative when the employee retires from his service or shifts to abroad permanently or dies or if the withdrawal application is not made within 36 months.

EPF Monthly Returns:Every employer who is registered with EPFO has to file monthly EPF returns mandatorily. EPFO has launched online receipt of Electronic Challan cum Return (ECR) is April 2012. Employers are required to register their establishment and generate user id and password under the EPFO portal. The registered employer can upload electronic return on portal. Online challan will popped based on uploaded return after employer’s approval. The employer can make payment through internet banking. The EPF return must be filed by the 15th date of next month. For example, the due date of EPF return for March, 2021 is 15th April, 2021.

EPF returns can be filed by employer only. Before filing the returns, employer has to do 4 important things–

- KYC Details: Before filing the returns, the employer has to take KYC details of every employee working in his organization. The KYC details include Aadhar card details, PAN No and Bank details with proof.

- PF Calculations: The employer is required to do the PF calculations of every employee from the salary statement. These calculations include calculation of employee’s contribution, calculation of admin charges, EDLI charges, EPF wages and EPS wages.

- Generate UAN: The employer has to generate Universal Account Number i.e. UAN of every employee through EPFO portal.

- Mark Exited Employees: The employer has to mark exited employees from the portal i.e. employee who has left the company. For example, if current month is March, then you have to mark the exit date of employees who has left the company in February.

EPF ECR File

After obtaining registration under EPF/ESIC Act, adding, deleting or modifying records of Employees on regular basis is also essential.

Computation of ESIC and EPF liability and ensuring that the same is deposited within due date Filing returns under EPF and ESIC.

EPF ECR file also known as the PF calculation sheet which is used to create EPF contributions text file and it is further used to create monthly EPF challans.

Fields present in EPF ECR File Format| S No | Field Name | Details |

| 1 | UAN | Here we have to put the UAN number of the employee |

| 2 | Member Name | Here we have to write the member name |

| 3 | Gross Wages | This is also new in the ECR file, here we have to add the gross wages of employees |

| 4 | EPF Wages | Basic wage of employee has to be entered |

| 5 | EPS Wages | Basic wage of employee has to be entered |

| 6 | EDLI Wages | Basic wage of employee has to be entered |

| 7 | EPF Contribution Remitted | 12% of employee contribution |

| 8 | EPS Contribution Remitted | 8.33% of employer contribution |

| 9 | EPF EPS Difference Remitted | Generally it 3.67% of employer contribution towards PF, when the basic wage of an employee is greater than 15000 then it will automatically calculate the PF contribution of employer |

| 10 | NCP Days | Non contribution period days of employee i.e. absenteeism days. |

| 11 | Refund Of Advances | If is there any advance taken by the employee from the PF account, then he can repay that amount here. |

The major differences in Old ECR format and the new UAN based format are Universal Account Number; in the ECR text file 2 version, UAN is mandatory and in the old format we don’t need to add a UAN number. Another main difference is gross wages entry, in the old ECR format there is no need to add gross wages but in the new ECR file we as employer have to show gross wages of employees also.

Aadhaar Seeding Mandatory for all EPF Accounts- June 1, 2021As on 1st June 2021, EPFO has announced that Aadhaar Seeding is mandatory for all EPF accounts. Employers have been directed that ECR (Electronic Challan cum Return) is allowed only for accounts where the employee’s Aadhaar is seeded. This means if your Aadhaar is not linked to your EPF account, the employer’s contribution will not get credited to your EPF account. This decision has been taken under Section 142 of the Social Security Code 2020.

Contributions above 2.5 lakh per annum towards EPF would now be taxed. This will be effective from 1st April 2021, i.e. the new financial year.

The reason stated behind this new development is to better organize the tax exemption availed by those who fall in the high-income groups.

EPFO, on March 4th, 2021, announced the EPF rate of interest at 8.50%, keeping it the same as of the previous year 2019-20. To receive EPF interest, subscribers should make sure that there KYC details are updated and correct as per their PAN and bank records. Due to KYC mismatch, the interest payment of approximately 40 lakh subscribers for the financial year 2019-20 was delayed.

Universal Account Number or UAN

Every employer liable to get himself registered under EPF Scheme is required to get all its employees, liable for deduction of EPF, registered on EPF Portal. The Employee Provident Fund Organization (EPFO) allots unique Universal Account Number (“UAN”) to all employees. UAN is a 12-digit Account Number. The UAN of an employee remains the same throughout life irrespective of the number of jobs he/she changes. Every time an employee switches his/her job, EPFO allots a new member identification number (ID), which is linked to the UAN. You can put in a request for a new member ID by submitting the UAN to the new employer. Once the member ID is created, it gets linked to the UAN of the employee.

Features of UAN- The UAN helps to centralize employee data in the country

- One of the most significant uses of this unique number is that it brings down the burden of employee verification from companies and employers by EPF organization.

- This account made it possible for EPFO to extract the bank account details and KYC of the member and KYC without the help of the employers.

- It is useful for EPFO to track multiple job switches of the employee.

- Untimely and early EPF withdrawals have reduced considerably with the introduction of UAN.

- Every new PF account with a new job will come under the umbrella of a single unified account.

- It is easier to withdraw (fully or partially) PF online with this number.

- The employees themselves can transfer PF balance from old to new account using this unique account number.

- Any time you want a PF statement (visa purpose, loan security, etc.), you can download one instantly – either by logging in using the member ID or UAN or by sending an SMS.

- There is no need for new employers to validate your profile if the UAN is already Aadhaar and KYC-verified

- UAN ensures that employers cannot access or withhold the PF money of their employees.

- It is easier for employees to ensure that his/her employer is regularly depositing their contribution in the PF account.

Documents required for opening UAN

If you have just joined your first registered company for a job, you need the following documents to get your Universal Account Number.

Bank account info:

- Bank Name

- Account number,

- IFSC code

- Branch name

ID proof:

Any photo-affixed and national identity cards like driving license, passport, voter ID, Aadhaar, and SSLC Book

Address proof:

A recent utility bill in your name, rental/lease agreement, ration card or any of the ID proof mentioned above if it has your current address

PAN card:

Your PAN should be linked to the UAN.

Aadhaar card:

Since Aadhaar is linked to the bank account and mobile number, it is mandatory

Check UAN Number

There are two ways in which you can find out your UAN number. The first is by getting it through your employer through offline mode and the second way is to find it by using the UAN portal:-

Checking your UAN with your employerNormally, in case of your first employment, your employer will notify you about your Universal Account Number. However, if, for some reason, you don’t have a record of it, your UAN number is printed on your salary slip from the time your company starts deducting your salary towards PF contributions. This is the most common protocol followed by Indian companies, making it easy for you to check your UAN right on the salary slip.

Finding your UAN on the websiteLog on to the UAN portal www.unifiedportal-mem.epfindia.gov.in/memberinterface

- Click on the ‘Know your UAN Status’ tab.

- Post clicking, the system will ask you to enter your registered Mobile number and captcha appears on screen. After entering your mobile number, click on “Request OTP”.

- System will send an OTP to a registered mobile number.

- Upon validation of OTP, system will ask you to enter basic details such as Name, Date of Birth and Aadhar Number/PAN/Member ID and captcha appearing on screen.

- Upon entering valid information, the system will display UAN allotted to assessee.

4 ways to check your PF balance with UAN

Employers generally share your PF balance status once every year, normally at the end of each financial year. However, in case you don’t want to wait that long or want to check your PF balance on a monthly basis, then you can do that at your convenience using your UAN number via any of these 4 simple paths.

Check UAN Number

Check PF Balance Using EPFO Portal

Go to www.epfindia.gov.in and select the ‘For Employees’ tab under ‘Our Services’. A Member Passbook Facility page will open. Enter your UAN number and password based on your credentials here and you will immediately get access to your passbook. Members of establishments who are exempted under the EPF Scheme, 1952, will not be allowed to access the passbook facility.

Check PF Balance Using SMS Facility

Message EPFOHO “UAN” to 7738299899. Once the message is successfully sent, keep selecting the options and reply based on the messages you receive and within minutes you will get your balance via SMS.

Check PF Balance Using Missed Call Facility

Give a missed call on 011-22901406 from your registered mobile number and the balance details will be sent to you as a SMS.

Check PF Balance Using UMANG App

Download the app of EPFO and click on the option ‘‘Employee Centric Services’. Enter your UAN and log in using the OTP sent to your mobile number. Then you can check your EPF passbook, raise a claim or track any claims you have initiated.

Link Aadhaar with UAN

Offline mode of Aadhar Updation

EPFO has developed an Aadhaar Linking Application Form and you will need to fill it using your UAN, Aadhaar number, and other required personal details. You will also have to attach self-attested copies of your UAN card, PAN card, and Aadhaar card with this form. Then you can submit all the documents at the field offices of EPFO or Common Services Centers (CSC). Once verified and registered your Aadhaar will be linked to your UAN and you will get notified about the same via SMS.

Online mode of Aadhar Generation

To link your Aadhaar on the website, you will just have to enter your UAN number and your mobile number to generate an OTP. On entering the correct OTP, you will be asked to enter your Aadhaar number and specify your gender. Choose the OTP verification after this step to successfully generate and verify your Aadhaar. Once done click ‘Submit’. Your Aadhaar will be linked to your UAN within 15 days.

- Access Passbook

- Obtain UAN Card

- List of previous member IDs

- KYC Details

- Edit personal details

- Withdraw balance in EPF Account

- UAN number remains the same till the time you are employed whereas the EPF number is generated every time when the employee changes the job.

- You can access your provident fund account online by the help of UAN number whereas in case of EPF there is no such facility is there.

- In case of UAN number you can make a withdrawal request without the signature of your employer where as in EPF employer signature is compulsory for withdrawal request.

- UAN number can be linked with Aadhaar card number which is very useful whereas the EPF you cannot link it with Aadhaar number.

- In case of job change no need to transfer the provident fund amount from old employer to new employer in case of UAN number. Just give the UAN no to the new employer and the contribution would be done on the same account. Whereas in case of EPF you are supposed to transfer the amount from old account to new account, this can take much longer and is full of hassles.

EPF Registration for Employers – EPF Employer Login, Registration

Online registration is important for employers as they deduct the TDS from employees’ salary. In order to register online, you will be required to create an account first. PF registration is obligatory for companies with more than 20 employees.

EPF registration is mandatory for all establishments-

The employer must obtain the registration within 1 month of attaining the strength, failing which penalties will be applicable.0020 A registered establishment continues to be under the purview of the Act even if the employee strength falls below the required minimum.

Central Government may apply the provisions to any establishment employing less than 20 employees after giving not less than two months’ notice for compulsory registration. Where the employer and majority of employees have agreed that the provisions of this act should be made applicable to the establishment, they may themselves apply to the Central Provident Fund (PF) Commissioner.

The Central PF Commissioner may apply the provisions of this Act to that establishment after passing the notification in the Official Gazette from the date of such agreement or from any subsequent date specified in the agreement. Some establishments having less than 20 employees would also be required to obtain PF registration but that is voluntary registration.

All the employees will be eligible for a PF from the commencement of their employment and the responsibility of deduction & payment of PF lies with the employer. The PF contribution of 12% should be divided equally between the employer and employee. The employer’s contribution is 12% of the basic salary. If the establishment has employed less than 20 employees, the PF deduction rate will be 10%.

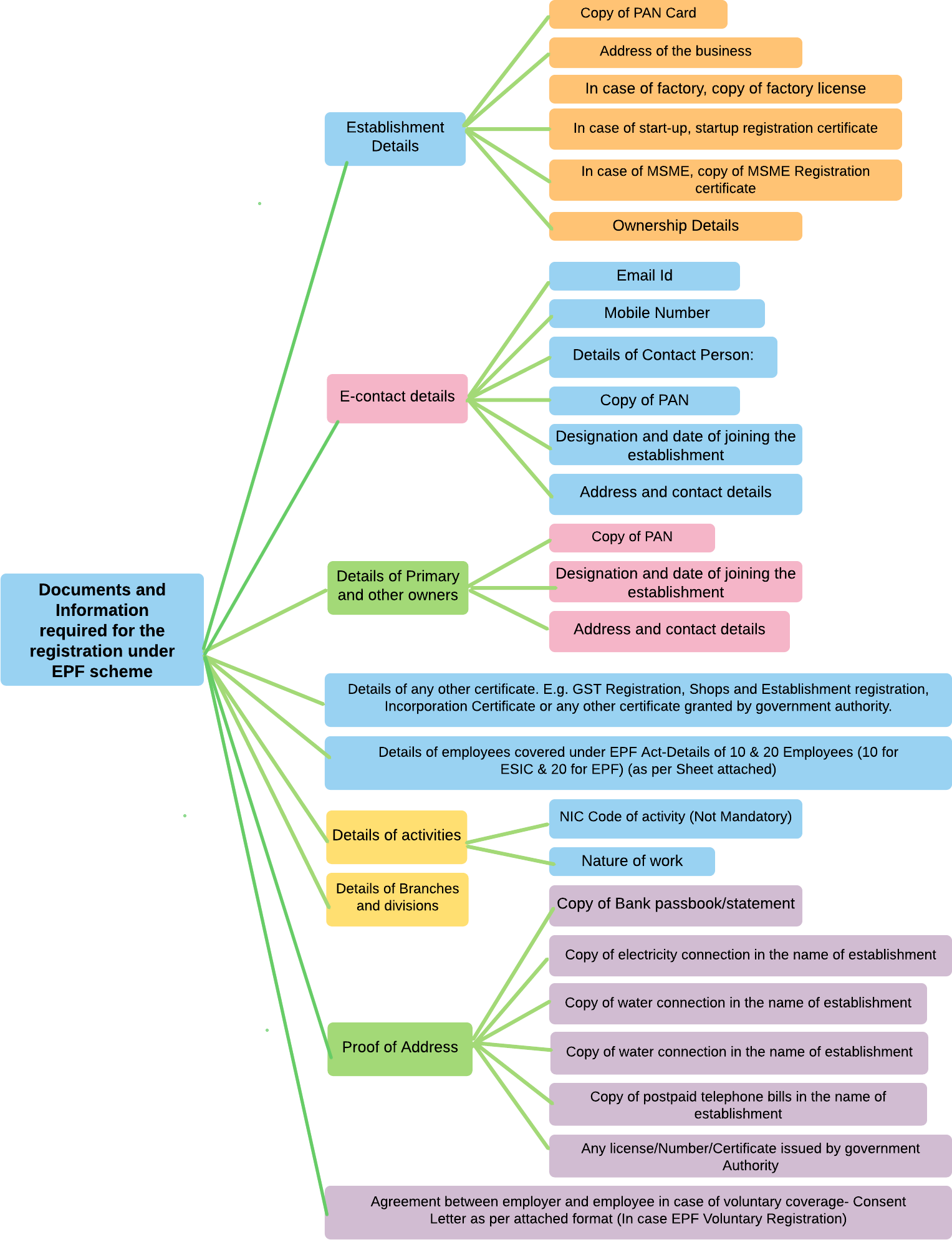

EPF Registration ProcedureThe employer must register the establishment online. With the convenience of online registration the employer can register the establishment by providing the following details:

Establishment details- The establishment details to be provided are the Name of the establishment, Address, Incorporation Date, PAN and Type of establishment

- If the establishment is a factory then the details to be provided are the Factory License Number, Date of License and Place of issue of License.

- If the establishment is an MSME then MSME registration details to be provided.

- If the establishment is registered under Startup India, then the Startup India registration details are to be provided.

The employer must provide email id and mobile number of the authorized person.

Contact PersonEmployers must provide details of the contact person like a manager. The details required are: Name, Date of Birth, Gender, PAN card, Designation date of joining and address details.

IdentifiersThe identifiers are the license information that the employer needs to provide.

Employment detailsThe employment details required to be provided are the Employee strength, Gender, Type of activities, Wages above limit and Total wages.

Branch/DivisionBranch details such as name/premise number, LIN (Labour Identification Number) and address.

ActivitiesThe employer needs to enter the NIC Code (National Industrial Classification) and select the nature of business and the activities included from the drop down lists available.

Steps for EPF Registration for Employers- New Registration

Visit the EPFO Website

To register the organisation, the employer will need to visit the EPFO portal, which is https://www.epfindia.gov.in/site_en/index.php

and click on the option that says, ‘Establishment Registration’.

Select Establishment Registration

Clicking on ‘Establishment Registration’ will lead you to the next page, which is

https://registration.shramsuvidha.gov.in/user/register, where the manual can be downloaded. The user manual must be read

completely by a new user before registration.

Select Download Manual

Click on ‘Sign Up’ Button.

Select Sign-up Button

Clicking on ‘Sign Up’ will ask for the Name, Email, Mobile Number, and Verification Code to be filled. After these details are filled,

click on ‘SIGN UP’ to create your account.

Enter Basic Details

There will be an option called ‘Registration for EPFO-ESIC’

The next page will give you an option called ‘Apply for New Registration’. Clicking on that will give two options called ‘Employees’ State Insurance Act, 1948’ and ‘Employees’ Provident Fund and Miscellaneous Provision Act, 1952’, which can be checked and then click on the ‘Submit’ button

Apply for New Registration-

This leads you to a page where the details of the employer such as Establishment Details, eContacts, Contact Persons, Identifiers,

Employment Details, Particulars of workers, Branch/Division, Activities, and Attachments are mentioned. All mandatory details that

must be filled under each section are displayed with a red asterisk.

The summary of the registration form can be viewed on the dashboard.

Click on the ‘Submit’ button to submit the registration.

Click on Submit Button

This is followed by the employer’s Digital Signature Certificate (DSC) registration. For a fresh EPF registration application, DSC

registration is mandatory.

Attach DSC

After filling all the “Registration Form for EPFO” and attaching the relevant documents, the employer’s Digital Signature Certificate (DSC) is to be uploaded and attached to the form. Once, the DSC of the employer is uploaded, the employer will receive a successful completion of registration form message and an email from Unified Shram Suvidha Platform with a confirmation that theEPFO registration has been completed.

Employees’ Provident Fund Registration-For already registered users

To register with EPF scheme go to the Employee Provident Fund Organisation (EPFO) websitehttp://www.epfindia.gov.in/site_en/index.php.

Go to the section of ‘Establishment Registration’ that opens up a new page with ‘Instruction Manual’. It will explain the process of Employer Registration, followed by registration of DSC [Digital Signature Certificate] of the Employer which is a prerequisite for fresh application submissionBefore registering, you will be provided with the instruction manual and read the details carefully

For already registered users log in to the portal using your credentials- username and password. The instruction manual will appear describing the procedure followed by Digital Signature Certificate (DSC).

Click on “I have read the instruction manual” and proceed to fill up all the details to register.

An email link and pin will be sent to your given email address and phone number, clink on the link to activate your email address and phone.

Upload the required documents, to get yourself registered. Those who are already registered can log in using their Universal Account Number (UAN)

EPF UAN Activation

To activate UAN, you must have your Universal Account Number and PF member ID with you.You need to visit the EPF Members (Employees) Login to EPF website of EPF e-SEWA/EPF Members Portal and on the right side, you have the option to login using UAN. However, UAN must have been activated earlier. Universal Account Number (UAN) is a 12 digit number which is provided to each member of the Employees’ Provided Fund Organization (EPFO) through which he can manage his PF accounts. It helps the person to get all Provided Fund (PF) information in one place irrespective of the organization he works for. With the help of UAN, the employee can easily withdraw and transfer funds.

In order to activate your UAN, follow the steps given below:

Step 1: You need to visit the member website of EPF i.e. EPF e-SEWA/EPF Members Portal

Step 2: On the right corner below, you will find the option of ‘Activate UAN’ and click on it

Step 3: As the new dashboard opens up, enter either UAN, PAN, Member ID or Aadhar and other details as Name, Birth date, etc. according to EPFO records

Step 4: Enter the ‘captcha’ code and get an authorization PIN on your registered mobile with EPFO

Step 5:Use the One Time Password (OTP) to validate and activate the UAN online

Step 6: Another message will be sent to confirm activation of the UAN

Step 7: Once UAN is activated, you can log in using it to check the status of the Provident Fund

Step 1: Visit EPF Members Portal and log in using UAN & Password

Step 2: As the new page opens up, under the section of ‘Manage’, click on KYC from the dropdown menu

Step 3: Update the details like name and number of PAN, Aadhar, Bank documents, etc.

Step 4: Save it and it will show as Pending KYC as long as it is verified from the other end

- Visit the EPFO e-SEWA portal.

- Go to the ‘Manage’ section and click on ‘Contact details’ in the drop-down menu

- Click on ‘Change mobile number’.

- Then enter the new mobile number and re-enter it.

- Next, to authorize this information, click on ‘Get authorizations PIN’

- . Enter the OTP received on your mobile number and click on ‘Save changes’ to complete the process.

Steps to check EPF Balance

Step 1:Visit EPF’s website at www.epfindia.gov.in

Step 2: Go to ‘For Members’ in the “Our Services” section

Step 3: Click on the ‘Member Passbook’ option

Step 4: Now enter your ‘UAN’, password and captcha code and login to your EPF account

Step 5: Select the ‘Member ID’ to view your passbook

Step 6: Your passbook will be displayed with complete details in the document

Step 7: The member can also check his EPF balance by sending an SMS to ‘7738299899‘ in the format

EPFOHO

Different EPF forms are mandatory for all activities that employees wish to undertake in their accounts; the activities include registration, withdrawal, and transfer of PF, availing loans from an existing EPF account or for any other reason.

| EPF Form | Use of the EPF Form |

|---|---|

| Form 31 | EPF Withdrawal |

| Form 14 | Buying LIC Policy |

| Form 10D | For claiming monthly pension |

| Form 10C | For claiming withdrawal benefits/scheme certificate of EPS |

| Form 11 | EPF Account Transfer |

| Form 19 | Final Employees’ Provident Fund Settlement |

| Form 20 | EPF Final settlement in case of death of the employee |

| Form 2 | Declaration and nomination form for EPF & EPS |

| Form 5 IF | Claim as per EDLI scheme |

| Form 15G | To save TDS on the interest income on EPF |

| Form 5 | New employees registering for EPF and EPS |

| Form 11 | Auto transfer of EPF |

PF Payment Online

Employee Provident Fund Scheme is one of the most useful employee beneficial schemes introduced by Ministry of Labor. It is one of the ideal retirement funds. It is a type of savings account where both employer and employee contribute an equal amount at regular intervals. Such contribution can be made only by those employers who are registered and employees of registered employers. Employer registration can be either through statute mandate or voluntary.

As per the PF Act, every company/organization employing more than 20 individuals, including employees who are on contract, is mandatorily required to register under PF Act. Once the PF Act is applicable, the employer’s organization continues to be governed by the PF Act even if the number of employees falls below 20 at any time.

Further, it is not mandatorily apply to all employees of registered establishment. Only such employees earning up to 15,000 are eligible to be covered under the PF Act and can make contribution. Both employer and employee, who are not mandated by PF Act, can voluntarily register and contribute for PF.Though contribution to PF account is made both by employer and employee, payment is to be made to PF account by employer who is registered with PF Act.

From September 2015 it is mandatory for all establishments to pay PF online. Online PF payment can be made by the employer either on EPFO website or through authorized bank website (if bank allows direct payment through their website) in which employer has an account and net banking.

Presently EPFO has tie up arrangement with 10 banks to collect EPFO dues and banks are SBI, PNB, Indian Bank, Bank of Baroda, HDFC Bank, ICICI Bank, Axis Bank and Kotak Mahindra Bank.

In case the employee’s PF contribution was deducted but not deposited by the employer, it will not be allowed as a deduction for the employee with effect from A.Y. 2021-22. The government has decided to retain the EPF interest rate of 8.5% for the financial year 2020-21.

ECR stands for Electronic Challan cum Return. This is an electronic monthly return to be uploaded by the employers through the Unified Portal.

The return will have member wise details of the wages and contributions; including basic details for the new and existing members (members who have joined or have left service in the wage month for which the return is uploaded). The approval of uploaded ECR will result in the generation of a Challan using which the employer has to remit the dues in the designated branches of SBI. In this way, each ECR will be linked with a remitted Challan and the ECRs uploaded but not remitted will lapse after 12-15 days of the generation of the challan.

The monthly upload of ECR will relieve the employer from manual filing of returns; both monthly and annually. If you upload the ECR, there is no need to file Forms 5/10/12A, 3A, and 6A.The upload of ECRs that are backed with remitted Challan in the EPFO application will result in the updating of member balances on a monthly basis. This information will be shared with the members through the Know Your PF Balance link.

Employers will get the confirmation of payment through SMS instantly. The members’ accounts will be credited with the contribution on monthly basis. Employers can view the annual accounts slip. For earlier years employers can request for the annual slips through this portal.

Step By Step Process to File ECR (Electronic Challan cum Return)

Login to unified portal of EPFO using your Electronic Challan cum Return (ECR) portal credentials https://unifiedportal-emp.epfindia.gov.in/epfo/. Login to EPFO portal using your ECR portal credentials: Once logged in, you can check the details of Establishment Name, Establishment ID, Exemption Status (PF, Pension, EDLI), Establishment Address and PF office.-

Ensure PF details of establishment such as establishment ID, Name, address, exemption status, etc. shown are correct. From ‘Payment’ option drop down select ‘ECR upload’ i.e. To upload ECR, go to Payments tab >> ECR [UPLOAD]

On next screen, i.e. ECR File Upload, click on ‘ECR Help File’ to view the ECR file format To upload the ECR, Select ‘Wage Month’, ‘Salary Disbursal Date’, Rate of contribution and upload ECR text file

Select your ECR text file to be uploaded. An ECR text file appears. Select the remaining fields like File Type (Select ECR), Contribution Rate % (Default value is 12%), add comment, and click on Upload Button:

Uploaded ECR file will be validated for predefined conditions and a screen will appear with a message ‘File Validation Successful’. If ECR file is not validated, error will throw up i.e. if uploaded ECR file fails, you will get an error message. Correct the ECR text file for the specified format and upload again till it is successfully validated.

Once uploaded, the file will be validated by the portal against the pre-defined conditions. Once validation is

successful, you can see the following screen with ‘Validation Successful’ message: Click on Verify button to

generate TRRN (Temporary Return Reference Number).

In the same page TRRN generated will be displayed for the uploaded ECR file. Click on ‘Verify

Generate ECR summary sheet by clicking on ‘Prepare Challan’ button.

On the next screen, you can adjust “Total EDLI Contributions (ER Share A/C 21)” (if required), enter Administration & Inspection Charges for “Total EPF Charges (A/C 2)” & “Total EDLI Charges (A/C 22).” Once done, click on ‘Generate Challan’ Button.

Select payment mode as ‘online’ and choose from any of the banks appearing in drop down menu and click on ‘continue’. This action will take you to your bank’s internet banking login website where you need to login and make payment through net banking

Presently EPFO has tie up arrangement with 10 banks to collect EPFO dues and banks are SBI, PNB, Indian Bank, Bank of Baroda, HDFC Bank, ICICI Bank, Axis Bank and Kotak Mahindra Bank.

On successful payment, Payment/Transaction-id will be generated and e-Receipt for transaction confirmation will be populated. You can also download Acknowledgment File and Receipt File under “In-Process Challan List”. The finalized ECR (Electronic Challan-cum-Receipt) will be updated at EPFO Portal.

Provident Fund (PF) Due Dates

The PF will be deducted from every employees’ salary, and the payment due date is within the 15th of the following month. E.g., if you want to deposit the PF contribution for June, then as an employer you should clear all the payments before the 15th of July. Payment and filing for the PF return date are probably the same, and you can process it at the same time.

Therefore, the due date of the PF return is the same as the payment date, and that is before the 15th of the following month. The PF annual return due date is 25th April of the following year.

Late Fees/Interest- Delay in the deposition of Provident Fund: InterestThe person who fails to complete the payment within the given deadline shall be responsible for paying 12% per year interest for each day he has delayed.

PenaltyThe EPFO has mentioned some charges that will apply to the late payment of the Provident Fund deposit. Here are the charges you shall look into

| Period of Delay | Penalty |

|---|---|

| Delay upto 2 months | 5% interest per annum |

| Delay of 2-4 months | 10% interest per annum |

| Delay of 4-6 months | 15% interest per annum |

| Delay of more than 6 months | 25% interest per annum which can’t exceed 100% at a time. |

Further, to promote the timely payment of ESI and PF to employees’ accounts, the income tax act also provides for disallowance of PF and ESI deposited after the due date. Accordingly, employers shall not get the deduction of EPF or ESI deposited after the due date under Income tax and they will end up paying income tax on it.

Steps to file EPF return

Download the list of Active Employees:

- After generating the UANs and marking exited employees, the employer should download the list of active employees from EPFO portal and match the employees from your PF calculation sheet to active employees on portal so that no employee will be left out from the return.

- To download the list of active employees: Login into EPFO Portal > Go to Dashboard > List of Active Members

- Click on Search and the List of Active Members will appear

- Download the list from Export to Excel option. Cross verify the downloaded sheet with your PF calculation sheet to match the employees

Download ECR file

- For filing the return, the employer has to fill the ECR sheet provided by EPFO.

- To download the ECR sheet: Go to Payments > Select ECR/Return Filing option > Select ECR Upload

- The ECR Upload screen will open. Select Download ECR File option. Enter the month you are filing the return for and select file type from ECR or Arrear option. If you are filing a monthly return then select ECR option as a file type and if you are filing return for an employee who you missed while filing monthly return, then select Arrear as a file type. Click on ECR file download option.

Prepare the ECR sheet

- You are required to fill all the details in downloaded ECR sheet. UAN number and Member Name fields will be pre-filled. Add the gross wages of employee from the salary statement in Gross Wages column. In EPF wages, add the basic wages + dearness allowance of employees. Next column is EPS Wages. The EPS Wages are calculated on EPF wages. EPS wages will be equal to EPF wages but maximum EPS wages are 15,000/- Even if the EPF wages for certain employee are 22,500/- his EPS wages will be 15,000/- only.

- The next column is EDLI Wages i.e. Employees Deposit Linked Insurance wages. EDLI wages are equal to the EPS Wages. EPF Contribution Remitted is EPF contribution. In EPF Contribution column, you have to enter the 12% amount of EPF wages because EPF contribution is 12% of basic + DA of an employee’s salary. Enter the 8.33% of EPS wages in EPS Contribution Remitted column and difference between EPF contribution and EPS contribution in EPF EPS Diff Remitted column. In NCP (Non Contributing Period) Days column add the number of days the employee was absent in a month.

- After filling all the details into sheet, calculate employer’s contribution. The employer’s contribution is also 12% but is it divided as 3.67% into EPF, 8.33% into EPS, 0.50% into EDLI and 0.50% into PF admin charges. These calculations will be needed while preparing challan. Refer to the image below for employer’s contribution calculation.

Prepare Text File

- Copy all the details filled in the downloaded ECR sheet and paste them in a new excel sheet as value. Save this file as a .CSV (Comma delimited) format.

- Open the saved .CSV file in Notepad. Press Ctrl + H and replace all commas ( , ) with # ~ # and save the file.

Generate Challan

- Go to the Payments option on EPFO portal and select ECR Upload option. ECR Upload screen will open. Click on ECR File Upload option.

- Fill in the details shown on ECR upload screen. In Wage Month column, select the month you are uploading the return for. Enter the salary disbursal date. Upload the created .txt file in Select File option. Select the file type either ECR or Arrear. Select the contribution rate. Add remark and press on Upload.d

- After uploading the file, a text box will be shown on the screen if you have filled all the details correctly i.e. validation successful

Download the ECR Statement

- Download the ECR statement from Draft ECRs column. Check all the details from statement. If the details in statement are correct, proceed further to verify the file.

Verify ECR

- To verify the uploaded ECR file, click on Verify option from Draft ECR’s. If you are sure that you have filled everything correctly, click on verify, and press OK option on the dialogue box asking if you are user that you want to verify.

- Verified ECR file will show in In Process ECRs list located just below the Draft ECRs. Select Prepare Challan option in Action Column.

ECR Summary

- After selecting prepare challan option, ECR Summary screen will open. Here you will see all the details you filled in ECR file. These details include name and ID of your establishment, wage month, return month, total number of UANs, total gross wages, EPF wages, EPS wages, EDLI wages and NCP days. All the calculations in these fields will be automatically filled from the uploaded ECR file.

Administration Charges

- In the Details column, total EPF contribution, EPS contribution, difference between EPF & EPS and total EDLI contribution by employer will be pre-filled. You have to define the Administration charges in Total EPF Charges (A/c 2).Administration Charges should be 500/- minimum.

Employer Details

- In the Employer Details column, add the total number of employees in a month, number of excluded employees and gross wages of excluded employees and press Generate Challan button.

- Click on 'create a challan' to generate challan.

Finalize Challan

- A dialogue box stating successful challan generation will appear. We are required to verify and finalize the challan details for payment. Click on the Finalize option. The EPFO portal will ask if you are sure to finalize the challan. Press OK if you are sure.

Payment

- After finalizing the challan, find your challan TRRN from the In-Process Challan List and click on Pay. A Challan Payment screen will open.

- Select your bank, select Continue option and make payment through internet banking.

| Employee Centric Services | View Passbook Raise Claims Track Claims Get Remittance Details by Establishment ID Get TRRN Status |

| EPF General Services | Search Establishment Search EPFO Office Know your claim status Account Details on SMS Account Details on Missed Call |

| Pensioner Services | View Passbook Update Jeevan Pramaan |

| eKYC Services | Aadhaar Seeding |

The EPF account consists of contributions from the employer and employee. However, the money in an EPF account cannot be withdrawn at whim.

PF Withdrawal Rules 2021

The Employees’ Provident Fund Organization (EPFO) has revised several of its rules regarding withdrawal from the Provident Fund (PF) account in 2021. According to the new rules, PF account holders can withdraw money equivalent to three months of their basic salary plus dearness allowance or 75% of the net balance in their PF or EPF account, whichever is lower. This will be taken as a non-refundable deposit. These withdrawal claims can be raised online. Online claims are stipulated to be settled within 3 working days while offline claims can take up to 20 days for settlement.

| Reasons | Eligibility | Withdrawal Limit |

|---|---|---|

| Housing Loan for construction or addition of house/purchase of site/flat | Minimum 60 months of service | Up to of 36 months of his/her basic along with DA/ the total of employee and employer shares with interest/ the total cost of the house |

| Marriage of self/son/daughter/brother/sister or for post matriculation education of children | Minimum 84 months of service | Up to 50% from the EPF account |

| One year before retirement | Should be above 54 years of age | Up to 90% of his/her EPF amount |

| Medical expenses/Natural Calamity/purchase of equipment by physically handicapped/closure of factory/cut in electricity in establishment | No minimum service tenure | Up to 6 months of his/her basic and DA/ the entire contribution |

The EPF account consists of contributions from the employer and employee. However, the money in an EPF account cannot be withdrawn at whim.

- Money from the EPF account cannot be withdrawn during employment, unlike a bank account. EPF is a long-term retirement savings scheme. The money can be withdrawn only after retirement.

- Partial withdrawal from EPF accounts is permitted in the case of an emergency such as medical emergency, house purchase or construction, and higher education. Partial withdrawal is subject to limits depending on the reason. The account holder can request online for partial withdrawal.

- Although the EPF corpus can be withdrawn only after retirement, early retirement is not considered until the person reaches 55 years of age. EPFO allows withdrawal of 90% of the EPF corpus 1 year before retirement, provided the person is not less than 54 years old.

- The EPF corpus can be withdrawn if a person faces unemployment before retirement due to lock-down or retrenchment.

- The EPF subscriber has to declare unemployment in order to withdraw the EPF amount.

- As per the new rule, EPFO allows withdrawal of 75% of the EPF corpus after 1 month of unemployment. The remaining 25% can be transferred to a new EPF account after gaining new employment.

- As per the old rule, 100% EPF withdrawal is allowed after 2 months of unemployment.

- EPF corpus withdrawal is exempted from tax but under certain conditions. Tax exemption on EPF corpus is permitted only if an employee contributes to the EPF account for 5 continuous years. The EPF amount is taxable if there is a break in the contribution to the account for 5 continuous years. In that case, the entire EPF amount will be considered as taxable income for that financial year.

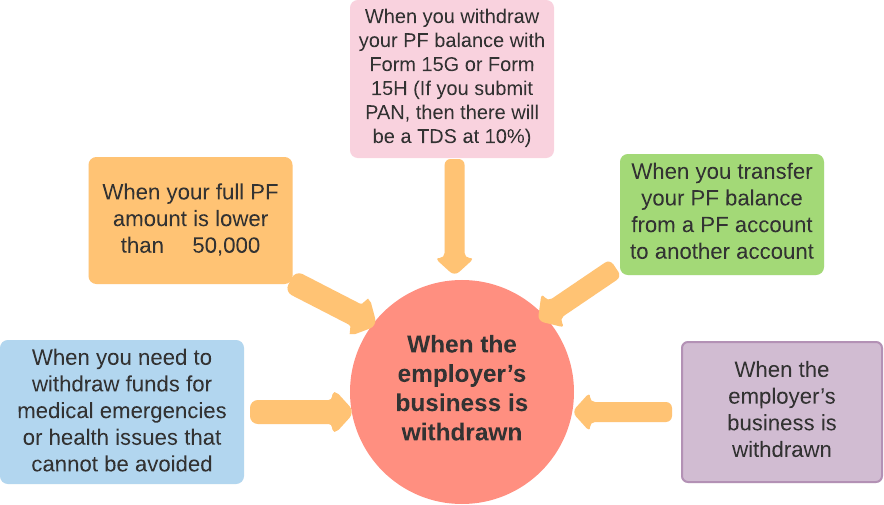

- Tax is deducted at source on premature withdrawal of the EPF corpus. However, if the entire amount is less than 50, 000, then TDS is not applicable. Keep in mind, if an employee provides PAN with the application, the applicable TDS rate is 10%. Otherwise, it is 30% plus tax. Form 15H/15G is a declaration form, which states that a person's total income is not taxable and thus, TDS is avoidable.

- An employee does not have to await approval from the employer for EPF withdrawal anymore. It can be done directly from the EPFO, provided the employee's UAN and Aadhaar are linked, and the employer has approved it. EPF withdrawal status can be checked online.

Steps for EPF Withdrawal Online

Employees can make a PF withdrawal claim on the EPFO member portal by following the steps mentioned below. As already mentioned, if the employee has seeded his/her Aadhaar card details with one’s UAN account, they do not require the attestation of their employer to make a PF withdrawal.

Sign in to the UAN Member Portal with your UAN and Password.Visit the EPFO member portal.Choose the “For Employees” option under the “Our Services” tab.

On the new webpage click on the “Member UAN/Online Service (OCS/OTCP)” option under the “Services” tab of the “For Employees” page

This will redirect you to a new webpage. Log in to the portal using your UAN, password, and the Captcha code.

Click on the “KYC” option under the “Manage” tab.

You will be redirected to a new webpage. Scroll down to the bottom of the page to find the “Digitally Approved KYC” section and check your KYC details. Ensure the details are correct.

Click on the “Online Service” tab from the top menu to proceed with the withdrawal if all the KYC details are correct.

Click on the “CLAIM (FORM-31, 19 & 10C)” option from the drop down menu

You will be redirected to a new webpage with an automatically generated “ONLINE CLAIM (FORM 31, 19 & 10C)” form.

You will be required to enter the Last 4 digits of your registered bank account number and verify the same.

After the verification of the bank account, a “Certificate of Undertaking” will be generated. Click “Yes” on the certificate pop-up to proceed.

Click on the “Proceed for Online Claim” option when prompted.

For online fund withdrawal, select the “PF ADVANCE (FORM - 31)” option from the drop-down menu provided next to the “I want to apply for” option.

A reason for claim has to be selected from the drop-down options provided next to the “Purpose for which advance is required” option. It is worth noting that all options for which the employee is not eligible for withdrawal will be mentioned in red. The fields provided for the address of the employee and the amount for advance is also required to be filled up.

Click on the checkbox at the end of the page and submit your withdrawal application.You might be required to upload certain scanned documents (depends on the nature of withdrawal).

Once the employer approves the withdrawal request, the withdrawal amount will be withdrawn from the EPF account and will be deposited to the respective bank account. Once the claim has been settled, you will receive an SMS notification on your registered mobile number.

Although no formal time limit has been provided by the EPFO, the money usually gets credited within 15-20 days.

Steps to enter exit date and withdraw your PF easily

If the withdrawal of your Provident Fund (PF) is getting delayed, then it may happen due to the exit date not being mentioned. Hence, in order to avoid this, The Employees’ Provident Fund Organization (EPFO) has come up with a facility in the Unified Portal where the employee can enter the date of exit from the previous employer by himself. Prior to this only the employer could enter the exit date, but now even employees can enter the date of exit.

You can change the exit date by logging to the UAN portal using your Unified Account Number (UAN) and password. However, you must check whether the exit date is mentioned by clicking on ‘Service History’ under ‘View’ on the top panel.

Given below are the steps you will have to follow in order to enter the Exit Date:

- Log in to your UAN portal using your Unified Account Number and Password

- On the top panel, click on ‘Manage’ and click on ‘Mark Exit’ located under it

- From the drop-down option choose the employer

- You will be directed to a new page where you will have to enter your date of birth, date of joining, and date of exit. Mention the date of exit as the one mentioned in your resignation letter if your exit date is before the 15th day of the month

When you make PF withdrawals, you can enjoy tax exemptions. However, this is applicable only when you make a withdrawal after offering 5 years of continuous service. It is also determined by the tax slab that is applicable to you. If you withdraw your PF balance before the completion of 5 years, then tax deducted at source (TDS) or tax will be applied on your funds.

However, no tax will be levied on EPF withdrawals before 5 years in certain cases depending on the situation. They are:

Transfer EPF Online

Step 1: Log in to the EPFO members’ portal using your UAN and password

Step 2: Go to the ‘Online Services’ tab on the main menu of the home page and select ‘Transfer Request’ to generate an online transfer request

Step 3: A new dashboard displaying all your personal details will be shown. Verify all of that like DOB, EPF and date of joining, etc. so as to claim the process

Step 4: Once you verify, go to Step 1, select the option of previous or present employer and then provide the details of the previous employer through which you want to claim

Step 5: Submit the details, an OTP will be sent to your registered mobile number. You need to authenticate your identity by entering the OTP, then only the request will be submitted and an online filled-in form will be generated. You need to sign the form and send it to your present or previous employer

Step 6: The employer will also get an online notification about the EPF transfer request. EPFO Office will process the claim only after employer digitally forwards the claim to the EPFO after verifying your employment details

Post submission of the request, you can check the status of your EPF transfer claim under the ‘Track Claim Status’ menu, which is under the ‘Online Services’ menu

You can easily link your Aadhaar to your EPF account online. Follow the steps given below:

Step 1: Visit EPFO member portal and login using your credentials

Step 2: Go to the ‘Manage’ option from the menu bar

Step 3: From the drop-down list, select ‘KYC’ option

Step 4: Select ‘Aadhaar’ from the list of documents

Step 5: Enter your Aadhaar Number and Name as per Aadhaar

Step 6: Save and proceed

Step 7: Your Aadhaar data will be verified with UIDAI’s data

On successful approval, your Aadhaar will be linked with your EPF account and you can see the Verified status written against your Aadhaar details.

EPF Tax Rules

EPF deposits and interest was completely exempt from tax until the year 2020. However, in Budget 2021, the government has announced that if the deposit in EPF and VPF (Voluntary Provident Fund) exceeds 2.5 Lakh in a financial year, then the interest earned on the contributions above 2.5 Lakh will be taxable.In case no contribution is made to the EPF account by the employer, then interest component will be exempt up to the deposit of 5 Lakh in the said financial year.

EPF on Umang App

| Employee Centric Services | View Passbook Raise Claims Track Claims Get Remittance Details by Establishment ID Get TRRN Status |

| EPF General Services | Search Establishment Search EPFO Office Know your claim status Account Details on SMS Account Details on Missed Call |

| Pensioner Services | View Passbook Update Jeevan Pramaan |

| eKYC Services | Aadhaar Seeding |

Aadhaar Card Necessary for EPF Account Nominees

According to the new rules released by the Employees’ Provident Fund Organization (EPFO), submitted the Aadhaar card number of the nominee is mandatory for e-nomination of your provident fund account. The newly established e-nomination function on EPFO which not just requires the subscribers to link their Aadhaar card with the account but also mandates the submission of Aadhaar card number of the nominee. Apart from the Aadhaar card number, scanned images, Date of Birth and mobile number are some of the important details of the nominee/s which requires to be provided duly. However, the submission of bank details of the nominee remains optional.

Online Grievances Portal for PF Withdrawal

If you want to register any grievance regarding the services provided by the EPFO, you can visit the EPF grievance management system online. In this system, you can file a grievance, send a reminder, check the status of your complaint or grievance, upload your grievance document, or even change your password.

How to register a grievance?- You will have to go the EPFO Grievance Management System and click on ‘Register Grievance’.

- You will then see a grievance registration form. Here, you will have to fill all the required fields accurately

- You will need to choose your status from the drop-down option

- Next, you will have to key in your PF number, your establishment, address of establishment, name of complainant, contact details, grievance details, etc. You can then enter the captcha code and click ‘Submit’.

You can register a grievance when you face issues associated with:

- Return of cheque or misplacement of cheque

- Scheme certificate (10C)

- Transfer of your PF accumulations (F-13)

- Settlement of your pension (10-D)

- Provision of PF balance or PF slip

- Others

You can file a grievance online and then check its status on the portal itself. In case your complaint is not resolved within the stipulated period of time, you can send a reminder to them by clicking on ‘Send Reminder’. Here, you will need to enter your grievance registration number and password (if you have any).

Types of PF Withdrawals

Subscribers can make three different types of PF withdrawals on the EPFO member portal. They are:

Subscribers can make the above-listed withdrawals on the EPFO member portal with the attestation of their employer if they have seeded their Aadhaar card details with their UAN.

PF Withdrawal Rules

In order to ensure that employees continue to be enrolled in the scheme and avoid making withdrawals from their PF corpus and instead save it for the future or for retirement, EPFO has listed a number of PF withdrawal rules. They are as follows

All withdrawals made before completion of 5 years of continuous service are subject to tax. Withdrawals after completion of 5 years of continuous service in the EPF are tax-free.

In case the employee was terminated or is unemployed as a result of ill-health and so on, withdrawals will not attract tax.

If the employee makes a withdrawal before the completion of 5 continuous years in the scheme, the principal amount as well as the interest accrued, is subject to tax. That said, the amount will be taxable in the current financial year.

For withdrawals before completion of 5 continuous years towards the scheme, the employee will be taxed 30% of the principal amount and the interest accrued if he/she has not submitted their PAN to the EPFO authorities. If the employee has submitted his/her PAN details to the EPFO authorities, 10% TDS (tax deducted at source) will be applicable

Funds transferred from one’s PF account towards the National Pension Scheme (NPS) will not attract tax when one makes a withdrawal.

If the employee shifts jobs and in the process has different PF account, it will be considered as continuous service to the scheme provided there has been no gap in contributions.

Employees have to facilitate the use of the Composite Claims Form to make a partial withdrawal or a final settlement claim.

If the employee has seeded his/her Aadhaar card details with their UAN, they can submit the Composite Claims Form to make a withdrawal directly to the EPFO without the requirement of the attestation of their employer. Those who have not seeded their Aadhaar card details with their UAN have to submit the Composite Claims Form with the attestation of their employer to make a withdrawal.

The labor ministry has announced that EPF members can now withdraw twice from their EPF account to meet the emergency expenses arising due to the Corona virus pandemic. Members can avail a non refundable withdrawal of up to 75% of the amount available in their EPF account or 3 months of their basic wages and dearness allowance, whichever is lower. Furthermore, EPFO is set to settle these withdrawal claims within 3 days and has also created an auto-claim settlement process for members whose KYC is complete in all respects.

Withdrawal Procedure

With the amendments made by the Employees’ Provident Fund Organization (EPFO), now subscribers to the scheme do not require the attestation of their employer to make a partial or complete withdrawal. All that the subscriber has to ensure is that his/her UAN is seeded with their Aadhaar card details. The EPFO has also rolled out the Composite Claims Form, which can be used to request for a partial or complete withdrawal. Subscribers can carry out the whole process of making a withdrawal online either on the EPFO member portal or on the UAN portal.

PF Withdrawal Claim Forms

The PF Withdrawal Claim Forms that need to be submitted to withdraw the provident fund or pension fund vary based on the age, reason for making the claim, and whether or not the employee is still in service. Earlier, Form 19, Form 31, and Form 10C were used to make withdrawals. But recently, a composite claim form has replaced the above-mentioned forms. The forms that required the UAN details of the employee have now been replaced with a composite claim form that requires the Aadhaar details of the employee.As mentioned earlier, the PF claim form that needs to be submitted varies based on certain criteria.

1) When an employee is still under service

- If he/she wishes to take an advance from the PF account, the composite claim form (Aadhaar/Non Aadhaar) has to be submitted.

- If he/she wishes to finance his/her LIC policy through the PF account, Form 14 has to be submitted.

- If he/she has crossed 58 years of age and wishes to claim the pension fund.

- Form 10D should be applied for a monthly pension if 10 years of eligible service has been completed.

- The composite claim form (Aadhaar/Non-Aadhaar) should be submitted if 10 years of eligible service has not been completed.

2. When an employee switches the job and wishes to transfer EPF account, Form 13 should be applied

- When an employee leaves an establishment and doesn’t join another

- He/she can make a PF and pension fund claim using the composite claim form (Aadhar/Non Aadhar)

- . Is above the age of 58, and has completed 10 years of eligible service, he/she can make a PF claim using the composite claim form (Aadhaar/Non-Aadhaar) and a pension claim using Form 10D

3. When an employee leaves an establishment due to a physical disability

- He/she can make a PF claim using composite claim form (Aadhaar/Non-Aadhaar)

- He/she can make a pension claim using Form 10D

- . Is above the age of 58 and has not completed 10 years of eligible service, he/she can make the PF and pension claim using the composite claim form (Aadhaar/Non-Aadhaar).

4. When an employee is deceased while in service

- Before the age of 58 while still in service, the nominee/heir/beneficiary can apply for the PF settlement using Form 20, monthly pension using Form 10D, and EDLI (Employees’ Deposit Linked Insurance) amount using Form 5IF.

- After the age of 58 and had completed 10 years of eligible service, the nominee/heir/beneficiary can claim the PF using Form 20, the pension using Form 10D, and the EDLI amount using Form 5IF.

- After the age of 58 and had not completed 10 years of eligible service, the nominee/heir/beneficiary can make the PF settlement using Form 20, withdraw the pension using the composite claim form (Aadhaar/Non-Aadhaar), and claim the EDLI amount using Form 5IF.

5. When an employee is deceased

- Before the age of 58, the nominee/heir/beneficiary may claim the PF amount through Form 20 and pension amount through Form 10D.

- After the age of 58 and had completed 10 years of eligible service, the nominee/heir/beneficiary can claim the PF amount using Form 20, and the pension amount using Form 10D.

- After the age of 58 and had not completed 10 years of eligible service at the age of 58, the nominee, heir or beneficiary can apply for a final PF settlement using Form 20 and for the pension fund using the composite claim form (Aadhaar/Non-Aadhaar).

Reasons for PF withdrawal

You can withdraw money from your EPF account to meet the financial requirements of a medical treatment, provided it meets the following conditions:

- Any major surgery in a particular hospital