Changes in Schedule III of Companies Act, 2013: An Overview

The Schedule III to the Companies Act 2013 provides general instructions for presentation of financial statements of a company under both Accounting Standards (AS) and Indian Accounting Standard (Ind AS). The Schedule III has been divided into 3 divisions:

- Division I - Applicable to Companies whose financial statements are prepared in accordance with AS

- Division II - Applicable to Companies whose financial statements are prepared in accordance with Ind AS (Other than Non Banking Financial Companies (NBFCs))

- Division III - Applicable to Non Banking Financial Companies whose financial statements are prepared under Ind AS (Newly inserted – Notification dated 11th October 2018)

Changes in Schedule III of Companies Act, 2013

The Ministry of Corporate Affairs has amended Schedule III of Companies Act 2013 on 24 March 2021 with an objective to increase transparency and provide additional disclosures to users of financial statements. These amendments are effective from 1 April 2021. Since an auditor is required to issue a true and fair view on the financial statements, the additional disclosures as prescribed in Schedule III will form part of financial statement and hence will be covered by auditor’s report.The Companies in India are required to prepare their financial statements in form of Schedule III to the Companies Act, 2013. Schedule III of Companies Act, 2013 came into force with effect from the 1st April, 2014 vide Notification S.O.902 (E), dated 26th March 2014 and subsequently amended vide Notification G.S.R. 679(E), dated 4th September 2015, vide Notification G.S.R. 404(E), dated 6th April 2016 and vide Notification G.S.R. 1022(E), dated 11th October, 2018 and very recently vide Notification G.S.R. 207(E), dated 24th March, 2021.

The recent amendment dated 24th March, 2021 to amend Schedule III to the Companies Act, 2013 read with Companies (Accounts) Rules, 2014 and Companies (Audit and Auditors) Rule, 2014 to enhance the disclosures required to be made by the Company in its Financial Statements. The main aim of the amendments in Schedule III of the Companies Act, 2013 is to improve the transparency in the financial statements of the company.

By these amendments MCA is increasing stringency in compliance and adding numerous additional disclosures in Financial Statement, Directors Report and Audit Report.In recent years, there have been substantial changes in the reporting requirement by the auditors, but no such corresponding amendments were made in Schedule-III for the preparation of the financial statements. Thus, to align the company’s financial statements in accordance with the auditor’s reporting requirements.

Majority of the amendments to Schedule III to the Companies Act, 2013 have been undertaken in response to the amendments covered in the newly issued Companies (Auditors and Report Order) 2020 and the Companies (Indian Accounting Standards) Amendment Rules, 2020. These amendments are in the form of reclassification of items items/sub items, renaming of items and additional disclosure to financial statements etc. To tune with this ICAI also revised ‘Guidance note on Schedule III to the Companies Act, 2013’.

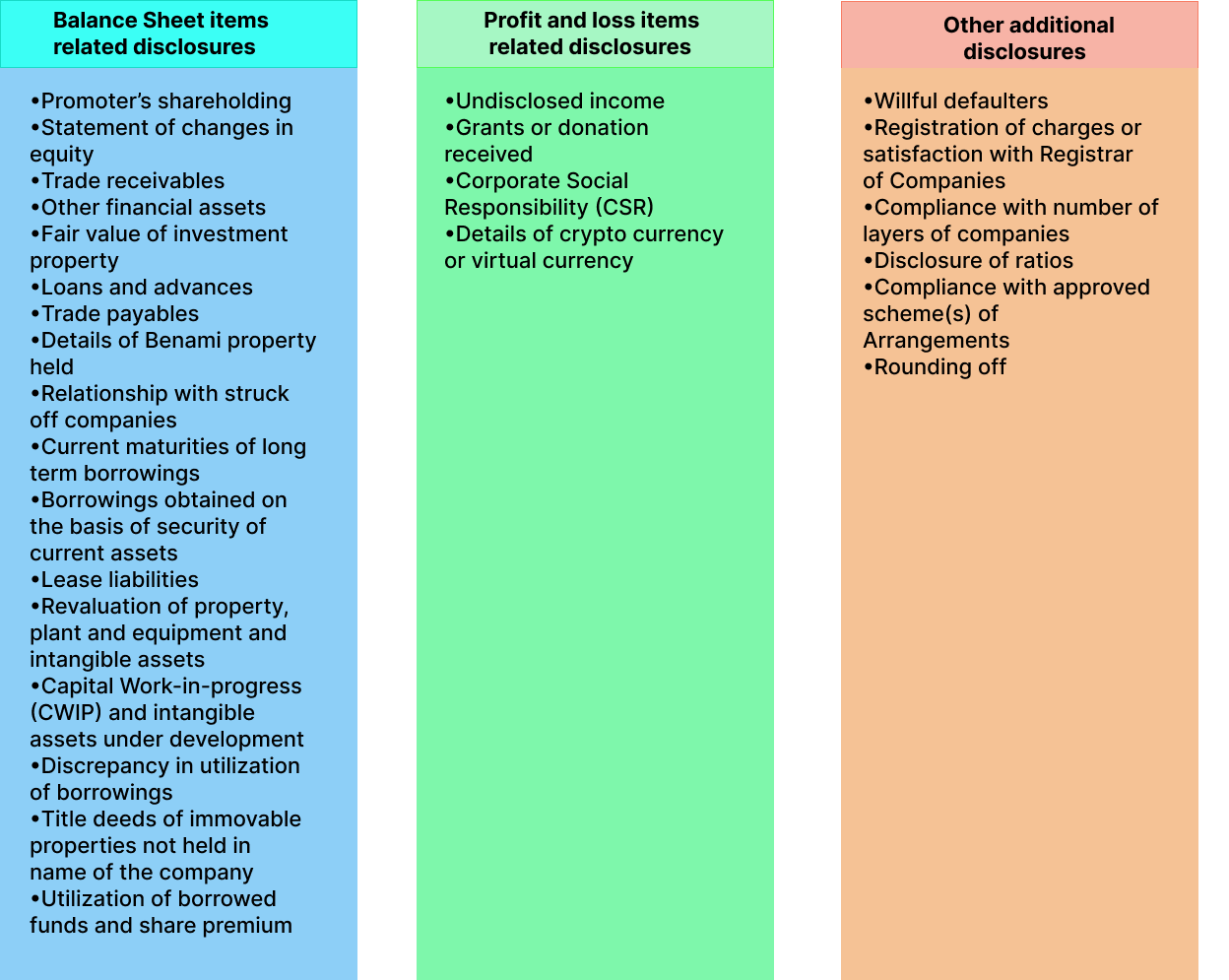

A brief snippet of the amendments in Schedule III:-- Shareholding of Promoters: As compared to earlier version, the entities shall now disclose the shares held by the promoters at the end of the financial year and % change during the year in notes to accounts in tabular format as mentioned in the Schedule.

- Rounding Off: It is mandatory for the companies to round off the figures appearing in the financial statements on the basis of ‘Total Income’. Earlier this provision was optional and round off was done on the basis of ‘Turnover’.

- Short Term Borrowings: From 1 April 2021 onwards, the current maturities from long term borrowings is required to be separately disclosed in the financial statements.

- Trade Payables Due For Payments: Gone are those days where ageing schedule for only receivables were made. From now onwards, it shall be prepared for trade payables also which are due for payment, in a tabular form, whether or not, due date of payment is specified on bill. However, unbilled dues shall be separately disclosed.

- Disclosure for Tangible and Intangible Asset: At the beginning and end of the reporting period, a reconciliation of the gross and net carrying amounts of each class of assets showing additions, disposals, acquisitions through business combinations, amount of change due to revaluation and other adjustments and the related depreciation and impairment losses or reversals shall be disclosed separately, if the changes is 10% or more in each class of asset.

- Trade Receivables outstanding: Ageing schedule shall be prepared for trade receivables in a tabular form in a manner as notified by MCA, whether or not, due date of payment is specified on bill. However, unbilled dues shall be separately disclosed.

- Borrowing from Banks and Financial Institutions: At balance sheet date, the companies shall disclose the details of those funds which were borrowed from banks and financial institutions for a specific purpose.

- Title deeds of Immovable Property: The companies have to give the details of all those immovable properties whose title deeds are not in the name of the company, except those immovable properties in which the company is lessee and lease agreement are executed.

- Loan Granted to Promoters, Directors, KMPs and the Related Parties: The company shall disclose all the loans and advances in the nature of loan granted to promoter director and KMPs and related parties, severally or jointly with any other person either repayable on demand, without specifying any terms or period of repayment.

- Benami Property: Company shall disclose all the benami property in which proceedings have been initiated or pending against the company for holding any benami property under the Benami Transactions (Prohibition) Act, 1988 and rule made thereunder, disclosures shall be made in the manner prescribed.

- Willful Defaulter: If any company is declared as willful defaulter by the bank or financial institution or any other lender then disclosures shall be made by the company in the manner prescribed.

- Ratios: Companies shall disclose the all those ratios which are prescribed and shall explain the items included in numerator and denominator for computing the above ratios. Moreover, if any change in the ratio is more than 25% as compared to the preceding year then explanation for the same shall be provided.

- Undisclosed income: Where a company has surrendered or disclosed any income under the relevant provisions of the Income Tax Act and which are not disclosed earlier shall be disclosed in the books of accounts, unless there is immune impact.

- Corporate Social Responsibility: Where a company under section 135 of the Companies Act, 2013, then disclosure shall be made in the manner prescribed in the Schedule III to the Companies Act, 2013.

- Crypto Currency or Virtual Currency: If any company has traded or invested in Crypto Currency or Virtual Currency then following disclosures shall be made in the financial statements:-

(a). Profit and loss made from crypto currencies.

(b). Amount of currency held at reporting date.

(c). Deposit or advance taken from any person for trading or investment in crypto.

On analyzing the amendments in Schedule III and CARO 2020, it can be stated that the majority of the modifications made in Schedule III and CARO 2020 are to match the two reporting frameworks and improve transparency between the company and the users of financial statements. It further enabled to reduce the risk of fraud and other unethical behavior on part of the companies.

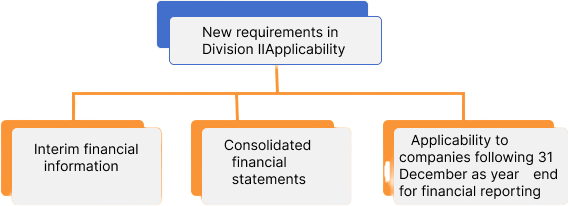

Applicability of financial reporting disclosures— amendment to Schedule III

- Full / condensed interim financial statements:

If a complete set of financial statements is presented as interim financial statements, all new disclosures are required including for comparatives. When condensed financial statements are presented as interim financial statements, necessary accounting standard disclosures as specified in Ind AS 34 that were not included in the last set of published financial statements are required to be provided. Distinction needs to be made between regulatory disclosures and those required by accounting standards. Therefore, considering the new disclosures under Schedule III are regulatory disclosures, these need not to be included in condensed interim financial statements, but may be provided voluntarily. - Quarterly and half yearly SEBI results:

SEBI Listing Obligations and Disclosure Requirements (LODR) requires Schedule III format to be used for SEBI results. Schedule III amendments make no changes in format of statement of profit and loss. However, there are a few new line items inserted or grouping is changed in the format of balance sheet. These format changes need to be made in half yearly results since SEBI format is aligned to Schedule III format. Comparative figures also need to be re-grouped / re-classified, wherever required, with appropriate notes.

Guidance note on Schedule III provided following guidance on applicability of Schedule III requirements to consolidated financial statements (CFS). Schedule III itself states that the provisions of the Schedule are to be followed mutatis mutandis to a consolidated financial statement. MCA has also clarified vide General Circular No. 39 / 2014 dated 14th October 2014 that Schedule III to the Act with the applicable Accounting Standards does not envisage that a company while preparing its consolidated financial statements merely repeats the disclosures made by it under stand-alone accounts being consolidated. Accordingly, the company would need to give all disclosures relevant for CFS only. Guidance note provided detailed guidance on many disclosure requirements to help user understand what should be furnished in the financial statements.

One may argue that above guidance may be equally be applicable to amendment made in Schedule III. MCA / Institute of Chartered Accountants of India (ICAI) should provide clarification on same to ensure consistency in application. For large groups, which have various group companies (including foreign companies), this may pose a significant challenge. Companies will need to gear up the systems and process to enable disclosures in CFS.

Applicability to companies following 31st December as year-end for financial reporting:

The notification for Schedule III amendment states that Schedule III amendment are effective from 1st April 2021 and it does not explicitly state that it would be applicable only to financial statement prepared for year beginning on or after 1st April 2021. Hence it is not clear whether Schedule III amendment would be applicable for annual financial reporting for 31st December 2021.

Amendment in Division I to schedule III to the Companies Act, 2013

- Earlier is was optional but now it is mandatory to round off the figures appearing in the Financial Statements depending upon the Total Income of the company, as given below:—

| [Total Income] | Rounding off |

| (a) less than one hundred crore rupees | To the nearest hundreds, thousands, lakhs or millions, or decimals thereof. |

| (b)one hundred crore rupees or more | To the nearest lakhs, millions or crores, or decimals thereof. |

- To tune with AS-10 “Property, Plant and Equipment” under the heading “II Assets”, under sub-heading “Non-current assets”, the item “Tangible Assets” changed to “Property, Plant and Equipment and Intangible assets”

- For Property, Plant and Equipment a reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions through business combinations, amount of change due to revaluation (if change is 10% or more in the aggregate of the net carrying value of each class of Property, Plant and Equipment) and other adjustments and the related depreciation and impairment losses/reversals shall be disclosed”

- For Intangible assets a reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposal acquisitions through business combinations, amount of change due to revaluation (if change is 10% or more in the aggregate of the net carrying value of each class of intangible assets) and other adjustments and the related depreciation and impairment losses or reversals shall be disclosed separately.”

- A company shall disclose Shareholding of Promoters* in the Notes – Share Capital, as below:

| Shares held by promoters at the end of the year | % Change during the year*** | |||

| S. No | Promoter name | No. of Shares** | %of total shares** | |

| Total | ||||

*Promoter here means promoter as defined in the Companies Act, 2013.

** Details shall be given separately for each class of shares Advertisement

*** Percentage change shall be computed with respect to the number at the beginning of the year or if issued during the year for the first time then with respect to the date of issue. ”

- Sub-item “current maturities of Long term borrowings” reclassified under “Short-term borrowings” from “Other current liabilities”.

- The following ageing schedule shall be given for Trade payables due for payment:-

Trade Payables ageing schedule

(Amount in )

| Particulars | Outstanding for following periods from due date of payment# | Total | |||

| Less than 1 year | 1-2 years | 2-3years | More than 3 years | ||

| (i). MSME (ii). Others (iii). Disputed dues – MSME (iv). Disputed dues – Others |

|||||

| Unbilled dues shall be disclosed separately; | |||||

# Similar information shall be given where no due date of payment is specified in that case disclosure shall be from the date of the transaction. Unbilled dues shall be disclosed separately;

- Sub- item “(I a) Security Deposits” reclassified under “Other non-current assets” from “Long-term loans and advances” i.e. Security Deposit – To be shown separately under other non -current assets instead of Loans and advances.

- Short Term Borrowings: From 1st April 2021 onwards, the current maturities within 12 months from long term borrowings is required to be separately disclosed in the financial statements.

- For trade receivables outstanding, both non-current and current following ageing schedule shall be given:

Trade Receivables ageing schedule

(Amount in )

| Particulars | Outstanding for following periods from due date of payment# | Total | ||||

| Less than 6 months | 6 months -1 year | 1-2 years | 2-3 years | More than 3 years | ||

| (i). Undisputed Trade receivables – considered good (ii). Undisputed Trade Receivables – considered doubtful (iii). Disputed Trade Receivables considered good (iv). Disputed Trade Receivables considered doubtful |

||||||

# Similar information shall be given where no due date of payment is specified, in that case disclosure shall be from the date of the transaction. Unbilled dues shall be disclosed separately.”

- Where the company has not used the borrowings from banks and financial institutions for the specific purpose for which it was taken at the balance sheet date, the company shall disclose the details of where they have been used.”;

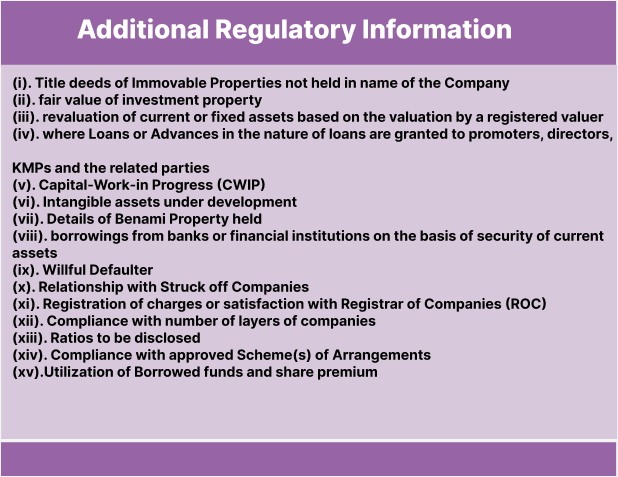

Additional Regulatory Information

- Title deeds of Immovable Property not held in name of the Company

The company shall provide the details of all the immovable property (other than properties where the Company is the lessee and the lease agreements are duly executed in favor of the lessee whose title deeds are not held in the name of the company in format given below and where such immovable property is jointly held with others, details are required to be given to the extent of the company’s share.

| Relevant line item in the Balance Sheet | Outstanding for following periods from due date of payment# | Gross carrying value | Title deeds held in the name of | Whether title deed holder is a promoter, director or relative of promoter/director or employee of promoter/director | Property held since which date | Reason for not being held in the name of the Company** |

| PPE | Land Building |

**also indicate if in dispute | ||||

| Investment property | Land Building |

|||||

| PPE retired from active use and held for disposal | Land Building |

|||||

| Others |

#Relative here means relative as defined in the Companies Act, 2013. *Promoter here means promoter as defined in the Companies Act, 2013.

- Where the Company has revalued its Property, Plant and Equipment, the company shall disclose as to whether the revaluation is based on the valuation by a registered valuer as defined under rule 2 of the Companies (Registered Valuers and Valuation) Rules,

- Following disclosures shall be made where Loans or Advances in the nature of loans are granted to promoters, directors, KMPs and the related parties (as defined under Companies Act, 2013,) either severally or jointly with any other person, that are:

(a) repayable on demand or

(b) without specifying any terms or period of repayment

| Type of Borrower | Amount of loan or advance in the nature of loan outstanding | Percentage to the total Loans and Advances in the nature of loans |

| Promoters | ||

| Directors | ||

| KMPs | ||

| Related Parties |

- Capital-Work-in Progress (CWIP)

(a). For Capital-work-in progress, following ageing schedule shall be given:

CWIP aging schedule

(Amount in )

| CWIP | Amount in CWIP for a period of | Total* | |||

| Less than 1 year | 1-2years | 2-3years | More than 3 years | ||

| Projects in progress Projects temporarily suspended | |||||

*Total shall tally with CWIP amount in the balance sheet.

(b). For capital-work-in progress, whose completion is overdue or has exceeded its cost compared to its original plan, following CWIP completion schedule shall be given**:

CWIP aging schedule

(Amount in )

| CWIP | To be completed in | |||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | |

| Project 1 Project 2 | ||||

**Details of projects where activity has been suspended shall be given separately.

- Intangible assets under development:

(a). For Intangible assets under development, following ageing schedule shall be given:

Intangible assets under development aging schedule

(Amount in )

| Intangible assets under development | Amount in CWIP for a period of | Total* | |||

| Less than 1 year | 1-2years | 2-3years | More than 3 years | ||

| Projects in progress Projects temporarily suspended | |||||

* Total shall tally with the amount of Intangible assets under development in the balance sheet.

(b). For Intangible assets under development, whose completion is overdue or has exceeded its cost compared to its original plan, following Intangible assets under development completion schedule shall be given**:

Intangible assets under development aging schedule

(Amount in )

| Intangible assets under development | To be completed in | |||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | |

| Project 1 Project 2 |

||||

**Details of projects where activity has been suspended shall be given separately.

- Details of Benami Property held

Where any proceedings have been initiated or pending against the company for holding any benami property under the Benami Transactions (Prohibition) Act, 1988 (45 of 1988) and the rules made thereunder, the company shall disclose the following:-

(a). Details of such property, including year of acquisition,

(b). Amount thereof,

(c). Details of Beneficiaries,

(d). If property is in the books, then reference to the item in the Balance Sheet,

(e). If property is not in the books, then the fact shall be stated with reasons,

(f). Where there are proceedings against the company under this law as an co-conspirator of the transaction or as the transferor then the details shall be provided,

(g). Nature of proceedings, status of same and company’s view on - Where the Company has borrowings from banks or financial institutions on the basis of security of current assets, it shall disclose the following:-

(a). Whether quarterly returns or statements of current assets filed by the Company with banks or financial institutions are in agreement with the books of

(b). if not, summary of reconciliation and reasons of material discrepancies, if any to be adequately - Willful Defaulter*

Where a company is a declared willful defaulter by any bank or financial Institution or other lender, following details shall be given:

(a). Date of declaration as willful defaulter,

(b). Details of defaults (amount and nature of defaults),

* “willful defaulter” here means a person or an issuer who or which is categorized as a willful defaulter by any bank or financial institution (as defined under the Act) or consortium thereof, in accordance with the guidelines on willful defaulters issued by the Reserve Bank of India. - Relationship with Struck off Companies

Where the company has any transactions with companies struck off under section 248 of the Companies Act, 2013 or section 560 of Companies Act, 1956, the Company shall disclose the following details:-

| Name of struck off Company | Nature of transactions with struck-off Company | Balance outstanding | Relationship with the Struck off company, if any, to be disclosed |

| company, if any, to be disclosed | |||

| Receivables | |||

| Payables | |||

| Shares held by stuck off company | |||

| Other outstanding balances (to be specified) |

- Registration of charges or satisfaction with Registrar of Companies

Where any charges or satisfaction are yet to be registered with Registrar of Companies, beyond the statutory period, the details and reasons thereof, shall be disclosed. - Compliance with number of layers of companies

Where the company has not complied with the number of layers prescribed under clause (87) of section 2 of the Act read with Companies (Restriction on number of Layers) Rules, 2017, the name and CIN of the companies beyond the specified layers and the relationship/extent of holding of the company in such downstream companies shall be disclosed. - Ratios:

Companies shall disclose the all those ratios which are prescribed and shall explain the items included in numerator and denominator for computing the above ratios. Moreover, if any change in the ratio is more than 25% as compared to the preceding year then explanation for the same shall be provided.

| Ratios | Numerator | Denominator | Current Period | Previous Period | % Variance | Reason for variance |

| Current Ratio | ||||||

| Debt-equity ratio | ||||||

| Debt service coverage ratio | ||||||

| Return on equity | ||||||

| Inventory turnover ratio | ||||||

| Trade receivables turnover ratio | ||||||

| Trade payables turnover ratio | ||||||

| Net capital turnover ratio | ||||||

| Net profit ratio | ||||||

| Return on capital employed | ||||||

| Return on investment |

1. Current Ratio

The current ratio indicates a company’s overall liquidity position. It is widely used by banks in making decisions regarding the advancing of working capital credit to their clients.

Current Ratio = Current Assets/ Current Liabilities

2. Debt – Equity Ratio

Debt-to-equity ratio compares a Company’s total debt to shareholders equity. Both of these numbers can be found in a Company’s balance sheet.

Debt – Equity Ratio = Total Debt/ Shareholder’s Equity

3. Debt Service Coverage Ratio

Debt Service coverage ratio is used to analyze the firm’s ability to pay-off current interest and installments. Debt Service Coverage Ratio = Earnings available for debt service / Debt Service

Earning for Debt Service = Net Profit before taxes + Non-cash operating expenses like depreciation and other amortizations + Interest + other adjustments like loss on sale of Fixed assets etc.

Debt service = Interest & Lease Payments + Principal Repayments. “Net Profit after tax” means reported amount of “Profit / (loss) for the period” and it does not include items of other comprehensive income.

4. Return on Equity (ROE):

It measures the profitability of equity funds invested in the Company. The ratio reveals how profitability of the equity-holders’ funds have been utilized by the Company. It also measures the percentage return generated to equity-holders. The ratio is computed as:ROE = Net Profits after taxes – Preference Dividend (if any) / Average Shareholder’s Equity

5. Inventory Turnover Ratio

This ratio also known as stock turnover ratio and it establishes the relationship between the cost of goods sold during the period or sales during the period and average inventory held during the period. It measures the efficiency with which a Company utilizes or manages its inventory.

Inventory Turnover ratio = Cost of goods sold OR sales/ Average Inventory

Average inventory is (Opening + Closing balance / 2)

When the information opening and closing balances of inventory is not available then the ratio can be calculated by dividing COGS OR Sales by closing balance of Inventory.

6. Trade receivables turnover ratio

It measures the efficiency at which the firm is managing the receivables.

Trade receivables turnover ratio = Net Credit Sales / Average Accounts Receivable

Net credit sales consist of gross credit sales minus sales return.

Trade receivables include sundry debtors and bill’s receivables.

Average trade debtors = (Opening + Closing balance / 2) When the information about credit sales, opening and closing balances of trade debtors is not available then the ratio can be calculated by dividing total sales by closing balances of trade receivables.

7. Trade payables turnover ratio

It indicates the number of times sundry creditors have been paid during a period. It is calculated to judge the requirements of cash for paying sundry creditors. It is calculated by dividing the net credit purchases by average creditors. Trade payables turnover ratio = Net Credit Purchases / Average Trade Payables Net credit purchases consist of gross credit purchases minus purchase return When the information about credit purchases, opening and closing balances of trade creditors is not available then the ratio is calculated by dividing total purchases by the closing balance of trade creditors.

8. Net capital turnover ratio

It indicates a company’s effectiveness in using its working capital. The working capital turnover ratio is calculated as follows: Net Sales divided by the average amount of working capital during the same period.

Net capital turnover ratio = Net Sales/ Average Working Capital

Net Sales shall be calculated as total sales minus sales returns.

Working capital shall be calculated as current assets minus current liabilities.

9. Net profit ratio

It measures the relationship between net profit and sales of the business.

Net Profit Ratio = Net Profit / Net Sales

Net profit shall be after tax.

Net sales shall be calculated as total sales minus sales returns.

10. Return on capital employed (ROCE)

Return on capital employed indicates the ability of a company’s management to generate returns for both the debt holders and the equity holders. Higher the ratio, more efficiently is the capital being employed by the company to generate returns.

ROCE = Earnings before interest and taxes / Capital Employed Capital Employed = Tangible Net Worth + Total Debt + Deferred Tax Liability

11. Return on investment

Return on investment (ROI) is a financial ratio used to calculate the benefit an investor will receive in relation to their investment cost. The higher the ratio, the greater the benefit earned. The one of widely used method is Time Weighted Rate of Return (TWRR) and the same should be followed to calculate ROI. It adjusts the return for the timing of investment cash flows and its formula / method of calculation is commonly available. However, the same is given below for quick reference:

ROI = {MV (T1) – MV (T0) – Sum [C (t)]}

{MV (T0) + Sum [W (t) * C (t)]}

Where,

T1 = End of time period

T0 = Beginning of time period

t = Specific date falling between T1 and T0

MV (T1) = Market Value at T1

MV (T0) = Market Value at T0

C (t) = Cash inflow, cash outflow on specific date

W (t) = Weight of the net cash flow (i.e. either net inflow or net outflow) on day ‘t’, calculated as [T1 – t] / T1

Companies may provide ROI separately for each asset class (e.g., equity, fixed income, money market, etc.).

- Compliance with approved Scheme(s) of Arrangements

Where any Scheme of Arrangements has been approved by the Competent Authority in terms of sections 230 to 237 of the Companies Act, 2013, the Company shall disclose that the effect of such Scheme of Arrangements have been accounted for in the books of account of the Company ‘in accordance with the Scheme’ and ‘in accordance with accounting standards’ and deviation in this regard shall be explained. - Utilization of Borrowed funds and share premium:

(A). Where company has advanced or loaned or invested funds (either borrowed funds or share premium or any other sources or kind of funds) to any other person(s) or entity(ies), including foreign entities (Intermediaries) with the understanding (whether recorded in writing or otherwise) that the Intermediary shall

(i). directly or indirectly lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the company (Ultimate Beneficiaries) or

(ii). provide any guarantee, security or the like to or on behalf of the Ultimate Beneficiaries; the company shall disclose the following:-

- date and amount of fund advanced or loaned or invested in Intermediaries with complete details of each

- date and amount of fund further advanced or loaned or invested by such Intermediaries to other intermediaries or Ultimate Beneficiaries alongwith complete details of the ultimate

- date and amount of guarantee, security or the like provided to or on behalf of the Ultimate Beneficiaries

- declaration that relevant provisions of the Foreign Exchange Management Act, 1999 (42 of 1999) and Companies Act has been complied with for such transactions and the transactions are not violative of the Prevention of Money-Laundering act, 2002 (15 of 2003).;

(B). Where a company has received any fund from any person(s) or entity(ies), including foreign entities (Funding Party) with the understanding (whether recorded in writing or otherwise) that the company shall

(i). directly or indirectly lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the Funding Party (Ultimate Beneficiaries) or

(ii). provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries, the company shall disclose the following:-

(1). date and amount of fund received from Funding parties with complete details of each Funding

(2). date and amount of fund further advanced or loaned or invested other intermediaries or Ultimate Beneficiaries alongwith complete details of the other intermediaries’ or ultimate

(3). date and amount of guarantee, security or the like provided to or on behalf of the Ultimate Beneficiaries

(4). declaration that relevant provisions of the Foreign Exchange Management Act, 1999 (42 of 1999) and Companies Act has been complied with for such transactions and the transactions are not violative of the Prevention of Money-Laundering act, 2002 (15 of 2003).;

(iii).In Part II- Statement of Profit and Loss,-

(A). under the heading “III. Total Revenue (I +II)”, for the word “Revenue”, the word “Income” shall be substituted;

(B). under the heading “General Instructions for Preparation of Statement of Profit and Loss”,-

(1). in paragraph 2, in item (A), after sub-item (b), the following shall be inserted, namely:-“(ba) Grants or donations received (relevant in case of section 8 companies only)”;

(2). in paragraph “5. Additional information”, after item (viii) and the entries relating thereto, the following shall be inserted, namely:- “

- Undisclosed income

The Company shall give details of any transaction not recorded in the books of accounts that has been surrendered or disclosed as income during the year in the tax assessments under the Income Tax Act, 1961 (such as, search or survey or any other relevant provisions of the Income Tax Act, 1961), unless there is immunity for disclosure under any scheme and also shall state whether the previously unrecorded income and related assets have been properly recorded in the books of account during the year.; - Corporate Social Responsibility (CSR)

Where the company covered under section 135 of the companies act, the following shall be disclosed with regard to CSR activities:-

(a). amount required to be spent by the company during the year,

(b). amount of expenditure incurred,

(c). shortfall at the end of the year,

(c). shortfall at the end of the year,

(d). total of previous years shortfall,

(e). reason for shortfall,

(f). nature of CSR activities,

(g). details of related party transactions, e.g., contribution to a trust controlled by the company in relation to CSR expenditure as per relevant Accounting Standard,

(h). where a provision is made with respect to a liability incurred by entering into a contractual obligation, the movements in the provision during the year should be shown - Details of Crypto Currency or Virtual Currency

Where the Company has traded or invested in Crypto currency or Virtual Currency during the financial year, the following shall be disclosed:-

(a). profit or loss on transactions involving Crypto currency or Virtual Currency

(b). amount of currency held as at the reporting date,

(c). deposits or advances from any person for the purpose of trading or investing in Crypto Currency/ virtual currency.”

The amendments to Division -I are smaller changes and mostly relate to the words used in the Balance Sheet of an AS compliant company like the replacement of the word “Fixed assets” under “Non-current assets” with “Property, Plant and Equipment”.

Multiple Activity CompaniesWhere a company has multiple activities e.g. both manufacturing and trading i.e. it falls under more than one category, it should comply with the various disclosure requirements relating to each of its classified activities. For instance, in respect of its manufacturing activities, such a company should comply with the requirements relating to a manufacturing company, whereas in respect of its trading or service activities, it should comply with the requirements relating to those categories of companies. However, in case of complexities in segregating the required information it would be sufficient compliance if the information is disclosed with respect to main activities with a suitable disclosure explaining the reasons thereof.

PART I — BALANCE SHEET

Name of the Company…………………….

Balance Sheet as at ………………………

(Rupees in…………)

| Particulars | Note No. | Figures as at the of current reporting period | Figures as at the end of the previous reporting period |

| 1 | 2 | 3 | 4 |

| I. EQUITY AND LIABILITIES (1) Shareholders’ funds (a) Share capital (b) Reserves and surplus (c) Money received against share Warrants (2) Share application money pending allotment (3) Non-current liabilities (a) Long-term borrowings (b) Deferred tax liabilities (Net) (c) Other Long term liabilities (d) Long-term provisions (4) Current liabilities (a) Short-term borrowings (b) Trade payables (c) Other current liabilities (d) Short-term provisionsTOTAL II. ASSETS Non-current assets (1) (a) Property, Plant and Equipment and Intangible assets (i) Property, Plant and Equipment (ii) Intangible assets (iii) Capital work-in-progress (iv) Intangible assets under development (b) Non-current investments (c) Deferred tax assets (net) (d) Long-term loans and advances (e) Other non-current assets (2) Current assets (a) Current investments (b) Inventories (c) Trade receivables (d) Cash and cash equivalents (e) Short-term loans and advances (f) Other current assets |

|||

| Total | |||

PART II – STATEMENT OF PROFIT AND LOSS

Name of the Company…………………….

Profit and loss statement for the year ended ………………………

(Rupees in…………)

| Particulars | Note No. | Figures as at the end of current reporting period | Figures as at the end of the previous reporting period | |

| 1 | 2 | 3 | 4 | |

| I | Revenue from operations | xxx | xxx | |

| II | Other income | xxx | xxx | |

| III | Total Income (I + II) | xxx | xxx | |

| IV | Expenses Cost of materials consumed Purchases of Stock-in-Trade Changes in inventories of finished goods work-in-progress and Stock in-Trade Employee benefits expense Finance costs Depreciation and amortization expense Other expenses Total expenses |

xxx xxx xxx xxx |

xxx xxx xxx xxx |

|

| V | Profit before exceptional and extraordinary items and tax (III – IV) | xxx | xxx | |

| VI | Exceptional items | xxx | xxx | |

| VII | Profit before extraordinary items and tax (V –VI) | xxx | xxx | |

| VIII | Extraordinary items | xxx | xxx | |

| IX | Profit before tax (VII- VIII) | xxx | xxx | |

| X | Tax expense: (1) Current tax (2) Deferred tax |

xxx |

xxx |

|

| XI | Profit (Loss) for the period from continuing operations (VII-VIII) | xxx | xxx | |

| XII | Profit/(loss) from discontinuing operations | xxx | xxx | |

| XIII | Tax expense of discontinuing operation | xxx | xxx | |

| XIII | Profit/(loss) from Discontinuing operations (after tax) (XII-XIII) | xxx | xxx | |

| XV | Profit (Loss) for the period (XI + XIV) | xxx | xxx | |

| XVI | Earnings per equity share: (1) Basic (2) Diluted |

xxx | xxx |

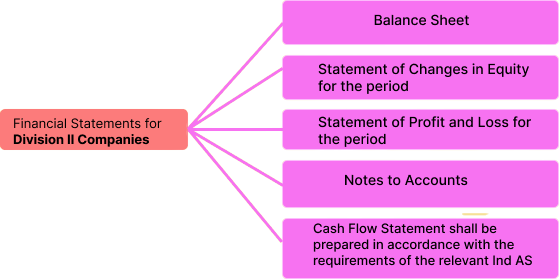

Amendment in Division II to schedule III to the Companies Act, 2013- Overview

The majority of the modifications made in Schedule III and CARO 2020 were to match the two reporting frameworks and improve transparency between the company and the users of financial statements. It further enabled the reduction of the risk of fraud and other unethical behavior on part of the companies.

CARO 2020 provides a para-wise commentary on Companies (Auditor’s Report) Order. It is a complete guide on the applicability and the matters that need to be reported by an Auditor on CARO, supplemented by Clause-wise Ready Reckoner, FAQs, Case Studies, in a Nutshell, etc.These amendments bring in numerous additional disclosures in Financial Statement, Directors Report and Audit Report. Companies will have to gear up to comply with the additional disclosure requirements with regards to these requirements; MCA/ICAI should come up with guidance/clarifications so as to enable consistency in reporting.Here is an overview of the requirement of schedule III specifically with respect to Division-II of Schedule-III-Financial Statements for a company whose financial statements are drawn up in compliance of the Companies (Indian Accounting Standards) Rules, 2015.

As per Ind AS 101, a company’s first Ind AS financial statements shall include at least three balance sheets, two statements of profit and loss, two statements of cash flows and two statements of changes in equity and related notes. This Guidance Note does not deal with the presentation aspects of reconciliations that are required to be provided as a part of a company’s first Ind AS financial statements.If an entity publishes a complete set of Financial Statements in its interim financial report, the form and content of those statements shall conform to the requirements of Ind AS 1 for a complete set of Financial Statements.

If an entity publishes a set of condensed Financial Statements in its interim financial report, those condensed statements shall include, at a minimum, each of the headings and subtotals that were included in its most recent annual Financial Statements and the selected explanatory notes as required by this Standard. Additional line items or notes shall be included if their omission would make the condensed interim Financial Statements misleading.”

Disclosures required

To comply with all these amendments, the Company/Auditor needs to check every aspect of financial transactions thoroughly and needs to incorporate these amendments in the financials of 31-03-2022 onwards

General Instructions for Preparation of Balance Sheet- An entity shall classify an asset as current when-

(i). it expects to realize the asset, or intends to sell or consume it, in its normal operating cycle;

(ii). it holds the asset primarily for the purpose of trading;

(iii). it expects to realize the asset within twelve months after the reporting period; or

(iv). the asset is cash or a cash equivalent unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period.

(v). An entity shall classify all other assets as non-current. - The operating cycle of an entity is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. When the entity’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months.

- An entity shall classify a liability as current when-

(i). it expects to settle the liability in its normal operating cycle;

(ii). it holds the liability primarily for the purpose of trading;

(iii). the liability is due to be settled within twelve months after the reporting period; or

(iv). it does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting period. Terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification

(v). An entity shall classify all other liabilities as non-current. - A receivable shall be classified as a ‘trade receivable’ if it is in respect of the amount due on account of goods sold or services rendered in the normal course of business.

- A payable shall be classified as a ‘trade payable’ if it is in respect of the amount due on account of goods purchased or services received in the normal course of business.

- A company shall disclose the following in the Notes:

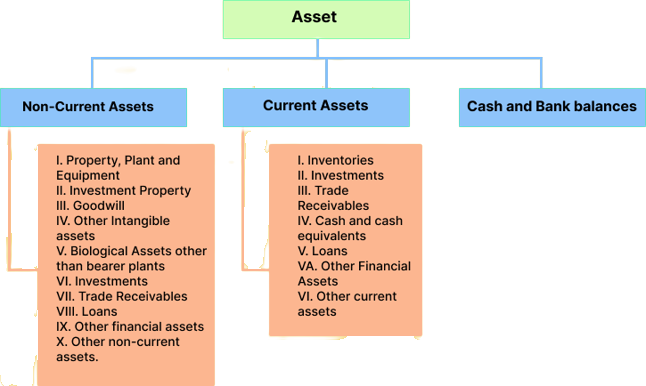

A. Non-Current Assets

I. Property, Plant and Equipment:

- Classification shall be given as:

(a). Land

(b). Buildings

(c). Plant and Equipment

(d). Furniture and Fixtures

(e). Vehicles

(f). Office equipment

(g). Bearer Plants

(h). Others (specify nature) - Assets under lease shall be separately specified under each class of assets

- A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions through business combinations, amount of change due to revaluation (if change is 10% or more in the aggregate of the net carrying value of each class of Property, Plant and Equipment) and other adjustments and the related depreciation and impairment losses or reversals shall be disclosed separately.

II. Investment Property:

A reconciliation of the gross and net carrying amounts of each class of property at the beginning and end of the reporting period showing additions, disposals, acquisitions through business combinations and other adjustments and the related depreciation and impairment losses or reversals shall be disclosed separately.

III. Goodwill:

A reconciliation of the gross and net carrying amount of goodwill at the beginning and end of the reporting period showing additions, impairments, disposals and other adjustments.

IV. Other Intangible assets:

- Classification shall be given as:

(a). Brands or trademarks

(b). Computer software

(c). Mastheads and publishing titles

(d). Mining rights copyrights, patents, other intellectual property rights, services and operating rights

(e). Recipes, formulae, models, designs and prototypes

(f). License and franchises

(g). Other (specify nature) - A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions through business combinations, amount of change due to revaluation (if change is 10% or more in the aggregate of the net carrying value of each class of intangible assets) and other adjustments and the related amortization and impairment losses or reversals shall be disclosed separately.

V. Biological Assets other than bearer plants:

A reconciliation of the carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions through business combinations and other adjustments shall be disclosed separately.

VI. Investments:

I. Property, Plant and Equipment:

- Investments shall be classified as

(a). Investments in Equity Instruments;

(b). Investments in Preference Shares;

(c). Investments in Government or trust securities;

(d). Investments in debentures or bonds;

(e). Investments in Mutual Funds;

(f). Investments in partnership firms; or

(g). Other investments (specify nature).

Under each classification, details shall be given of names of the bodies corporate that are-

- Subsidiaries,

- associates,

- joint ventures, or

- structured entities,

where investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid). Investments in partnership firms along with names of the firms, their partners, total capital and the shares of each partner shall be disclosed separately.

- The following shall also be disclosed:

(a). Aggregate amount of quoted investments and market value thereof;

(b). Aggregate amount of unquoted investments; and

(c). Aggregate amount of impairment in value of investments.

VII. Trade Receivables:

- Trade Receivables shall be sub-classified as:

(a). Trade Receivables considered good – Secured;

(b). Trade Receivables considered good – Unsecured;

(c). Trade Receivables which have significant increase in Credit Risk; and

(d). Trade Receivables – credit impaired. - Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately.

- Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated.

- For trade receivables outstanding, following ageing schedule shall be given:

Trade Receivables ageing schedule

(Amount in )

| Particulars | Outstanding for following periods from due date of payment# | |||||

| Less than 6 months | 6 months -1 year | 1-2 years | 2-3 years | More than 3 years | Total | |

| (i) Undisputed Trade receivables –considered good | ||||||

| (ii) Undisputed Trade Receivables – which have significant increase in credit risk | ||||||

| (iii) Undisputed Trade Receivables – credit impaired | ||||||

| (iv) Disputed Trade Receivables–considered good | ||||||

| (v) Disputed Trade Receivables – which have significant increase in credit risk | ||||||

| (vi) Disputed Trade Receivables – credit impaired | ||||||

# Similar information shall be given where no due date of payment is specified in that case disclosure shall be from the date of the transaction.

Unbilled dues shall be disclosed separately;

VIII. Loans:

(i). Loans shall be classified as-

(a). Loans to related parties (giving details thereof); and

(c) Other loans (specify nature).

(ii). Loans Receivables shall be sub-classified as:

(a). Loans Receivables considered good – Secured;

(b). Loans Receivables considered good – Unsecured;

(c). Loans Receivables which have significant increase in Credit Risk; and

(d). Loans Receivables – credit impaired,

(iii).Allowance for bad and doubtful loans shall be disclosed under the relevant heads separately.

(iv).Loans due by directors or other officers of the company or any of them either severally or jointly with any other persons or amounts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated.

IX. Other financial assets

(i) Security Deposits

(ii) Bank deposits with more than 12 months maturity

(iii) others(to be specified)

X. Other non-current assets:

Other non-current assets shall be classified as-

(i) Capital Advances; and

(ii) Advances other than capital advances;

(1). Advances other than capital advances shall be classified as:

(a) Security Deposits;

(b) Advances to related parties (giving details thereof); and

(c) Other advances (specify nature).

(2). Advances to directors or other officers of the company or any of them either severally or jointly with any other persons 0r advances to firms or private companies respectively in which any director is a partner or a director or a member should be separately stated, in case advances are of the nature of a financial asset as per relevant Ind AS, these are to be disclosed under ‘other financial assets’ separately.

(iii) Others (specify nature).

B. Current Assets

I. Inventories:

Inventories shall be classified as-

- Raw materials;

- Work-in-progress;

- Finished goods;

- Stock-in-trade (in respect of goods acquired for trading);

- stores and spares;

- Loose tools; and

- Others (specify nature).

Goods-in-transit shall be disclosed under the relevant sub-head of inventories.

Mode of valuation shall be stated.

II. Investments:

(i). Investments shall be classified as-

- Investments in Equity Instruments;

- Investment in Preference Shares;

- Investments in government or trust securities;

- Investments in debentures or bonds;

- Investments in Mutual Funds;

- Investments in partnership firms; and

- Other investments (specify nature).

Under each classification, details shall be given of names of the bodies corporate that are-

- subsidiaries,

- associates,

- joint ventures, or

- structured entities

in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid).

(ii). The following shall also be disclosed:

- Aggregate amount of quoted investments and market value thereof,

- Aggregate amount of unquoted investments;

- Aggregate amount of impairment in value of investments,

III. Trade Receivables:

- Trade Receivables shall be sub-classified as:

(a). Trade Receivables considered good – Secured;

(b). Trade Receivables considered good – Unsecured;

(c). Trade Receivables which have significant increase in Credit Risk; and?

(d). Trade Receivables – credit impaired. - Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately,

- Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated.

- For trade receivables outstanding, following ageing schedule shall be given:

Trade Receivables ageing schedule

(Amount in )

| Particulars | Outstanding for following periods from due date of payment# | |||||

| Less than 6 months | 6 months -1 year | 1-2 years | 2-3 years | More than 3 years | Total | |

| (i) Undisputed Trade receivables –considered good | ||||||

| (ii) Undisputed Trade Receivables –which have significant increase in credit risk | ||||||

| (iii) Undisputed Trade Receivables –credit impaired | ||||||

| (iv) Disputed Trade Receivables–considered good | ||||||

| (v) Disputed Trade Receivables –which have significant increase in credit risk | ||||||

| (vi) Disputed Trade Receivables –credit impaired | ||||||

# similar information shall be given where no due date of payment is specified in that case disclosure shall be from the date of the transaction.

Unbilled dues shall be disclosed separately.

IV. Cash and cash equivalents:

Cash and cash equivalents shall be classified as-

(a). Balances with Banks (of the nature of cash and cash equivalents);

(b). Cheques, drafts on hand;

(c). Cash on hand; and

(d). Others (specify nature).

V. Loans

- Loans shall be classified as:

(a). Security deposits;

(b). Loans to related parties (giving details thereof); and

(d). others (specify nature). - Loans Receivables shall be sub-classified as:

(a). Loans Receivables considered good – Secured;

(b). Loans Receivables considered good – Unsecured;

(c). Loans Receivables which have significant increase in Credit Risk; and

(d). Loans Receivables – credit impaired - Allowance for bad and doubtful loans shall be disclosed under the relevant heads separately.

- Loans due by directors or other officers of the company or any of them either severally or Jointly with any other person or amounts due by firms or private companies respectively in which any director is a partner or a director or a member shall be separately stated.

VA. Other Financial Assets:

This is an all-inclusive heading, which incorporates financial assets that do not fit into any other financial asset categories, such as, Security Deposits.

VI. Other current assets (specify nature):

This is an all-inclusive heading, which incorporates current assets that do not fit into any other asset categories. Other current assets shall be classified as-

(i) Advances other than capital advances

- Advances other than capital advances shall be classified as:

(a). Security Deposits;

(b). Advances to related parties (giving details thereof;

(c). Other advances (specify nature). - Advances to directors or other officers of the company or any of them either severally or jointly with any other persons or advances to firms or private companies respectively in which any director is a partner or a director or a member should be separately stated.

(ii) Others (specify nature)

C. Cash and Bank balances:

The following disclosures with regard to cash and bank balances shall be made:

- Earmarked balances with banks (for example. for unpaid dividend) shall be separately stated.

- Balances with banks to the extent held as margin money or security against the borrowings, guarantees, other commitments shall be disclosed separately.

- Repatriation restrictions, if any, in respect of cash and bank balances shall be separately stated.

D. Equity

I. Equity Share Capital:

For each class of equity share capital:

- the number and amount of shares authorized;

- the number of shares issued, subscribed and fully paid, and subscribed but not fully paid;

- par value per share;

- a reconciliation of the number of shares outstanding at the beginning and at the end of the period;

- the rights, preferences and restrictions attaching to each class of shares including restrictions on the distribution of dividends and the repayment of capital;

- shares in respect of each class in the company held by its holding company or its ultimate holding company including shares held by subsidiaries or associates of the holding company or the ultimate holding company In aggregate;

- Shares in the company held by each shareholder holding more than five per cent shares specifying the number of shares held;

- shares reserved for issue under options and contracts or commitments for the sale of shares or disinvestment, including the terms and amounts;

- for the period of five years immediately preceding the date at which the Balance Sheet is prepared-

- aggregate number and class of shares allotted as fully paid up pursuant to contract without payment being received in cash;

- aggregate number and class of shares allotted as fully paid up by way of bonus shares; and

- aggregate number and class of shares bought back;

- terms of any securities convertible into equity shares issued along with the earliest date of conversion in descending order starting from the farthest such date;

- calls unpaid (showing aggregate value of calls unpaid by directors and officers)

- forfeited shares (amount originally paid up)

- A company shall disclose Shareholding of Promoters* as under:

| Shares held by promoters at the end of the year | % Change during the year*** | |||

| S. No | Promoter name | No. of Shares** | %of total shares | |

| Total | ||||

*Promoter here means promoter as defined in the Companies Act, 2013.

** Details shall be given separately for each class of shares

*** percentage change shall be computed with respect to the number at the beginning of the year or if issued during the year for the first time then with respect to the date of issue.

II. Other Equity

(i). ‘Other Reserves’ shall be classified in the notes as-

- Capital Redemption Reserve;

- Debenture Redemption Reserve;

- Share Options Outstanding Account; and

- others- (specify the nature and purpose of each reserve and the amount in respect thereof);

(Additions and deductions since last balance sheet to be shown under each of the specified heads)

(ii). Retained Earnings represents surplus i.e. balance of the relevant column in the Statement of Changes in Equity;

(iii). A reserve specifically represented by earmarked investments shall disclose the fact that it is so represented; disclose the fact that it is so represented;

(iv). Debit balance of Statement of Profit and Loss shall be shown as a negative figure under the head ‘retained earnings’. Similarly, the balance of ‘Other Equity’, after adjusting negative balance of retained earnings, if any, shall be shown under the head ‘Other Equity’ even if the resulting figure is in the negative; and

(v). Under the sub-head ‘Other Equity’, disclosure shall be made for the nature and amount of each item.

E. Non-Current Liabilities

I. Borrowings:

- borrowings shall be classified as-

(a). Bonds or debentures

(b). Term loans

(I). from banks

(II). from other Parties

(c). Deferred payment liabilities

(d). Deposits

(e). (e) Loans from related Parties

(f). Liability component of compound financial instruments

(g). Other loans (specify nature); - borrowings shall further be sub-classified as secured and unsecured. Nature of security shall be specified separately in each case

- where loans have been guaranteed by directors or others, the aggregate amount of such loans under each head shall be disclosed;

- bonds or debentures (along with the rate of interest, and particulars of redemption or conversion, as the case may be) shall be stated in descending order of maturity or conversion, stating from farthest redemption or conversion date, as the case may be, where bonds/debentures are redeemable by installments, the date of maturity for this purpose must be reckoned as the date on which the first installment becomes due;

- particulars of any redeemed bonds or debentures which the company has power to reissue shall be disclosed;

- terms of repayment of term loans and other loans shall be stated; and

- Period and amount of default as on the balance sheet date in repayment of borrowings and interest shall be specified separately in each case.

(III). Provisions:

The amounts shall be classified as-

(a). Provision for employee benefits; and

(b). Others (specify nature).

(IV). Other current liabilities:

(a). Advances; and

(b). Others (specify nature).

F. Current Liabilities

I. Borrowings:

- Borrowings shall be classified as-

(a). Loans repayable on demand

(I). from banks

(II). from other parties

(b). Loans from related parties

(c). Deposits

(d). Other loans (specify nature); - Borrowings shall further be sub-classified as secured and unsecured. Nature of security shall be specified separately in each case;

- where loans have been guaranteed by directors or others, the aggregate amount of such loans under each head shall be disclosed;

- Period and amount of default as on the balance sheet date in repayment of borrowings and interest shall be specified separately in each case.

- Current maturities of Long term borrowings shall be disclosed separately

II. Other Financial Liabilities:

Other Financial liabilities shall be classified as-

(a). Interest accrued;

(b). Unpaid dividends

(c). Application money received for allotment of securities to the extent refundable and interest accrued thereon;

(d). Unpaid matured deposits and interest accrued thereon;

(e). Unpaid matured debentures and interest accrued thereon; and

(f). Others (specify nature).

‘Long term debt’ is a borrowing having a period of more than twelve months at the time of origination.

III. Other current liabilities:

The amounts shall be classified as

(a). revenue received in advance;

(b). other advances (specify nature);

(c). and others (specify nature);

IV. Provisions:

The amounts shall be classified as-

(i). provision for employee benefits; and

(ii). others (specify nature).

FA. Trade Payables

The following details relating to micro, small and medium enterprises shall be disclosed in the notes:

- the principal amount and the interest due thereon (to be shown separately) remaining unpaid to any supplier at the end of each accounting year;

- the amount of interest paid by the buyer in terms of section 16 of the Micro, Small and Medium Enterprises Development Act, 2006 (27 of 2006), along with the amount of the payment made to the supplier beyond the appointed day during each accounting year;

- the amount of interest due and payable for the period of delay in making payment (which has been paid but beyond the appointed day during the year) but without adding the interest specified under the Micro, Small and Medium Enterprises Development Act, 2006;

- the amount of interest accrued and remaining unpaid at the end of each accounting year; and

- the amount of further interest remaining due and payable even in the succeeding years, until such date when the interest dues above are actually paid to the small enterprise, for the purpose of disallowance of a deductible expenditure under section 23 of the Micro, Small and Medium Enterprises Development Act, 2006.

Explanation.- The terms ‘appointed day’, ‘buyer’, ‘enterprise’, ‘micro enterprise’, ‘small enterprise’ and ‘supplier’, shall have the same meaning as assigned to them under clauses (b), (d), (e), (h), (m) and (n) respectively of section 2 of the Micro, Small and Medium Enterprises Development Act, 2006.FB. Trade payables due for payment

The following ageing schedule shall be given for Trade payables due for payment:-

Trade Payables ageing schedule

(Amount in )

| Particulars | Outstanding for following periods from due date of payment# | ||||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | Total | |

| (i) MSME | |||||

| (ii) Others | |||||

| (iii) Disputed dues – MSME | |||||

| (iv) Disputed dues - Others | |||||

# Similar information shall be given where no due date of payment is specified in that case disclosure shall be from the date of the transaction.

Unbilled dues shall be disclosed separately;

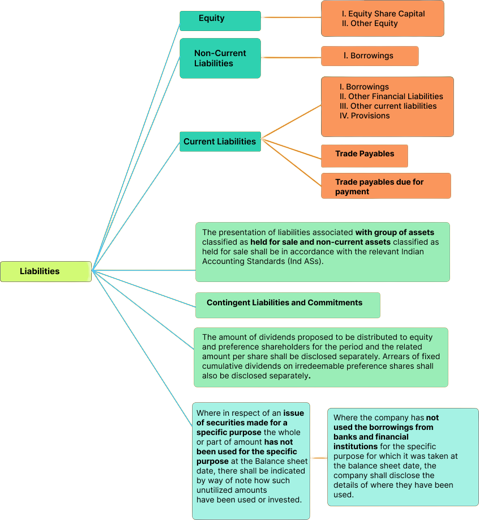

G. The presentation of liabilities associated with group of assets classified as held for sale and non-current assets classified as held for sale shall be in accordance with the relevant Indian Accounting Standards (Ind ASs).

H. Contingent Liabilities and Commitments:

(To the extent not provided for)

- Contingent Liabilities shall be classified as-

(a). claims against the company not acknowledged as debt;

(b). guarantees excluding financial guarantees; and

(c). other money for which the company is contingently liable. - Commitments shall be classified as-

(a). estimated amount of contracts remaining to be executed on capital account and not provided for;

(b). uncalled liability on shares and other investments partly paid; and

(c). other commitments (specify nature).

I. The amount of dividends proposed to be distributed to equity and preference shareholders for the period and the related amount per share shall be disclosed separately. Arrears of fixed cumulative dividends on irredeemable preference shares shall also be disclosed separately.

J. Where in respect of an issue of securities made for a specific purpose the whole or part of amount has not been used for the specific purpose at the Balance sheet date, there shall be indicated by way of note how such unutilized amounts have been used or invested.

JA. Where the company has not used the borrowings from banks and financial institutions for the specific purpose for which it was taken at the balance sheet date, the company shall disclose the details of where they have been used.

| SBNs | Other denomination notes | Total | |

| Closing cash in hand as on 08.11.2016 | |||

| (+) Permitted receipts | |||

| (-) Permitted payments | |||

| (-) Amount deposited in Banks | |||

| Closing cash in hand as on 30.12.2016 |

L. Additional Regulatory Information

(i). Title deeds of Immovable Properties not held in name of the Company

The company shall provide the details of all the immovable properties (other than properties where the Company is the lessee and the lease agreements are duly executed in favor of the lessee) whose title deeds are not held in the name of the company in following format and where such immovable property is jointly held with others, details are required to be given to the extent of the company’s share.

| Relevant line item in the Balance sheet | Description of item of property | Gross carrying value | Whether title deed holder is a promoter, director or relative# of promoter*/director or employee of promoter/director | Property held since which date | Reason for not being held in the name of the company** |

| PPE | Land | - | - | - | **also indicate if in dispute |

| Building | |||||

| Investment property | Land | ||||

| Building | |||||

| Non-current asset held for sale | Land | ||||

| Building | |||||

| others |

#Relative here means relative as defined in the Companies Act, 2013.

*Promoter here means promoter as defined in the Companies Act, 2013.

- The Company shall disclose as to whether the fair value of investment property (as measured for disclosure purposes in the financial statements) is based on the valuation by registered valuer as defined under rule 2 of Companies (Registered Valuers and Valuation) Rules, 2017.

- Where the Company has revalued its Property, Plant and Equipment (including Right-of-Use Assets), the company shall disclose as to whether the revaluation is based on the valuation by a registered valuer as defined under rule 2 of Companies (Registered Valuers and Valuation) Rules, 2017.

- Where the company has revalued its intangible assets, the company shall disclose as to whether the revaluation is based on the valuation by a registered valuer as defined under rule 2 of Companies (Registered Valuers and Valuation) Rules, 2017.

- The following disclosures shall be made where Loans or Advances in the nature of loans are granted to promoters, directors, KMPs and the related parties (as defined under Companies Act, 2013), either severally or jointly with any other person, that are:

(a). repayable on demand; or

(b). without specifying any terms or period of repayment,

| Type of Borrower | Amount of loan or advance in the nature of loan outstanding | Percentage to the total Loans and Advances in the nature of loans |

| Promoter | ||

| Directors | ||

| KMPs | ||

| Related Parties |

(vi). Capital-Work-in Progress (CWIP)

(a). For Capital-work-in progress, following ageing schedule shall be given:

CWIP aging schedule

(Amount in )

| CWIP | Amount in CWIP for a period of | Total* | |||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | ||

| Projects in progress | |||||

| Projects temporarily suspended | |||||

*Total shall tally with CWIP amount in the balance sheet.

(b). For capital-work-in progress, whose completion is overdue or has exceeded its cost compared to its original plan, following CWIP completion schedule shall be given**:

(Amount in )

| CWIP | To be completed in | |||

| Less than1 year | 1-2 years | 2-3 years | More than 3 years | |

| Project 1 | ||||

| Project 2" | ||||

**Details of projects where activity has been suspended shall be given separately.

(vii). Intangible assets under development:

(a). For Intangible assets under development, following ageing schedule shall be given:

Intangible assets under development aging schedule

(Amount in )

| Intangible assets under development | Amount in CWIP for a period of | Total* | |||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | ||

| Projects in progress | |||||

| Projects temporarily suspended | |||||

* Total shall tally with the amount of Intangible assets under development in the balance sheet.

(b). For Intangible assets under development, whose completion is overdue or has exceeded its cost compared to its original plan, the following shall be given**:

Intangible assets under development completion schedule

(Amount in )

| Intangible assets under development | To be completed in | |||

| Less than 1 year | 1-2 years | 2-3 years | More than 3 years | |

| Project 1 | ||||

| Project 2 | ||||

**Details of projects where activity has been suspended shall be given separately.

(viii).Details of Benami Property held

Where any proceeding has been initiated or pending against the company for holding any benami property under the Benami Transactions (Prohibition) Act, 1988 (45 of 1988) and rules made thereunder, the company shall disclose the following:-

- Details of such property,

- Amount thereof,

- Details of Beneficiaries,

- If property is in the books, then reference to the item in the Balance Sheet,

- If property is not in the books, then the fact shall be stated with reasons,

- Where there are proceedings against the company under this law as an a better of the transaction or as the transferor then the details shall be provided,

- Nature of proceedings, status of same and company’s view on same.

(ix). where the Company has borrowings from banks or financial institutions on the basis of security of current assets, it shall disclose the following:-

- whether quarterly returns or statements of current assets filed by the Company with banks or financial institutions are in agreement with the books of accounts;

- if not, summary of reconciliation and reasons of material discrepancies, if any to be adequately disclosed.

(x). Willful Defaulter*

Where a company is a declared willful defaulter by any bank or financial Institution or other lender, following details shall be given:

- Date of declaration as willful defaulter,

- willful defaulter” here means a person or an issuer who or which is categorized as a willful defaulter by any bank or financial institution (as defined under the Companies Act, 2013) or consortium thereof, in accordance with the guidelines on willful defaulters issued by the Reserve Bank of India.

(xi). Relationship with Struck off Companies

Where the company has any transactions with companies struck off under section 248 of the Companies Act, 2013 or section 560 of Companies Act, 1956, the Company shall disclose the following details, namely:-

| Name of struck off Company | Nature of transactions with struck-off Company | Balance outstanding | Relationship with the Struck off company, if any,to be disclosed |

| Investments in securities | |||

| Receivables | |||

| Payables | |||

| Shares held by stuck off company | |||

| Other outstanding balances (to be specified) |

(xii). Registration of charges or satisfaction with Registrar of Companies (ROC)

Where any charges or satisfaction are yet to be registered with ROC beyond the statutory period, details and reasons thereof shall be disclosed.

(xiii). Compliance with number of layers of companies

Where the company has not complied with the number of layers prescribed under clause (87) of section 2 of the Act read with the Companies (Restriction on number of Layers) Rules, 2017, the name and CIN of the companies beyond the specified layers and the relationship or extent of holding of the company in such downstream companies shall be disclosed.

(xiv).Following Ratios to be disclosed:-

- Current Ratio,

- Debt-Equity Ratio,

- Debt Service Coverage Ratio,

- Return on Equity Ratio,

- Inventory turnover ratio,

- Trade Receivables turnover ratio,

- Trade payables turnover ratio,

- Net capital turnover ratio,

- Net profit ratio,

- Return on Capital employed,

- Return on investment.

The company shall explain the items included in numerator and denominator for computing the above ratios. Further explanation shall be provided for any change in the ratio by more than 25% as compared to the preceding year.

(xv). Compliance with approved Scheme(s) of Arrangements

Where the Scheme of Arrangements has been approved by the Competent Authority in terms of sections 230 to 237 of the Companies Act, 2013, the company shall disclose that the effect of such Scheme of Arrangements have been accounted for in the books of account of the Company ‘in accordance with the Scheme’ and ‘in accordance with accounting standards’ and any deviation in this regard shall be explained.

(xvi).Utilization of Borrowed funds and share premium:

(A). Where company has advanced or loaned or invested funds (either borrowed funds or share premium or any other sources or kind of funds) to any other person(s) or entity(ies), including foreign entities (Intermediaries) with the understanding (whether recorded in writing or otherwise) that the Intermediary shall

- Directly or indirectly lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the company (Ultimate Beneficiaries) or

- Provide any guarantee, security or the like to or on behalf of the Ultimate Beneficiaries; the company shall disclose the following:-

- date and amount of fund advanced or loaned or invested in Intermediaries with complete details of each Intermediary.

- date and amount of fund further advanced or loaned or invested by such Intermediaries to other intermediaries or Ultimate Beneficiaries alongwith complete details of the ultimate beneficiaries.

- date and amount of guarantee, security or the like provided to or on behalf of the Ultimate Beneficiaries

- declaration that relevant provisions of the Foreign Exchange Management Act, 1999 (42 of 1999) and Companies Act has been complied with for such transactions and the transactions are not violative of the Prevention of Money-Laundering act, 2002 (15 of 2003).;

(B). Where a company has received any fund from any person(s) or entity(ies), including foreign entities (Funding Party) with the understanding (whether recorded in writing or otherwise) that the company shall

- directly or indirectly lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the Funding Party (Ultimate Beneficiaries) or

- provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries, the company shall disclose the following:-

- date and amount of fund received from Funding parties with complete details of each Funding party.

- date and amount of fund further advanced or loaned or invested other intermediaries or Ultimate Beneficiaries alongwith complete details of the other intermediaries’ or ultimate beneficiaries.

- date and amount of guarantee, security or the like provided to or on behalf of the Ultimate Beneficiaries

- declaration that relevant provisions of the Foreign Exchange Management Act, 1999 (42 of 1999) and Companies Act has been complied with for such transactions and the transactions are not violative of the Prevention of Money-Laundering act, 2002 (15 of 2003)

When a company applies an accounting policy retrospectively or makes a restatement of items in the financial statements or when it reclassifies items in its financial statements, the company shall attach to the Balance Sheet, a “Balance Sheet” as at the beginning of the earliest comparative period presented.