Declaration of commencement of business in Form 20A- Introduction

The Companies (Amendment) Bill, 2019 was passed with the aim to ensure more accountability and better enforcement in order to strengthen the norms of corporate governance and management of compliance in the corporate sector. This bill comprises of various new insertions and amendments. Amongst these, Section 10A is the latest addition to the Companies Act, 2013. This article talks about the essentials of the Section 10A of Companies Act in detail.

OverviewSection 10A of the Companies Act is a reinstatement of the provisions under Section 149 of the same Act. However, Section 149 was only applicable to public companies. The latest amendments have restricted every company having a share capital and incorporated post the commencement of the Ordinance, not to commence its businesses or exercise its borrowing powers unless the directors of the entity file a declaration within 180 days from the date of incorporation. It has to be filed in a prescribed form and requires every subscriber of the memorandum to pay the value of the shares as agreed for. Additionally, the registered office of the entity should be verified by filing all the necessary returns with the Registrar.Failure to comply with Section 10A may be an additional ground for the Registrar of Companies to strike off of the company’s name.

Essentials for Filing Form INC 20AThe following are the essentials required to file Form INR 20A.

- The Subscriber is required to pay the share subscription amount to the Company.

- The Company is required to obtain all the needed regulatory approval before the commencement of business. This goes out for business activities which are exclusively regulated by other sectoral regulators like the SEBI and IRDA as well.

The following is a part of Section 10A of the Companies Act:After section 10 of the principal Act, the following section shall be inserted, namely:—

Section 10A (1): A company incorporated after the commencement of the Companies (Amendment) Act, 2019 and having a share capital shall not commence any business or exercise any borrowing powers unless:

- A declaration is filed by a director within a period of one hundred and eighty days of the date of incorporation of the company in such form and verified in such manner as may be prescribed, with the Registrar that every subscriber to the memorandum has paid the value of the shares agreed to be taken by him on the date of making of such declaration; and

- The company has filed with the Registrar a verification of its registered office as provided in sub-section (2) of section 12.

The new Section 10A of the Companies Act has been introduced through the Companies (Amendment) Bill, 2019 and prescribes that every company is now required to file e-Form INC 20A with the Registrar of Companies.The section states that any company incorporated after the commencement of the Companies (Amendment) Bill, 2019 will be required to file the e-Form INC-20A with the Registrar of Companies within 180 days from the date of incorporation or commencement of its business. The form will comprise of the declaration by the director of the Company that all the subscribers to the memorandum have paid up the value of the shares agreed to be taken by the Director. It also declares that the company has filed and verified its registered office with the Registrar through Form INC-22 according to Section 12(2) of the Companies Act of 2013.

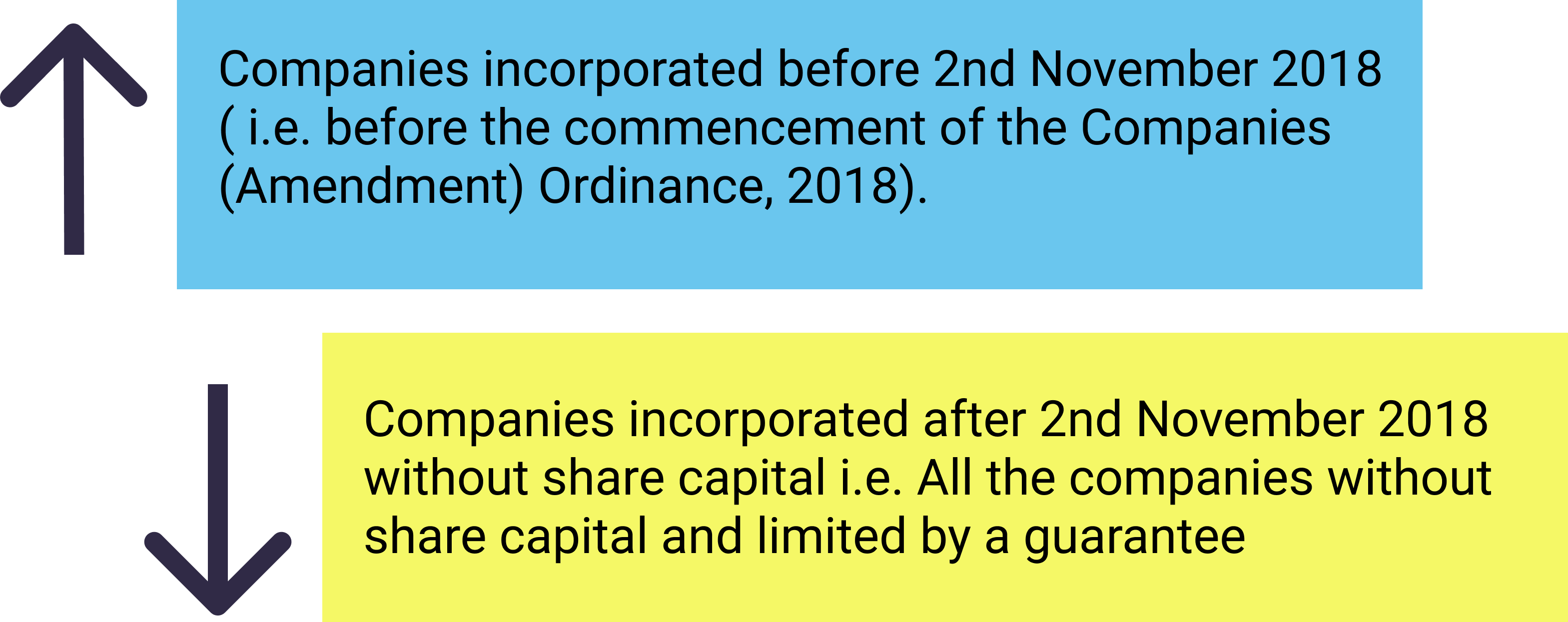

Companies which are not required to file Form 20A

The following companies are not required to file form 20A:

A company incorporated on or after 2nd of November 2018 and possessing a share capital hall not begin any business or exercise any borrowing powers until and unless a declaration of commencement of business is filed by a director (which is INC-20A). All the companies having Share Capital and incorporated on or after the Company (Amendment) Ordinance or 02/11/2018 needs to file a declaration in e-form INC-20A.

As per the Companies (Amendment) Ordinance 2018, there is a requirement for all the companies registered on or after 2nd November 2018 to file a certificate of commencement of business. Form 20A is a declaration filed by the directors/ owners with the ROC within 180 days of the date of incorporation of the company. It has to be verified by the practicing Chartered Accountant (CA), Company Secretary (CS), or Cost Management Accountant (CMA).

- Subject to the provisions of this Act, the memorandum and articles shall, when registered, bind the Company and the members thereof to the same extent as if they respectively had been signed by the company and by each member, and contained covenants on its and his part to observe all the provisions of the memorandum and of the articles.

- All monies payable by any member to the company under the memorandum or articles shall be a debt due from him to the company.

This is one of the most important compliances to follow as the penalties for non-filing is extremely high.

Time duration to submit E-form INC-20AWithin 180 days from the date of incorporation of the company, this form should be filed. It is time sensitive and only one-time filing.

Important note: MCA has now provided an additional time limit of 180 days for filing of the aforesaid declaration. It means all the newly incorporated companies can file form INC-20A within a period of 360 days from the date of its incorporation.

Benefits of filing Form 20A

Eligible for Borrowing Money:

Companies who file Form 20A, within 180 days of incorporation will automatically make it eligible to utilize their borrowing powers to raise funds from other sources, such as financial institutions, banks, etc. However, if companies fail to file Form 20A, it makes them ineligible to borrow money.

Avoid Fines & Penalties

Companies who file the form INC-20A within 180 days of incorporation can obtain protection from fines and penalties. When it comes to penalties, companies can fine up to 50,000/- per day of default and company directors 1000/- default per day, up to a maximum of 1,00,000/-

Authenticate the Business

Companies, who file the form INC-20A within 180 days of incorporation, are entered into a public database, with all information. The information is then available to the public, accessible at all times. Thus enabling the business to be authenticated by the public, this also helps in improving its credibility.

Consequences of not filing Form INC 20A

Penalty to be levied on the company: A penalty of 50,000 will be levied on the company if it fails to comply with the mentioned requirement.

Penalty to be levied on the officers: Every such officer in default shall be liable to a penalty of 1,000 per day for each day during which the default continues subject to a maximum of 1,00,000.

Registrar may initiate action for the removal of the name of Company

Company cannot borrow money

Company cannot start business

What are the required documents?

Following are the details and documents required:

Board Resolution:

- As per Section 10A, directors need to provide a Board Resolution for commencement of business.

Bank Statement of Company:

- Proof of payment by shareholders for the value of shares, as listed in the Memorandum of Association. For this purpose, it is mandatory to attach company bank account statements along with the form 20A.

Approval Letter:

- if any company requires approval from the Reserve Bank of India and Securities and Exchange Board of India then, it needs proof for the same.

Certification by CA/CS/CMA:

- The form is required to be verified and certified by a practicing Company Secretary, Chartered Accountant or Cost Accountant before filing it with the Registrar of Companies (ROC).

The registered office of the company has been verified –

- One has to make sure that the registered office of the company is established, before starting the business, by filing e-form INC-22 with MCA.

Other documents

- Certificate of Incorporation

- Digital Signature of Director

The e-Form is verified by a Practicing professional before filing with the ROC.

The form contains the declaration by the director of the Company that every subscriber to the memorandum has paid the value of the shares agreed to be taken by him and the company has filed with the Registrar a verification of its registered office as per section 12(2) of the Companies Act, 2013. Subscribers proof of payment for value of shares (Bank statement of company having all credit entries for receipt of subscription money received from all subscribers to MOA may be deemed fit)

A certificate of business commencement has to be obtained within 180 days from the date of incorporation and an e-Form has to be filed with the concerned ROC (Registrar Of Companies) regarding the same. A declaration under section 10A from the directors has to be provided in the form of a Board Resolution in the e-Form itself. In addition to this, a proof of deposit of the paid-up share capital by the subscribers also needs to be attached in the e-Form. If a company pursues objects requiring registration or approval from any sectoral regulators such as The Reserve Bank of India and Securities and Exchange Board of India etc, then it shall obtain such registration or approval along with the attached declaration. The e-Form has to be verified and certified by a practicing professional before filing with the ROC (Registrar Of Companies).

Preconditions for filing form

The first step is to open a company bank account (or a current account) for all its financial transactions. For which the following documents are required; Certificate of Incorporation, Memorandum of Association, Articles of Association, Permanent Account Number and Know Your Customer details of the company director/s. Separate bank account should be opened with the name of the company.

The company needs to collect the capital invested by the company shareholders, as mentioned in the final page of the company’s memorandum of association, including the list of shareholders and amount invested by each.

Once the capital invested by each shareholder is collected, it is deposited into the company bank account. Now, before filing a declaration of commencement of the business, the company has to acquire a certified copy of the bank statement, showing proof of deposit.

Directors of the company have to provide a declaration under section 10A in the form of board resolution.

Entries of deposited subscribed capital in a bank statement (subscribed at the time of incorporation), i.e. Also provide the proof of deposit of the paid-up share capital by the subscribers.

RBI issued registration certificate (only in case of NBFC) and from any other sectoral regulators if applicable.

One of the director’s digital signature certificate.

Form has to be certified by affixing the DSC of practicing professionals such as CS/CA/CMA.

Form has to be certified by affixing the DSC of practicing professionals such as CS/CA/CMA.

What is the Fee for Filing INC-20A?

Following is the fee applicable for INC-20A:

| Nominal Share Capital | Applicable Fees in |

| If the share capital is less than 1,00,000 | 200 |

| Above 1,00,000 and less than 5,00,000 | 300 |

| Above 5,00,000 and less than 25,00,000 | 400 |

| Above 25,00,000 and less than 1,00,00,000 | 500 |

| Above 1,00,00,000 | 600 |

In case, the company doesn’t have a share capital, (a company limited by guarantee is prerequisite to file such form) and is incorporated on or after 2nd of November 2018, the applicable fee is 200. Every company incorporated after 2nd Nov 2018 must submit the e-form INC-20A as INC 20A is Mandatory Declaration by Companies

Note: Without submitting the form of business commencement, the company would not be allowed to file any form. The registrar would initiate-Removal of the name of the company.Additional fee (in case the form is not filed within the time)

| Nominal Share Capital | Applicable Fees in () |

| Up to 30 days | 2 times of normal fees |

| Above 30 but not exceeding 60 days | 4 times of normal fees |

| Above 60 days but not exceeding 90 days | 6 times of normal fees |

| Above 90 days but not exceeding 180 days | 10 times of normal fees |

| Above 180 days | 12 times of normal fees |

MCA has now provided an additional time limit of 180 days for filing of the aforesaid declaration. It means all the newly incorporated companies can file form INC-20A within a period of 360 days from the date of its incorporation due to the present covid situations.

Procedure to File e-Form 20A

Go to the MCA Portal

Click on MCA Services. A dropdown box will appear in which select the option e filing.

Then many options will come, click on Company forms download Select Declaration of Commencement of Business

After this step a window will open and scroll down to the head “informational services”. There you can click on Form 20A to download with that you can also download instruction kit also.

Download the form. You can download the form with or without the Instruction Kit.Open it in PDF.Enter ‘Corporate Identity Number’ (CIN) of the company You may find CIN by entering the existing registration number or name of the company in the ‘Find CIN/GLN’ service at the MCA21 portal

The form will be downloaded in a pdf file. Open the form and fill in CIN (Corporate Identification Number). After this click on the “Pre fill” button which will automatically display the name, office address, email id of the company

Next step is to attach the required documents in the form and fill the declaration by providing DIN

Then after filling click on Check, the system will perform the form-level validation.

Then the form should be digitally signed by the director or authorized person and add DSC of the directors and certified professional in the form.

Add the DSC of the Directors and Certifying Professional in the form. The e-form should be digitally signed by the director or secretary of the company duly authorized by the board of directors or where the company has not appointed a secretary, by the company secretary in whole-time practice. Enter membership number or income-tax PAN in case the person digitally signing the e-Form is a secretary. Enter certificate of practice number in case person digitally signing the e-Form is a company secretary (whole time practice) and also select whether he/ she is an associate or fellow

Login to MCA portal again. Under MCA Services tab, click on upload e-forms. After successful upload, proceed to make payment of the fees. On successful payment, SRN will get generated.

The Declaration form is filed.

Part II – Instructions to fill the e-Form INC-20A Specific Instructions to fill the e-Form INC-20A at Field Level

Instructions to fill the e-Form are tabulated below at field level. Only important fields that require detailed instructions to be filled in e-Form are explained. Self-explanatory fields are not discussed.

| S. No/ Section Name | Field Name | Instructions | |

|---|---|---|---|

| 1. | (a) | Corporate identity number (CIN) of company Pre-fill button | Enter a Valid and ‘Active’ CIN of company having share capital and where the flag for filing commencement of business is enabled. Click the Pre-fill button. System will automatically display the name, address of the registered office and the email ID of the company. In case email ID is not prefilled automatically, then enter valid email ID. |

| 3. | (a) | Whether the affairs of the Company is regulated by any sectoral regulator (like RBI in case of NBFI activities) | Select the Radio button. |

| (b) | Specify the name of the regulator | Select one of the option from the drop-down values – IRDA / RBI / SEBI / Others if ‘Yes’ is selected in above field 3(a). | |

| Specify ‘Others’ | Enter the name of regulator if ‘Others’ is selected in field 3(b). | ||

| (c) | Specify the letter number/ registration number | Enter the letter number/ registration number if ‘Yes’ is selected in field 3(a). | |

| Date of approval/ registration | Enter the Date of approval/registration if ‘Yes’ is selected in field 3(a). | ||

| Attachments |

Any other information can be provided as an optional attachment(s). |

||

| Declaration | I am authorized by the Board of Directors of the Company vide resolution number ………………….. Dated ………… to sign…….. | Enter the serial number and date of board resolution authorizing the signatory to sign, give declaration and submit the e-Form. | |

| To be digitally signed by | Designation | Only Director of the company is allowed to sign this e-Form. | |

| DSC | The e-Form should be digitally signed by a director of the company. The person should have registered his/her DSC with MCA by using the following link (www.mca.gov.in). If not already register, then please register before signing this form. Disqualified Director should not sign the form. | ||

| Director identification number | Enter the approved DIN. | ||

| Certificate by practicing professional | This e-form needs to be verified by a practicing professional. Enter the details of the practicing professional and attach the digital signature. | ||

Common Instructions to fill e-Form INC-20A

| Buttons | Particulars |

|---|---|

| Pre-Fill | The Pre-fill button can appear more than once in an e-Form. The button appears next to a field that can be automatically filled using the MCA database. Click this button to populate the field. Note: You are required to be connected to the Internet to use the Pre-fill functionality. |

| Attach | Click this document to browse and select a document that needs to be attached to the e-Form. All the attachments should be scanned in pdf format. You have to click the attach button corresponding to the document you are making an attachment.In case you wish to attach any other document, please click the optional attach button. |

| Remove Attachment | You can view the attachments added to the e-Form in the List of attachment field. To remove any attachment from the e-Form, select the attachment in the List of attachment field and click the Remove attachment button. |

| Check Form |

Note: The Check Form functionality does not require Internet connectivity. |

| Modify |

The Modify button is enabled, after you have checked the e-Form using the Check Form button. To make changes to the filled and checked form:

|

| Pre scrutiny |

The Pre-scrutiny functionality requires Internet Connectivity. |

| Submit | This button is disabled at present. |

Part III – Important Points for Successful Submission of e-Form INC-20A Fee Rules

| S.No | Purpose of the form | Normal Fee | Additional Fee (Delay Fee) | Event Date | Time limit (days) for filing |

| 1. | Commencement of business and exercising borrowing powers | The Companies (Registration Offices and Fees) Rules, 2014 | The Companies (Registration Offices and Fees) Rules, 2014 | Date of incorporation of company | 180 days |

Note: Fees payable is subject to changes in pursuance of the Act or any rule or regulation made or notification issued thereunder.

Processing TypeThe e-Form will be auto approved (STP).

SRN GenerationOn successful submission of the e-Form INC-20A, SRN will be generated and shown to the user which will be used for future correspondence with MCA.

Challan GenerationOn successful submission of the e-Form INC-20A, challan will be generated depicting the details of the fees paid by the user to the Ministry. It is the acknowledgement to the user that the e-Form has been filed.

EmailWhen an e-Form is completely processed by the authority concerned, an acknowledgement of the same with related documents, if any, is sent to the user in the form of an email to the email id of the company.

Penalties for Default

The penalties for non-compliance are very high which has been done intentionally so as to curb out the number of shell companies incorporated. Following are the penalties for non-compliance:

Penalty to be levied on the company:

- A penalty of 50,000 will be levied on the company if it fails to comply with the mentioned requirement.

Penalty to be levied on the officers:

- Every such officer in default shall be liable to a penalty of 1,000 per day for each day during which the default continues subject to a maximum of 1,00,000.

Company strike-off:

- If the Registrar has reasonable grounds to believe that the company is not carrying on any business or operations even after 180 days of incorporation, the registrar may remove the name of the company from the Register of companies.

Companies which do not have acquired the commencement of business certificate will be denied submitting any ROC form with MCA. Further, substantial penalties will be levied for non-compliance from the company and directors as well.Suppose the company has not performed any business operation or activity according to the company’s registrar, who has a reason to believe so. In that case, the registrar is authorized to terminate the name of the company from his registrar. And the company will be labeled in the strike-out stage.

A company incorporated on or after 2nd of November 2018 and possessing a share capital (a company limited by guarantee is prerequisite to file such form) shall not begin any business or exercise any borrowing powers until and unless a declaration of commencement of business is filed by a director(which is INC-20A). This has been stated in Section 10A of the companies act in 2013.This form is submitted to familiarize MCA that subscribers have paid the value of the shares agreed to be taken by them as the date of submission on the form.

Appeal- As per the companies (adjudication of penalties) rules, 2014, ROC could not impose a lower fee considering of necessary precondition to levy the minimal penalty for adjudication. Nevertheless, the power to consider facts and diminish the amount of penalty is entitled to the regional director.

- Within the 60 days from receipt of the pronouncement order, an appeal to counter adjudication order can be filed with a particular regional director, ministry of corporate affairs.

- Forms to be submitted with MCA for appeal form no. ADJ (MoA – memorandum of appeal) must be lodged within 60 days from the date of adjudication order.

Declaration of commencement of Business at a glance

Section Atracts

10A of Companies Act 2013

Rule Attracts

23A of the Companies (Incorporation) Rules, 2014

Who needs to file the Form

Every Company incorporated on or after 2nd November, 2018) having share capital.

Time Limit

within 180 days from the date of incorporation and only one-time filing.

What to declare

Declaration that all the subscribers to the MOA have remitted the total value of the shares agreed to be taken by them in the Companies Bank Account.

Other declarations

In case company pursuing objects requiring registration or approval from any sectoral regulators such as RBI, SEBI etc, the registration or approval, as the case may be from such regulator shall also be obtained and attached with the declaration.

What to attached

The proof of receiving the subscription money in form of bank statement or if received in cash, attach the cash ledger. Here receiving cash amount must be check the limit allows by income tax act and others declaration as prescribed above like RBI, SEBI approvals if any.

Professional Certified by

This e-Form must be verified by a company Secretary or a chartered Accountant or a cost Accountant in practice

Penalty Provisions

Company can file such form INC-20A with Roc even after 180 days by paying additional fees as per fees rules.

Penalty On Company

the company shall be liable to a penalty of fifty thousand rupees.

Penalty on Officer in Default

every officer who is in default shall be liable to a penalty of one thousand rupees for each day during which such default continues but not exceeding an amount of one lakh rupees.

Power of ROC

If form not been filled within prescribed time period the Registrar may initiate action for the removal of the name of Company, on the grounds that company not carrying any business or operations.

Consequence if form is not filed within time:

Company cannot borrow money.

Company cannot start business

Important Practical Points related to this Form

No company can take any borrowings, raise any fund, do any agreement; make investment before filling form INC-20A, means not start any business activity.

Without filling INC-20A, company can change the directorship if the event held within 180 days from the date of incorporation but can’t do the same after lapse of 180 days of incorporation and can’t filled form DIR-12, in this regards the authority prospective that the company not start any business activity has not allowed to change the directorship.

Due to non filling form INC-20A, within 180 days or after 180 days from the date of incorporation, it is not allow the company to fill Form SH-7, MGT-14, charge related forms or any annual filling forms.

But it is noted that company can be strike off voluntary by filling form STK-2 who has not filed INC-20A within 180 days of incorporation. After a period of 180 days of incorporation, filing of form INC-20A is allowed to be filed first. Thereafter, they can file STK-2 if they desire so by following the relevant provisions of the Act relating to Strike off procedure.

No company changes its registered office before filling INC-20A.

Further there is the important point that after filling this form, no certificate has been generated by the authority. Only payment receipt is the proof of submitting the Form, further we can also check by view public documents on MCA the status of this Form.

This form is just a declaration made by the company to respective ROC that company have received the subscription money from the shareholders and take necessary approvals i.e. RBI, SEBI if any, and now the company started its business.

Conclusion

Staying compliant is vital to the longevity and health of the business wherein; filing INC-20A is the first step after the incorporation of the business. The next step is to maintain books of accounts to know the financial situation at the end of the year. Those Companies registered in India after the commencement of the Companies (Amendment) Ordinance, 2018 and having share capital is required to obtain the commencement of business certificate before commencing any business or exercising any borrowing powers. One can say that the Ministry has reintroduced the concept of Commencement of Business Certificate via Form INC-20A on MCA.

Form 20A is a declaration that needs to be filed by the directors of the company at the time of the commencement of the business. It should be verified by a Chartered Accountant (CA) or Company Secretary (CS) or a Cost Accountant in practice.In E-form 20A every subscriber to the MOA has paid the value of the shares agreed to be taken by him on the date of making of such declaration .and such contents of the said form shall be verified by a Company secretary or a Chartered Accountant or a cost accountant, in practice. Consequences of non-filing of Form-INC-20A may create hindrance for companies to start their business and also while borrowing of money. The company would be liable to a Penalty for late filing the Form INC-20A if it exceeds 180 days of from the date of incorporation.

Important Point in Regarding FORM INC-20A-- Filing of Form INC-20A is mandatory to obtain certificate of Commencement of business.

- All companies incorporated on or after 02/11/2018 and having share capital shall file Form INC-20A.

- Those companies who incorporate before 02/11/2018 and limited by guarantee not having share capital shall not require filing form INC-20A.

- Due date for the first time filing Form INC-20A is within 180days from the date of incorporation.

- If form INC-20A is not file on time then company liable to pay 50000 as a penalty and every officer who in default liable to pay 1000/- per day of default up to Maximum 100000.

- For Non-filing Form INC-20A within time then Company cannot start business and company cannot borrow money.

MCA has now provided an additional time limit of 180 days for filing of the aforesaid declaration. It means all the newly incorporated companies can file form INC-20A within a period of 360 days from the date of its incorporation due to covid situations.

Frequently Asked Questions

- 1. Is Form 20A a mandatory requirement and which companies are eligible to file it?

-

Yes, Form 20A is a mandatory requirement to declare the commencement of a business. As for the companies which are eligible to file form 20A, they are those that have been formed on or after 2 November, 2018, with a share capital.

- 2. Which companies are not eligible to file 'Form 20A'?

-

The companies which are eligible to file form 20A are those that have been formed before 2nd November, 2018, and have no share capital.

- 3. What is the due date for filing form 20A?

-

The due date for the first time filing of 'Form 20A' for companies incorporated on or after 2nd November 2018 within 180 days from date of incorporation.

- 4. What are the details required to be provided in 'Form 20A'?

-

The details required are that all shareholders (as listed in the MOA) have paid the total value of shares, as agreed by each shareholder.

- 5. What are the attachments to be included with form 20A?

-

Proof of payment by shareholders for the value of shares, as listed in the Memorandum of Association. For this purpose, company bank account statements are attached along with the form 20A.

- 6. What if the bank statement is not available?

-

In that case, instead of a bank account statement a valid payment proof like NEFT / IMPS receipts can be attached.

- 7. What is the penalty for not filing form 20A?

-

Companies that do not comply with the basic requirement of filing form 20A for the commencement of business, will have to file a penalty of 50,000/-Every company officer who is responsible for filing e-form INC 20A will be charged a penalty of 1,000/- day, for every day, until the form is filed and reaches the maximum amount of 1,00,000/-

- 8. What are the consequences of not filing form 20A within the stipulated time?

-

The ROC can remove a company name from the registry, if the company has not executed any business transaction or operation, after 180 days of registering the business.

- 9. How do I file condonation of delay for Inc-20A?

-

Currently, there is no foolproof process to file condonation of delay for INC-20A. So, we must wait for MCA clarification concerning this matter.

- 10. Where to get Form INC 20A?

-

Form INC 20A is available on the MCA portal.

- 11. Who is required to file INC 20A?

-

Directors of companies incorporated after 2nd Nov 2018 must file INC 20A.

- 12. What is INC 20A Form?

-

INC 20A is an e-form for declaration for commencement of business. Every company incorporated after 2nd Nov 2018 must submit the form INC-20A.

- 13. What is CIN?

-

The Corporate Identification Number (CIN) is 21 digits alpha-numeric code issued to companies on being registered by the Registrar of Companies (ROCs) situated in different states across India under the Ministry of Corporate Affairs (MCA). The CIN is the unique identification number of a company and must be entered in all the forms required to be filed by the company on the MCA portal.

- 14. What is ROC?

-

The Registrar of Companies (ROC) is an office under the MCA, which deals with the administration of companies in India. The Registrar of Companies (ROCs) is operating in all the major states/UT. The ROCs register companies across the states and the UTs, maintain a registry of records concerning companies that are registered with them and allow the general public to access this information on payment of a stipulated fee.

- 15. What are assets under charge?

-

A charge means a right or interest obtained by a creditor or lender in the property of the company by way of security that the company will pay back the debt. A company’s borrowings are backed by securities, on the strength of which loans are given to them by the banks and financial institutions. Assets under charge are the assets of the company upon which a charge is created for the company’s borrowing.

Every company creating or modifying a charge on its property or assets should register the particulars of charge with the ROC within 30 days of such creation. The company registration search provides the details of the assets under the charge of the company registered with the ROC.

- 16. What is DIN?

-

DIN or Director Identification Number is a unique Identification Number allotted to the person appointed as a director of a company. A DIN can be acquired by filling the SPICe form at the time of incorporation of the company.

- 17. What is the SPICe+ form?

-

The Simplified Proforma for Incorporating Company Electronically or SPICe+ helps incorporate a company with a single application for:

- The reservation of name;

- Application for allotment of DIN;

- Incorporation of a new company; and

- Allotment of PAN and TAN.

The form integrates many steps that were earlier individual forms into a single process and makes the company formation process time efficient.

- 18. What is DSC? Is it mandatory to file the SPICe+ (INC-32) and RUN?

-

DSC refers to a Digital Signature Certificate. It must be obtained from a certifying agency that has been recognized by the government. Since the registration process is now online, all the forms require a valid DSC. The cost of DSC acquisition may vary, largely depending on the certifying agency that it may be purchased from. To file a SPICe+ (INC–32) form, you need to have a DSC; however, for accessing the RUN and filing you do not require a DSC.

- 19. What is RUN?

-

Reservation of name or RUN is a web service used for reserving a name for a new company or to change the name for any existing company. However, from 23rd February 2020, the name of the company needs to be reserved in the SPICe+ form. RUN service is used to change the name of the company.