Export Promotion Capital Goods (EPCG) scheme - Introduction

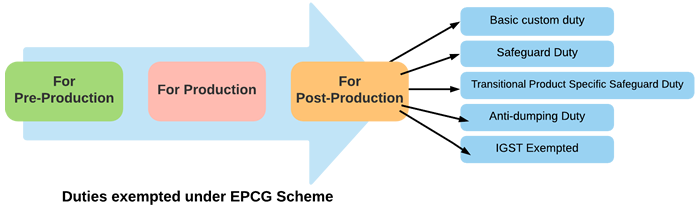

The Export Promotion Capital Goods (EPCG) scheme was introduced by the Directorate General of Foreign Trade (DGFT) under Chapter 5 of the Foreign Trade Policy (FTP) 2015-20. The idea behind the launch of this scheme was the facilitation of capital product imports so that Indian manufacturers can use them to produce quality goods. This scheme aims to improve India’s manufacturing prowess in the global market. EPCG Scheme allows import of capital goods (except those specified in the negative list in Appendix 5 F for pre-production, production and postproduction at zero customs duty. However, there is a compulsion on the business to bring in foreign currency which is equal to 600 per cent of duty saved on such importation measured in domestic currency. This is to be done within six years from availing of the Export Promotion Capital Goods Scheme.

Some services that were earlier allowed under the EPCG scheme were later discounted under the GST regime. As per FTP 2015-2020, Capital goods imported under EPCG Authorization for physical exports are also exempt from IGST and Compensation Cess upto 31.03.2020 only, leviable thereon under the subsection(7) and subsection (9) respectively, of section 3 of the Customs Tariff Act, 1975 (51 of 1975), as provided in the notification issued by Department of Revenue. The export promotion capital goods scheme can be availed on the import of capital goods during the pre-production, production, and post-production stage with nil customs duty. The scheme is applicable when the imported goods are:

- Capital goods under the definition provided in Chapter 9 of the FTP 2015-20, including those in semi-knocked down and completely knocked down condition

- Computer systems and software as parts/components of the capital goods

- Spares and tools, moulds, dies, fixtures, jigs and refractories

- Catalysts procured for the initial charge and one additional charge

- Capital goods for project imports, if notified by the Central Board of Excise and Customs

The objective of the EPCG Scheme is to facilitate the import of capital goods for producing quality goods and services and enhancing India’s manufacturing competitiveness. While advance licenses/authorizations were neutralizing the duty/tax incidence on ‘inputs’, the exporters earlier had no scheme to neutralize the duties/taxes paid on capital goods. Therefore, the EPCG Scheme aims at the procurement of capital goods duty/tax-free for exporters.

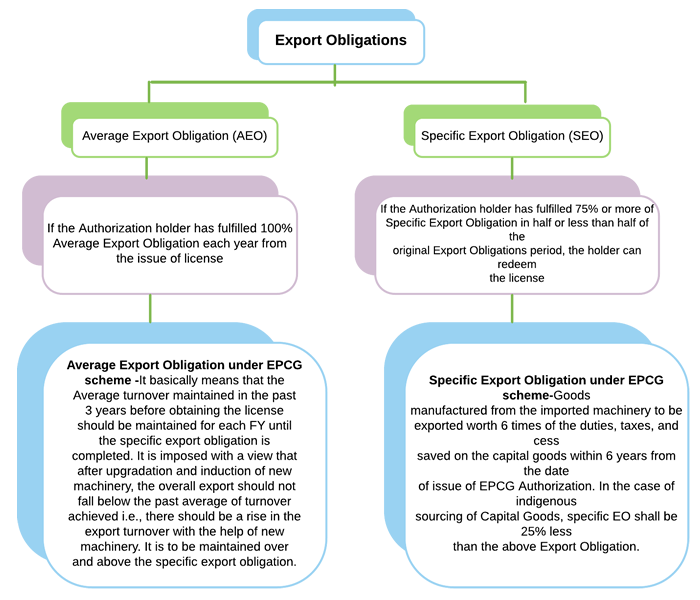

Export Obligation under EPCG SchemeExport Obligation (EO) is an arrangement used in the import of capital goods under the EPCG scheme. Such imports are made under an EO, which must be six times the duty that would otherwise be paid on the import of the capital goods. The EO must be fulfilled within six years from the date of issuance of the EPCG authorization. In the case of indigenous sourcing of capital goods, specific EO shall be 25% less than the stipulated EO (i.e. 5.4 times of notional duties, taxes and cess saved).

EO under the Scheme shall be, over and above, the average level of exports achieved by the applicant in the preceding three licensing years for the same and similar products within the overall EO period. Such average would be the arithmetic mean of export performance in the preceding three licensing years for the same and similar products. Some conditions for EPCG export obligation calculation are to be fulfilled as follows:

- The export obligation is to be fulfilled by the authorization holder through the export of products manufactured by themselves or through their supporting manufacturer/services i.e. Export Obligation under EPCG Scheme should only be fulfilled by the export of goods manufactured from the Imported/Domestically procured Machinery

- The export obligation under EPCG shall be over and above the average export volume for the previous three licensing years for the product(s) similar to it within the EO period, including extensions if any.

- While calculating the EO volume, shipments made under advance authorization, duty-free import authorization (DFIA), drawback scheme, MEIS and SEIS will also be considered.

- Royalty payment for R&D services received in freely convertible currency and foreign exchange is also counted while calculating exports under the EPCG scheme.

- Deemed exports, as defined in Chapter 7 of FTP 2015-20 are considered as a fulfillment towards EO. The benefits of deemed exports are also available to the exporter.

- An authorization received under the EPCG scheme remains active for 18 months from the date of its issue, and cannot be revalidated thereafter.

- Only 25% of EO is required for units located in Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and J&K.

- If the authorization holder completes 75% of the EO in less than half of the EO period, the remaining 25% is waived.

Only 75% of the EO is required for export of green technology products.

We can extend the Export Obligation period by two years after completion of 6 Years (6+2=8 Years). We can extend by paying a composition of 5% for the first year and 10% for the second year on the proportionate Duty saved value on pending / unfulfilled Export Obligation. But the minimum composition fee to be paid is ₹ 10,000/-. Alternatively, if the Exporter doesn’t want to pay the composition fees and has procured new export orders, he can enhance the EO by 10%/20% for the first/second-year respectively. In such cases, no composition fees will be required.

Capital Goods allowed under EPCG Scheme

As we all know that due to the heavy custom duties, companies have to pay on the Capital machinery imported for the production requirements, due to which businessmen usually do not import them and compromise with the quality of the goods. The higher the price of the Machinery used to be, the higher the custom duty was, and this functionality started affecting the competitiveness and quality of manufacturing industries deeply. To improve this situation, The Government of India came up with a scheme where it was allowed to import capital goods at zero customs duty. EPCG Scheme was introduced by the Government of India to facilitate the Import of Capital Goods/Machinery for producing high-quality goods and services. The main aim of the EPCG Scheme is to improve India’s competitiveness in the manufacturing sector. Under the EPCG Scheme, below are the Type of Capital Goods / Machinery eligible for Import

- All the capital goods, including semi-knocked down and complete, knocked down conditioned goods.

- All the software and computer systems included in the capital goods that are imported.

- Moulds, spares, jigs, dies, tools, fixtures, and refractories.

- Catalysts for initial charge along with one subsequent charge.

As per para 9.08 of FTP 2015-20, “Capital Goods” are defined as “any plant, machinery, equipment or accessories required for manufacture or production, either directly or indirectly, of goods or for rendering services, including those required for replacement, modernization, technological up-gradation or expansion. It includes packaging machinery and equipment, refrigeration equipment, power generating sets, machine tools, equipment, and instruments for testing, research and development, quality, and pollution control. Capital goods may be for use in manufacturing, mining, agriculture, aquaculture, animal husbandry, floriculture, horticulture, pisciculture, poultry, sericulture, and viticulture as well as for use in the services sector.”

Export Promotion Capital Goods are capital goods used in the production of goods that are exported to other countries. It includes machinery as well as spares. Hence, to qualify as Export Promotion Capital Goods, the commodity manufactured in India must be exported outside India. The capital goods allowed under Export Promotion Capital Goods Scheme shall include spares (including reconditioned/ refurbished), fixtures, jigs, tool, moulds and dies. Under this scheme of Foreign Trade Policy (FTP), importation of capital goods required for the manufacturing of export-oriented product specified in the Export Promotion Capital Goods Authorization is permitted at concessional/nil rate of duty. This scheme under Foreign Trade Policy allows technological up-gradation of the indigenous industry.

Export Promotion Capital Goods (EPCG) Authorizations are issued by licensing authority – Director General of Foreign Trade (DGFT) based on the certificate issued by an Independent chartered engineer. Few of the items on which Customs Duty Rates are revised are as follows: –

Reduced duty on copper scrap from 5% to 2.5%

- Basic and Special additional excise duty on petrol and high-speed diesel oil (both branded and unbranded) is reduced

- Increased duty on solar inverters from 5% to 20%

- Raised duty on solar lanterns from 5% to 15%

- The basic customs duty on gold and silver reduced.

- The department will rationalize duty on textile, chemicals and other products

The revised rates will be applicable from 2nd February 2021 onwards.

How to apply for an EPCG License?

In order to obtain a License under the EPCG scheme, it is a primary requirement to file an application with the licensing authority of the Director General of Foreign Trade. The application shall be attached with the required documents along with the company and personal details. The issuing authority is the licensing authority – Director General of Foreign Trade (DGFT).

To avail of the benefits of the EPCG License, the exporter has to file an application with the DGFT. To apply for this incentive, fill up the Ayat Niryat Form 5B (ANF 5B) along with the following documents:

- Permanent Account Number (PAN)

- Digital Signature Certificate

- Copy of Import Export Code (IEC), Registration-cum-membership certificate (RCMC), MSME & Central Excise Registration (if registered) & GST registration certificate

- Details of Capital Goods sought to be imported with HSN code/Name, Model Number, and Technical Description.

- List of Products to be exported using the above machinery with HSN code

- Chartered engineer’s certificate (along with original for verification) showing the nexus between the Capital Goods and the products to be exported in the format given in Appendix 5A.

- CA certificate (along with original for verification) indicating the last three financial year turnover in USD & INR only for the above mentioned Export Products i.e. Certificate of Chartered Accountant / Cost Accountant / Company Secretary in Appendix 5B.

- Factory Address where the machine will be installed.

- Stepwise Process/Flow Chart indicating the stages where the capital goods are to be used.

- End-use of Capital Goods for Export products and stage where and how to be used. (Detailed Explanation)

- Company brochure

- Performa invoice/ Purchase order of the Capital Goods/Machinery.

- Such other documents as may be prescribed by DGFT from time to time

- Registration certificate from Tourism Department

- Treasury Receipt Challan (if fee has not been paid electronically) evidencing payment of application fee in terms of Appendix 2L.

- Self-certified copy of MSME/IEM/LOI/IL in case of products or a self-certified copy of Service Tax Registration in case of Service Providers. (In case of Service Providers, who are not registered with Service Tax authorities, a declaration in this regard will be submitted as a part of the application (declaration no. 6), service tax registration is not required to be submitted. In such cases RCMC from EPC concerned will suffice).

All these documents must be self-certified copies.

- A manufacturing exporter who doesn’t have other similar supporting exporters.

- A merchant exporte with supporting manufacturer and/or service provider.

- Common service providers (CSP), as certified or assigned by the DGFT, Department of Commerce, or State Industrial Infrastructure Corporation./li>

The CSP will have to meet the conditions of the Export Obligation, and its shipping bills must contain the details of the EPCG authorization.

The exporter must inform the concerned authority about CSP activities before it begins exporting.

The CSP will provide bank guarantee equal to the customs duty saved, against the export goods.

There are two types of Export Obligations – Average Export Obligation and Specific Export Obligation. We have to maintain both the obligation. While maintaining specific export obligations, we have to fulfill block-wise as per given below table and same we have to submit to DGFT.

| Period from the date of issue of EPCG License | Minimum specific export obligation fulfilled |

|---|---|

| 1st Block(1st to 4th year) | 50% |

| 2nd Block(5th and 6th year) | Balance/ Pending Specific EO |

If the Authorization holder has fulfilled 100% Average Export Obligation each year from the issue of license and 75% or more of Specific Export Obligation in half or less than half of the original Export Obligations period, the holder can redeem the license as per para 5.09 FTP.

Export Obligations in a nutshell

Export Obligations equivalent to 6 times of duties, taxes and cess saved on import of Capital goods to be fulfilled in 6 years reckoned from the date of issue of authorization

Trounle obtaining credit

Most investors, banks or lenders will do a primary check to see if the applicant has got any basic licenses in order. Any busniess planning to scale to a greater level must apply for the license based on predicted sales/capacity.

In case of integrated tax and compensation cess are paid in cash on imports under EPCG, incidence of the said integrated tax and compensation cess would not be taken for computation of net duty saved provided that Input Tax Credit is not availed

Exemption from the maintenance of Average Export Obligations

The authorization holder would intimate the Regional Authority on the fulfillment of the export obligation, as well as average exports, within three months of completion of the block, by secured electronic filing using digital signatures. The authorization holder shall submit to RA concerned by 30th April of every year, report on the fulfillment of export obligation by secured electronic filing using digital signatures/ or hard copy thereof.

- For exporters of ‘green technology products’, specific EO shall be 75% of EO. Green technology products are: equipment for solar energy de-centralized and grid connected products, bio-mass gassifier, bio-mass or waste boiler, vapor absorption chillers, waste heat boiler, waste heat recovery units, unfired heat recovery steam generators, wind turbine, solar collector and parts thereof, water treatment plants, wind mill and wind mill turbine or engine, other generating sets - wind powered, electrically operated vehicles – motor cars, electrically operated vehicles – lorries and trucks, electrically operated vehicles – motor cycle and mopeds, and solar cells.

- For units located in Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, and Jammu & Kashmir, specific EO shall be 25% of the EO.

- The Export obligation can be fulfilled by direct exports, deemed exports, supply to SEZ, EOU Units, etc., Third Party exports, service exports in case of service providers.

Note: If the EPCG License holder intends to pay the IGST & Compensation cess while importing, then the net duty saved amount would be reduced accordingly, which will, in turn, reduce the obligation. However, this facility can only be availed on the condition that tax credit of IGST will not be taken by the Exporter.

If the EPCG Scheme is availed for the below mentioned Export products, then the average export obligation will be exempted:

- Handicrafts,

- Handlooms,

- Cottage & Tiny sector

- Agriculture

- Aqua-culture (including Fisheries), Pisciculture

- Animal husbandry,

- Floriculture & Horticulture,

- Poultry,

- Viticulture,

- Sericulture,

- Carpets,

- Coir, and

- Jute.

Apart from the exemption to the above sectors, relaxation is also provided to such sectors where the global growth rate has declined more than 5% for a particular FY.

The next step after Export Obligation is fulfilled is to close the EPCG License and apply for redemption/ Closure. We need to fill the redemption Form ANF 5B along with the specified documents mentioned in the form and submit it with the original license at the DGFT RA for Closure.

EPCG Redemption or EPCG License closure procedure is a mechanism through which the DGFT monitors the fulfillment of the export obligation given to holder by the Government. We can help you in closure of EPCG License by preparing correct documents as per DGFT Rule.

The License holder has to fill the redemption form of ANF 5B with the relevant documents mentioned and submit to DGFT RA. The DGFT will issue a closure certificate called Export Obligation Discharge Certificate.

We can surrender the EPCG License, if the holder does not want to import capital goods by submitting the relevant documents.

EPCG authorization at a glance

- EPCG authorization shall be valid for import for 18 months from the date of issue of authorization. Revalidation of EPCG authorization is not permitted.

- Export obligation period of 6 years is reckoned from the date of issue of the authorization

- Manufacturer exporters with or without supporting manufacturer(s).

- Merchant exporters tied to supporting manufacturer(s).

- A service provider who is designated/certified as a Common Service Provider (CSP) by the DGFT.

Additional items for import under EPCG Scheme for service providers

EPCG Scheme is available for manufacture as well for service providers like the hospital, hotel, university, etc., Following are the additional benefits to service providers under the EPCG scheme:

| Import of Capital Goods namely | Permissible for imports |

|---|---|

| Furniture, carpets, crockery, marble, chandelier, tiles, flooring, doors for rooms, fixing panels. | Permitted only for the hotel industry |

| Furniture and fixtures, flooring material, and furnishing material | Permitted for hospitals |

| Construction equipment’s viz. cranes etc. | Permitted only for Services Providers |

Following conditions shall apply to the fulfillment of EO:

- The authorization holder shall fulfill the EO by the export of goods or services which are manufactured or rendered by him or his supporting manufacturer.

- Shipments under the advance authorization, DFIA, drawback scheme or reward schemes under Chapter 3 of FTP would also be counted for the fulfillment of EO under EPCG Scheme.

- Import of restricted items is permitted under EPCG Scheme only after approval from Exim Facilitation Committee (EFC) at DGFT Headquarters.

- Export of restricted items is permitted under EPCG Scheme only after approval from Exim Facilitation Committee (EFC) at DGFT Headquarters.

- Import of capital goods for project imports is permitted under EPCG Scheme.

- Imported capital goods shall be subject to actual user condition till export obligation is completed and EODC is granted, which means imported capital goods is non-transferable till export obligation is completed and EODC is granted.

Application for grant of authorization shall be made in Form ANF 5A along with ‘nexus certificate’ from an independent Chartered Engineer (CEC) in Appendix 5A.

- The importer executes a bond in such form and for such sum and with such surety or security as may be specified by the Deputy Commissioner of Customs or Assistant Commissioner of Customs binding himself to comply with all the conditions of Customs notification as well as to fulfill an export obligation.

- The CSP(common service provider) shall execute the bond with bank guarantee and the bank guarantee shall be equivalent to 100% of the duty foregone, and the bank guarantee shall be given by CSP or by any one of the users or a combination thereof, at the option of the CSP.

- The capital goods imported, assembled, or manufactured are installed and put to use, after their import, in the importer’s factory or premises.

- Where the specified capital goods imported are found defective or unfit for use, the said goods may be re-exported to the foreign supplier within three years from the date of clearance of said goods.

- In case of direct export, EO is calculated as 6 times of actual duty saved value.

- And in domestic sourcing, EO is calculated as 6 times of duty save value calculated as per notional custom duty on FOR Value.

Certificate of Installation of Capital Goods

The authorization holder shall submit to the concerned RA, within six months from the date of completion of import, a certificate from the jurisdictional Customs authority or an independent Chartered Engineer, at the option of the authorization holder, confirming installation of capital goods at factory/ premises of authorization holder or his supporting manufacturer(s).

| Appendix | Description |

|---|---|

| Appendix 5A | Format of Chartered Engineer Certificate for nexus under EPCG Scheme |

| Appendix 5B | Certificate of Chartered Accountants/Cost Accountants/ Company Secretary (for the issue of EPCG authorization) |

| Appendix 5C | Certificate of Chartered Accountants/Cost Accountants/ Company Secretary (for the redemption of EPCG authorization/ issuance of post export EPCG duty credit scrip) |

| Appendix 5D | The export obligation under EPCG Scheme – List of services for which payments received in Indian Rupees terms. |

| Appendix 5E | Computation of annual average Export Obligation under EPCG Scheme |

| Appendix 5F | List of capital goods not permitted/ permitted for import subject to specific conditions under the EPCG scheme. |

| ANF-5A | Application form for issuance of EPCG/ Post Export EPCG authorization. |

| ANF-5B | Application form for the redemption of EPCG authorization/ post export EPCG duty credit scrip. |

| ANF-5C | Application for clubbing of EPCG authorization. |

- Extension of the time limit-The Extension of the time limit is available but only in exceptional cases where the exporter has sufficient evidence/proof to prove that the factors were beyond his control in order to meet the deadline.

- Penalty in case of Non-Compliance- In cases where the license holder under the EPCG scheme fails to fulfill the stipulated export obligation then the licensee shall be liable to pay the customs dues along with 15% interest per annum to the customs authority.

- Selling goods in the Domestic Tariff Area (DTA)- Selling goods in the Domestic Tariff Area (DTA)- Where the exporter as per his export obligation meets the deadline then only this business can sell the goods in the Domestic Tariff Area.

- Exemption from IGST & Compensation Cess under EPCG scheme- In the Goods and Services Tax regime, merchant exporters need to pay IGST and claim a refund for the same. The DGFT vide Notification No. 54/2015-20 has amended the FTP (Foreign Trade Policy) and has extended IGST and Compensation Tax exemption under EPCG Scheme till October 01, 2018. This move would offer much-needed relief to exporters who are under the stress with respect to refunds under the GST regime.

- EPCG authorization holder can export (goods manufactured/services rendered) either directly or through third party (Deemed Export).

- Royalty payments received in freely convertible currency and foreign exchange received for R&D services shall also be counted for discharge under EPCG.

- Shipments under Advance Authorization, DFIA, Drawback Schemes or reward Schemes would also count for fulfillment of Export Obligation.

- Deemed export is counted towards fulfillment of Export Obligation under EPCG Scheme. Supply to EOU/STP/EHTP/BTP Unit is called as deemed export and can be counted towards EO Fulfillment along with supply to SEZ units

Third Party Exports

Third-party Exports can be counted for Export Obligation (EO) fulfillment but in such cases Shipping Bill / Bill of Exports should contain the name of Third Party along with EPCG Authorization number where the names of both Authorization holder and supporting manufacturer are indicated in export documents like Shipping Bill/ Bill of Exports etc. along with EPCG authorization number.

Provision 5.7.1 of the EPCG Scheme relating to Third Party Exports contains “

- EPCG authorization holder shall export either directly or through third party(ies). If a merchant exporter is EPCG authorization holder, name of supporting manufacturer shall also be indicated on shipping bills.

- At the time of export, EPCG authorization number and date shall be endorsed on shipping bills which are proposed to be presented towards discharge of export obligation.”

Thus, Third Party Exports are allowed under this scheme, for e.g. a company that specializes in manufacturing cotton on imported machinery can either export the finished goods itself and then show this in its own name, or it can accomplish the export through a sale to a third party, which can still be considered a fulfillment of its own export obligation, provided the export has been completed on the finished good it manufactured using the machinery that was imported. What the company cannot do, however, is try to show or claim the discharge of the export obligation on goods or products that are in no way related to what it itself has manufactured, as we will see below.

EPCG is intended to promote exports and the Government through this scheme provides incentives and other financial assistance to Exporters. Heavy exporters can take advantage of this provision but it is ill-advised for those who do not expect to manufacture very much or intend to sell their produce almost entirely in the domestic market to go ahead for this scheme, as that could lead to extreme pressure and almost impossible-to-fulfill obligations later on. Each business should take this call carefully and not without a detailed written analysis of expected export amount.

What sort of Goods and Services does EPCG Scheme apply to?EPCG is a scheme that is primarily related to machinery, machinery parts and similar goods. Any company that is involved in manufacturing sector or in heavy production that would like to import machineries for its factories from a foreign country can consider this scheme. It is not, however, limited only to such companies as the government even wishes to include service providers under this scheme, “Alternatively, export obligation may also be fulfilled by exports of other good(s) manufactured or service(s) provided by the same firm/company or group company/ managed hotel which has the EPCG license. The incremental exports to be fulfilled by the license holder for fulfilling the remaining export obligation can include any combination of exports of the original product/ service and the substitute product (s)/ service (s). The exporter of goods can opt to get the export obligation refixed for the export of services and vice versa.” In this case, bills that document the services charged to companies or clients abroad are sufficient for satisfying the export obligation.

Benefit of EPCG License

The main benefit of the EPCG Scheme is importing capital goods with zero customs duty.

- Eligibility Criteria for applying under EPCG Scheme- Benefits under EPCG Scheme can be applied by any Exporter irrespective of his turnover.

Benefit of EPCG License

Manufacturer Exporter is eligible to apply for EPCG License. But Capital Goods imported under EPCG scheme comes with an actual user condition till the export obligation is completed. It means that the capital goods cannot be sold or transferred until the obligation is completed.

Merchant Exporter tied with supporting manufacturer is eligible to apply for EPCG License. Supporting Manufacturer’s Name and his factory address where the capital goods are proposed to be installed should be endorsed on the EPCG License. Merchant exporter while discharging his export obligation should indicate the name & address of supporting manufacturer in all his shipping documents i.e. shipping bill, Custom Invoice etc.

Various service exporters can take EPCG License to reduce capital cost. Service Exporter like Hotels, Tour Operators, Taxi Operators, Logistics Companies, Construction Companies can utilize the EPCG Scheme by importing / procuring domestically capital goods duty-free.

Capital Goods under EPCG Scheme can be imported at zero customs duty. However, it must be noted that IGST and Compensation cess is exempted only up to 31.03.2021. The Government may extend the date through a notification issued from time to time. Capital Goods under EPCG Scheme can also be procured from indigenous sources (i.e., from domestic suppliers). In such cases, applicable GST for the supply would be exempted.

The Exporter can also indigenously procure capital goods from a domestic manufacturer. Such domestic manufacturers shall be eligible for deemed export benefits under paragraph 7.03 of FTP. An EPCG authorization holder can source capital goods from a domestic manufacturer and claim deemed export benefit under the FTP. Domestic sourcing from export-oriented units is also permitted under the scheme. An EPCG authorization holder can opt for technological upgradation of capital goods that have been procured under the scheme. Deemed export is counted towards fulfillment of Export Obligation under EPCG Scheme. Supply to EOU/STP/EHTP/BTP Unit is called as deemed export and can be counted towards EO Fulfillment along with supply to SEZ units.

Fulfilling the EO is a basic precondition under the EPCG scheme. Heavy exporters are naturally better placed to fulfill this obligation and benefit from the EPCG. Therefore, it should be availed of only when production is in sizeable volumes, and one is confident of exporting the product overseas.

How to obtain an EPCG License?

- EPCG Scheme is a part of foreign trade policy of Government of India.

- EPCG scheme allows import of capital goods including spares for pre-production, production and post production at 0% custom duty.

- EPCG Authorization holder may also source capital goods from a domestic manufacturer. Such domestic manufacturer shall be eligible for deemed export benefit under FTP.

- License under this scheme shall not be issued for the import of any capital goods for Electricity Generations or Supply plants.

- Import of second hand capital goods are not permitted under the EPCG scheme.

- The EPCG License authorization shall be valid for a period of 18 months from the date of authorization. Revalidation of the EPCG authorization shall not be permitted.

To obtain an EPCG License, it is necessary to file an application toward that purpose with the licensing authority –Director General of Foreign Trade (DGFT) along with supporting documents and company and personal details and history.

Based on the amount of import duty exemption, the value addition is fixed up and export obligation has to be fulfilled accordingly.

If the export obligation was genuinely unable to be completed in the time specified by licensing authority, it may be permitted to get the export obligation period extended for further period of time. However, if the export obligation has been finished, all manufactured goods henceforth can be sold locally as well in the domestic tariff area (DTA). Hence, businesses must first seek to fulfill their obligations in foreign markets before they seek to exploit favorable conditions at home.

It supports exporters who earn foreign currency in various levels of financial assistance, exemption of import duty etc. In this case, the machineries that are being imported are used for manufacturing of goods which are required to be exported so as to earn foreign exchange. However, this requires a significant initial outlay of cash nonetheless and the benefits of the machinery will accrue slowly in the coming years only. Apart from other financial assistance for exporters, an almost complete exemption of the import duty amount while importing such machineries can be obtained. When applying for EPCG license from government, the guarantee is that the company will export the required amount or quantity of goods within the stipulated time. EPCG is a good facility provided to exporters and importers by government on exemption of import duty amount.

To incentivize fast track companies to accelerate exports, there is a provision for early redemption and in cases where Authorization holder has fulfilled 75% or more of specific export obligation and 100% of Average Export Obligation till date, if any, in half or less than half the original export obligation period specified, remaining export obligation shall be condoned.

Authorization holder is required to submit to RA concerned by 30th April of every year, report on fulfillment of export obligation.The scheme allows one or more requests for grant of extension in export obligation period, on payment of composition fee equal to 2% of proportionate duty saved amount on unfulfilled export obligation or an enhancement in export obligation imposed to the extent of 10% of total export obligation imposed under authorization, as the case may be, at the choice of exporter, for each year of extension sought. Such first extension in EO period can be for a maximum period of 2 years. Extension in EO period beyond two years’ period may be considered, for a further extension upto 2 years with a condition that 50% of duty payable in proportion to the unfulfilled export obligation is paid by authorization holder to Custom authorities before an endorsement of extension is made on EPCG authorization by RA concerned. In such cases, no composition fee is to be paid or additional EO is to be imposed. In case the firm is still not able to complete the export obligation, duty already deposited will be deducted from total duty plus interest to be paid for EO default.

In case, EPCG authorization holder fails to fulfill prescribed export obligation, he shall pay duties of Customs plus interest as prescribed by Customs authority. This facility can also be availed by EPCG authorization holder to exit at his option.

The EPCG Scheme provides for in addition, a specific EO of 75% of normal Export Obligation for export of Green Technology Products. The scheme also provides for Post Export EPCG duty credit scrip(s) which are available to exporters who intend to import capital goods on full payment of applicable duties in cash and choose to opt for this scheme. Further, for units located in Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Jammu &Kashmir, specific EO shall be 25% of the EO

EPCG License procedure

Apply for EPCG License-file an application with the DGFT

Indicate clearly the export items to be manufactured out of the imported machinery/capital goods.

Get EPCG License from the DGFT-import of capital goods has to be completed within 18 months of obtaining the EPCG License .The Revalidation of EPCG Authorization will not be permitted.

Register the said license at custom & execute a bond or bank guarantee (BG). At the time of import , a bond or bank guarntee has to be executed with customs authorities, as per applicable provisions.

Import of machinery or capital goods at 0% import duty

Install the machinery and obtain the installation certificate-After the installation of the capital goods, it is mandatory to obtain the instaalation certificate if the imported machinery by an independent Chartered Engineer and the same has to be submitted to DGFT.

Complete the export obligation in 6 yearsIn order to incentivize fast-track exporters, if 75% of specific export obligation & amp, 100% average export obligation is fulfilled in half or less than half of the export obligation period, then the remaining obligation shall be condoned and the EPCG License shall be closed by the concerned authorities.

Submit to DGFT for EODC/ closure of license

Obtain EODC from DGFT

Submit EODC/ Closure Letter to customs and cancel the bond/redeem the Bank Guarantee (BG).After completion of export obligation , a redemption letter has to be obtained from the concerned regional authority of DGFT.

Apply for an EPCG License online

The Applicant should submit an online application to DGFT to get EPCG License.

Visit the DGFT Official website-www.dgft.gov.in

Login the DSC-> select Services->Online E-com Application

Click on EPCG (0%)

Fill all the details and upload the necessary documents

Import of machinery or capital goods at 0% import duty

Kindly note the following important points to be noted to make the sure the documents are prepared erroe-free

- IEC/RCMC should show the applicant as a manufacturer exporter.

- IEC/RCMC should have the address where the machine is proposed to be installed

- MSME/SSI/,anufacturing proof should have export products listed in the EPCG License.

After filling all the details, submit the application.

After a successful application, DGFT will issue the EPCG License

Compliances to be followed after obtaining an EPCG License from DGFT

After obtaining an EPCG license from DGFT, it has to be registered at Customs. Once capital goods are cleared duty-free from Customs, it has to be installed at the said factory premises. An Installation Certificate has to be obtained from the Independent Chartered Engineer or Customs authority as a proof of Installation & commissioning. Once production starts, applicant should complete the export obligation in given time frame and submit all the export documents to DGFT office to close the EPCG license.

EPCG Authorization holder needs to install the capital goods imported within a period of six months in front of an Independent Chartered Engineer. The chartered engineer will check that as per the authorization capital goods have been installed in given factory / supporting manufacturer premises or not and also cross verify the capital goods imported details with the license. And as per the verification, he will generate a certificate mentioning company name, Imported capital goods with quantity, BOE details, capital goods installation date on his letterhead with signed and stamped. The certificate generated by an Independent Chartered engineer is called the Installation Certificate. The same original copy should be submitted in DGFT and customs and receive the acknowledgment for the same.

Conditions where EPCG authorizations can be clubbed together

- All the authorizations have been issued to the same authorization holder.

- Application for clubbing shall be made to the Regional Authority of the DGFT in Form ANF-5C.

- Export products of all the authorizations shall be the same or similar.

- The total export obligation would be re-fixed taking into account the total duty saved amount of the clubbed authorizations.

- On clubbing, authorizations for all-purpose shall be deemed to be a single EPCG authorization.

- The export obligation period shall be reckoned from the first authorization issue date.

- The average obligation shall be highest among all the clubbed authorizations.

- Clubbing would be permitted during valid EOP including an extended period if any.

Note: Post export EPCG duty credit scrip(s) shall be available to exporters who intend to import capital goods on full payment of applicable duties, taxes, and cess in cash and choose to opt for this scheme. Basic customs duty paid on capital goods shall be remitted in the form of freely transferable duty credit scrip(s).

Power of Regional Authority to extend the export obligation period under EPCG

The Regional Authority is empowered to extend upto two extensions of one year each in the export obligation period under EPCG.

- on payment of composition fee equal to 5% and 10% respectively of proportionate duty saved amount on unfulfilled export obligation for the first/second year of extension; or

- on enhancement in export obligation imposed to the extent of 10%/ 20% respectively of the total export obligation imposed under the authorizations for first/second year of the extension. as the case may be, at the choice of the exporter.

Implications of Failure of Export Obligation

- In case, EPCG authorization holder fails to fulfill prescribed export obligation, he shall pay duties of Customs plus interest as prescribed by Customs authority. This facility can also be availed by EPCG authorization holder to exit at his option.

- The scheme allows one or more requests for grant of extension in export obligation period, on payment of composition fee equal to 2% of proportionate duty saved amount on unfulfilled export obligation or an enhancement in export obligation imposed to the extent of 10% of total export obligation imposed under authorization, as the case may be, at the choice of exporter, for each year of extension sought. Such first extension in EO period can be for a maximum period of 2 years.

- Extension in EO period beyond two years’ period may be considered, for a further extension upto 2 years with a condition that 50% of duty payable in proportion to the unfulfilled export obligation is paid by authorization holder to Custom authorities before an endorsement of extension is made on EPCG authorization by RA concerned. In such cases, no composition fee is to be paid or additional EO is to be imposed. In case the firm is still not able to complete the export obligation, duty already deposited will be deducted from total duty plus interest to be paid for EO default.

- If Average Export Obligation is not fulfilled, but Specific EO is fulfilled, Then Entire duty saved amount with 15% annual interest should be paid at Customs and submit the proof of duty paid to DGFT for regularization.

- If the authorization holder failed to fulfill the specific export obligation but maintained average export obligation, the holder has to pay proportionate Duty Saved Amount with 15% annual interest on pending specific export obligation on actual imported capital goods at customs and submit the proof of duty paid to license authority concerned.

EPCG Redemption

After Export Obligation is fulfilled, The next step is to close the EPCG License and apply for redemption/Closure. We need to fill the redemption form ANF 5B along with the specified documents mentioned in the form and submit it with the original license at the DGFT RA for Closure. EPCG Redemption or EPCG License closure procedure is a mechanism through which the DGFT monitors the fulfillment of the export obligation given to holder by the Government.

The License holder has to fill the redemption form of ANF 5B with the relevant documents mentioned and submit to DGFT RA. The DGFT will issue a closure certificate called Export Obligation Discharge Certificate.

Conclusion

EPCG License, like the Importer Exporter Code, is of interest and concern for indigenous businesses that either import from or export heavily to companies abroad. It is a scheme introduced by the government to incentivize exports and can serve to benefit industries and companies of all sorts in all sectors. It consists in the waiving of import duty on products imported in return for performance or discharge of an export requirement or obligation to the tune of several times the import duty saved within a preset time. Specifically, the government grants Import Duty at a mere 3% of the stipulated charge that would otherwise have to be paid subject to the condition that within a period of 8 years an export obligation of 8 times the Duty Saved has been satisfactorily discharged. In some exceptional cases, the time for the fulfillment of this duty can be extended up to 12 years, but this provision is not easy even for Medium or some Large Scale Enterprises to easily avail, as it applies only to export obligations exceeding ₹100 Crore.

Frequently Asked Questions

- 1. What is EPCG scheme?

-

- Export Promotion Capital Good (EPCG) License, as the name suggests, is intended to act as a stimulus for exports. In EPCG Scheme, the exporter can import capital goods duty free i.e. Zero custom duty and one has to export finished goods worth 6 times of the actual duty saved value in 6 years. It allows an exporter to import of capital goods including spares for pre-production, production and post-production at zero Customs duty, for exports. The main goal of the EPCG Scheme is to improve India’s competitiveness in the manufacturing sector.

- 2. Who all are covered under the EPCG Scheme?

-

- 1.Manufacturer exporters with or without supporting manufacturer(s),

- 2.Merchant exporters tied to supporting manufacturer(s) and

- 3.Service Providers including Common Service Provider (CSP).

- 3.Can a new exporter avail this scheme?

-

- Yes, in such case, there will be no average export obligation.

- 4. What is EPCG license?

-

- The duty free authorization issued by DGFT RA is called EPCG License. It is Non-transferable license. It is used to import duty free capital goods.

- 5. What is zero duty EPCG scheme?

-

- Zero duty EPCG Scheme allows import of capital goods for pre-production, post production and production at zero customs duty, subject to an export obligation equivalent to 6 times of actual imported duty-saved value in 6 years.

- 6. Which types of capital goods can be imported into India under the EPCG scheme?

-

- Plant, machinery, equipment or accessories required for manufacture or production, either directly or indirectly, of goods or for rendering services, including those required for replacement, modernization, technological upgradation or expansion.

- Packaging machinery and equipment

- Refractories for initial lining

- Refrigeration equipment

- Power generating sets

- Machine tools

- Catalysts for initial charge

- Equipment and instruments for testing, research and development, quality and pollution control.

- Capital goods used in manufacturing, mining, agriculture, aquaculture, animal husbandry, floriculture, horticulture, pisciculture, poultry, sericulture and viticulture as well as those used in services sector.

- Computer software system

- Spares, moulds, dies, jigs, fixtures

- Catalysts for initial charge plus one subsequent charge

Which types of capital goods can be imported into India under the EPCG scheme?

- 7. Can the Capital goods be sourced indigenously?

-

- EPCG Authorization holder may source Capital Goods from domestic manufacturers also.

- 8.What are the benefits of domestic sourcing?

-

- Domestic manufacturers will be eligible for deemed export benefits. Specific EO shall be 25% less than the stipulated EO. Domestic sourcing of capital goods shall not attract GST till 30th September 2021..

- 9. Which authority issues EPCG License and How to obtain an EPCG License?

-

- The issuing authorities are the Regional Licensing Authorities of Director General of Foreign Trade (DGFT), Ministry of Commerce & Industry. An online application in Form ANF 5A is filed online at dgft.gov.in using digital signature with the Company and personal details.t

- 10. How to get EPCG License from DGFT?

-

- In order to obtain an EPCG License from DGFT, the primary requirement is to file an online application with the RA of DGFT with DSC. While applying online application all the necessary documents are required to be uploaded. We have an experience team who can help you in applying for EPCG License.

- 11. Can a new Exporter avail the EPCG Scheme?

-

- Yes, the Average Export Obligation imposed in such cases will be zero.

- 12. What Documents are required for EPCG License?

-

To avail of the benefits of the EPCG License, the exporter has to file an application with the DGFT. To apply for this incentive, fill up the Ayat Niryat Form 5B (ANF 5B) along with the following documents:

- Permanent Account Number (PAN)

- Digital Signature Certificate

- Fees @₹ 100/- per annum

- Copy of Import Export Code (IEC), Registration-cum-membership certificate (RCMC), MSME & Central Excise Registration (if registered) & GST registration certificate

- Details of Capital Goods sought to be imported with HSN code/Name, Model Number, and Technical Description.

- Details of Capital Goods sought to be imported with HSN code/Name, Model Number, and Technical Description.

- List of Products to be exported using the above machinery with HSN code.

- Chartered engineer’s certificate (along with original for verification) showing the nexus between the Capital Goods and the products to be exported in the format given in Appendix 5A.

- CA certificate (along with original for verification) indicating the last three financial year turnover in USD & INR only for the above mentioned Export Products i.e. Certificate of Chartered Accountant / Cost Accountant / Company Secretary in Appendix 5B.

- Factory Address where the machine will be installed.

- Stepwise Process/Flow Chart indicating the stages where the capital goods are to be used.

All these documents must be self-certified copies.

- 13.What is the time limit for issuance of EPCG authorization?

-

As per the Foreign Trade Policy, an application, which is complete in all respect, should be processed by DGFT in 3 days.

- 14. What are the conditions to be fulfilled under EPCG Scheme?

-

- 1.Average export obligation for proceeding 3 years exports.

- 2.Specific exports 6 times of the duty saved amount in six years.

There are two types of export obligation that are mandatory:

- 15.How the Export Obligation under an EPCG to be fulfilled?

-

- Export Obligation under EPCG Scheme is required to be fulfilled by export of goods manufactured/services rendered through the Machine by the applicant

- 16. How calculation of EO is done?

-

- EO is reckoned with reference to actual Duty saved in case of direct import. On domestic sourcing, EO is reckoned with reference to notional Customs Duties saved on FOR value.

- 17. Is there any exemption from maintenance of Average Export Obligation?

-

- Exporters of (i) Handicrafts, (ii) Handlooms, (iii) Cottage & Tiny sector, (iv)Agriculture, (v) Aqua-culture (including Fisheries), Pisciculture, (vi) Animal husbandry, (vii) Floriculture & Horticulture, (viii) Poultry, (ix) Viticulture, (x) Sericulture, (xi) Carpets, (xii) Coir, and (xiii) Jute are exempted.

- Apart from the exemption to the above sectors, relaxation is also provided to such sectors where the global growth rate has declined more than 5% for a particular FY.

- 18.What is Installation Certificate and where is it required to be submitted?

-

- Installation Certificate confirms installation of capital goods at factory/premises of authorization holder or his supporting manufacturer. It may be obtained from Jurisdictional Customs Authority or Chartered Engineering. It is required to be submitted to RA within 6 months from the date of completion of imports.

- 19. Whether exports made through third party will be considered for EO?

-

- Yes, where the names of both Authorization holder and supporting manufacturer are indicated in export documents like Shipping Bill/ Bill of Exports etc. along with EPCG authorization number i.e Shipping Bill / Bill of Exports should contain the name of Third Party along with EPCG Authorization number.

- 20. Whether a Capital goods imported by one unit can be transferred to other unit?

-

- The transfer of Capital Goods from one unit of the company to their another unit may be allowed by EPCG Committee in DGFT subject to the condition that both the addresses are mentioned in IEC and RCMC and submission of fresh installation certificate is done within 6 months of such transfer.

Frequently Asked Questions

- 21. What are the green technologies products? Is any special benefit is allowed under the Scheme for exports of such products?

-

- Green technology products are: equipment for solar energy decentralized and grid connected products, bio-mass gassifier, bio-mass or waste boiler, vapor absorption chillers, waste heat boiler, waste heat recovery units, unfired heat recovery steam generators, wind turbine, solar collector and parts thereof, water treatment plants, wind mill and wind mill turbine or engine, other generating sets - wind powered, electrically operated vehicles – motor cars, electrically operated vehicles – lorries and trucks, electrically operated vehicles – motor cycle and mopeds, and solar cells.Exports of these products provides for reduced export obligation of 75%.

- 22. Is EPCG scheme advisable?

-

- Maintenance of Average Export Obligation is a major problem in EPCG Cases which we come across regularly. Therefore If the Company is sure to achieve stable export orders in the years to come, then the EPCG Scheme is a very good option for them.

- 23. What is Post Export EPCG Duty Credit Scrips?

-

- This scheme is beneficial for those Exporters who intend to pay all the duties in cash at the time of Import and after fulfilling an Export Obligation, and then claim the benefit of duty-free in the form of Duty Credit Scrips. It is available to exporters who intend to import on full payment of applicable duties, taxes and cess in cash and chose to opt this Scheme.

- 24. It is available to exporters who intend to import on full payment of applicable duties, taxes and cess in cash and chose to opt this Scheme.?

-

- Specific EO is 85% of the applicable specific EO. However, average EO shall remain unchanged. A request for issuance of Duty Credit Scrip may be filed in ANF 5B in proportion of EO fulfilled within the specified export obligation period along with proof of actual duty payment , installation certificate, proof of EO fulfillment, etc. RA issues freely transferable duty credit scrip equivalent to proportionate EO fulfilled.

- 25. Whether export under EPCG scheme is eligible for MEIS and other schemes?

-

- Yes, MEIS benefit is over and above all schemes under the policy.

- 26. What should be done after fulfilling of export obligation?

-

- An application on the prescribed form ANF 5C along with the specified documents is required to be submitted to licensing authority for redemption.

- 27.What is EPCG license registration procedure?

-

- On receiving the EPCG License from DGFT the next step would be to register the license at Customs. It is not possible to clear the machinery duty-free unless you register the license at the port where the consignment will arrive. License is registered to the port of customs as mentioned in the license.

- 28.Is it mandatory to register EPCG license at Customs?

-

- Yes, it is mandatory to register EPCG License at customs.

- 29. Is it possible for any amendment/Changes in EPCG License after it is issued? If yes, explain what can be amended?

-

- If the Authorization holder has received the license but wanted to procure indigenously, the holder can amend the license and take an invalidation letter.-

- Due to changes in contract or increase in the value of imported capital goods, there will be a change in CIF value so we can amend the license.

- Some time we are unable to import due to some or the other problem and the validity of import is going to expire so we can apply for revalidation of license.

- Sometimes we want to add a new export product in the EPCG License due to some or the other reason. In such cases also, an EPCG license can be amended and new export products can be added.

Yes, we can amend the EPCG License and below are the details-

- 30. When can a shipment be counted under EPCG Scheme?

-

The following details should be mentioned in the shipping Bill to be counted in EPCG Scheme,

- EPCG License No. Should be mentioned in the shipping bill,

- Export Product with ITC HS code mentioned in the shipping bill should be the same as on License.

- 31. Can Capital Goods/machinery under the EPCG Scheme be procured indigenously/From the Domestic Suppliers? If yes, what is the advantage to both Domestic Supplier and the EPCG Authorization Holder?

-

- Yes, Capital Goods/ machinery can be obtained from Domestic Suppliers with the help of an Invalidation Letter. Benefit to Domestic Supplier – he can claim the benefits of Deemed Exports against such supplies. Benefit to EPCG Authorization Holder – Specific Export Obligation will be decreased by 25% and such supplies will not attract GST until 31.03.2021. (Date may be extended from time to time).

- 32. Can shipments exported under Advance Authorization/Duty Drawback/DFIA/MEIS be counted towards EPCG EO fulfillment?

-

- Yes, we can calculate the shipping consisting of Advance Authorization/Duty Drawback/DFIA/MEIS No. to be counted in EO fulfillment only if EPCG license no. is mentioned. It means that the EPCG Scheme can be combined with any other export promotion scheme.

- 33.What are the compliances to be followed after obtaining an EPCG License from DGFT?

-

- After obtaining an EPCG license from DGFT, it has to be registered at Customs. Once capital goods are cleared duty-free from Customs, it has to be installed at the said factory premises. An Installation Certificate has to be obtained from the Independent Chartered Engineer or Customs authority as a proof of Installation & commissioning. Once production starts, applicant should complete the export obligation in given time frame and submit all the export documents to DGFT office to close the EPCG license.

- 34. What is the Installation Certificate under EPCG Scheme? What are the conditions associated with it? Explain in detail.

-

- An EPCG Authorization holder needs to install the capital goods imported within a period of six months in front of an Independent Chartered Engineer. The chartered engineer will check that as per the authorization capital goods have been installed in given factory / supporting manufacturer premises or not and also cross verify the capital goods imported details with the license. And as per the verification, he will generate a certificate mentioning company name, Imported capital goods with quantity, BOE details, capital goods installation date on his letterhead with signed and stamped. The certificate generated by an Independent Chartered engineer is called the Installation Certificate. The same original copy should be submitted in DGFT and customs and receive the acknowledgment for the same.

- 35.What is export obligation?

-

- Export Obligation is a task/job given by the DGFT to the applicant to export certain value of goods in certain time frame. Export obligation is mandatory to be fulfilled.

- 36. Can Export Obligation under EPCG Scheme be fulfilled by the Export of alternate products? (i.e. By the Export of products not manufactured out of the Imported machinery)

-

- No, in the current Foreign Trade Policy 2015-21, there is no provision to fulfill export obligation through alternate products. Export Obligation will be completed only with those finished goods produced from imported capital goods mentioned in the EPCG License.

Frequently Asked Questions

- 37. Can Deemed Exports be counted towards the fulfillment of Export Obligation under EPCG Scheme?

-

- Yes, Deemed export is counted towards fulfillment of Export Obligation under EPCG Scheme. Supply to EOU/STP/EHTP/BTP Unit is called as deemed export and can be counted towards EO Fulfillment along with supply to SEZ units.

- 38. Can the Export Obligation period of 6 years under the EPCG Scheme be extended?

-

- Provisions for extension in the EO Period shall be governed as per the EPCG license issue date. For example, the EPCG License issued prior to the notification of FTP 2015-20 shall be governed by relevant provisions of HBP Vol 1 applicable at the time of issuance of EPCG Authorization. As per Current Policy in place – Yes, We can extend the Export Obligation period by two years after completion of 6 Years (6+2=8 Years). We can extend by paying a composition of 5% for the first year and 10% for the second year on the proportionate Duty saved value on pending / unfulfilled Export Obligation. But the minimum composition fee to be paid is ₹ 10,000/-. Alternatively, if the Exporter doesn’t want to pay the composition fees and has procured new export orders. He can enhance the EO by 10%/20% for the first/second-year respectively. In such cases, no composition fees will be required.

- 39. If the Export Obligation is still not completed in the extended period of 2 years, can the EO be extended further?

-

- Further extension of EO after (6+2=8 Years) is difficult. You have to apply to the EPCG Committee at DGFT New Delhi for an extension. The extension can be granted of an additional 2 years in case of genuine hardships only..

- 40. What if the Specific Export Obligation is not fulfilled even in the extended EO period, but Average Export Obligation is fulfilled?

-

- If the authorization holder failed to fulfill the specific export obligation but maintained average export obligation, the holder has to pay proportionate Duty Saved Amount with 15% annual interest on pending specific export obligation on actual imported capital goods at customs and submit the proof of duty paid to license authority concerned.

- 41. What if Average Export Obligation is not fulfilled, but Specific Export Obligation is fulfilled?

-

- If Average Export Obligation is not fulfilled, but Specific EO is fulfilled, Then Entire duty saved amount with 15% annual interest should be paid at Customs and submit the proof of duty paid to DGFT for regularization.

- 42. What is Block-wise Export Obligation under the EPCG Scheme?

-

- There are two types of Export Obligations – Average Export Obligation and Specific Export Obligation. We have to maintain both the obligation. While maintaining specific export obligations, we have to fulfill block-wise as per given below table and same we have to submit to DGFT.

Period from the date of issue of EPCG License Minimum specific export obligation fulfilled 1st Block(1st to 4th year) 50% 2nd Block(5th and 6th year) Balance/ Pending Specific EO - 43. What is the incentive for the early fulfillment of Export Obligation??

-

- If the Authorization holder has fulfilled 100% Average Export Obligation each year from the issue of license and 75% or more of Specific Export Obligation in half or less than half of the original Export Obligations period, the holder can redeem the license as per para 5.09 FTP..

- 44.What is the next step after Export Obligation is fulfilled?

-

- The next step is to close the EPCG License and apply for redemption/Closure. We need to fill the redemption form ANF 5B along with the specified documents mentioned in the form and submit it with the original license at the DGFT RA for Closure.

- 45.What is EPCG Redemption?

-

- EPCG Redemption or EPCG License closure procedure is a mechanism through which the DGFT monitors the fulfillment of the export obligation given to holder by the Government.

- 46. How to redeem/close EPCG license?

-

- The License holder has to fill the redemption form of ANF 5B with the relevant documents mentioned and submit to DGFT RA. The DGFT will issue a closure certificate called Export Obligation Discharge Certificate.

- 47.Can we surrender/cancel EPCG license if not used for duty-free import?

-

- We can surrender the EPCG License, if the holder does not want to import capital goods by submitting the relevant documents.

- 48. Is EPCG License transferable?

-

- No, EPCG License is non-transferable.

- 49.Can we sell EPCG license?

-

- No, EPCG License is not possible to sell.

- 50. What is the validity of EPCG license?

-

- The import validity of EPCG License is 2 years and export validity of EPCG License is of 6years from the issue of license.

- 51. Whether supply of goods against EPCG authorization is exempt under GST?

-

- Supply of goods against EPCG authorization is deemed export but not exempted upfront and hence supply against EPCG is liable to GST; however, the recipient or supplier has the option either to avail input tax credit or refund of GST paid.

- 52. Whether capital goods imported against EPCG authorization can be transferred/ sold?

-

- Import of capital goods against EPCG authorization shall be subject to actual user condition till export obligation is completed and EODC is granted, hence capital goods cannot be transferred or sold till export obligation is completed and EODC is granted.

- 53. Whether benefits of project import regulation and EPCG can be availed simultaneously?

-

- Yes, concessional benefits under project import regulations and exemption under EPCG can be availed simultaneously and export obligation will be calculated with respect to the concessional tax saving as prescribed under project import regulation.

- 54. Whether second-hand capital goods can be imported under EPCG authorization?

-

- The FTP of 2015-20 relating to EPCG provided that second-hand capital goods shall not be permitted to be imported under EPCG Scheme. This clause was deleted during the annual review of the policy in 2020. Correspondingly the Appendix-5F prohibiting the import of goods subject to conditions under EPCG has now been deleted.

- 55. Whether two or more EPCG authorizations can be clubbed together?

-

- All the authorizations have been issued to the same authorization holder.

- 2)Application for clubbing shall be made to the Regional Authority of the DGFT in Form ANF-5C.

- 3)Export products of all the authorizations shall be the same or similar.

- 4)The total export obligation would be re-fixed taking into account the total duty saved amount of the clubbed authorizations.

- 5)On clubbing, authorizations for all-purpose shall be deemed to be a single EPCG authorization.

- 6)The export obligation period shall be reckoned from the first authorization issue date.

- 7)The average obligation shall be highest among all the clubbed authorizations.

Yes, subject to the following conditions:

Frequently Asked Questions

- 56. Whether the Regional Authority is empowered to extend the export obligation period under EPCG?

-

- 1.on payment of composition fee equal to 5% and 10% respectively of proportionate duty saved amount on unfulfilled export obligation for the first/second year of extension; or

- 2.on enhancement in export obligation imposed to the extent of 10%/ 20% respectively of the total export obligation imposed under the authorizations for first/second year of the extension.2.on enhancement in export obligation imposed to the extent of 10%/ 20% respectively of the total export obligation imposed under the authorizations for first/second year of the extension.

Two extensions of one year each in the export obligation period may be considered by RA concerned:

- 57. Whether furniture and carpets can be imported duty-free under the EPCG scheme by a hotel?

-

- EPCG scheme is available for manufacturers as well as for service providers like hotels, hospitals, etc., Further, furniture and carpets are allowed to be imported duty-free under the EPCG scheme by the hotel industry only not for the manufacturing company.

- 58. Whether construction material like cement, steel & computer and printers are allowed to be imported under EPCG Scheme?

-

- No, as these items are prohibited under Appendix-5F. .

- 59. Can a deemed exporter claim EPCG??

-

- Yes

- 60. Can a person hold EPCG authorization source capital goods from a domestic manufacturer?

-

- Yes

- 61. Can an Exporter claim EPCG after export (post export EPCG)?

-

- Yes. Post export EPCG duty credit scrip(s) shall be available to exporters who intend to import capital goods on full payment of applicable duties, taxes, and cess in cash and choose to opt for this scheme. Basic customs duty paid on capital goods shall be remitted in the form of freely transferable duty credit scrip(s).

- 62. What are the benefits of domestic sourcing?

-

- Domestic manufacturers will be eligible for deemed export benefits. Specific EO shall be 25% less than the stipulated EO. Domestic sourcing of capital goods will neutralize GST by refund route to the supplier or recipient till the date notified and extended by Government.

- 63. What is the installation certificate and where is it required to be submitted?

-

- Installation certificate confirms the installation of capital goods at factory/premises of authorization holder or his supporting manufacturer. It may be obtained from Jurisdictional Customs Authority or Chartered Engineering. It is required to be submitted to RA within 6 months from the date of completion of imports.

- 64. Whether a capital goods imported by one unit can be transferred to another unit?

-

- The transfer of capital goods from one unit of the company to its another unit may be allowed by the EPCG Committee in DGFT subject to the condition that both the addresses are mentioned in IEC and RCMC and submission of fresh installation certificate is done within 6 months of such transfer.

- 65. What should be done after fulfilling of export obligation?

-

- An application on the prescribed form ANF 5C along with the specified documents is required to be submitted to licensing authority for redemption.