Farmer Producer Company Registration in India

Producer Company is a legally recognized body of farmers/ agriculturists with the aim to improve the standard of their living, and ensure a good status of their available support, incomes and profitability. Under Companies Act 1956, a Producer Company can be formed by 10 individuals (or more) or 2 institutions (or more) or by a combination of both (10 individuals and 2 institutions) having their business objective as one of the following:

- Production, harvesting, processing, procurement, grading, pooling, handling, marketing, selling, export of primary produce of the Members or import of goods or services for their benefit. Primary produce has been defined under the Companies Act 1956 as a produce arising from agriculture by a farmer which includes animal husbandry, floriculture, horticulture, viticulture, pisciculture, re-vegetation, bee raising, forestry, forest products and farming plantation products, produce of hand-loom, handicraft and other cottage industries.

- Rendering technical services, consultancy services, training, education, research and development and all other activities for the promotion of the interests of its Members;

- Generation, transmission and distribution of power, revitalization of land and water resources, their use, conservation and communications relatable to primary produce;

- Promoting mutual assistance, welfare measures, financial services, insurance of producers or their primary produce;

Characteristics of a Farmer Producer Organization:

- Minimum 10 or more individuals, being a producer, or any two or more producer companies, or combination thereof, are required to form Producer Company.

- All Producer Company shall have at least 5 directors but not more than 15 directors.

- Conversion is not possible into any other business structure such as Private Limited company, Public Limited Company, LLP etc.

- It can never be converted into a public company however it can be converted into a multi-state co-operative society.

- Every Producer Company must contain words like “Producer Company Limited” at the end of its name

- Minimum Paid-up capital must be ₹ 5 lakh.

- Voting rights in this kind of companies are aligned with the principle of “one man-one vote”, regardless of shareholding in the producer Companies

Objectives of the FPO scheme:

- To build a sustainable agriculture sector by promoting and supporting Farmer Producer Organisations, that enables farmers to improve production and productivity in the state.

- To provide support for the promotion of Farmer Producer Organisations through the qualified Resource Institutions (RIs).

- To promote economically viable and self-governing Farmer Producer Organisations

- To provide the required assistance and resources such as technical knowledge, inputs, financial resources, and infrastructure to strengthen the FPOs.

- To enable farmers in accessing the markets through their FPOs, both as buyers and sellers.

- To create a policy environment for investments in FPOs to leverage their production and marketing strength

Nature of the Farmers Producer Organization

A Farmer Producer Organization also known as Farmer Producer Company or FPC is a firm registered under the Ministry Of Corporate Affairs for the collective welfare of farmers to grow, collect, process and market the farm produce thus benefiting farmers and consumers to get quality products at reasonable prices. “Farmers Producer Organization” (FPO) is one type of Producer Organization where the members are farmers. Small Farmers’ Agribusiness Consortium (SFAC) is providing support for promotion of FPOs.

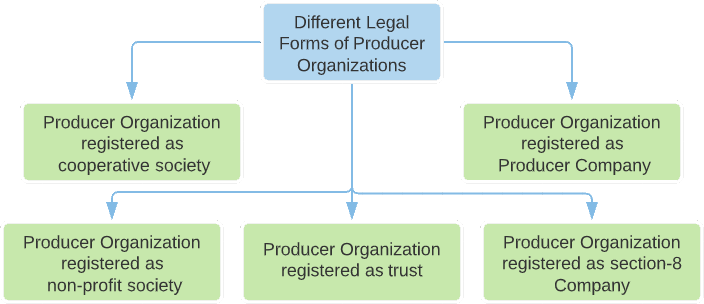

- A Producer Company is a hybrid between a Private Limited Company and a Cooperative Society, thus enjoying the benefits of professional management of a Private Limited Company as well as mutual benefits derived from a Cooperative Society.

- It is formed by a group of producers for farm or non-farm activities viz. farmers, milk producers, fishermen, weavers, rural artisans, craftsmen. Producer Organization is a generic name for an organization of producers of any produce, e.g., agricultural, non- farm products, artisan products, etc.

- It is a registered body and a legal entity.

- The liability of the members is limited to the unpaid amount of the shares held by them. Hence, the private assets of the members are safe from company losses.

- The minimum number of membership depends on the legal form of the Producer Organization. Minimum number of producers required to form a Producer Company is 10 while there is no limit for maximum number of members and the membership can be increased as per feasibility and need. Studies have shown that a Producer Organization will require about 700 to 1000 active producers as members for sustainable operation.

- Membership is acquired by purchase of shares in a Producer Company. A Producer Company can act only through its members. Members create the company and Members can also wind up the company. Members act through their General Meetings. The rights of the members are to transfer one’s shares, to vote on resolutions at meetings of the Company, to enjoy the profits of the company in the form of dividends etc. A member is ceased of his/her membership by completely transferring his/her shares, by forfeiting his/her shares, by a valid surrender, by death.

- A producer company can have a minimum of 5 Directors and not more than 15 Directors. The tenure of a director appointed by AGM is minimum one year and a maximum of 5 years. The directors of the company can be removed before the tenure by passing an ordinary resolution at a general body meeting. If a regular director is out of the State in which the meetings are held, for a period of 3 months or more, another person can be appointed as director in his place, who is called an alternate director. The tenure of the alternate director must be not less than 3 months. The moment the original director returns, the alternate Director ceases to be the Director.

- A director or an officer who fails to provide information to a member or a person, for whom he is required to provide information about the Producer Company, the Director is liable for imprisonment for a term extending to 6 months and with a fine equivalent to 5% of turnover of the company in the previous year. If there is a failure for convening an Annual General Meeting or other general meetings, the Director shall be punishable with a fine extended up to ₹1 lakh. In case the default continues, an additional fine extended up to ₹10,000/- per day

- A full time CEO is appointed by the Board of Directors as per Articles of Association. The CEO is to be other than a member who is accountable to both the Board of Directors and members.

- Each Producer Organization will have an elected Board of Management / Board of Directors as per the bye-laws who will manage the Producer Organization. The Board can engage professionals to manage its affairs. In the initial years, professional and managerial assistance is usually extended by the Producer Organization Promoting Institution (POPI) whose broad responsibilities are Cluster identification, Diagnostic and Feasibility Studies, Business Planning, Mobilization of Producers and Registration/Incorporation of Producer Organization, Resource Mobilization, Development of Management Systems and Procedures, Business Operations, Assessment and Audit. As the leaders of the Producer Organization gain experience, they should take over the affairs of the Producer Organization completely.

- There cannot be any government or private equity stake in the Producer Companies, which implies that Producer Companies cannot become a public or deemed public limited company. Hence, any Government or other corporate threat is non-existent in professional functioning of the company.

- Producers are shareholders in the organization. It is an organization of the producers, by the producers and for the producers. All primary producers residing in the relevant geography, and producing the same or similar produce, for which the Producer Organization has been formed, can become member of the Producer Organization. Membership is voluntary. Although primary producers obtain membership of Producer Organization voluntarily, the promoting institution should make efforts to bring all producers into the Producer Organization, especially the small producers.

- The minimum Authorized Capital of Producer Company is ₹ 5 lakhs which can be more than ₹ 5 lakhs as indicated in the Memorandum of Association. The minimum paid up capital for Producer Company is ₹ 1 Lakh.

- Every Producer Company name should end with “Producer Company Limited” which indicates its status as Producer Company

- It deals with business activities related to the primary produce/product. They will also have better bargaining power vis-à-vis the bulk buyers of produce and bulk suppliers of inputs. By aggregating the demand for inputs, the Producer Organization can buy in bulk, thus procuring at cheaper price compared to individual purchase. Besides, by transporting in bulk, cost of transportation is reduced, thus reducing the overall cost of production. Similarly, the Producer Organization may aggregate the produce of all members and market in bulk, thus, fetching better price per unit of produce. The Producer Organization can also provide market information to the producers to enable them hold on to their produce till the market price become favorable. All these interventions will result in more income to the primary producers.

- A person can become member of more than one Producer Organization, if there are two different Producer Organizations in the vicinity; each for a different type of produce, say vegetables and milk, one person can become member of both these Producer Organizations, if the family produces both milk and vegetables.

- It works for the benefit of the member producers to ensure better income for the producers through an organization of their own. Small producers do not have the volume individually (both inputs and produce) to get the benefit of economies of scale. The Producer Organization can aggregate the produce of its members, and sell it using the commodity exchanges. The produce needs to meet the quality standards specified by the commodity exchanges, and be stored scientifically in approved warehouses. The Producer Organization can become a member of the Commodity Exchanges to do trading directly, or else it can sell through the exchange-approved brokers.

- For exporting agricultural produce, all the members will have to follow Good Agricultural Practices (GAP). There are also other specific quality parameters that the importing countries impose for different produce which need to be complied with. For non-farm produce (handloom, handicrafts etc.), there are other quality specifications and other stipulations against using child labour, etc.

- A part of the profit is shared amongst the producers. Rest of the surplus is added to its owned funds for business expansion.

- Any individual or institution can promote a Producer Organization. The cost of registration may be reimbursed to the promoters duly approved by its general body in its first meeting with a resolution passed to that effect.

Institutions registered as cooperative societies and producer companies have legal provisions for sharing of profit earned by the Producer Organization by way of dividend. Other legal forms do not explicitly provide for profit sharing. However, the Producer Organization can offer better price for the produce it procures from the members, thus, benefiting the latter. Similarly, it can procure inputs/raw material in bulk and sell to members with low margin. Such activities are permissible for Producer Organizations under all legal forms. Institutions can be built for promoting common interests of members/producers. The limitation is that surplus generated by such a Producer Organization cannot be divided among members by way of dividend etc. The Producer Organization can re-invest the surplus to grow the business.

Limitations of a Producer Company

- It is a must to register the company and non-registered entities are not given the benefit of the Act.

- The members cannot transfer their shares freely.

- The Producer Company should follow the statutory provisions of Indian Companies Act and should comply with the mandatory prescriptions of the Act without fail

Pre-Requirements for Incorporation of Farmer Producer Organization:

- Any 10 or more producers (Individuals) can join together to form a production company but there is no upper limit on the number of members

- Or, any 2 or more producer institutions can form a producer company

- A minimum capital of ₹ 500,000 is required to incorporate a producer company

- There should be minimum 5 directors (maximum of 15) in a producer company

- It can never be converted into a public company however it can be converted into a multi-state co-operative society

- There is no limit for the maximum number of members in a producer company

- The company can only possess equity share capital

- The company must carry on 4 board meetings per year, and it should hold after every three months.

- A full time chief executive (CEO) should be appointed by the board.

Other Mandatory Requirements:

- Only a person or member engaged in activities related to the production of primary produce can participate in the ownership of the company.

- All the members should be primary producers

- The liabilities of the producer company members are limited to the amount of their unpaid share

- The name of the proposed company must contain “Producer Company Limited” at the end of their name.

- The proposed Producer Company is deemed as the private limited company as per the provisions of the Companies Act.

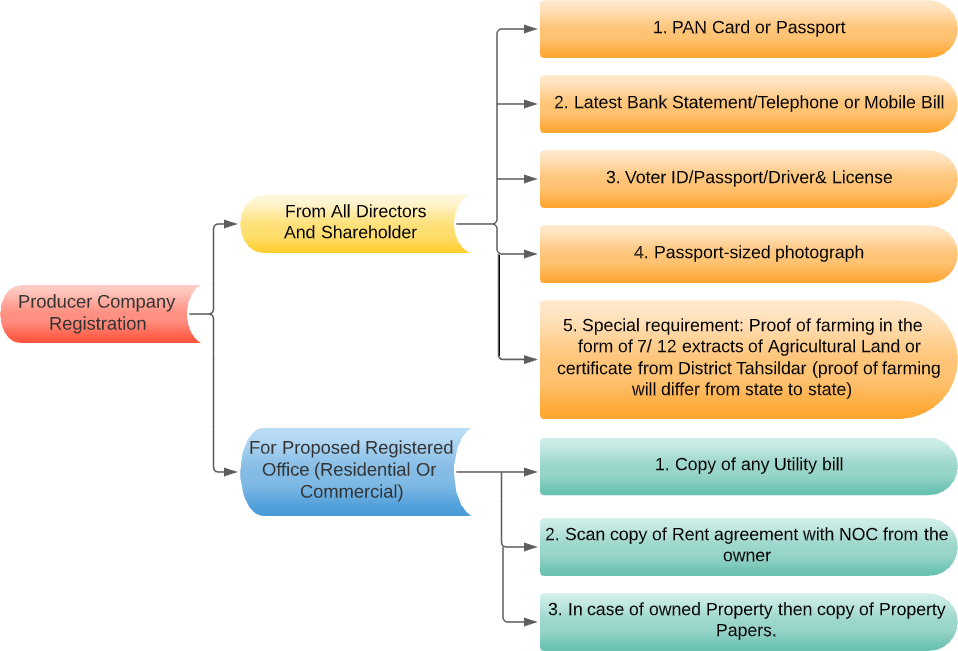

Documents required for filing SPICe (INC-32)

Benefits of a Producer Company Registration

Separate Legal Entity

Uninterrupted Existence

Better Credibility

Easy Management

Owning Property

Limited Liability

Activities Performed by the Farmer Producer Organization

Production Businesses

Read More...Technical Service Businesses

Read More...Marketing Businesses

Read More...Infrastructure Businesses

Read More...Financial Businesses

Read More...Benefits for Producer Companies

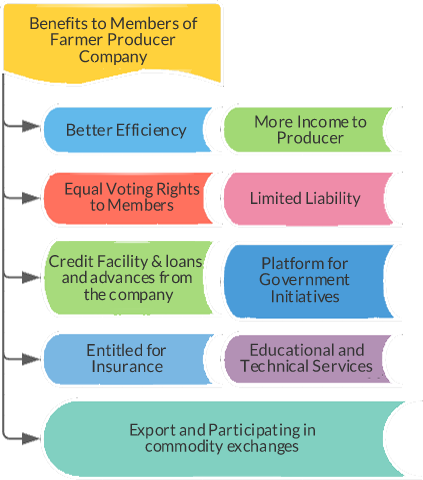

- Members of the producer company get the bonus shares in the same proportion to the shares held by them.

- Every member of the Company will receive a value for the product or products pooled and supplied as determined by the Director. The amount will be distributed in cash or by allotment of equity shares. This may be subject to the conditions of the Board.

- Members of Producer Company are also eligible to get financial assistance by way of credit facility for a period not exceeding 6 months.

- The additional amount that may be remaining (after providing provision for payment of limited return and reserves) may be distributed as patronage bonus to the members of the producer company. This will be in proportion to their participation in business activities either in cash or through equity shares.

- Limited liability and better management.

The following are the benefits enjoyed by a Producer Company:-

Loans and Investments

The primary producers are in need of financial support from time to time, thus, a special provision under the Companies acts 1956 was passed for giving loans to producer members. A Producer Company can provide financial assistance to its members through:-

Loans And Advances

As per the law, loans and advances would be issued to the members of the producer company against security for 7 or less than 7 years from the date of disbursement of the loan.

Credit Facilities

Credit facilities would be given to the members of the producer company for a period of 6 months or less than that.

NABARD Loan

NABARD stands for National Bank for Agriculture & Rural Development that helps to meet the financial requirements of small and regional scale farmers. The members of Producer Company can obtain loans under the NABARD loan scheme.

Farmer Producer Organization Incorporation Process

Obtain DSC-Digital signature Certificate in Electronic Format from Government Recognized Certifying Agencies

Register Your Director by Applying for Din-Director Identification Number (in Form DIN 3 in existing company or directly with SPICe INC 32 upto 3 directors)

Obtain Name approval Certificate in RUN Form(Reserve Unique Name) or directly apply with SPICe INC 32 -in both cases 2 chances are given with one Resubmission(RSUB)

Enlist the Company's Constitution in Memorandum of Association (MOA) and Articles of Association(AOA) in e-(AoA) directly with SPICe INC 32

To get the Company Identification Number -(CIN) address for the Registered Office and NOC from the Landlord is required

Farmer Producer Organization Incorporated

Current Bank Account to be opened in Company's Name

Application for Goods and Services Tax Identification Number(GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration(AGILE-PRO) in Form INC 35

Apply For PAN and TAN with SPICe INC 32 & Get the Certificate Of Incorporation -(COI) issued by ROC with the PAN & TAN

Apply For PAN and TAN

Get the Certificate Of Incorporation -(COI) issued by ROC with the PAN & TAN

Application for Goods and Services Tax Identification Number(GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration(AGILE-PRO) in Form INC 35

Current Bank Account to be opened in Company's Name

Farmer Producer Organization Incorporated

Key Compliances of the Producer Company

| S.No | Particulars | Section | Provisions |

|---|---|---|---|

| 1 | Name of the said company | Section 581F(a) | Name of the company shall end with the word “Producer Company Limited” |

| 2 | Total Number of Directors | Section 581P | Minimum number of mandatory Directors to run a production company is 5. The maximum limit is 15. |

| 3 | Election of the Directors | Section 581P(2) | Election of the Directors is required to be conducted within a period of ninety days fromProducer Company registration which may be relaxed to 365 days instead of 90 days for the Inter-State co-operative society which is incorporated as Producer Company. |

| 4 | Additional Directors and the Expert Directors | Section 581P(6) | Additional Directors and Expert Directors shall not exceed 1/5th of the total number of directors subject to Articles of Association of the Company. Expert directors can be elected as a Chairman but will not have any right to vote in the election of a Chairman. |

| 5 | Share Capital and the transfer of shares of a Producer Company | Section 581ZB, Section 581ZC, Section 581ZD | The Producer Company can have only Equity Share. The Articles may provide special rights to the Active Members of the Company. The Shares of Producer Company are non-transferable. The Board may grant approval to the active member to transfer their share to another active member. In the event of Death, the shares shall be transferred automatically to the nominee appointed by the Member. The Member shall nominate the person within 3 months of becoming a member of the Company. If the nominee is not a producer, the Board may direct nominee to surrender the shares. However, shares with special rights can be transferred, with prior approval of the Board. |

| 6 | Alteration of Memorandum of association (MOA) and Articles of Association (AOA) | Section 581H- MoA, Section 581I- AoA | Alteration in Memorandum of association and Articles of Association in accordance with the provisions of Section 581B by passing a Special Resolution. In case of alteration in Article of Association, the resolution shall be approved by at least 2/3rd of the elected directors or 1/3rd of the members. The copy of altered MOA and AOA shall be filed with ROC within 30 days of alteration. |

| 7 | Annual General Meeting (AGM) | Section- 581ZA, Section 581 S, Section- 581Y | Annual General Meeting of Producer Company: First AGM of the Company shall be held within 90 days from the date of incorporation. The Registrar may grant an extension for a period not exceeding 3 months. The extension is not eligible for a first annual general meeting. |

| 8 | Meetings of the Board Quorum. | Section 581V | Meetings of the Board: The board shall hold 4 meetings in every year with the gap of not more than three months between two meetings. The notice shall be given in advance at least 7 days before the Meeting by the Chief Executive. Shorter Notice can be called by stating the reason for the Meeting. The quorum 1/3rd of total Directors and minimum 3 Directors. Penalty: If the Chief Executive fails to comply with the provisions of sending notice, he shall be punishable by a maximum fine of ₹ 1,000/-. |

| 9 | Chief Executive | Section 581W | Chief Executive: The Company should appoint one full-time appointed Chief Executive other than members whose appointment shall be confirmed by the Board amongst persons other than the members. |

| 10 | Company Secretary | Section 581X | Company Secretary: Every Producer Company, having an average annual turnover exceeding ₹ 5 crores in each of three consecutive financial years shall have a whole time Company Secretary. Penalty for not appointing: Both the Company and every officer who is at default shall be punishable with fine of ₹ 500/- for everyday during which the said default continues. |

| 11 | Internal Audit | Section 581ZF | Every Producer Company must have internal audit of its accounts. The same shall be carried out in such an interval and in such a manner as specified by in the articles, by a Chartered Accountant. |

| 12 | General Reserve and the other reserve | Section 581ZI | General Reserve and other reserves: Every Producer Company shall maintain a general reserve in every year in addition to the Reserves as may be specified in the Articles. Sufficient funds are not available for transfer to maintain the specified reserve as mentioned in the article that such contribution shall be made by the members in proportion to their patronage in the business of that company in that year. |

Penalties

Any below-mentioned default by Directors of the Producer Companies amount to the penalty:

- handing over the custody of the books of account.

- fails to convene annual general meetings or other general meetings.

The company may be punishable by the fine ₹ 1 Lakh. If the default is in the nature of continuation than the everyday penalty of ₹ 10,000 is levied till the default continues.

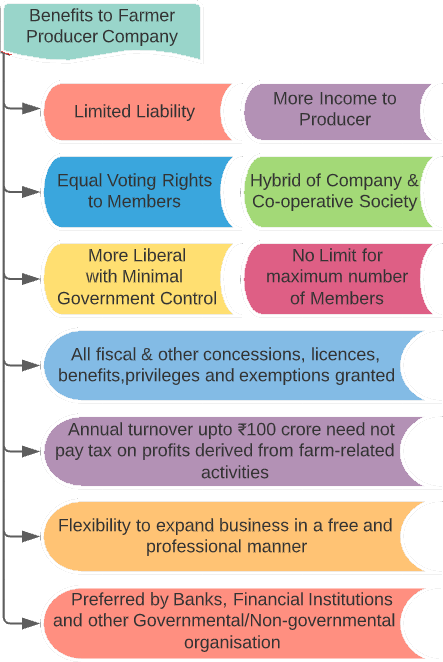

Tax Benefit (Taxability of Producer Company)

The Income Tax Act, 1961 under section 10(1) exempts the agricultural income that may sometimes vary on the basis of the agricultural activity carried out.

The Income Tax Act does not specify any specific tax benefit which essentially provides special tax benefits or exemptions to producer companies by its definition. But the tax benefit and exemption to a producer company totally depends upon the activity it carries on.

For example, income derived from selling the grown green tea leaves is an agricultural income under the Income Tax Act and it is 100 % tax-free. However, if the tea leaves are further processed for the manufacturing of tea, only 60% of such income will be considered as agricultural income and 40% of such income will be taxed.

Government schemes for Farmer Producer Companies

1. The Government aims to address price fluctuation in vegetables for the benefit of farmers and consumers.

2. 100% tax deduction for FPOs with an annual turnover of up to ₹ 100 crores,

There are various schemes launched by the Government of India for the support of FPOs; these include:

- The Government has issued the National Policy and Process Guidelines for Farmer Producer Organizations extending the benefits of central and state-funded programmes in agriculture to FPOs members on a priority basis from the RKVY (Rashtriya Krishi Vikas Yojana) programmes, 'National Food Security Mission' (NFSM) & Agricultural Technology Management Agency (ATMA) Scheme etc.

- The Department of Agriculture and Cooperation (DAC), Ministry of Agriculture regulated under the Government of India will work as the nodal agency for the implementation and growth of FPOs and will act with State Governments and Food Corporation of India (FCI) to incorporate FPOs procurement agencies under the minimum support price procurement agencies.DAC, along with its respective agencies, will work with NABARD (National Bank for Agriculture & Rural Development ) and other financial institutions to provide term loan for working capital and infrastructure investment requirements of FPOs. DAC will also work with all applicable stakeholders to reach 100% financial inclusion for members of FPOs and associate them to Kisan Credit cards. Kisan Credit Cards (KCC) so that such farmers could borrow loans from banks.PM Kisan and other farmers’ schemes were targeted to save farmers from the clutches of the money lenders and to provide them each penny intended for them. Also, DAC will work with the Ministry of Corporate Affairs and other stakeholders to improve the provisions under the law relating to the registration, management and regulation of FPOs and will circulate updates to this policy statement and guidelines from time to time as required.

- SFAC (Small Farmers Agribusiness Consortium) has been designated as a central procurement agency to undertake price support operations under the Minimum Support Price (MSP) programmes for pulses and oilseeds and it will operate only through FPOs at the farm gate. Minimum Support Price (MSP) is a form of market intervention by the Government of India to insure agricultural producers against any sharp fall in farm prices.

- It also launched the “Equity Grant and Credit Guarantee Fund Scheme” enabling the FPOs to access a grant up to ₹ 10 lakh to double members’ equity and seek collateral-free loan up to ₹ 1 crore from banks, which in turn can seek 85% cover from the Credit Guarantee Fund.

- Associating FPOs to financial institutions like cooperative banks, State Financial Corporations etc. for working capital, storage and processing infrastructure and other investments.

- The National Agricultural Cooperative Marketing Federation of India (NAFED) will take measures to include FPOs in the list of eligible institutions which undertakes price support purchase orders.

- An Agricultural Produce Market Committee (APMC) is a marketing board established by state governments in India to ensure farmers are safeguarded from exploitation by large retailers, as well as ensuring the farm to retail price spread does not reach excessively high levels. Suitable amendments in the APMC Act has been brought to treat the country as a single, unified market for agro-produce with no restrictions on commodity movement as also to enable FPOs market their produce directly to the consumers/ bulk-buyers, without payment of Mandi Fee.

- Pradhan Mantri Kisan Samman Nidhi (PM-KISAN) Scheme, benefit is provided to the eligible beneficiary to the tune of ₹ 6000/- per year. It is payable in three 4-monthly instalments of ₹ 2000/- each. The payment is made online directly into the bank accounts of the eligible beneficiaries under Direct Benefit Transfer mode.

- Awareness and capacity building of farmers and position holders in FPCs are made on regular interval to help them understand the real benefit of institution.

Annual Compliances for Producer Company - Checklist

| S.No | Compliance | Section & Rules | Form | Particulars of Compliance |

|---|---|---|---|---|

| 1 | Receipt of MBP-1 | 184(1) | Form MBP- 1 |

|

| 2 | Receipt of DIR- 8 | 164(2) 143(3)(g) |

Form DIR – 8 | Every Director of the Company in each Financial Year will file with the Company disclosure of non-disqualification. |

| 3 | E- Forms Filing Requirements | 581ZA | E-form: MGT-7 | Annual Return: Every Company will file its Annual Return within 60 days of holding of Annual General Meeting. Annual Return will be for the period 1st April to 31st March. |

| 4 | Annual Form | 581ZA | E-form: AOC-4 | Financial Statement: Company is required to file its Balance Sheet along with Statement of Profit and Loss Account, Cash flow statement, Directors’ Report and Auditors’ Report in this form within 30 days of holding of Annual General Meeting. Attachment: Balance Sheet, Statement of Profit& Loss Account, Cash Flow Statement, Directors’ Report, Auditors’ Report and Notice of AGM. |

| 5 | Annual Form | Section 73 Rule 16 | E-form DPT-3 | Return of Deposit: Company is required to file this form every year on or before 30th June in respect of return of Deposit and Particulars not considered as Deposit as on 31st March. |

| 6 | Event Based Form | Section 90 | BEN-2 | Disclosure of Significant Beneficial Owner (SBO): Company shall file BEN-2 within 30 days of receipt of BEN-1 from Share holder. Note: On regular basis company have to check whether there is any SBO in company due to change in its shareholding or due to change in shareholding of body corporate members. |

| 7 | Annual Form | Rule 12A | DIR-3 KYC | KYC of Directors: All the Directors of company shall file this form on or before 30th September every year for all the directors of the Company. |

| 8 | Half Yearly Return | Section 405 | MSME-1 | Delay in Payment to MSME Vendor: Company have to file this return half yearly in respect of pending payments to MSME vendors as at end of half year.

|

| 9 | Directors’ Report | 581ZA | Directors’ Report shall be prepared by mentioning all the information required for Company under Section 134 read with relevant rules and relevant provisions of other Act. | |

| 10 | Circulation of Financial Statement & other relevant Documents | Company will send to the members of the Company approved Financial Statement, Directors’ Report & Auditors’ Report at least 14 clear days before the Annual General Meeting. | ||

| 11 | Notice of AGM | 581ZA | The Producer Company shall in each year hold an Annual General Meeting and not more than 15 months shall elapse between the dates of one Annual General Meeting to the next.

A general meeting of the Producer Company shall be called by giving not less than fourteen days prior notice in writing |

|

| 12 | Sending of Notice of AGM | 581ZA | The notice calling the annual general meeting shall be accompanied by the following documents, namely : –

|

|

| 13 | Board Meetings | 581V | Board shall meet at least once in every three months and at least four such meetings shall be convened in every year. Quorum: 1/3rd of the total strength of Directors subject to a minimum – 3 |

|

| 14 | Appointment of Auditor | 581 | E-form ADT-1 | Auditor will be appointed for 5 (Five) years and form ADT-1 will be filed for 5-year appointment within 15 days of Annual General Meeting. |

Conclusion

The agricultural industry is the backbone of Indian economy. 60% of India’s population relies on agricultural activities for their livelihood. But these primary producers and farmers struggle a lot to get their share of profit. Keeping their miserable condition in mind, the Government of India has come up with an expert committee, headed by Y.K. Alagh to look into the matter. In 2002, the committee brought the concept o f Producer companies in the Indian economy with the aim to improve the standard of living of farmers and agriculturists. Since then, they are working with the motive to uplift Indian farmers and agriculturalists (collectively termed “Producers”).

Frequently Asked Questions

- 1. What are the minimum requirements to register a Producer Company?

-

- Minimum 10 individuals (who are a producer) or at least 2 producer institutes must subscribe the shares of the company.

- Minimum 5 directors in the company, one of which must be Indian citizen and resident.

- A place of business in India must be provided as a registered office address.

- 2. What are the minimum requirements towards Capital?

-

- Minimum paid-up capital of ₹ 5 Lakhs is required to form the Producer Company.

- 3. What is the requirement of DSC (Digital Signature Certificate)?

-

- DSC is provided in the form of token issued by Certified Authorities and is a substitute of Physical Signature and enable the owner to sign documents digitally.

- Company incorporation is a complete online process and all the forms required to be filed for incorporation of company are required to be signed digitally with the help of DSC of the Directors.

- Company Sarthi helps its clients in the issuance of DSC.

- 4. What is the requirement of Documents for DSC issuance?

-

- Self-attested Documents and Details required are:

- Duly filled and Signed Application Form

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Valid and active Mobile Number and e-Mail id

- On submission of above documents with the DSC Authority partner, applicant will receive the OTP on the given Mobile and e-Mail ID and thereafter applicant has to complete Mobile and Video verification.

- 5. What is the eligibility to become a Director in Company?

-

- Any natural person above the age of 18 years can become the director in the company after procuring Director Identification Number (DIN).

- There are no specific criteria provided in terms of citizenship or residency, a foreign national can also become a director.

- 6. What is Director Identification Number (DIN)?

-

- DIN is a unique number assigned by the Ministry of Corporate Affairs to Individuals on whose name the application is made, allowing that individual to become a Director in a Company or Designated Partner in an LLP.

- DIN is allowed only once in lifetime and can be used to become a Director in any number of company as per eligibility criteria.

- The application of DIN Allotment is now merged with the application for the formation of a company subject to a limit of maximum 3 DIN.

- 7. What is the requirement of Documents for DIN issuance?

-

- Self-attested Documents and Details required are:

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Special requirement:Proof of farming in the form of 7/ 12 extracts of Agricultural Land or certificate from District Tahsildar (proof of farming will differ from state to state)

- Valid and active Mobile Number and e-Mail id

- Proof of Identity of Applicant (Any one)

- Valid Passport

- Driving License

- Voter ID Card

- Proof of Residence of Applicant (Any one not older than 2 months having same address as that in the Proof of Identity):

- Bank Statement

- Electricity bill

- Telephone bill

- Mobile bill

- 8. How to reserve the name of the Company?

-

- Applicant has to give few choices of the name which can be checked at the Company Sarthi for the availability.

- On the availability of atleast one name, Company Sarthi inform you of the same and ask you to provide two options of that name and the priority preference.

- Company Sarthi also seeks from you the main objects of the company and State in which Registered office will be situated.

- Although Company Sarthi follows a rigorous process of checking availability of Name, the registrar may ask to re-submit application with a different name if names applied do not fall under the criteria of uniqueness, relevancy or do not fulfill other requirements.

- 9. Does any subscriber have to be physically present for completing the process of Incorporation of the Company?

-

- No, none of the promoters are required to be physically present for completing the process of Incorporation of the Company.

- All the forms are filed on the web portal and are digitally signed.

- Also, the required documents can be sent through e-mail or uploaded on our portal for filing.

- 10. What documents are required for registered office of Company?

-

- Business address Proof (Any one not older than 2 Months):

- Electricity Bill

- Pipe Lined Gas Bill

- Telephone Bill

- Mobile Bill

- No Objection Certificate to be obtained from the owner(s) of registered office.

- Rent Agreement of the registered office should be provided if property is on rent.

- 11. Are the shares of the Producer Company transferrable?

-

- Yes— members of the producer company transfer shares along with the special rights.

- 12. What kind of Company Producer Company?

-

- Private Limited Company as per the Companies Act, 2013.

- 13. What is the Annual Compliances for Producer Company?

-

- Producer Company shall hold atleast four board meeting in a year. Board shall meet atleast once in three months by giving seven days advance notice. The gap between two meetings shall not be more than 3 months.

- Every producer company shall hold Annual General Meeting in every financial year. The gap between two AGM shall not be more than fifteen Months. The AGM shall be called by issuing at least 14 days’ notice.

- Every producer company shall hold their first AGM within 90 days from the date of its incorporation.

- File their financial statements in form AOC-4 within 30 days of holding Annual General Meeting.

- File their Annual Return in Form MGT-7 within 60 days of holding Annual General Meeting.

- Every producer company shall have Internal Audit of its accounts.

- 14. What is the tenure of the Directorship period in Producer Company?

-

- The minimum period is 1 year while the maximum period of Directorship is 5 years.

- 15. What are the types of Producer Companies?

-

- Production Businesses – Companies which are involved in the manufacturing and the production of the primary produce.

- Marketing Businesses – Businesses involved in the marketing or promotion of the primary produce.

- Technical Service Businesses – Companies who offers technical assistance to producers.

- Financing Businesses – Business involved in providing finance facilities to the agricultural activities.

- Infrastructure Businesses – Business involved in providing infrastructure facilities like electricity, water resources etc.