Hindu Undivided Family (HUF) – Introduction

Hindu Undivided Family (‘HUF’) is treated as a ‘person’ under section 2(31) of the Income-tax Act, 1961 (herein after referred to as ‘the Act’). HUF is a separate entity for the purpose of assessment under the Act.Under Hindu Law, an HUF is a family which consists of all persons lineally descended from a common ancestor and includes their wives and unmarried daughters. An HUF cannot be created under a contract; it is created automatically in a Hindu Family.Jain and Sikh families even though are not governed by the Hindu Law, but they are treated as HUF under the Act.Assessment of HUF:-

Assessment of HUF:-

An HUF is recognized as a separate assessable entity under the Act. Its income may be assessed if following two conditions are satisfied:

- There should be a coparcenership. In this connection, it is worthwhile to mention that once a joint family income is assessed as that of HUF, it continues to be assessed as such in subsequent assessment years till partition is claimed by coparceners.

- There should be a joint family property which consists of ancestral property, property acquired with the aid of ancestral property and property transferred by its members.

Ancestral Property: Ancestral property may be defined as the property which a man inherits from any of his three immediate male ancestors, i.e. his father, grandfather and great grandfather. Therefore, property inherited from any other relation is not treated as ancestral property. Income from ancestral property held by following families is taxable as income of HUF:

- A family of widow mother and sons (may be minor or major);

- Family of husband and wife, having no child;

- Family of two widows of deceased brothers;

- Family of two or more brothers;

- Family of uncle and nephew;

- Family of mother, son and son’s wife;

- Family of a male and his late brother’s wife.

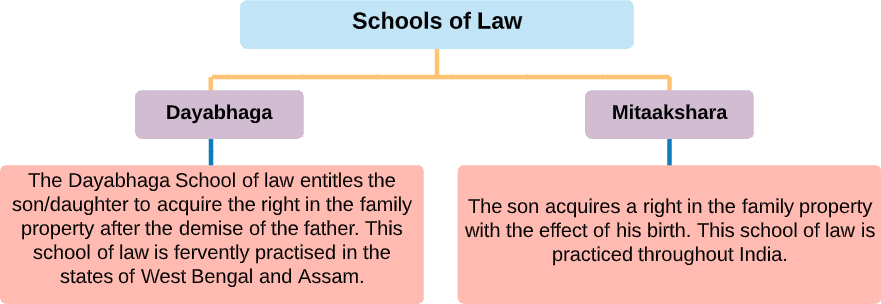

Property obtained by daughter from joint family property would be her absolute property. Any income there from is chargeable to tax in her hands in the individual status only. This will also apply to any legal heir obtaining property in the capacity of a descendent. HUF is a unique type of legal entity which derives its roots from Hindu Law. HUF is an entity as a family, which consists of male lineally descended from a common ancestor. The members of the family would also include their spouses and unmarried daughters. Given the nature of the entity, the relation of HUF’s arises from status and not legal contracts. A HUF forms under two schools of law, which are Dayabhaga and Mitaakshara.

Note: The Hindu Succession (Amendment) Act, 2005 gave Hindu women the right to be coparceners or joint legal heirs in the same way a male heir does.

What Is HUF?

The term HUF stands for ‘Hindu Undivided Family’ and comprises all successors of a common male ancestor and includes their wives and unmarried daughters. A HUF consists of a Karta, coparceners, and members. Karta manages the entire business and makes the final decision. Normally, the eldest member (Male or Female) of the family takes the position of Karta. A HUF, as such, can consist of a very large number of members including female members as well as distant blood relatives in the male line. However, out of this, coparceners are only those males and females who are within 4 degrees of the lineal descendent from the common male ancestor. The relevance of the concept of the coparcener is that only coparceners can ask for partition in the property. The other family members; i.e., other than coparceners in the HUF, have no direct claim over HUF property, but can claim only through the coparceners.

The term ‘Hindu Undivided Family’ (HUF) is governed by the Hindu Law. It is not possible to create a HUF by an agreement between two parties, nor can it be formed by a group of people who do not constitute family.

The HUF even continues to exist after the death of the common ancestor, and the next eldest male or female member becomes the head of the family and is known as “Karta”.

By creating HUF, you can save taxes by creating a family unit and pooling in assets, since HUF is taxed separately. Income of a HUF is assessed in the hands of the HUF alone and not in the hands of any of its coparceners or members.

HUF as the name suggests stands for Hindu Undivided family governed under Hindu law board and could be formed by a married couple or by members of a joint family. HUF could be formed by two members, at least one of whom should be a male member of the family. Senior most male member of the family would become ‘Karta’. Although it is governed by the Hindu law board, it can be formed by Jains, Sikhs and Buddhists as well. Membership into a HUF does not come from a contract but from status under hindu law.

The essentials are:-

- One should be Hindu, Jains, Sikhs and Buddhists are considered as Hindus but not Muslims or Christians

- There should be a family i.e. group of persons – more than one and

- They should be undivided i.e. living jointly and having commonness amongst them.

All these three essentials are cumulative. It is a body consisting of persons lineally descended from a common ancestor and includes their wives and unmarried daughters, who are living together, joint in food, estate and, worship (not now necessary). The daughter, on her marriage, ceases to be a member of her father’s HUF and becomes a member of her husband’s HUF. However, after 1-9-2005, daughter married or unmarried is a coparcener like a son.

Here are the legal formalities involved in forming an HUF.

HUF comprises of all descendants of a common male ancestor and includes their wives and unmarried daughters. The term of HUF is not defined in the income tax law; it is defined under the Hindu Law as a family. The family continues to exist even after the death of the common ancestor and the next eldest male member becomes the head of the family or the “Karta”. In financial terms, we can call him ‘manager of the family’. Even upon the death of all the male members, the HUF continues to exist.

In case the control and management of the HUF are situated outside India, the HUF would be a non-resident. The residential status of a HUF is determined not on the basis of where the Karta resides but on the basis of where the HUF is managed from.

- All coparceners;

- A son in the womb of his mother at the time of partition;

- Mother;

- Wife.

Why should you form an HUF?

Characteristics of a HUF

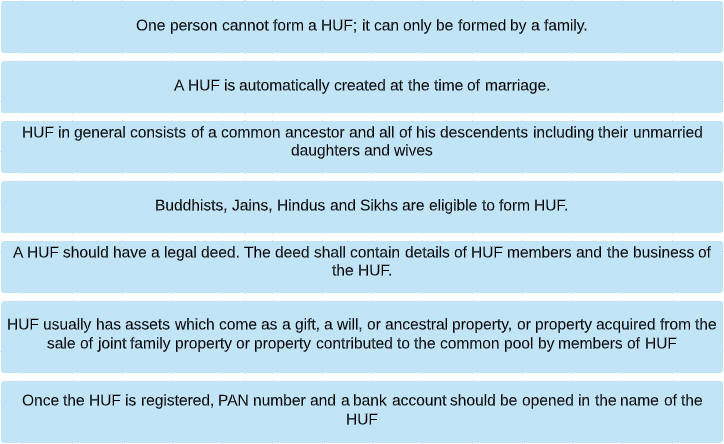

One person cannot form HUF. There have to be minimum of two members to constitute a HUF. An HUF is formed by a family. An HUF is automatically created at the time of marriage. Once an HUF is formed it must be formally registered in its name. An HUF should have a legal deed. The deed shall contain details of HUF members and the business of the HUF. A PAN number and a bank account should be opened in the name of the HUF.

HUF consists of a common ancestor and all of his lineal descendants, including their wives and unmarried daughters

In case the control and management of the HUF is situated outside India, the HUF would be a non-resident . Where the affairs of the HUF are managed from outside India the HUF would be a non-resident.

Every member of the family can deposit their income in the common corpus.

Single person’s authority while participation from the entire family.

Gifts collected up to a worth of 50,000 will be tax free. A father who owns a HUF account can gift a property or money of higher worth to a son who owns a smaller HUF account, but he should specify that the gift is for the son’s HUF and not to him as an individual. Under section 64(2) and 56(2) tax benefits can be enjoyed in such instance.

Corpus can be used for investment in tax-free money instruments.

Corpus can be divided only on agreement of every coparcener of the family.

The Income Tax Act recognizes the HUF as an independent assessable or taxable entity. Hence, HUFs enjoy all deductions and exemptions under the IT Act independent of the income and tax liabilities of its members. A separate Income Tax Return is filed under Income Tax Act.

Tax Saving- For example- an ancestral property that yields rental income. Under normal circumstances, the rent will be attached to a person’s income and will be taxed according to that individual’s tax slab. However, if it is transferred to an HUF, the income will be that of the HUF’s and will be taxed separately.

Nature of Joint Hindu Family Business

Formation

- There should be at least two members in the family to form a HUF.

- Ancestral property should have been inherited by members of HUF.

- All of the members enjoy this property and have an equal share in that property.

- Thus, any child taking birth in that family becomes a member of the HUF.

- There is no requirement for an agreement to become a member.

Liability

- There is limited liability of all the members or co-parceners in the Hindu Undivided Family business.

- All the co-parceners have equal rights and shares in the property of Hindu Undivided Family business

- The Karta has unlimited liability.

Control

- Karta is the person who has full control over the Hindu Undivided Family business.

- Karta can take advice from all the members but he is not bound to accept their decisions.

Continuity

- After the “Karta” is deceased, the very next eldest member takes up the position of Karta in Hindu Undivided Family business.

- The business can be divided and ended up by the mutual consent of the members.

Minor Members

- The person who has taken birth in Hindu Undivided Family can be a member of the family business.

- Therefore, a minor can also be a member of the family.

Prerequisites for Formation

A HUF establishes in compliance with the requirements specified below:

CapitalCapital is one of the major considerations with regards to the set-up of any business entity. A HUF establishes by using the ancestral property, assets gifted by relatives and friends, or received by the HUF through a will.

MembersIf a married couple forms HUF, then the child would be integrated into the entity after his/her birth. The person of another religion cannot form an entity, except for Sikhism and Jainism. On a detailed note, the members of a HUF include a Karta, members, and coparceners. The Karta heads the family with decision-making responsibilities. Any male member could play the role of a Karta with the consent of the family members. A coparcener is a person who is entitled to his/her share of the property. A coparcener is classified into the following hierarchies:

- A first-degree coparcener could be a first-time holder of ancestral property.

- A second-degree coparcener includes the sons and daughters of the family.

- A third-degree coparcener includes the grandsons and granddaughters of the family.

- A fourth-degree coparcener includes the great grand-sons of the family.

The HUF wouldn’t cease to exist on the death of a sole male member. It would continue to function with the existing female members. However, a widower to a Karta cannot consider as an heir to the throne. An adopted child is entitled to membership but cannot be a coparcener.

As is the case with the establishment of any entity, the name assigned to the HUF shouldn’t be in contravention with any of the specified laws. However, there is no requirement for obtaining name approval.

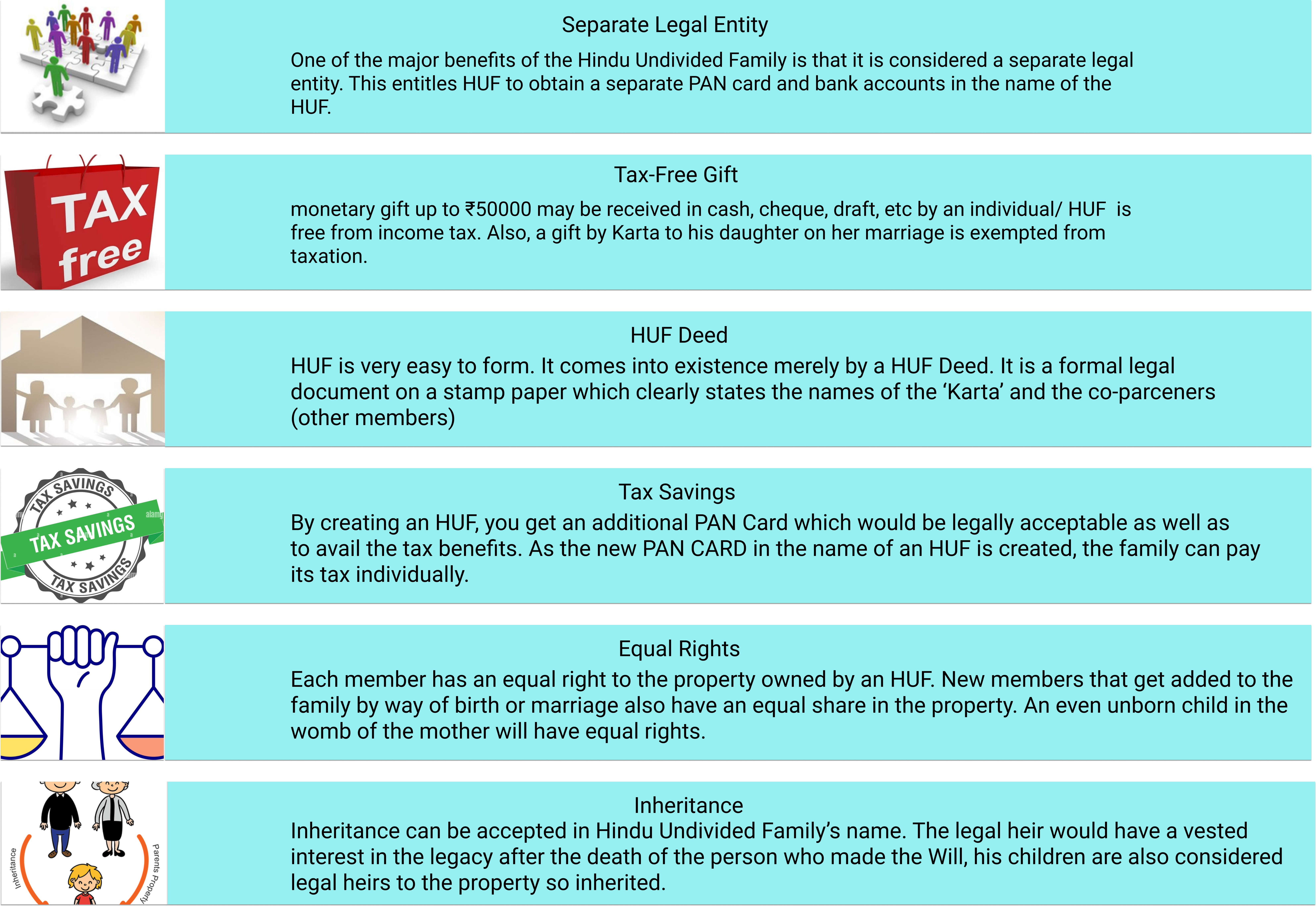

HUF DeedHUF may be formed with or without a legal deed, though it is always advisable to pursue a business with a written document. With respect to a HUF, a legal deed consists of details of membership of the HUF, the source of funds, and the likes of it. The Deed acts as proof of the existence of the entity that has been formed. The document should include a declaration by a family member for the name of the Karta, powers vested with the Karta, and the entitlement of the Karta to hold the transactions on behalf of its members. In addition to it, the document should state the capital that was invested in forming the HUF.

PANFollowed by the formation of a deed, the Karta is required to obtain a PAN Card, which is an important document for pursuing financial transactions. The application for PAN must be made in Form 49A, either online through the NSDL website or manual means. The PAN Card must be used by the entity for the filing of income tax returns and claiming applicable deductions. The application for PAN and income-tax return should consist of the signature of the Karta.

Separate Bank AccountAs implicit as it might sound, a HUF must function with a bank account, wherein the funds of the entity can be maintained. Maintenance of such bank account is strictly for business purposes, and shouldn’t include the savings of any member.

Conditions to Be Fulfilled To Create a HUF

Advantages of HUF Registration

Separate Legal entity

- HUF is a separate legal entity in the eyes of the law. This entitles HUF to obtain a separate PAN card, file separate Income tax returns and open bank accounts in the name of the HUF.

Tax-Free Gift

- Monetary gifts up to 50k may be received in cash, cheque, draft, etc. by an individual/ HUF. It is not taxable as per the income tax act. Also, a gift by Karta to his daughter on her marriage is exempted from taxation.

Tax Savings

- A HUF is taxed separately from its members, therefore, deductions or exemptions allowed under the Income tax laws can be claimed by it separately. For example, if you and your spouse along with your 2 children decide to create a HUF, all 4 of you as well as the HUF can claim a deduction for Section 80C.

Effective Control

- The Karta has full control over the business activities and takes a decision quickly.

- No one can interfere in the decision of Karta as every member is bound to accept his decision.

- Hence, it avoids clashes among the members and results in very speedy decision making.

Continued Business Existence

- After the death of Karta, the next eldest member takes up his position. So, it does not affect the activities of the business.

- Hence, all the business activities are done smoothly, continuously without any threat.

Limited Liability of Members

- As all the liability of the members is restricted to the extent of their share in the business.

- But the Karta has unlimited liability due to his complete hold on the business.

- Hence, in case of dissolution of the business, Karta’s personal assets and his share will be liable.

Expanded Loyalty and Cooperation

- All the business operations are carried on by the members of a family jointly.

- So, this increases loyalty and cooperation with each other without any hindrance.

- Therefore, all the targets of the business can be achieved by the cooperation among the members and the Karta.

Deductions under Chapter VIA available to HUF

| S.No. | Section | Deduction |

|---|---|---|

| 1 | Section 80C | Deduction available to HUF[Insurance Premium can be paid on the life of any member which does not exceed 10% of total sum assured for policies issued on or after 1st Apr, 2012] |

| 2 | Section 80CCF | Investment in Infrastructure Bonds up to 20,000/- (Discontinued w.e.f. A.Y. 2013-14) |

| 3 | Section 80D | Mediclaim Policy on the health of any member of the family. Deduction for payment on account of preventive health check-ups not available. |

| 4 | Section 80DD | For maintenance including medical treatment of a dependant member of the family. |

| 5 | Section 80DDB | Medical treatment for any dependant member of the HUF |

| 6 | Section 80G | Donation to certain funds, charitable institutions ,etc. |

| 7 | Sections 80IA / 80IAB / 80IB / 80IC / 80ID / 80IE / 80JJA | New Industrial undertakings |

Disadvantage of forming a HUF

Though HUF seems like the perfect way to save tax as a family, it comes with its own drawbacks. Below-mentioned are the few demerits of a joint Hindu family business:

Equal rights of members

- The greatest disadvantage of opening a HUF is that its members have equal rights on the property. The common property cannot be sold without the concurrence of all the members. Any additions to the family, by way of birth or marriage, become a member of the HUF and get equal rights. A HUF can get too large to manage.

Partition

- Perhaps the worst nightmare of opening a HUF is closing it down. The only way a HUF can be dissolved is by a partition. Corpus can be divided only on agreement of every coparcener of the family. Under a partition, assets are distributed to members which can lead to a lot of disputes and can be a lot of legal hassle.

Joint family system losing relevance

- HUF was recognized as a separate taxable entity by the income tax department. However, in today’s times, where nuclear families are the norm, HUF is losing relevance. Several cases have come to fore where couples or families are fighting it out on common household expenses; forget to pool in of assets. Divorce rates are rising and therefore, HUF as a tax vehicle is losing importance.

HUF continues to be assessed as such till partition

- Once a HUF is formed, you must continue to file its tax returns, unless a partition takes place. Any claim for partition is made to the assessing officer. The assessing officer, on receiving such a claim, must make an enquiry after giving due notice to the members. Income from the property which was partitioned is taxed as individual income of the member. If the member forms another HUF with his wife and children, the income of the property which was transferred from the original HUF is taxed in the hands of new HUF.

Limited Resources

- All the members of Joint Hindu Family Business totally depend upon the ancestral property due to their limited liability.

- Many commercial banks resist extending the credit limit due to the weak financial position of the business.

- Hence, this will result in limited expansion and growth of the business.

Unlimited Liability of Karta

- All the important decision regarding management of various business activities are taken by Karta.

- But there is a disadvantage with the Karta that he has unlimited liability.

- Hence, all the business debts are paid by using the personal assets of the Karta.

Dominance of Karta

- The Karta takes all the decisions individually and manages the business

- He also involves other members in decision making.

- But Karta is not bound to accept the decisions of the members which may create conflicts between the Karta and the other members. Hence, due to clashes in decision making, lack of cooperation between Karta and other members occurs.

Limited Managerial Skills

- Sometimes the members suffer due to unfair decisions taken by the Karta in respect of business operations.

- Unfair decisions are taken due to the lack of managerial skills.

- So, the Karta cannot be knowledgeable or proficient in all managerial functions.

- Nowadays, the joint Hindu family business is declining due to the decreasing number of joint Hindu families in the nation.

Income under HUF

Taxability of HUF

In order to compute the income of an HUF, one has to first ascertain its income under the different heads of income (ignoring incomes exempted under sections 10 to 13A of the Act). The following points should be kept in mind while computing income:

- If funds of an HUF are invested in a company or a firm, fees or remuneration received by the member as a director or a partner in the company or firm may be treated as income of the family (if fees or remuneration is earned essentially as a result of investment of funds).

- However, if fees or remuneration is earned for services rendered by the member in his personal capacity, it will be treated as the personal income of the member.

- If any remuneration is paid by the HUF to the karta or any other member for services rendered by him, remuneration is deductible from income of HUF if such payment is genuine and not excessive and paid under a valid and bona fide agreement.

The following incomes are not taxed as income of HUF:-

- If a member has converted or transferred without adequate consideration his self-acquired property into join family property, income from such property is not taxable in hands of the family.

- Income of impartible estate (though it belongs to family) is taxable in the hands of holder of estate and not in hands of HUF.

- Personal income of the members cannot be treated as income of HUF.

- "Stridhan" is absolute property of a woman; hence income arising there from is not taxable as income of HUF.

- Income from individual property of daughter is not taxable in hands of HUF even if such property is vested into HUF by daughter.

(1).Deduction from gross total income: An HUF is entitled for deductions available under Chapter VI-A (as applicable) while calculating its taxable income.

(2). Rate of Tax:

- An HUF is taxed on same slab rates which are applicable to an Individual.

- An HUF is liable to pay Minimum Alternate Tax (MAT) the tax payable is less than 18.5 % (including cess and surcharge) of "Adjusted Total Income" subject to prescribed conditions.

Creation of HUF

HUF stands for Hindu Undivided Family wherein the Income that is being earned belongs to the whole family and not to any specific individual. As the Income is being generated in the hands of the whole family, this income cannot be taxed in the hands of the family but is taxed in the hands of the HUF. And, therefore HUF is considered as a separate entity for the purpose of Income Tax Act and the HUF has a separate PAN Card and a separate income tax return is filed for the same. A HUF automatically comes into existence when a person gets married and starts his family. It is not necessary that this new family should also have kids. The day when bride and groom get married, they have formed a HUF. Although a HUF is automatically formed at the time of marriage, it is always advisable to have a written agreement as the Banks and Income Tax Dept ask for the HUF Deed. It is not necessary that HUF is created on the day of marriage itself and can be created at any point of time in future. Creating a HUF is not a difficult task and the steps involved in creating a HUF are explained below.

Logic behind Forming a HUF to Save TaxBasically the logic behind forming an HUF to save tax is to avail the benefit of an extra PAN Card legally. As the Income of the Family is not taxed in the hands of any specific Individual, a new PAN Card is allotted to the HUF and Tax would be paid by the Family using this PAN Card. As a new PAN Card would be allotted to the whole family, it will also enjoy the benefits of Income Tax Slab Rates i.e. Income would be Tax Free up to the specified limits and would then be taxed progressively at 10%, 20% & 30% resulting in tax saving. The major advantage of creating a Hindu Undivided Family Account is that the family gets an extra PAN Card and can split the family income and thereby resulting in tax saving and reducing the tax outgo. This is the major reason why CA’s advise their clients to create a HUF and save taxes of upto 1.8 Lakhs every year.

However it should be noted that there is a disadvantage as well and that is the fact that all assets of in the name of the Hindu Undivided Family are assets of the family and not of a specific individual. All members of the family have a right in the assets of the Hindu Undivided Family (including an unborn child in the womb of a mother). Therefore proper caution should be exercised while gifting assets to the Hindu Undivided Family as the whole family would be having a share in the assets of the family as compared to the fact that if these assets were in the name of a specific individual – only that individual would have a right over that asset. A HUF is taxed separately from its members, therefore, deductions (such as under Section 80) or exemptions allowed under the tax laws can be claimed by it separately. For example, if you and your spouse along with your 2 children decide to create a HUF, all 4 of you as well as the HUF can claim a deduction for Section 80C. HUF is usually used by families as a means to build assets.

How is HUF taxed?- HUF has its own PAN and files a separate tax return. A separate joint Hindu family business is created since it has an entity separate from its members.

- Deductions under section 80 and other exemptions can be claimed by the HUF in its income tax return.

- HUF can take an insurance policy on the life of its members.

- HUF can pay a salary to its members if they contribute to its functioning of the HUF. This salary expense can be deducted from the income of HUF.

- Investments can be made from HUF’s income. Any returns from these investments are taxable in the hands of the HUF.

- A HUF is taxed at the same rates as an individual.

How to create HUF Capital and put Money in HUF

There are certain ways through which HUF Capital can be created and some of the most popular methods to infuse capital in a HUF is by receiving gifts in such a manner that they don’t attract any tax. Some of the most effective and popular methods of creating HUF Capital by receiving gifts without attracting any tax are:-

Gifts received at the time of marriage

- Gifts received at the time of marriage of any member of the HUF are fully exempted from the levy of Income Tax. However, gifts received at the time of marriage of daughter are not exempted and are taxable.

Ancestral property

- Your ancestral property is not only your own and belongs to the whole family i.e. the HUF. The Ancestral property can be transferred to the HUF to create capital of the HUF.

Aggregate Value of Gifts is less than 50,000

- If the aggregate value of gifts received from any person during a financial year does not exceed 50,000, then this whole amount is exempted from levy of any tax. There is no limit on gifts received from family members and this limit of 50,000 is only for gifts received from non-relatives.

Gifts received from members of the HUF

- If a gift is received from members of the HUF, then the income generated from these funds would get clubbed and taxed in the hands of the member making the gift. However, if this income is invested in tax-free instruments, the members making the gift will not have to bear extra tax burden as the income is already tax free.

On maturity of this instrument, the HUF can invest the money anywhere and in any way in which it likes and the income won’t be clubbed. In other words, Income generated from Income won’t get clubbed.

Capital created by HUF through Income earned

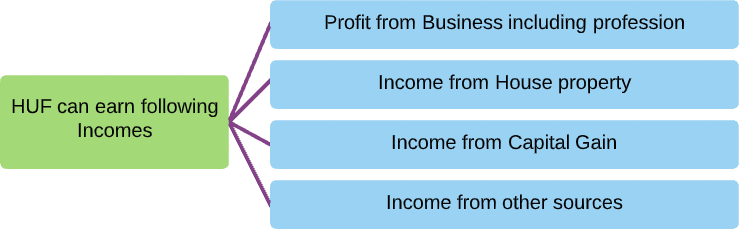

For an HUF, the income sources are almost similar to individual taxpayers such as profits from business or profession, income from house property, capital gains, income from other sources and so on. Since the HUF is a separate entity, it cannot earn income from salary. Further, all income that arises on the investment of the HUF's funds and utilization of its assets is regarded as income and is separately assessed and taxed. On the income earned, the HUF is taxed on the same slab rates applicable to an individual. The HUF is even entitled to avail similar exemption level and deductions like those under sections 80C, 80D etc as that of an individual tax payer. HUF can pay salary to its members if they are contributing to its functioning and work of the joint Hindu family business. This salary expense can be deducted from the income of the HUF. With proper planning, an individual can avail various deductions under personal tax filing and other deductions for an equal amount under HUF tax filing. Some examples of sources from where a HUF can earn more income are:-

- Through any Business

- Investing in Shares and Mutual Funds,

- Investing in Real Estate

- Investing in fixed deposits

- Through Rental Income

- Various other sources

As taxpayers we all look to minimize our tax liability by availing benefits under various sections of the Income Tax Act. Saving taxes through HUF is a valid and lawful thing to do. HUF is treated as a 'person' under section 2(31) of the Income-tax Act and is a separate entity for the purpose of assessment. Personal income of the members is not treated as income of an HUF. HUF has its own PAN and files a separate tax return.

Some of the investment options that are used by HUF are bank fixed deposits, mutual funds, insurance etc.

- Mutual Funds: In case of mutual funds, the Karta has to add Hindu Undivided Family within brackets after his name to distinguish it from his personal investments.

- Insurance: In the case of insurance under HUF, it is allowed only on the life of the Karta. Proposals on the life of co-parceners or members may be allowed only if the Karta is uninsurable. In all such cases, the Karta will be the proposer. If coparceners apply for individual insurance on the basis of income of HUF, it will be treated as separate insurance. Payment of premium will have to be made through HUF funds. The insurance under HUF would belong to and become the assets of the HUF.

- PPF: However, PPF account in the name of HUF is not more permitted as clarified by the Ministry of Finance in 2005. To claim deduction under section 80C, an HUF can contribute to the PPF account of its members and claim a tax deduction.

- Bank Fixed Deposits: Form15 G can be filed for claiming Deduction of TDS on Interest and require that the final tax liability on the estimated income shall be Nil. Form 15G, having validity of 1 financial year only, can only be furnished if the aggregate income is less than the basic exemption limit.

The rent from such a property would either be taxed in hands of the Husband or the Wife or both. As this Income is arising from an asset which belongs to the whole family, this Income shall be taxed in the hands of the Family (provided an HUF is formed) and one would be able to enjoy the benefits of slab rates. If HUF is paying rent of more than 50,000 per month and is not falling in the tax audit category under Section 44AB – such person would also be required to deduct TDS @ 5% under Section 194IB.

Other Relevant Points regarding HUF

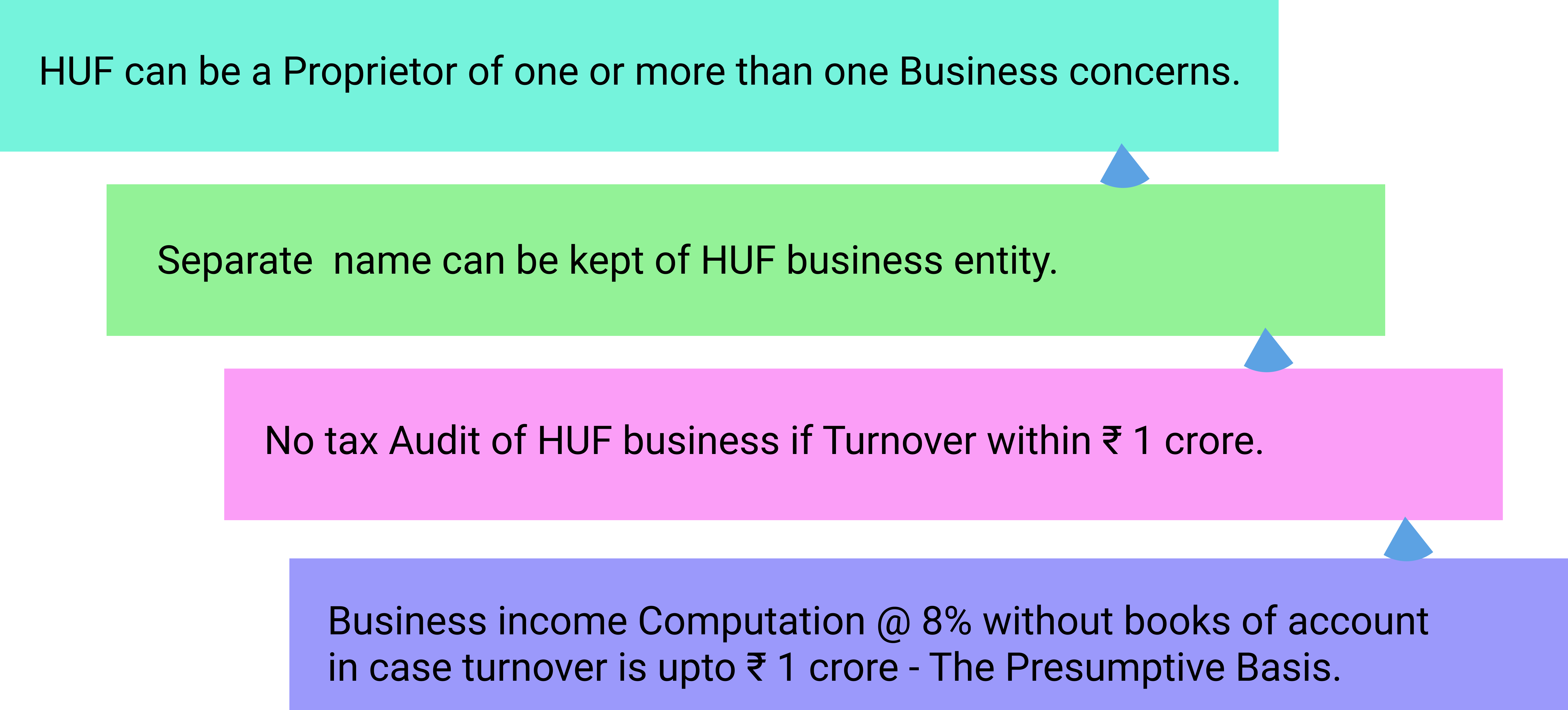

HUF is also required to file Income Tax Return every year just like an Individual and if the turnover of the business of the HUF is more than 25 Lakhs/ 1 Crore, tax audit under Section 44AB would also be required to be conducted by a Chartered Accountant.

Due Date of filing of Income Tax Return of the HUF would be 31st July of the Assessment Year. However, in case the Tax Audit is required to be conducted, the Due Date of filing of Return would be 30th Sept.

The Karta of the HUF has the power to sign all documents on behalf of the HUF. However, he may also permit other adult members to have this power.

An adopted child can become a member of the HUF but he cannot become a co-parcener. The difference between a member and a co-parcener is that the member cannot ask for partition of the HUF.

HUF’s are recognized all over India except Kerala wherein HUF’s are not recognized. This de-recognition was done 1975 with effect from 01.12.1976.

The HUF may be a resident or a non-resident in India depending on where the control of the HUF is residing.

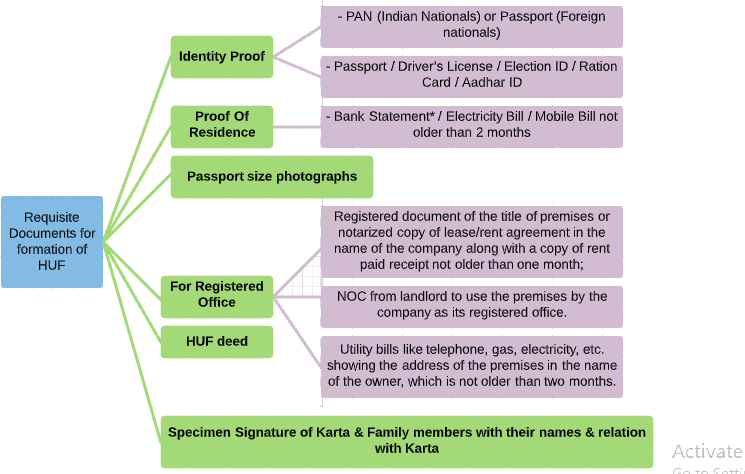

Requisite Documents for formation of HUF

Steps to Create HUF

Minimum two members are required to form a HUF, constituting a joint family. A HUF is automatically formed when a person marries and starts their family. It is not compulsory for the couple to have kids. Owning an estate or a property is also not mandatory to form a HUF. The Hindu Law though does not govern Buddhists, Jains, and Sikhs; it can be treated as a HUF for taxation purpose. In HUF, the income generated belongs to the whole family, instead of a specific individual. Thus, this income is then taxed in the hands of the HUF. Naturally, HUF is treated as a distinct entity for tax purposes. HUF need to have a separate PAN card and need to file separate IT returns. One of the major benefits of the Hindu Undivided Family is that it is considered a separate legal entity. This entitles HUF to obtain a separate PAN card and bank accounts in the name of the HUF. Once a HUF is formed, typically the oldest member of the family becomes the “Karta” and is provided with an additional exemption. In addition, the tax slabs are lower when compared to that of regular corporate. Until January 2016, women were not eligible to be the Karta of a HUF. However, the Delhi High Court, in a landmark case, gave the decision in favor of a woman being the Karta of HUF. The decision is yet to be implemented in the Income Tax Act.

Who Should Opt For HUF?HUF arrangement suits those taxpayers who have income from ancestral property and expects to inherit these assets (both real and financial). A taxpayer will be able to divert the inheritance to the HUF account and thus preventing personal tax liability from increasing. In addition, HUF is also beneficial to taxpayers with a higher savings rate.

Legal Formalities Involved While Forming A HUF:- Form corpus – A capital asset can be used to form the HUF. It can be any ancestral property, assets received as a gift from relatives or through a will.

- Register a deed – A deed is required on stamp paper declaring the formation of the HUF. It should include information of the Karta and the co-parceners. In addition, sources of funds in the corpus are also mentioned. Once the declaration deed is made, the Karta can apply for a permanent account number (PAN) for the HUF as a separate legal entity.

- Opening bank account – Once the PAN is allocated, open a bank account in the name of the HUF.

There are 3 steps involved in creating a HUF.

Create HUF Deed

Apply for HUF PAN Card

Open HUF Bank Account

The 1st Step in creating a HUF is to create the HUF Deed. The HUF Deed is a written formal document on a Stamp Paper stating the names of the Karta and the Co-parceners (Members) of the HUF. The eldest male member of the HUF becomes the Karta of the HUF. A declaration is also provided by each member of the family where they declare the name of Karta and also state that –

- Karta has the authority of the accounts vested in his hand

- That the members are the only members of the HUF

- The Karta holds the right to govern all the transactions of the HUF accounts on behalf of the members.

The names of the members of the HUF and the name of the HUF are also required to be stated in the HUF Deed at the time of creation of HUF. The name of the HUF is usually the name of the Karta followed by the word HUF. For example: If the Karta of the HUF is Sudesh Kumar, the name of his HUF would be Sudesh Kumar HUF. It also states the capital with which the HUF has been initiated. There are various sources through which Capital can be introduced in the HUF. Most notary public agents have such formats and help in creating of HUF at a nominal fee. The fees charged by notary public agents for creating a HUF Deed Format are a few hundred only. Creating a HUF Deed is not mandatory and PAN Card and Bank Account can be opened without HUF as well but it’s always better to have a written document in place.

As a HUF is treated as a separate entity different from its members, a HUF is required to apply for a separate PAN Card. An application for HUF PAN Card is required to be made in Form 49A which can be furnished online as well as manually. HUF PAN Card Application can be made online through this link: https://tin.tin.nsdl.com/pan/form49A.html. Form 49A (for Indian Citizens) and Form 49AA (for Foreign Citizens) Once the PAN Card has been allotted, the HUF would be required to file separate Income Tax Returns and can therefore claim benefit of income tax slab rates and also claim most of the income tax deductions which are available to an Individual. The application for PAN Card and the Income Tax Return would be signed by the Karta.

Step 3: Open HUF Bank AccountA HUF is also required to open a Bank Account in which it will receive all payments. A HUF Account can be opened in any bank account. At the time of opening of HUF Bank Account for creation of HUF, the HUF would also be required to have a Rubber Stamp of the HUF and all documents pertaining of the HUF should be properly stamped. This rubber stamp should be rectangular as Round Stamps are now not accepted (RBI Circular) Once all the above 3 steps are completed i.e. the HUF Deed has been created, PAN Card has been allotted and the Bank Account has opened, the HUF is now a separate legal entity and can start receiving payments and the amounts received in the name of the HUF will not be taxed in the hands of the individual members of the HUF.

Compliances for HUF post registration

Accounting and Book Keeping

- It is always advisable to maintain records for business activities of a HUF, unlike Partnership firm, on cash or accrual basis in order to judge whether these operations are generating a profit.

Tax Audit

- There is no obligation for a HUF under any law to get the accounts except in cases where the turnover of the business in any financial year exceeds 1 Cr and gross receipt from profession exceeds 50 Lakh. In both cases, the audit of accounts is compulsory for a HUF under the Income Tax Act, 1961. In case the Tax Audit is required to be conducted, the Due Date of filing of Return would be 30th Sept.

Income Tax Returns

- Income tax filing must be filed by all HUFs having a taxable income. Due Date of filing of Income Tax Return of the HUF would be 31st July of the Assessment Year.

GST Registrations and returns

- One has to get themselves registered under GST if their annual turnover is more than 40 lakhs. Also, if they are doing online business (selling through amazon, flipkart etc.), they are required to get a GST number under goods and service tax Act. Once they have registered under GST, then they are required to file monthly or quarterly details of sale and purchases.

The income earned by the HUF would be taxable as per the Income Tax Slabs and the HUF is also required to file income tax returns just like Individuals. All income tax deductions are also available to HUF just like they are available to an Individual. Moreover, if the turnover of the business of the HUF is more than the limit specified under Section 44AB i.e. 50 Lakhs/ 1 Crore, it would also be required to get an audit conducted by a Chartered Accountant.

Modes of Creation of HUF

A Hindu Undivided Family can be created by following ways-

Blending of individual property with the family Hotchpot

Read More...Receipts of Gifts

Read More...Doing Joint labor for the benefit of HUF

Read More...Inheritance through a specific bequest under a Will

Read More...Partition of a larger Hindu Undivided Family

Read More...Reunion of separated co-parceners

Read More...Women can be Karta of HUF

The Karta of a Hindu joint Family in Hindu Law is the senior most member of the family entitled to manage family affairs, in his absence the next eldest male member after him is entitled to be the Karta. A Karta is the caretaker of the whole family and looks after the welfare of all the members of the family. His relationship with other members is a relationship of trust and confidence.

At least one male member is necessary to constitute a coparcenary. But the question arises that if no male member is left in the family or if all male members are minors then who becomes the Karta? or Can a female member of a Hindu Joint Family become a Karta then in such circumstances ?

The Hindu Succession Amendment Act, 2005 has conferred equal property rights on daughters as well. Now the daughters by birth will acquire rights over coparcenary property.

The eldest female member of the family, being the coparcener in an HUF, may become the Karta of an HUF. It was argued that the 2005 Amendment to the Hindu Succession Act only recognized the rights of a female member to inheritance and does not address the issue of management of the HUF estate.

In case of wife of the deceased Karta, the same argument cannot be extended since the wife of the deceased Karta is never treated as a coparcener to the HUF. A widow therefore, cannot act as Karta of the HUF after the death of her husband. Interestingly, in cases where the surviving male coparceners were minors, the courts took a view that the widow can be a manager of the HUF while distinguishing the position of a manager from that of a Karta.

Thus if a woman, who is not a coparcener (widow or wife of a coparcener) has a son above the age of 18 years, in such a case it is not possible for her to be the Karta of the HUF.

The Hindu Succession (Amendment) Act, 2005 removed this discrimination by giving equal rights to daughters in the Hindu Mitakshara coparcenary property as that to a son. Pursuant to the said amendment, a daughter of a coparcener (i.e., her father) shall, by birth,

- become a coparcener in the same manner as a son,

- be entitled to the coparcenary property in the same manner as a son,

- be subject to the same liabilities in respect of the coparcenary property as that of a son, and

- be responsible to discharge the debts of her father, grandfather or great-grand father contracted by them after the commencement of the Hindu Succession (Amendment) Act, 2005, in the same manner as a son.

The amendment does not have a retrospective effect, and if a coparcenary property has been partitioned or disposed of before 20 December 2004, the above amendment shall not affect such property, and a daughter cannot claim any right over such property.

The Hindu Succession (Amendment) Act, 2005 by extending the applicability of the amendment to not only Hindu women being recognized as coparceners on equal footing with a son, but also recognizing the eldest woman member of the HUF as the Karta of the HUF and its properties.

Please note that Property obtained by daughter from joint family property would be her absolute property. Any income therefrom is chargeable to tax in her hands in the individual status only. This will also apply to any legal heir obtaining property in the capacity of a descendent.

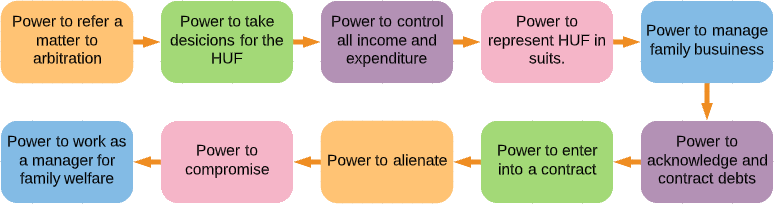

Powers of a Karta

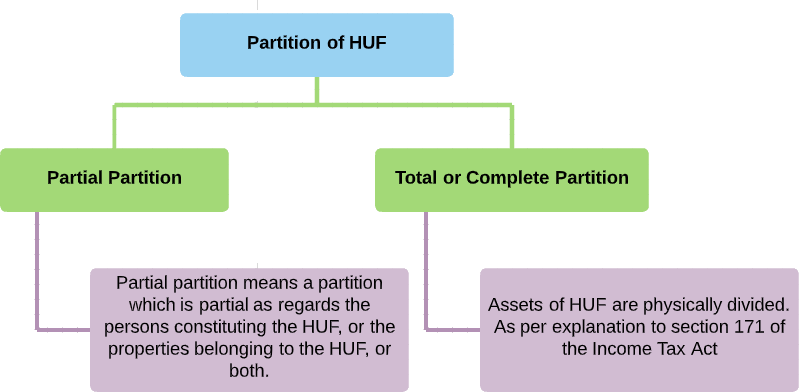

Partition of HUF under Income Tax Act, 1961

The Partition of HUF should be recognized as per the Income Tax Act and not as per the Hindu Law. Section 6 of the Hindu Succession Act would govern the rights of the parties but insofar as income-tax law is concerned, the matter has to be governed by section 171(1) of the Income Tax Act, 1961. The Hindu Law does not require that the property in every case be partitioned by metes and bound or physically into different portions to complete a partition. But the Income Tax Law introduced certain additional conditions of its own to give effect to the partition u/s 171. Section 171 of the Income Tax Act, 1961 defines the partition of HUF and deals with the provisions of assessment after its partition. Thus a transaction may be treated as severance of status under Hindu Law but not a partition under 1961 Act as physical division of property is necessary under 1961 Act.

Partition’ means- where the property admits of a physical division, a physical division of the property, but a physical division of the income without a physical division of the property producing the income shall not be deemed to be a partition; or

- where the property does not admit of a physical division, then such division as the property admits of, but a mere severance of status shall not be deemed to be a partition.

Therefore a transaction can be recorded as a partition u/s 171 only if, where the property admits of a physical division, such division has actually taken place.

A Partial partition that has taken place after 31-12-1 978 is not recognized the Income Tax Act, 1961 (Sub-section 9 of section 179. Therefore even after the Partial partition, the income of the HUF shall be liable to be assessed under the Income-Tax Act as if no partition had taken place.After the Partition, the assessment of HUF shall be made as per the provisions of Section 171 of the Income Tax Act and order to be passed by the Assessing Officer.The sum received by a member as and towards his share as coparcener of HUF, on its partition cannot be brought to tax as income.Setting apart of certain assets of HUF in favor of certain coparceners on the condition that no further claim in properties will be made by them, is nothing but a partial partition and not a family arrangement and not recognized in view of section 171(9) of the Act.

Procedure of partition and assessment

The following procedure u/s 171 is prescribed under the Income Tax Act regarding partition and assessment after partition of HUF:

1. The HUF hitherto assessed as undivided shall be deemed for the purposes of this Act to continue to be a Hindu undivided family, except where and in so far as a finding of partition has been given under this section in respect of the HUF.

2. Where, at the time of making an assessment u/s 143 or u/s 144, it is claimed by or on behalf of any member of a Hindu family assessed as undivided that a partition, whether total or partial, has taken place among the members of such family, the AO shall make an inquiry thereinto after giving notice of the inquiry to all the members of the family.

3. On the completion of the inquiry, the AO shall record a finding as to whether there has been a total or partial partition of the joint family property, and, if there has been such a partition, the date on which it has taken place.

4. Where a finding of total or partial partition has been recorded by the AO and the partition took place during the previous year,—

- the total income of the joint family in respect of the period up to the date of partition shall be assessed as if no partition had taken place; and

- each member or group of members shall, in addition to any tax for which he or it may be separately liable and notwithstanding anything contained in clause (2) of section 10, be jointly and severally liable for the tax on the income so assessed.

5. Where a finding of total or partial partition has been recorded by the AO and the partition took place after the expiry of the previous year, the total income of the previous year of the joint family shall be assessed as if no partition had taken place; and each member of group of members shall be jointly and severally liable for the tax on the income so assessed.

6. Notwithstanding anything contained in this section, if the AO finds after completion of the assessment of a Hindu undivided family that the family has already effected a partition, whether total or partial, the AO shall proceed to recover the tax from every person who was a member of the family before the partition, and every such person shall be jointly and severally liable for the tax on the income so assessed.

7. For the purposes of this section, the several liability of any member or group of members thereunder shall be computed according to the portion of the joint family property allotted to him or it at the partition, whether total or partial.

8. The above provisions shall, so far as may be, apply in relation to the levy and collection of any penalty, interest, fine or other sum in respect of any period up to date of the partition, whether total or partial, of a HUF as they apply in relation to the levy and collection of tax in respect of any such period.

There is no ipso facto partition of joint Hindu family properties immediately after the death of a male coparcener of the Mitakshara School having coparcenary interest in the coparcenary property. The death has nothing to do with the actual disruption of the status of a HUF. It freezes or quantifies the share of a female heir in the coparcenary property on account of the death of a coparcener at the relevant point of time. Therefore, there was no partition and disruption of the HUF as per Income tax 1956 Act.

Residential Status of HUF

Section 6 (2) of the Income-tax Act, 1961, clearly contemplates a situation where a HUF can be non-resident also. In fact, HUF can also be Not Ordinarily Resident. HUF will be considered to be resident in India unless, during the previous year, the control and management of its affairs is situated wholly outside India. In such a case, it will be treated as non-resident HUF.

Section (6) (b) of the Income-tax Act, 1961 further provides that, in case of a HUF whose manager has not been resident in India in nine out of ten previous years preceding the previous year or has, during the seven previous years preceding that year, been in India for a total 729 days or less, such HUF is to be regarded as not-ordinarily resident within the meaning of the Income-tax Act, 1961. As such, it is not necessary for a HUF to be resident in India.

In case of change of Karta of HUF during the year, the residential status of HUF can be determined by considering the period of stay in India of both Karta of HUF i.e. previous Karta and successive Karta.

Under the Income Tax Act the residential status is determined with reference to the previous year relevant to a particular assessment year. Therefore the residential status of HUF may also be different for different assessment years considering the facts of relevant previous year.

The test is not where the Karta resides; the test is where the control and management of the affairs of HUF is situated. Even if a part of control and management is situated in India, such HUF will be treated as resident in India.

Though, generally, Karta is supposed to manage the affairs of HUF, it is not an absolute rule and, by consent, the power of control and management may be delegated to other members of the family, either fully or partially.

The relevant factor for determining the status is where the control and management of HUF is situated (even in part). Therefore the HUF may be resident even where the Karta was residing outside India for whole of the year.

As per Section 10(2) of the Income-tax Act, 1961, any sum received by an individual from Hindu Undivided Family of which he is member is exempt from tax.

But the amount received not as a member of Joint Family but in pursuance of some statutory provision, etc. would not be exempted in this section. Also the position of member of joint family in law to claim the right u/s 10(2) does not get affected only with the reason that they are living apart from the other members of the family.

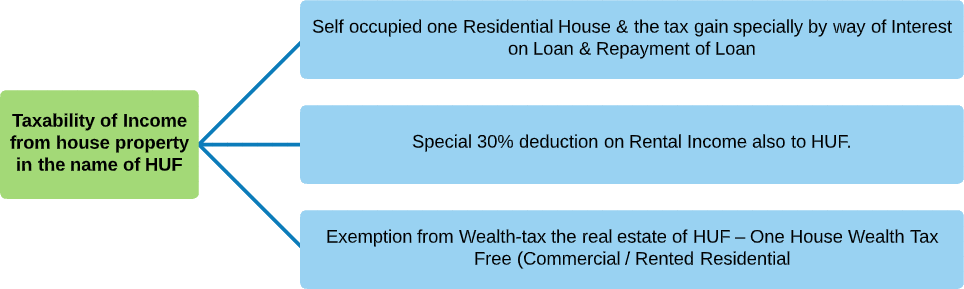

Taxability of Income from house property in the name of HUF

Property purchased with the aid of joint family funds, howsoever small that may be, still the property would be HUF income and cannot be income of the individual with major portion of purchase price.

Proprietorship and Partnership by HUF

A HUF is undoubtedly a “Person” within the meaning of section 2(31), it is however not a juristic person for all purposes and cannot enter in to an agreement of partnership either with another HUF or Individual. It is open to the manager of a Joint Hindu family, as representing the family, to agree to become a partner with another person. And therefore any remuneration received by Karta would be the personal income of Karta and not the income of the HUF as there is no real connection between the investment of the assets of HUF and remuneration received by Karta. The remuneration received by Karta as representative of HUF cannot be treated as income of the HUF. Remuneration will be income of HUF only when there is direct nexus between family funds and remuneration paid. Where the receipt is a compensation made for the services rendered and not for the return of investment, it is to be treated as individual income of the partner. However, where members of HUF become the partners in a firm by investment of family funds & not because of any Special Services rendered by them, then the income will belong to HUF. Once the character of an individual has been treated differently than HUF for the purposes of interest, there is no reason as to why that would not extend to the salary and bonus paid to such partners on account of their personal services rendered to the firm in contra-distinction to their capacity as representatives of HUF . Therefore, the same reasoning would apply to the cases where payment in the form of salary and bonus has been made to a partner in his individual capacity in contra-distinction to his representative character of the HUF.

As per Section 40(b)(i) “in the case of any firm assessable as such,— any payment of salary, bonus, commission or remuneration, by whatever name called (hereinafter referred to as “remuneration”) to any partner who is not a working partner” Partner of a firm is an individual even if he is partner as a representative of HUF. Where assessee-firm paid salary to a partner who was actively engaged in conducting affairs of business of firm, it was to be held that assessee-firm would be entitled to deduction in respect of salary paid to said partner even though he was a partner in representative capacity of HUF. Salary paid to working partner even though as Karta of HUF, is received as individual and as working partner, hence allowable as deduction while computing income of firm. It is individuals of HUF who indirectly become partner in firm in which HUF is said to be partner and therefore provisions of Section 40(b) that prohibits deduction of payments of commission to any partner who is not a working partner, in computing income under the head PGBP, will not be applicable. Therefore deduction of any commission payable to any individual of HUF shall be allowable. Where a person is a partner in a partnership firm not in his individual capacity but as the karta of the Hindu undivided family, the income accruing to his wife on account of her being a partner in the same partnership firm cannot be included in the total income of such person in an individual assessment or in the assessment of the Hindu undivided family. Section 78 shows that where succession to business is by inheritance, then loss will be allowed to be set-off and not otherwise.

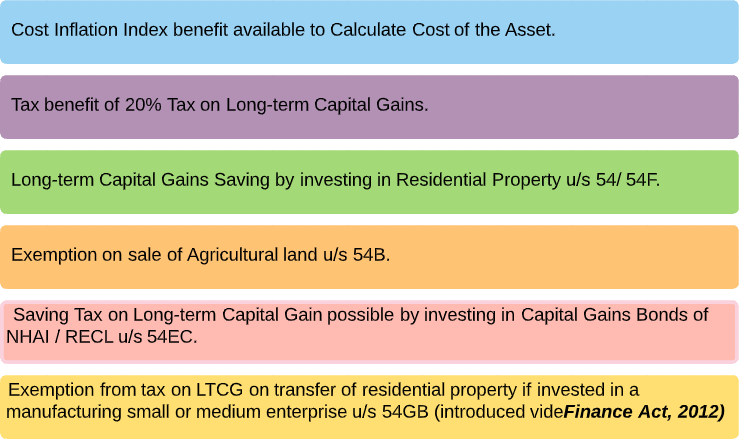

Capital Gain Exemption available to HUF

General provisions applicable to HUF:

1. In order to avail the benefit of adopting market value as on say,1-4-1981, the Capital asset should have become property of previous owner before 1-4-1981 to make assessee entitled to benefit of adopting market value as on 1-4-1981 but where construction of building was completed in 1988 and possession of flat was handed over to previous owner, i.e., HUF, it could not be said that flat itself became property of HUF prior to that date and, hence, assessees were not entitled to adopt market value of flat as on 1-4-1981. So indexing had to be allowed of the financial year in which flat was held by assessee on partition of HUF.

2. When an individual assessee or an HUF assessee sells a residential building or land appurtenant thereto, he can invest capital gain for purchase of a residential building to seek exemption of the capital gain tax. The expression ‘a residential house’ should be understood in a sense that building should be residential in nature and ‘a’ should not be understood to indicate a singular number. That when an HUF’s residential house is sold, the capital gain should be invested for the purchase of only one residential house, is an incorrect proposition. After all, the property of the HUF is held by the members as joint tenants. If the members, keeping in view the future needs in event of separation, purchase more than one residential building, it cannot be said that the benefit of exemption is to be denied u/s 54(1). Therefore, the benefit u/s 54 can be available on purchase of more than one residential house Properties by HUF.

3. If the agricultural land sold was of the HUF of the assessee but the flat purchased in the co-operative society was not in the name of the HUF, to claim benefit u/s 54F, residential house which is purchased or constructed has to be of same assessee whose agricultural land is sold.

(4). If HUF transfer a land which is used for agricultural purposes by a HUF, the rollover relief u/s 54B is available to the HUF. The amendment is applicable on transfers made after 01-04-2013.

5. Under section 48, any payment made by assessee for education, maintenance and marriage of his unmarried daughter, though under consent decree, could not be said to be an expenditure wholly and exclusively incurred in connection with transfer of property or could also not be considered as a cost of acquisition or cost of improvement.

Capital Gain Exemption available to HUF

Exemption from tax on Long Term Capital Gain (LTCG) on transfer of residential property if invested in a manufacturing small or medium enterprise is available to an Individual or HUF subject to the condition that

- Transfer made on or before 31st March, 2017.

- Amount is reinvested before due date of furnishing return of income u/s 139 (1)

- In Equity of a new start up SME company in the manufacturing sector in which in hold more than 50% share capital or voting rights

- Amount is utilized by the company for purchase of new plant & machinery

- The share cannot be transferred within a period of 5 years

At the time of Sale of any Real Estate Property, Tax is liable to be paid on the Gains earned on the sale of the Real Estate Property. Such Gains could either be Short Term Capital Gains or Long Term Capital Gains. The basis of such Classification in the Income Tax Return has been given below:- Short Term Capital Gain (STCG): If the Real Estate Property is held for less than 24 Months taxed as per normal Income Tax Slabs Long Term Capital Gain (LTCG): If the Real Estate Property is held for more than 24 Months taxed at 20%. In case a loss arises on the sale of a property, the capital loss can be set-off against other Capital Gains in that year. If the Loss cannot be set-off against capital gain in that year, it can be carried forward for the next 8 years and set-off in the future years. However, loss can only be carried forward if the return was filed before the due date.

The Capital Gains would be computed using the following formula

| Full Value of Consideration/ Sale Price | XXX | |

| (Less) | Expenditure incurred wholly and exclusively in connection with such Transfer/Sale | (XXX) |

| (Less) | Cost of Acquisition/ Purchase Price | (XXX) |

| (Less) | Cost of Improvement | (XXX) |

| Gross Capital Gains | XXX | |

| (Less) | Exemption (if any) available u/s 54B/54D/54G/54GA for LTCG or Exemption (if any) available u/s 54/54B/54D/54EC/54ED/54F/54G for STCG | (XXX) |

| Capital Gains | XXX |

Capital Gains Tax Rate on Sale of Shares and Mutual Funds

Long Term Capital Gains arising on the sale of Shares and Mutual Funds are exempted under Section 10(38) and Short Term Capital Gains arising on the sale of Shares and Mutual Funds are taxed @ 15% under Section 111A provided that:-

- The transaction of sale is entered into on or after 1-10-2004 and

- Such transaction is chargeable to Securities Transaction Tax (STT) i.e. the sale transaction is through recognized stock exchange or sale of units of equity oriented fund is to a Mutual Fund.

Short Term Capital Gains on sale of Shares and Mutual Funds u/s 111A

Tax on short term capital gains is levied at a flat rate of 15% under Section 111A if the above mentioned 2 conditions are satisfied. However, where the income of the individual tax payer other than the short term capital gains is less than the minimum amount exempted from tax as per Slab Rates i.e. 250000, then the short term capital gains shall be reduced by an amount by which the other incomes fall short of 250000.

Taxability of gift received in cash or in kind by HUF without consideration

1. If any sum of money exceeding 50,000 is received by the HUF without consideration then provisions of section 56(2)(vii) are applicable and the same is taxable in the hands of HUF.

2. Gift received in kind by HUF without consideration is also taxable subject to the provisions of s. 56(2)(vii) which states that any sum or property received without consideration or inadequate consideration by an HUF from its members would also be excluded from taxation.

In case of HUF, relative means members of the HUF.

- The gift made by the family of a sole coparcener to the wife of the Karta of the family is considered to be VALID.

- Gift by HUF to bride of male member in the form of jewellery at the time of marriage is valid. Obligation of Karta is towards marriage of both sons & daughters.

- Gift of HUF Property by Father Within reasonable limits as a “gift of affection” to a wife, daughter & son.

- A coparcener can dispose of his undivided interest in the coparcenary property by a will, BUT he CANNOT make a gift of such interest. It is said to be void.

- Gift to a stranger of a joint family property by the manager of the family is void. Manager has NO absolute power of disposal over HUF property

- The gift of family property by Karta of an HUF to coparceners or non¬coparceners is void

- Hindu father can make a gift of ancestral property within reasonable limits at the time of marriage or even long after marriage

- The Karta is empowered to make gifts to his wife within reasonable limit of the movable assets. But the Karta CANNOT make gifts to his second wife. It is invalid.

- Gift made by Karta to nephew & interest on the amount gifted was deposited in the firm. It was held that gift was void.

- Gift by Karta to minor children of family- Gift made by Karta from Natural love & Affection within reasonable limits, the gift was said to be Valid.

- Gift on Marriage Occasion is valid.

Return of Income

HUF is required to furnish return in Form ITR-2 or ITR-3 or ITR-4S or ITR-4, as the case may be. However, ITR-4S (Sugam) not applicable to residents HUFs

- having assets (including financial interest in any entity) located outside India; or

- signing authority in any account located outside India. [Inserted vide Finance Act, 2012] In case of above HUFs, the return to be furnished

- electronically under digital signature, or

- transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V.

Note: E- filing is mandatory if total income exceeds 10 lakhs. HUFs to whom Section 44AB is applicable, shall furnish the return elec¬tronically in ITR-4 under digital signature. I. Clubbing Provisions of Section 64(2) in case of HUF Where any member of HUF converts any property belonging to it, in to the common property of HUF, then individual shall be deemed to have transferred the property to the HUF i.e. to the members of the family for being held by them jointly. The Income from the property so transferred shall be taxable in the hands of Individual and not in the hands of HUF. On partition amongst the members – the income derived from such property as is received by the spouse shall be taxable in the hands of spouse itself. Demand against member of HUF can be recovered from HUF to the extent of its share in property of HUF. The Act recognizes status of HUF different from individual status of Karta of HUF and two are treated as different legal entities, it is necessary that notice u/s 148 should be sent in correct status because jurisdiction to make assessment is assumed by issuing valid notice and it cannot be conferred by consent of parties. After having issued notice u/s 148 to individual, AO had no jurisdiction to assess HUF of assessee and that defect of jurisdiction could not be cured by obtaining consent of assessee to assess him in status of HUF. Joint family property does not lose its character merely because at one point of time there was only one male member or one coparcener. An assessee who has received share on partition of HUF property but subsequently gets married is entitled to be assessed in respect of the said share in said property in status of HUF.

Key points in creation of HUF and format of deed for creation of HUF

- Under the Income Tax Act, an HUF is a separate entity for the purpose of income tax return.

- The same tax slabs are applicable to HUF as to individual assessee.

- You cannot transfer your own assets/money into HUF.

- If you have ancestral property and earning some income from this property, then it is better to transfer this asset to HUF and save tax up to exemption limit applicable to individual.

- You can transfer the money received on sale of ancestral property /assets into your HUF.

- The income from property of HUF can be further invested in instruments such as shares, mutual funds, etc. and will be assessed under HUF.

- Existence of property or multiple members is not a pre-requisite to create HUF. A family which does not own any property may still have the character of Hindu joint family. This jointness is understood in terms of faith and food. This is because as a Hindu is born as a member of the joint family.

- Any gifts received by the members of HUF (birthday, marriage, etc.) can be treated as assets of HUF.

- The HUF is taxable as separate person under income tax hence one can save tax from basic exemption of 2.5 lakh. HUF will also gain from the tax slab structure of computing income tax.

- Apart from basic exemption of 2.50 lakh, section 80C deduction up to 1.50 lakh is also available.

Features of a Hindu Undivided Family (HUF) Deed

Creating a HUF makes your family a separate entity and offers various features like:

- Own PAN Card for separate tax returns

- Exemptions & deductions under Section 80

- Separate insurance policy

- Payment of salary to members

- Investment from HUF’s income

- Pay the same tax as an individual

- Separate bank account for the HUF where the assets, funds, etc., can be maintained.

- HUF deed that has written declaration of all the members and their agreement to making the assigned person the Karta and giving him the powers and responsibilities of decision-making for the family.

- A specific name

Conclusion

Hindu Undivided Family (HUF) is just a normal prevailing condition in the Hindu Society. It must be noted that HUF is a creature of law and cannot be created by act of parties or by executing a contract deed. Hindu Undivided Family is different from a Hindu coparcenary. Hindu coparcenary is a special feature of the Mitakshara School of Hindu Law. It consists exclusively of male members, much narrower than Hindu Undivided Family. A coparcenary includes only those who acquire by birth an interest in the joint or coparcenary property. No coparcenary can commence without a common male ancestor. It may be recalled that the Hindu Succession Act, 1956 has been amended w.e.f. 09.09.2005 with a view to give daughters on birth equal rights as a son on his birth. Consequently, the daughter has the right to be a coparcener and also a right to claim partition or vest her individual property in the HUF. These are important rights hitherto denied to the daughter. To create HUF, at least two coparceners are required either son or daughter. Therefore only husband and wife cannot create an HUF, unless the property has been received by a coparcener on partition or otherwise. However, there is no impediment to starting a new HUF by gift from family members. In short, even a husband and wife can create HUF if (a) they have received the property on partition or (b) they have received a gift for HUF. There's no need to fill an application form or submit KYC documents for joining an HUF. All lineal descendants of the Karta, their spouses and children automatically become members of his family. Wives join the HUF as members, while children join on birth as coparceners. Even the unborn child of a member or co-parcener has an equal share in the HUF. The Karta will have to maintain the books of accounts of the HUF and file tax returns on its behalf. The date of filing tax returns and the tax rate are no different from that of individual taxpayers. He also needs to invest to save tax under Section 80C and 80CCF.

Frequently Asked Questions

- 1.What is a HUF?

-

HUF means Hindu Undivided Family. You can save taxes by creating a family unit and pooling in assets to form a HUF. HUF is taxed separately from its members. A Hindu family can come together and form a HUF. Buddhists, Jains, and Sikhs can also form a HUF. HUF has its own PAN and files tax returns independent of its members.

- 2.How is HUF taxed?

-

- HUF has its own PAN and files a separate tax return. A separate joint Hindu family business is created since it has an entity separate from its members.

- Deductions under section 80 and other exemptions can be claimed by the HUF in its income tax return.

- HUF can take an insurance policy on the life of its members.

- HUF can pay a salary to its members if they contribute to its functioning of the HUF. This salary expense can be deducted from the income of HUF.

- Investments can be made from HUF’s income. Any returns from these investments are taxable in the hands of the HUF.

- A HUF is taxed at the same rates as an individual.

- 3. Who is the Karta of an HUF?

-

The head of a HUF is called the Karta; he is the senior-most male member of the family.

- 4. Can a Woman be HUF Karta?

-

Yes! Until January 2016, a woman could not be the HUF Karta. But in a landmark case, the Delhi High Court ruled in favor of a female being the Karta of a HUF. However, the same has not been incorporated in the Income Tax Act as yet.

- 5. Who are HUF Coparceners?

-

All the members of the Karta’s family can be members of the HUF. The male members are called coparceners, while the females are referred to as just members. The difference between the two is that any of the coparceners can demand partition of the HUF. The female members do not have this right in most parts of the country, except for some states like Maharashtra and Tamil Nadu that have allowed unmarried daughters to function as coparceners. The Hindu Succession (Amendment) Act, 2005 which came into force from September 9th September 2005 removed this gender discrimination by giving equal rights to daughters as sons. The daughters become the coparceners of their father’s families on birth in the same manner as sons and have the same rights as sons in the family properties.

- 6. Can a daughter claim a share in her father’s property where her father had passed away before the amendment made in 2005, giving equal rights to daughters and sons?

-

No. Both the daughter and the father has to be alive on the date of the amendment for the daughter to get the benefit, irrespective of whether she has been married or not on that date. If the father has passed away before the amendment date, then she wouldn’t have been a daughter on the date of the amendment. Hence she cannot claim a share in father’s property.

- 7. Are there any incomes which are not taxed as income of HUF?

-

The following incomes are not taxed as income of HUF-

- If a member transfers his self-acquired property to the HUF without receiving proper sale consideration, income from such property is not taxable in the hands of the HUF. It will continue to be taxed in the hands of the member.

- Personal income of the members cannot be treated as income of HUF..

- “Stridhan” is an absolute property of a woman; hence income from it is not taxable as income of HUF.

- Income from an individual property of the daughter is not taxable in the hands of HUF even if such property is vested into HUF by the daughter.

- 8. Is there any minimum number of coparceners required for an entity to be taxed as HUF?

-

A HUF can be formed with just two members one of whom is a coparcener. But for an entity to be taxed as a HUF, it should have at least two coparceners. For instance, if HUF consists of only the husband and wife, then there is only one coparcener. So it will not be taxed in the hands of HUF except in the case where the funds are received on the partition of larger HUF. It will be taxed in the hands of a sole coparcener.

- 9. Should a HUF always be a resident of India?

-

It is not necessary that a HUF must always be a resident of India. In case the control and management of the HUF are situated outside India, the HUF would be a non-resident. Where the affairs of the HUF are managed from outside India, the HUF would be a non-resident.

- 10. Karta of HUF sits outside India. HUF is managed by the other members residing in India. Will HUF be a non-resident?

-

The residential status of a HUF is determined not on the basis of where the Karta resides but on the basis of where the HUF is managed from. In this case, though the Karta resides outside India, the HUF is managed by members from India and hence the HUF will be a resident of India.

- 11. Can the members of the HUF and the HUF separately claim deduction under Section 80C?

-

The HUF being a separate taxable assessee, can claim a deduction under section 80C. However, the member and the HUF cannot claim a deduction in respect of the same investment made or expense incurred.

- 12. Upon the demise of the Karta, who takes over the title ‘Karta’?

-

Upon the demise of Karta, the eldest male member of the family becomes the Karta of the family. Even when the deceased Karta’s wife is alive, the eldest son or any other eldest male member of the family will take over that position.

- 13. What happens if the eldest male member of the family is an NRI?

-

A HUF is considered to be a resident of India if the control and management of its affairs happen wholly or partly in India. In some cases, the Karta of the family may be non-resident. The resident status of the family will not change to be non-resident only because the Karta is a non-resident unless the decisions concerning the family are made outside India.

- 14. Does HUF arise from a contract?

-

No HUF arises only from status.

- 15. What is ancestral property?

-

It is the property, which a man inherits from any of his three immediate male ancestors, i.e., father, grandfather, and great-grandfather.

- 16. Whether a single person can constitute HUF?

-

No. A single person cannot constitute HUF. There have to be a minimum of two members to constitute a HUF. The existence of estate or property is not an essential requirement to form a Hindu Undivided Family. Under Hindu Law, an HUF is a family which consists of all persons lineally descended from a common ancestor and includes their wives and unmarried daughters. An HUF cannot be created under a contract; it is created automatically in a Hindu Family.

- 17. What is HUF under Income Tax Act?

-

A HUF is recognized under Income Tax Act as a separate assessable entity if two conditions are satisfied:

- There should be a coparcenership.

- Coparcenery is joint inheritance or heirship of property. Coparcenership is said to exist in a Hindu Undivided Family if the right to joint enjoyment, the right to call for partitition and the right of survivorship is held in coparcenary.

- There should be a joint family property which consists of ancestral property, property acquired with the aid of ancestral property and property transferred by its members.

- Ancestral property is any property which a man inherits from any of his three immediate male ancestors, i.e. his father, grandfather and great grandfather. Property inherited from any other relation is not treated as ancestral property.

Finally, it is important to note that once a joint family income is assessed as that of HUF, it continues to be assessed as such in subsequent assessment years till partition is claimed by coparceners.

- 18. Can there be HUF with only female members?

-

Yes. As so long as the property which was originally of the joint Hindu family remains in the hands of the widows of the member of the family and is not divided, HUF can continue with female members.

- 19. Can Karta gift HUF property?

-

Gift by Karta of HUF, a movable property or an immovable property within reasonable limits in favor of his daughter is permissible on the occasion of her marriage.

- 20. Which Individuals are part of HUF?

-

HUF consist of Co-Parceners (who are Family Members) and the distant relatives i.e. called as Members of HUF.

- 21. Who are Co-Parceners and Members?

-

Co-Parceners: Co-Parceners are the Family Members and it is consist of 4 levels of Lineal descendants including the first male ancestor. It is only a Co-Parcener who can demand the Partition of HUF. It will include the following:

- Karta

- Son/ Daughter of Karta

- Grandson/Granddaughter of Karta

- Great Grandson/ Great Granddaughter of Karta

Members of HUF: Any other distant Relatives who are not the Family Member (e.g. Brother-in-law, Sister-in-law etc.) would be deemed as the Member of HUF. Although they are Members of HUF, they are not the Co-Parceners. A member cannot demand the Partition of HUF.

Important Note: Wife is not considered as the direct part of HUF i.e. Co-Parcener. She will be a Member in Husband’s family HUF. Although, She will be a Co-Parcener in her Father’s Property. All co-parceners are members, but all members are not co-parcener. - 22. Is there any minimum number of co-parceners required for an entity to be taxed as HUF?

-

A HUF can be formed with just two members one of whom is a co-parcener. But for an entity to be taxed as a HUF, it should have at least two co-parceners. For example; when any HUF consist of only Husband and Wife, then there is only one co-parcener (because the wife is a member but not a co-parcener) and therefore, in such case income can’t be taxed in hands of HUF. It will be taxed in the hands of Individual Co-Parceners.

- 23. Can HUF pay remuneration to Karta or Any Member of HUF?

-