Joint Venture Registration in India

MCA specified the meaning of joint venture as-“joint venture, would mean a joint arrangement, entered into in writing, whereby the parties that have joint control of the arrangement, have rights to the net assets of the arrangement. The usage of the term is similar to that under the Accounting Standards.”

A Joint Venture may be defined as any arrangement whereby two or more parties co-operate in order to run a business or to achieve a commercial objective. This co-operation may take various forms, such as equity-based or contractual Joint Ventures. It may be on a long-term basis involving the running of a business in perpetuity or on a limited basis involving the realization of a particular project. It may involve an entirely new business, or an existing business that is expected to significantly benefit from the introduction of the new participant. A Joint Venture is, therefore, a highly flexible concept. The nature of any particular Joint Venture will depend to a great extent on its own underlying facts and characteristics and on the resources and wishes of the involved parties. Overall, a Joint Venture may be summarized as a symbiotic business alliance between two or more companies whereby the complimentary resources of the partners are mutually shared and put to use. It is an effective business strategy for enhancing marketing, positioning and client acquisition which has stood the test of time. The alliance can be a formal contractual agreement or an informal understanding between the parties.

Global proliferation of business and commerce has given an international dimension to Joint Ventures. Corporate entities across the globe seek cross-border alliances to share the resources, opportunities and potential to deliver cutting edge performance. Such alliances are designed to suit the commercial requirements of parties and vary from a mere transitory arrangement for one partner to establish its presence in a new market to a calculated step towards a full merger of the technologies and capabilities of the partners.

In sectors where 100% FDI is not allowed in India, a joint venture is the best medium, offering a low risk option for companies wanting to enter into the vibrant Indian market. All companies registered in India, even those with up to 100% overseas equity, are considered the same as local companies.

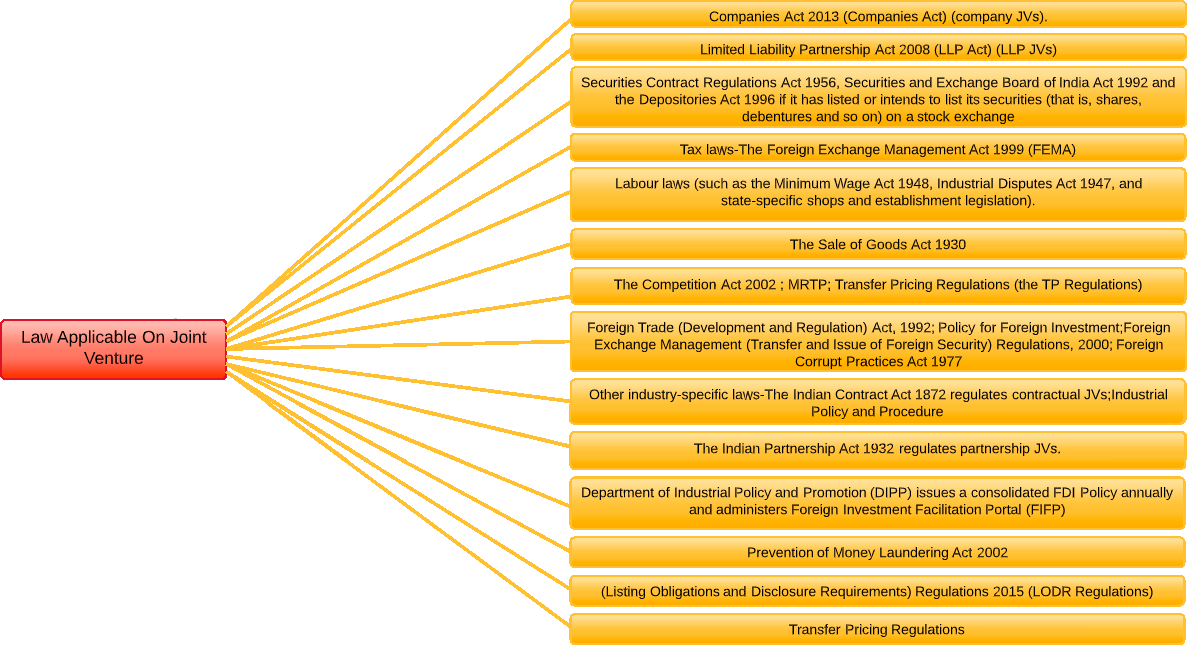

Corporate joint ventures are regulated by the Companies Act, 2013 and the Limited Liability Partnership Act, 2008.Corporate Joint Ventures will also be subject to the country’s tax laws, The Foreign Exchange Management Act of 1999, labor laws (such as Code on Wages Act, 2019, Industrial Disputes Act, 1947, and state-specific shops and establishment legislation), The Competition Act of 2002, and various industry-specific laws.

A Joint Venture may be formed with any of the business entities existing in India.

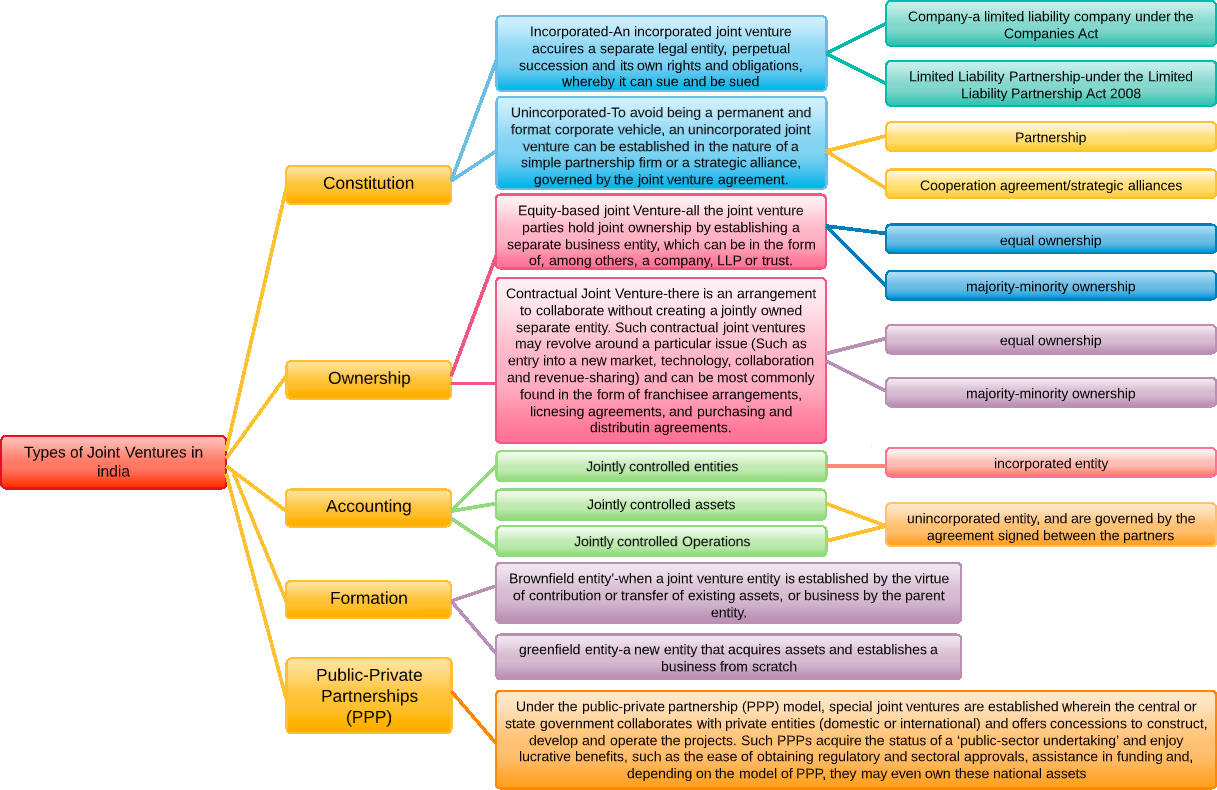

Types of joint ventures in India

Advantages of joint ventures

Leveraging Resources

Exploiting Capabilities and Expertise

Improved economies of scale

Synergy benefits

Strategic Alliance

Sharing Liabilities & Responsibilities

More risk mitigation

Increased technology transfer

Market Access & New market penetration

Flexible Business Diversification

Success factors in a strategic JV

Agreement

Among the terms that should be clearly defined from the outset are the timespan of the venture, performance norms, and governance processes. A joint venture board should be established and agreement reached as to the scale of investment required from each party. Whether the parties will extract surplus cash or reinvest it into the business, along with a potential exit strategy, are other significant considerations.

Alignment

Successful JVs are founded on shared objectives. The partners’ risk/reward strategies must be aligned to ensure both derive value from the arrangement.

Development

The strategic partnership, as well as the relationships between parties, are ongoing, rather than static, and need to be developed. Frequent communication is required to foster a feeling of belonging amongst employees on both sides.

Flexibility

Parties should be aware of potential differences in business culture and decision-making processes and deal with any issues that arise in a flexible manner.

Limitations of joint ventures

![]()

Limited control

Unlike a wholly owned subsidiary, a joint venture company offers a limited degree of control to both the entities. This is due to a very obvious reason that both, the Indian as well as the foreign company, have almost equal stake in a joint venture. Therefore, if a foreign entity is willing to reap the advantages like sharing of risks, easy entry into Indian markets, taking advantage of infrastructure set up, etc., rather than exercising full control of the new company, then setting up of a joint venture with an Indian company is best suited.

![]()

Cultural and social differences

Every country has its own way of doing business. In a joint venture, two or more companies from different mindsets, social and cultural backgrounds come together for doing business. Indian company might fear complete acquisition by its foreign collaborator. On the other hand, foreign entity might be apprehensive about Indian entity before investing such a huge amount of capital. Thus, both the collaborators must be sure about their compatibility with each other and willing to sort out their differences for a smooth and profitable business ahead.

![]()

Imbalance in the levels of expertise

investment, or assets brought into the venture by the different parties may lead to problems between the two parties. One party or the other may begin to feel that it is contributing the lion’s share of resources to the project and resent a 50/50 distribution of profits. This can be avoided by frank discussions and clear communication during the formation of the joint venture, so that each party clearly understands – and readily accepts – its role in the JV.

![]()

Choosing the right partner

Before entering into a joint venture with any Indian company, the foreign investor must understand what it shall gain from this joint venture. It must suit to the requirements of foreign entity. For example, if a foreign investor is ready to contribute in terms of capital, knowledge and skill and technology but lacks in setting up of infrastructure, manpower, access to Indian markets, then the proposed Indian collaborator must compensate for it

![]()

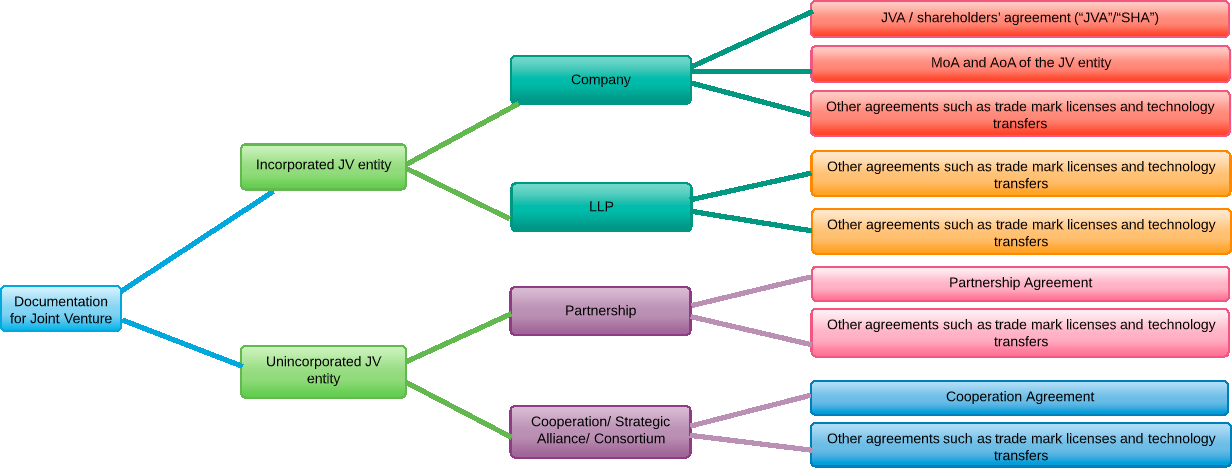

Documentation in a Joint Venture

Transactions in a joint venture demand efficient and clear documentation. Depending upon the nature of the structure, definitive agreements would be drafted and executed, which will set out terms and conditions for both the partners. A few examples are, joint venture agreement, shareholder’s agreement, memorandum and articles of association or any other agreement for collaboration.

Common sectors of Joint Venture

Joint ventures in India are used across sectors; however, they are more prevalent in high-technology, high-capital or high-technical skills sectors. Foreign investments can be made under the ‘automatic route’ (no prior approval from the government is required before investing) or the ‘approval route’ (prior approval of the government is mandatorily required). In an attempt to simplify the rules and regulations pertaining to the FDI regime in India, the Department of Industrial Policy and Promotion (DIPP) issues a consolidated FDI Policy annually, which subsumes all prior press notes, press releases and clarifications issued by the DIPP and reflects the current policy framework on FDI. Recently, the Foreign Investment Promotion Board, which was an inter-ministerial body responsible for processing FDI approvals and recommending government approvals, was abolished and replaced by the Foreign Investment Facilitation Portal (FIFP), which is administered by the DIPP. The FIFP serves as an online interface between foreign investors and the government of India and facilitates the approval and clearance of applications through a ‘single window’ system.

Joint venture parties working together to increase synergy, some of these joint ventures are governed by the rules prescribed under a particular statute and, generally, as prescribed by exchange-control laws

- Insurance companies are required to be owned and controlled by Indian parties as per the rules stipulated by the Insurance Regulatory Authority of India. As a result of this regulatory requirement, many international insurance companies have formed joint ventures with Indian companies.

- In the defense sector, Indian companies are being encouraged to enter into joint ventures with foreign entities that have high technological expertise, whether in air, land or sea-related defense equipment under the ‘Make in India’ initiative of the Indian government.

- Strategic alliances and technology-transfer agreements between Indian and foreign partners are extremely prevalent in the technology, media and telecom sectors, which provide great investment opportunities in diverse areas such as software development, hardware, print media, sports and outsourcing.

- Multiple foreign asset-management companies have formed joint ventures with Indian banks and financial institutions

- Other sectors where joint ventures are commonly used and have witnessed a rise in participation by foreign parties are the power sector and railway infrastructure sector.

- Some sector-specific rules have to be followed for foreign investors, for example:

- the pharmaceutical sector (where non-compete clauses are not permitted in foreign-investment joint venture agreements);

- the aviation sector (security clearance for foreign personnel);

- Single-brand retailing (30% domestic sourcing norms for foreign direct investment (FDI) beyond 51%);

- The defense sector (the joint venture company, along with the manufacturing facility, should have a maintenance and life cycle support facility for the product being manufactured in India); and

- multi-brand retailing (minimum amount to be brought in as FDI would be US$100 million and 30% of the value of procurement of manufactured or processed products will be sourced from Indian micro, small and medium-sized industries, which have a total investment in plant and machinery not exceeding US$2 million).

Law Applicable On Joint Venture

Nature of joint venture

Management of JV companies

- The management constitution, control, and safeguards should be agreed upon when preparing the memorandum of understanding (MoU) as Memorandum of Association (MoA) and Articles of Association (AoA), serves as the charter documents of the company

- Foreign investors should note that in India, the JV agreement between the partners will not bind the JV company unless its terms are included in the AoA of the JV company.

- Further, to avoid future conflicts, the JV parties should include a provision in the JV agreement stating that if the AoA is inconsistent with the provisions of the JV agreement, then the parties will amend the MoA and AoA accordingly.

Exit strategy

- The exit strategy depends on the type of entity that was constituted

- the Indian joint venture agreement may also provide for the termination of operations and the liquidation and closure of the venture. Any of those options can be used independently or in combination with each other.

- The general exit options available are: buy-sell agreements, unilateral sale rights, and, put/call rights.

Profit repatriation

- India allows free of charge repatriation of profits once the entire domestic and federal (tax) liabilities are met.

- Investment exit processes are also fairly simple, and profits can be repatriated once all the tax debt and other compulsions are fulfilled.

- Troubles only arise when people escape or dodge these liabilities, or do so out of ignorance.

Royalty payments

- Earlier there were monetary caps on remittances (both lump sum fees and royalties) made for technology collaborations and license or use of trademark or brand name.

- Now, these restrictions and caps have been removed.

Pre-incorporation due diligence

- Overseas firms should conduct a formal due diligence check to evaluate the expectations and limitations of the Indian associate, to check the validity of the partners’ business operations, to review the validity of the documents produced by the prospective partners, and to evaluate any risk factors associated with the potential partners.

Tax consideration

- The sale of shares in an Indian company is usually taxed in India as capital gains, even if the seller is not a resident of India. India taxes such capital gains as well as interest payments at variable rates.

- Therefore, overseas entities and foreign investors are generally advised to invest through an intermediate jurisdiction. India has entered into double tax avoidance agreements (DTAAs) with countries across the world.

- Some of these DTAAs contain beneficial provisions with regard to capital gains tax and withholding taxes on interest payments.

HR due diligence

- In a joint venture undertaking, it becomes very important to legally establish whether the employees are recruited as rehires or transferred from one of the existing partner entities; each will have its own set of legal implications

- An employment contract in India typically includes provisions on duties and responsibilities, non-disclosure of confidential information, assignment of intellectual property, non-compete, non-solicitation and termination, as well as the company’s leave taking policy (casual leaves/sick leaves/privileged leaves).

- Nevertheless, foreign employers are advised to have a detailed employment contract in place, particularly if they operate in the information technology (IT) or knowledge industry sectors where employees are likely to generate forms of intellectual property.

Intellectual property rights

- India recognizes different types of intellectual property (IP), which are protected under separate laws. As a result, registering intellectual property involves navigating complex legalities and submitting numerous documents

- This requires expertise and familiarity with procedural norms to ensure fast and effective registration. Overseas investors entering into JVs in India can protect their IP through registration and detailing provisions in the joint venture agreement.

- Additionally, independent documentation may also be executed, such as a name and logo license agreement (also known as a registered user agreement) with Indian organizations.

- Typically, the licensing agreement, know-how agreement, technical services or technical assistance agreement, royalty payment, franchise agreement, and agreement including all other profit-making matters, including the use of intellectual property rights form annexes or attachments to the main joint venture agreement.

Due diligence before entering into a joint venture agreement

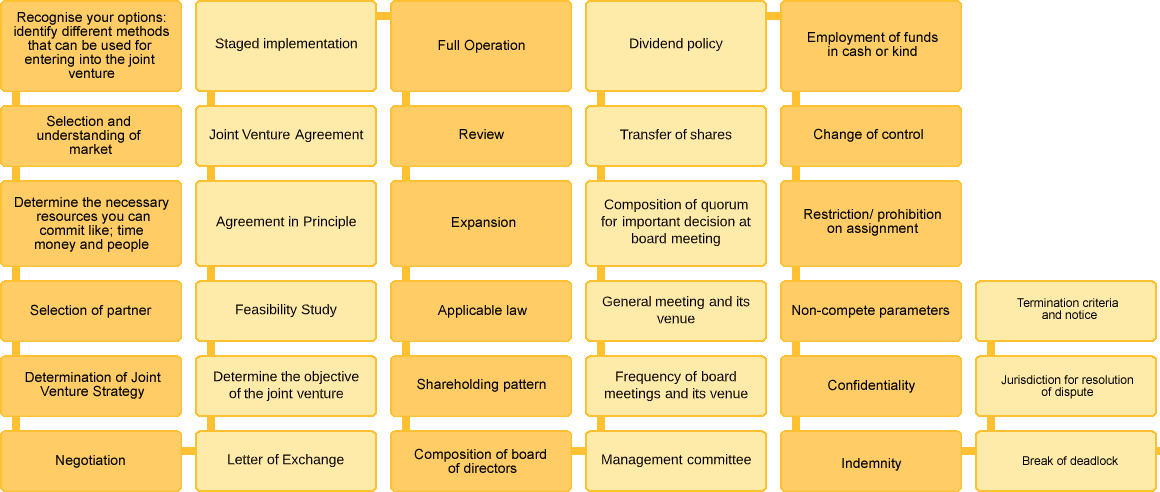

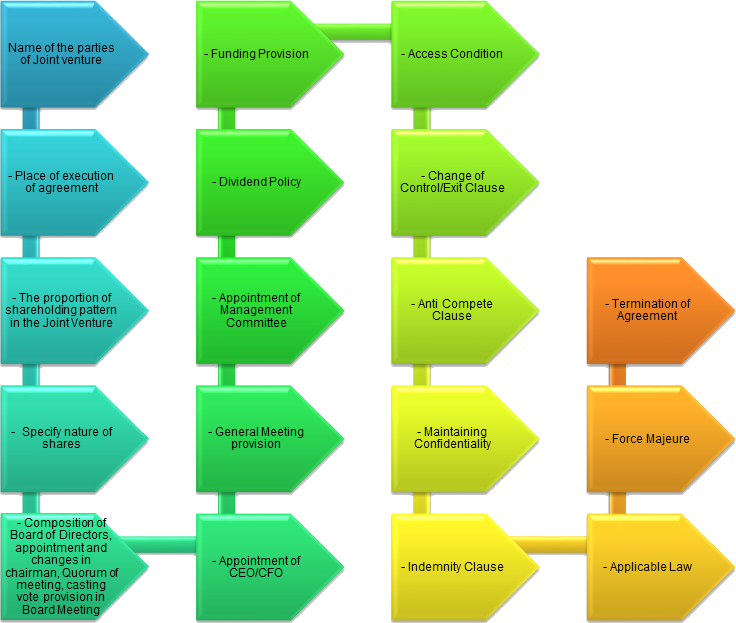

Important Clause of Joint Venture Agreement

Tax implications

- Income of a Joint Venture projects, may be assessed in the status of an ‘Association of persons’ under the Income-Tax Act.

- The deductions under Section 80-IA or Section 80-IB, etc., will be available to such a Joint Venture assessable in the status of an AOP.

- No share of income of such AOP, fully deductible under Section 80-IA or 80-IB, would be liable to tax again in the hands of the members thereof

- The IT Act provides that taxability of an entity that is resident in a jurisdiction with which India has signed a double-taxation avoidance agreement (DTAA) would be governed under the provisions of the IT Act or the relevant DTAA, whichever is more beneficial to such non-resident taxpayer.

Investment into the joint venture can be made either in the form of common stock or preferred stock, or debt. Foreign investors are generally allowed to invest in common stock or preferred stock, and debt convertible into common stock. While return on debt by way of interest can be claimed as a tax-deductible expenditure by the Indian entity, any return by way of dividends payable to common or preferred stock holders would not be allowed as a tax-deductible expense. Note that conversion of compulsorily convertible preference shares and compulsorily convertible debentures into equity shares have been specifically exempted from tax. As per the provisions of the IT Act, if shares are received for a consideration lower than their fair market value (computed in accordance with prescribed method), then the difference between the fair market value of the security received by the shareholder

and price paid for the same could be chargeable to tax in the hands of the recipient under the heading ‘income from other sources’.

Further, if the transfer of unlisted securities is made at a value less than their fair market value, then the fair market value (computed in accordance with the prescribed method) of such securities may be deemed to be the full value of sale consideration and the transferor may accordingly be liable to pay capital gains tax as per the provisions of the IT Act.

Further, certain payments to residents and all payments to non-residents that are chargeable to income tax in India are subject to withholding tax obligations. Failure to withhold such tax may result in interest, penalty and fines as prescribed under the IT Act.

Sale or purchase of shares of the joint venture entities or infusion of capital into the joint venture entity would, however, be outside the ambit of goods and services tax (GST) legislation in India, as the same would amount to transfer of securities or money, as the case may be.

Foreign exchange regulations also restrict (or provide detailed procedures for) contribution of assets to the joint venture entity depending on the nature of entity, type of asset and the resident status of the entity or person contributing the asset. The contribution of assets classifiable as supply of goods or the supply of services to a joint venture entity by joint venture partners may be eligible to tax under the GST legislation in India. These restrictions and taxability of such transactions have to be analyzed case by case.

Points to note Pre-incorporation for Joint Venture Companies

A Joint Venture is different from a company for the reason that a Joint Venture unlike a company is formed for a specific purpose or specific term, depending on the objective of such venture. Once the purpose or the term is complete the entity so formed under the Joint Venture agreement may come to an end. Joint Venture unlike a company is limited to a specific purpose or term, clearly defined by the parties. The following points should be kept in mind pre-incorporation of joint venture capital company-

- The separation of roles of the chairperson and the managing director or chief executive officer;

- A requirement of 50% of the total directors to be independent, which should also include at least one independent female director;

- An increase in the number of board and audit committee meetings;

- The provision of a transparent framework for regulating information rights of promoters with relation to significant shareholding and access to unpublished price-sensitive information; and

- Half- yearly disclosures for the related party transactions (RPTs).

- It was noted that joint venture agreements have several clauses pertaining to voting rights, additional quorum requirements, and arbitration provisions ousting statutory remedies, pre-emption rights or restrictions on transfer of shares.

- There should be an appropriate exception to the doctrine of ultra vires under Section 9 of the Companies Act and the parties should have “party autonomy of contract” in their joint venture documentation.

- There are also issues relating to Intellectual Property Rights and Confidentiality, which can lead to differences between the parties to the Joint Venture. Parties may not agree on issues of sharing of information and technology or control and management of the Joint Venture. Therefore, parties must discuss and negotiate the terms fully before entering into any Joint Venture to avoid conflicts of interests.

- A joint venture may have a 50-50 ownership split, or another split like 60-40 or 70-30. The majority corporate owner or investor usually has more control in decisions and earns a great share of the partnership earnings.

- Compliance requirement varies depending upon the residency of the transferor and transferee of the shares:

| Transferor | Transferee | Compliance, if any |

| India Resident | India Resident | None, record of transfer on share certificate |

| India Resident | Non-Resident | Filing of Form FC-TRS with the RBI |

| Non-Resident | India Resident | Reporting requirements with the authorized dealer, subject to the restriction that the Indian Resident should not have any previous tie-up or venture in the same field |

| Non-Resident | Non-Resident | None, intimation to RBI recommended |

Documentation for Joint Venture Companies

Depending upon the nature of the JV structure, definitive agreements would be drafted.

Registration of Venture Capital Funds

A venture capital fund is a pooled investment scheme that primarily invests the financial capital of third-party investors in enterprises that are too risky for the standard capital markets or bank loans. Venture capital can also include managerial and technical expertise. Most venture capital comes from a group of wealthy investors, investment banks and other financial institutions that pool such investments or partnerships.

The venture capital fund regulations by the Securities and Exchange Board of India are a comprehensive set of laws to be followed by the venture capital funds in India. From the registration of venture capital funds to the action to be taken in case of default, the regulation has been divided in VI chapters. Venture Capital Fund (VCF) is a form of fund established in the form of a trust or a company including a body corporate registered with SEBI that provides capital to early-stage or high-growth companies (start-ups). While VCF offers high level of risk associated with the investments, returns offered are also exponential in nature.

A company or trust (which functioned as a venture capital fund before the commencement of these regulations) shall cease to function as a venture capital fund if it does not apply to SEBI for registration within 3 months from the commencement of the regulations.

There are certain conditions which must be fulfilled before the certificate of registration is granted by SEBI:

- In case of a company, the MOA of the company shall have the business of venture capital fund as its main object, and invitation to public shall be expressly barred by the MOA and AOA, in addition to this, any officer of the company shall be involved in any litigation connected to the security market or should not have been convicted of an economic offence.

- In case of a trust, the trust is in form of a deed and has been duly registered under the Indian registration act. Carrying the business of venture capital fund is its primary objective. Any trustee of the trust is not involved in a litigation connected to security market and has not been convicted of any economic offence.

- In case of a body corporate, it should be formed under the laws of central or state legislature and it is permitted to venture in the field of venture capital funds.

The application for registration shall be complete in all respect. If SEBI discovers anything in the application that renders it incomplete, it shall give the applicant a time of thirty days to remove the loophole, failing which the application can be rejected by the board.

Steps to Register Venture Capital Fund in India

Check the Eligibility Criteria before granting the certificate to the applicant by SEBI

- Check whether the company registration document i.e. MOA, Trust Deed or Partnership Deed permits to carry the activity of ‘Venture Capital Fund’ and compliance are followed properly

- Check whether the Applicant/Sponsor/Manager or Key Investment Team of the Manager of the Fund have adequate experience of not less than five years and are fit and proper persons based on the criteria specified in Schedule II of SEBI Regulations 2008

Apply to SEBI in Form A with all the necessary documents

- As provided in the SEBI (Alternative Investment Funds) Regulations, 2012, attach a covering letter with Current status of registration with SEBI as VCF, history of undertaking activities of Venture Capital prior to this application and also state whether applying for registration of a new fund or not

- Form A should be appropriately filled, numbered, duly signed and stamped along with an application fees of ₹25,000/- by way of bank draft in favour

- The applicant shall also make an online application in terms of the guidelines as prescribed by SEBI from time to time.

Collect Certificate of Registration from SEBI

- On receipt of registration/ re-registration fees, SEBI will grant the applicant the certificate of registration as an ‘Alternative Investment Fund’ or ‘Venture Capital Fund’ .

Check Application Status

- If applicant fulfils the requirements as specified in the Regulations, SEBI shall approve the application and inform the applicant

- Reply from SEBI is generally received within 21 days. Make sure requirements are complied with without delay”

Pay Registration Fee

- On receipt of approval from SEBI, applicant must pay registration fee of ₹5,00,000/- (If applicant is not registered with SEBI as a Venture Capital Fund) / Re-registration fees of ₹1,00,000/- (If applicant is registered with SEBI as a Venture Capital Fund) by way of bank draft in favour of “The Securities and Exchange Board of India”, payable at Mumbai.

Follow Compliance Post the Registration

- Comply with SEBI’s reporting requirements from time to time

- Check SEBI website regularly for updation/circulars/guidelines issued with respect to Venture capital fund activity

- Intimate SEBI in any material change in the details already furnished to SEBI within a reasonable period of time

Conditions and Restrictions on Investments

The regulation has applied a lot of condition and restriction to the amount of investment to be made in and by the venture capital fund in India.

An investment in the venture capital fund can be made by any person whether Indian, Foreigner or NRI, but no investment which is less than ₹ 5,00,000/- can be allowed in the venture capital fund. This however does not apply to investment made by the employees, directors or the principal officers of the company or by the trustee where the venture capital fund is a trust.

The investment strategy at the time of registration shall be disclosed by the venture capital fund. The venture capital fund shall also disclose the duration of its life cycle. Not more than 25% of the fund shall be invested in a single venture capital undertaking .Investment to be made in the following manner:

- At least 66.67% of the fund to be invested shall be invested in unlisted equity shares or other instruments linked to equity shares of the venture capital undertaking.

- Not more than 33.33% of the investible fund shall be invested by the way of IPO of a venture capital undertaking whose shares are proposed to be listed, the debt instrument of the venture capital undertaking in which the venture capital fund has already invested, preferential allotment of equity shares of a listed company, equity shares or equity linked instrument of a financially weak company and (Special Purpose Vehicles) SPV's which have been created by the venture capital fund

No venture capital fund shall get its units listed on any recognized stock exchange till the expiry of three years from the date when they were issued to the investors by the venture capital fund. The venture capital funds shall also not invite any member of the public by way of advertisement to subscribe to its units. The venture capital fund may receive investments only through private placements of its units.

Placement Memorandum or Subscription Agreement

Every venture capital fund shall issue a placement memorandum which contains all the terms and conditions, relating to the scheme, through which money is proposed to be raised from the investors. The venture capital fund may also enter into a subscription agreement with the investors which would specify the terms and conditions of the scheme through which money is proposed to be raised. The venture capital fund shall submit a copy of such placement memorandum or subscription agreement with SEBI along with the report of the money actually raised through such agreement or memorandum.

The placement memorandum or the subscription agreement shall have the following essential:

It shall contain the details of the trustee and the trust as well as the details of the directors and the principal officers of the venture capital fund. It shall also state the minimum amount of money to be raised to start the venture capital fund and the minimum share to be invested in every scheme of the venture capital funds. Tax implications which would be applied to the investors shall also be stated. The manner of subscription to the units of the fund, the period of maturity of the fund if any and the manner in which the fund would be wound up shall also be stated.

Every venture capital fund shall maintain a book of record for a period of eight years which would generate the true picture of the venture capital fund. SEBI at any time can call for information regarding the working of the venture capital fund; the information shall be submitted to SEBI in the specified time period.

Investigation

SEBI on receiving a complaint from the investors or appoint one or more person as investigating officer, who would undertake investigation in relation to the maintenance of the account books of the venture capital fund, compliance of the regulation and the affairs of venture capital funds. A notice of at least ten days shall be given before the investigation is carried on though if SEBI deems it to be in interest of the investors it may not serve a notice at all. It shall be the duty of every officer of the venture capital fund to cooperate with the investigation officers, they shall be provided with all the documents, books etc. which are in the custody of the officers of the venture capital fund. The investigation officer shall also be furnished with any statement he demands for. After the completion of investigation the investigation officer shall submit his report to SEBI. The board after considering the investigation and giving the venture capital fund to be heard may direct the venture capital fund not to launch new schemes or prohibiting the concerned person from disposing off the property of the venture capital fund or to refund to any investor any amount of money or asset.

Action In Case of Default

Any venture capital fund that fails to act in accordance with the regulations, or fails to furnish reports of the affairs of the venture capital fund to SEBI or furnishes report that is not true, does not cooperate in any enquiry instituted by SEBI or fails to act on the complaints made by the investors or does not give a satisfactory reply in this regard to SEBI, shall be dealt with in manner provided in SEBI (procedures for holding enquiry by enquiry officers and imposing penalty) regulations, 2002

Conclusion

Choosing a good home partner is the most important tool to the success of any joint venture.

Once an associate is selected, normally a memorandum of understanding (MoU) or a letter of intent is signed by the parties – stressing the foundation of the future joint venture agreement.

An MoU and a joint venture agreement must be marked after consulting a chartered accountant firm well versed in the Foreign Exchange Management Act; Indian Income-tax Act, 1961; the Companies Act, 2013; international laws and applicable Indian rules, regulations, and procedures.

Terms and conditions should be properly assessed before signing the contract. Negotiations need an understanding of the cultural and legal background of all the involved parties. The JV union should obtain all the required governmental approvals and licenses within a specified period.

Foreign companies no longer require a no-objection certificate (NOC) from the Indian associate for investing in the sector where the joint venture operates.

Overseas firms in existing joint ventures can function independently in the same business segment. Previously, they needed prior approval from their Indian partners.

Companies in India are grouped into two categories – companies owned or controlled by foreign investors, and companies owned and controlled by Indian residents.

This is an understanding whereby an independent legal entity is created in accordance with the agreement of two or more parties.

The associated parties undertake to provide money or other resources as their contribution to the capital or assets of the corporate entity.

This structure is ideal for long-term, broad-based joint ventures, and include joint venture companies and joint venture limited liability partnerships (LLPs).

Frequently Asked Questions

- 1. Is joint venture a legal entity in India?

-

Yes, a 'joint venture' is recognized as a distinct legal concept in India. As per the provisions of the Companies Act 2013, a joint venture is defined as a joint arrangement, whereby the parties that have joint control of the arrangement have the rights to its net assets.

- 2. Do joint ventures need to be registered?

-

Joint venture is not required to file formal paperwork or documentation of status with state or federal governments. Instead, development of a joint venture is contractual and involves one business entity entering into a contract with another entity.

- 3. How do I register a joint venture?

-

For registration as Joint Venture Company in India, Foreign Company will have to become shareholder in new Indian company and then such joint venture company will be considered as Indian domestic company.

- 4. Is joint venture private company?

-

A joint venture is an operating company owned by a government entity and a private company (or multiple companies including foreign companies if permitted by law), or a consortium of private companies

- 5. How many minimum members are required in joint venture?

-

A private limited company must have at least two shareholders, while a public company should have at least seven shareholders. Under the Companies Act, 2013, it is mandatory that at least one director of every company is a resident of India.

- 6. Can a minor be a party of joint venture?

-

The parties involved in the joint venture are known as co-venturers while the members of the partnership are called partners. A minor cannot become a party to Joint Venture. Conversely, a minor can become a partner to the benefits of the partnership firm.

- 7. Who is liable in a joint venture?

-

In general, the members of a joint venture that is set up as a separate corporation or limited liability company (LLC) will only be liable to the extent of their investment in the corporation's stock or their interest in the LLC.

- 8. Who is liable in a joint venture?

-

In general, the members of a joint venture that is set up as a separate corporation or limited liability company (LLC) will only be liable to the extent of their investment in the corporation's stock or their interest in the LLC.

- 9. Can you sue a joint venture?

-

Joint venture members can be sued individually and found liable for damages caused by a joint venture and it should be recalled that a joint venture is, above all, a partnership type entity with unlimited liability imposed upon its members.

- 10. Why do companies do joint ventures?

-

A joint venture affords each party access to the resources of the other participant(s) without having to spend excessive amounts of capital. Each company is able to maintain its own identity and can easily return to normal business operations once the joint venture is complete.

- 11. Can a joint venture open a bank account?

-

Partners in a joint venture must separate business funds from personal assets. Before establishing a bank account for a joint venture, the partners should check the rates and fees of at least three financial institutions, comparing monthly minimum requirements, debit- and credit-card policies and miscellaneous fees.

In addition, if the venture has a fictitious business name, it must be registered; present that certificate to the bank as well. Verify the identity of each partner who has the authority to use the joint venture's bank account.

- 12. Do Joint Ventures file tax returns?

-

The venture itself does not make a tax filing on any of the funds that flow through it. Like general partnerships, the Internal Revenue Service (IRS) does not consider joint ventures as a business structure and does not require a copy of the joint venture agreement or other proof of the venture's existence.

If you receive income from a joint venture, you must report it to the Internal Revenue Service on your personal return because joint ventures do not file their own returns. Only spouses can elect that the IRS treat their enterprise as a qualified joint venture instead of a partnership.

- 13. How do you manage a joint venture?

-

- Alignment of goals.

- Having a clear governance structure.

- Successful integration of both partners.

- Adaptability to changes.

- 14. What is the advantage and disadvantage of joint venture?

-

The Advantages and Disadvantages of Joint Venture:

Advantages of Joint Ventures Disadvantages of Joint Venture Profit at low cost Flexibility is restricted Flexible nature Assets and claims Start-up push Equal involvement is impossible Shared costs, expenses, benefits, and risk Rapport formation - 15. What is the difference between strategic alliance and joint venture?

-

A Strategic Alliance is an arrangement between two companies to undertake a mutually beneficial project, with each remaining independent. Joint Venture is a form of Strategic Alliance that is more complex and binding. In a Joint Venture, two businesses pool resources to create a separate business entity.

There are three types of strategic alliances: Joint Venture, Equity Strategic Alliance, and Non-equity Strategic Alliance.

- 16. With an incorporated joint venture, what controls exist in your jurisdiction in relation to nominee directors? How should a nominee director balance the potentially conflicting interests of the joint venture company and the appointing shareholder?

-

A ‘nominee director’ has been defined under section 149 of the Companies Act to mean a director nominated by any financial institution in pursuance of the provisions of any law or agreement, or appointed by any government or person, to represent its interests. Practically, a nominee director is expected to monitor the operations of the company, but at the same time is burdened with many fiduciary and statutory duties and obligations, the breach of which can attract penal provisions under various pieces of legislation. When facing a situation with a conflict of interests, where the interests of shareholders are in contrast with other stakeholders such as the employees or the joint venture company itself, the Companies Act has, without prioritizing one over the other, provided recognition to both shareholders and stakeholders. In reality, it implies that the directors are liable to make difficult choices in deciding the hierarchy of conflicting interests without necessarily being favorable to the nominator, the underlying principle being that they are to act in the interests of the company at all times

According to Section 166 of the Companies Act, which mandates a director must act in the best interests of the company and in good faith to promote the company’s objectives. A director has to maintain a balance between the interests of the nominator and the wider interests of the joint venture company and other stakeholders, and ensure that all duties are discharged with due diligence and reasonable care following due process and exercising of his or her independent judgment. If the joint venture company is proven to have committed any contravention of law, a nominee director will not be exempted and will be held equally liable as an ‘officer in default’. A director has to be diligent with RPTs and abstain from self-dealing and ensure that he or she complies with the requirements prescribed under section 184 of the Companies Act and LODR Regulations (applicable if the joint venture entity is a listed entity) with respect to the disclosure of interest by the directors, primarily in relation to any contract or arrangement by a company, where any such non-compliance may be penalized, including by imprisonment.

- 17. Are there any restrictions on the contribution of assets to a joint venture entity?

-

There are no restrictions on contributions of assets to a joint venture entity. However, depending on the type of the joint venture entity, there may be certain compliance requirements under extant laws for contribution of such assets. For example, if assets are contributed by a joint venture partner in a limited liability company in lieu of shares, the Companies Act lays down certain procedures for issue of shares for ‘consideration other than cash’. Further, the Companies Act stipulates rules in relation to valuation and treatment of the non-cash consideration.

Further, extant foreign exchange regulations also restrict (or provide detailed procedures for) contribution of assets to the joint venture entity depending on the nature of entity, type of asset and the resident status of the entity or person contributing the asset. The contribution of assets classifiable as supply of goods or the supply of services to a joint venture entity by joint venture partners may be eligible to tax under the GST legislation in India. These restrictions and taxability of such transactions have to be analyzed case by case.

- 18. What is the interaction between the constitution of the joint venture entity and the agreement between the joint venture parties?

-

Unless the joint venture company is party to the contractual arrangement between the joint venture parties, the provisions of such arrangement may not be directly enforceable against it. Therefore, the articles of association (AoA) of the joint venture company must either incorporate the provisions of the joint venture agreement or be silent on the same, thereby not hosting any contradictory or restrictive provision in relation to rights specified in the joint venture agreement in order for the joint venture company to give effect to these provisions. However, in the case of any conflict or inconsistency between the provisions of the AoA and the joint venture agreement (to the extent the joint venture company is affected), the former shall take precedence over the latter. Some understandings, such as pooling arrangements and voting agreements between the joint venture partners may affect the governance of the joint venture company but do not directly involve the joint venture company by itself, owing to privacy of contract. It has also been observed by the courts in India that the consensual agreements between particular shareholders relating to their specific shares can be enforced against the parties like any other agreement. However, in the case of an aggrieved shareholder whose rights in relation to the joint venture company cannot be enforced, he or she can approach the courts to seek liquidated damages, as stipulated under the agreement or liquidated damages for breach of contract as per the Indian Contract Act 1872.

There is no requirement to register a joint venture agreement.

- 19. How may the joint venture parties interact with the joint venture entity? Are there any restrictions?

-

The joint venture agreement and the AoA provide rights to the joint venture parties to nominate directors on the board of the joint venture company, thus creating an important channel for the joint venture parties to interact with the joint venture entity. A critical element to be factored in relation to transactions between the joint venture parties and the joint venture entity is the regulation of specified types of transactions between related parties under the Companies Act and the SEBI (Listing Obligations and Disclosure Requirements) Regulations 2015 (LODR Regulations) for listed companies (the related party transactions (RPTs) regime). ‘Related party’ has been fairly broadly defined under the Companies Act and LODR Regulations and includes any person on whose advice, directions or instructions a director or manager is accustomed to act (except in the case of professional advice).

As per the Companies Act, all transactions by the joint venture company with related parties have to be approved by the board and, under certain circumstances, by the shareholders of the joint venture company, except if transactions are in the ordinary course of business of the company and made at arm’s length. Further, the related shareholder may not vote on such a transaction. However, the aforesaid proviso will not apply to a joint venture company in which 90 per cent or more members are relatives of the promoters or are related parties. Additionally, the requirement for passing a shareholder resolution will be obviated in the case of transactions entered into between the holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at a general meeting for approval. An ‘arm’s-length’ transaction refers to a transaction between two related parties that is conducted as if they were unrelated, so that there is no conflict of interest and is compliant with the TP Regulations.

- 20. What are the tax considerations on termination of the joint venture?

-

Joint venture partners may exit from the joint venture by transferring the securities held by them in the joint venture company, whereby the proceeds thereof are subject to capital-gains tax, payable by the joint venture partners at the following rates.

Nature of joint venture entity Nature of gain Period of holding Tax rate* non-resident partner Tax rate* resident partner Company: disposal of unlisted securities Long-term capital gains > 2 years 10% 20% Short-term capital gains < 2 years 40% 30% LLP: disposal of interest in joint venture Long-term capital gains > 3 years 20% 20% Short-term capital gains < 3 years 40% 30% Exclusive of applicable surcharge and cess. However, for non-resident partners, the tax liability in India is subject to the provisions of the DTAA signed by India with the country of which the joint venture partner is a resident.

The joint venture company may also distribute its assets or surplus cash to the joint venture partners through dividends, and such distribution may be deemed as dividends under the IT Act to the extent that there are accumulated profits attracting DDT. For a joint venture LLP, any capital asset distributed by the LLP to its partners would be deemed to be the sale consideration and capital gains arising thereof will be taxable according to the fair market value of the assets as on the date of the distribution.

In terms of the GST legislation, disposal of business assets, where input tax credit has been availed on such assets, shall be eligible to GST in India, even when such disposal is made without any consideration. Additionally, where a person ceases to be a taxable person and his or her registration is cancelled, such person is liable to reverse the amount of input tax credit availed on inputs held in stock or inputs contained in semi-finished or finished goods lying in stock, capital goods and plant and machinery or pay output tax on such goods, whichever is higher. Accordingly, where the joint venture ceases to be a taxable person and his or her GST registration is cancelled, he or she would either be liable to pay GST on the disposal of his or her business assets or reverse applicable input tax credit, whichever is higher, in terms of the GST legislation.