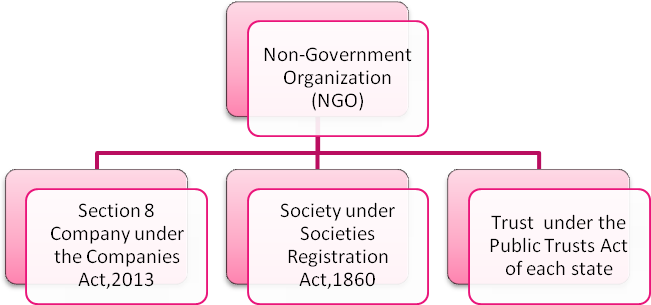

Registration of Non-Government Organization

An NGO is a non-government organization with a charitable objective, for the betterment of the society in general. It can be started as a Trust, a Society or a Non-Profit Company [Section 8 Company], depending on the activity you wish to undertake. Other names for such not-for-profit organizations are "Sangathan", "Sangh", "Sangam". Income tax exemption is available for all non-profit NGOs. These are sometimes confused with non-profitable companies, which refers to a regular business is not making a profit. NGO may be defined as association having a definite cultural, educational, economical, religious or social association organization. They are not owned by any one and cannot distribute profits as such. Whatever profits they may earn from economic activities are reinvested or spent on appropriate non-profit activities. The typical sources of revenue or non-governmental organizations are donations, membership fees, interest and dividends on investments. An NGO is a non-profit citizen group which is organized on a local, national or on an international level to serve as a social welfare for the people in need. The unique features of NGO include:-

- The voluntary association of person having interest in it.

- It is generally free from government interference as it has its own rules & regulations being followed by its members.

- they work parallel to the Government

Task-oriented and driven by people with a common interest, NGOs do a variety of service and humanitarian functions, bring resident issues to Governments, advocate and display policies and encourage political participation through arrangement of info. Some are arranged around particular concerns such as human rights, environment or wellness. NGO registration is indeed a blessing for the society. They offer analysis and experience, function as early caution mechanisms and assist keep track of and implement international agreements. Their relationship with workplaces and agencies of the United Nations system varies depending on their goals, their venue and the mandate of a specific institution.

NGO’s are set up to fill the gaps between the Government & the society. It plays a critical part in developing society by providing help in humanitarian, educational, health care, public policy, social, human rights, environmental and other areas in need as India has a huge problem regarding the above issues. Since their function is in the non-profit scheme due to which they face problems like lack of qualities in terms of skills and opportunities regarding the employment.

Each law defines the formation of a different type of organization, namely – Trust Registration, Society Registration, and Section 8 Company Registration. Choosing the kind of registration procedure for the charitable firm is crucial. Every non government organization in India requires a legal entity such as trust deed/ Memorandum of Understanding(MOU’s)/Articles of Association(AoA’s) that consists the address and name of the non government organization, goals, details of legal main managing committee members, human resource and staffing or by any kind of staffing agencies, administrative laws, rules and regulations and procedures.

Classification of NGOs in India on the basis of levels

Benefits of registering as an NGO in India

A registered NGO gains the legal status and becomes accountable for the funds received. For instance, when an individual donates funds to a charitable trust, it is received under the name of the organization and used for the trust’s activities. In an unregistered firm, the assets can be received under anyone’s name and may be used for their own profit.

All the companies need a minimum share capital to function independently. This isn’t the case with NGOs since they can be directly funded with the donations made to them. The subscriptions can also help to support the proceedings undertaken by the company. This means that NGOs do not need a higher share of capital to function independently.

An organization that is registered as an NGO reinforces the ethical, social and legal norms of our society. They can function without making their limited liability status public which is a significant benefit for the company in terms of the capital they need to make public.

Improved recognition Better legal standing. Higher credibility amongst donors, Government departments and other stakeholders. Relaxation from a number of companies act regulations

The registration of an NGO is necessary to seek tax exemption from the Income Tax Authority. Companies registered as NGOs under Income Tax Return Act of 1961 are not restricted to transfer their ownership or claims of the interests earned. However, other companies cannot move their ownership with such ease, which benefits NGO registered companies.All companies registered as NGOs under Income Tax Act 2013 are exempted of stamp duty, which accounts for more tax-saving methods for the company. All the taxes saved through stamp duty are then invested in the promotion of the motto taken up by the company. Exemption of stamp duty protects funds for the company, which makes the functioning of the company smoother increasing the productivity of the company.

Right To Acquire Assets

When your organization is officially registered, it then becomes permitted to acquire land, own fixed assets and/or acquire liabilities under its common seal. It is against the law for an unregistered organization to buy, hold/sell land anywhere.

Transfer Of Ownership

Under the Income Tax Act 1961 NGOs registered under the Companies Act, 2013 are not restricted to transfer their ownership or claims of the interests earned.

Tax saving

Registering your company as an NGO under the Companies Act, 2013 and avail several taxation benefits for the directors of the company. NGOs are exempt from several taxes, and it helps the company save taxes and invest the saved money in further projects.

Corporate Entity

As a corporate body, your organization’s transactions and engagements with the community will improve. The NGO can also sue to enforce its legal rights or be sued via its registered trustees.

Exemption On Stamp Duty

Under Income Tax Act, Section 8 companies as NGOs are exempted from stamp duty, which results in more tax-saving methods for the company. All the taxes saved through stamp duty are then invested in the promotion of the objectives taken up by the company. Also, it helps in protecting funds for the company, which as a result helps in smoother functioning of the company and increasing the productivity of the company.

Structured Financial Plan

Having an NGO can bear a tax-free mechanism for actions you are carrying-on under the registered NGO. NGOs are considered not-for-profit and tax exempted. You can develop a structured financial plan that allows the organization to do business devoid of tax liabilities.

Stability Of Entity

The registration of your organization can suggest that there is effective and responsible leadership in place. The public will perceive same as being stable than an unregistered organization. Political parties, government, donor agencies, financial institutions, charity organizations and other NGOs will want to partner with a registered body to further common objectives.

Perpetual Succession

This means an NGO got an unlimited lifetime and will carry on existing even if the founder/trustees die or leave the NGO. The organization’s continuation will only cease if it is formally wound up by the Order of Court of India. Along with other benefits, this may allow perpetual succession.

Name Preservation

Once your organization is registered, no one can use the same name or name similar to it throughout in India. This has the benefit of protecting your corporate image and name from unauthorized use.

Admission To Credit

Registering an NGO can afford access to credit from lenders and financial institutions. You can use a loan facility to promote the organization’s activities, finance a mortgage, acquire land or fixed assets. Banks will want to see proof of registration with condition precedent to giving a loan.

Opening Bank Account

Opening a corporate account with a bank for the NGO may signal the fact that is transparent. Some private persons, government, donor agencies and other NGOs will not be comfortable writing you a cheque for your organization in your personal name. A bank account for the NGO would signal its corporate existence and its readiness to receive donations. You need to provide proof that your organization is registered to be able to open an account with a bank.The basic requirement for running an NGO is to have a bank account under its name. In order to open an account, it is mandatory to be registered as a Trust, Society or Section 8 Company.

Steps that can be taken to raise funds for NGO

Registration of Non-Government Organization (NGO) as business entity

Read More...Registration of Non-Government Organization (NGO) in DARPAN-NITI Aayog Portal

Read More...Registration of Non-Government Organization (NGO) to get tax exemption u/s 12AB/80G

Read More...other special registration required by NGO

Read More...Mandatory Registration with MCA for Getting CSR Funding

Read More...Registration of NGO in India

Trust

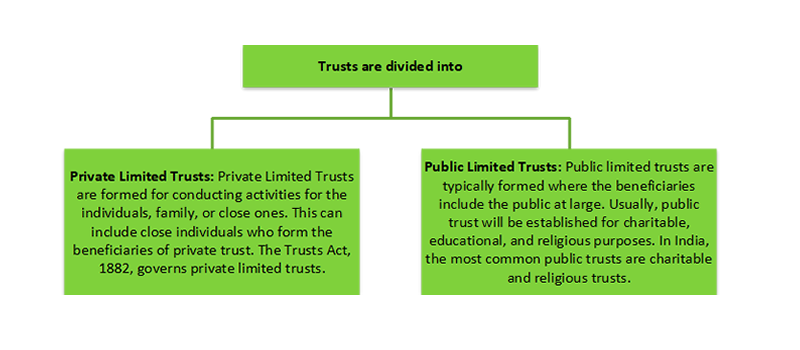

One of the ways in which an NGO can be registered is Trust or more commonly called Charitable trust. Trust is a legal entity created by the “trustor” or “settlor” who transfers the assets to the second party or “trustee” for the benefit of the third party or “beneficiary”. Trusts are formed to help and support the deprived sections of the society. Any group of individuals can register a trust and in India as such there are no specific laws to govern the public trust, however, some states like Maharashtra and Tamil Nadu have their own Public Trust Act

Societies

A society is an entity that can be created by a group of individuals united in their cause for promoting science, arts, literature, social welfare and useful information. In addition, societies work for creating military orphan funds, maintaining public museum and libraries.

Societies are governed by the Societies Registration Act, 1860. They must be registered with the respective state Registrar of Societies to be eligible for tax exemption.

Section 8 Companies

A Section 8 company is similar to a trust and society. The objectives of a Section 8 Companies are to promote arts, science, commerce, sports, social welfare, religion, charity and environmental protection. They are registered under the Companies Act, 2013 for charitable purpose. They have better credibility among government bodies, donors and other stakeholders.

What to register - Trust, Society Or Company?

| Trust | Society | Sec - 8 Company | |

|---|---|---|---|

| Meaning | It is considered to be the oldest form of charitable organizations. It is, in essence, an arrangement between parties whereby one party holds ownership over property on behalf of another person | It is formed when a collection of people come together for initiating a common purpose- literary, scientific or charitable purpose. But it is not limited to charitable purposes but may extend to multiple other fields. | It is a company established with the purpose has in its objects the promotion of commerce, art, science, sports, education, research, social welfare, religion, charity, protection of environment or any such other object and whereby they apply any profits into furthering the objective. |

| Governed by | Trust Act of each state. A trust is established under and governed by the Indian Trust Act, 1882 for private trusts. General law is applied for public trusts except in a few states such as Gujarat and Maharashtra, which have their own state laws | Societies Registration Act (State Law),1860 | Companies Act, 2013 |

| Registered as | NGO/NPO | NGO/NPO | NGO/NPO. But they enjoy all the privileges of a limited company without the need for them needing to add Pvt. Ltd. to the name. |

| Registration Authority | Deputy Registrar of the state | Registrar or Deputy Registrar of the particular state in which it is to be registered. | Registrar of Companies (ROC) or Regional Director |

| Members: | Minimum of 3 members and a maximum of 21 members | Minimum of 7 members and the maximum is unlimited | Minimum of 2 Directors/Shareholders |

| Jurisdiction: | Where the registered office of the Trust is situated. Before the Sub - Registrar or the District Registrar in the particular area or the Charity Commissioner. | Where the registered office of the Society is situated. Before the District Registrar in the particular area or the Charity Commissioner. | Online Registration |

| Document of constitution | Trust Deed | Memorandum of Association (MOA), By-Laws, Forms | MoA and AoA (Articles of Association) |

| Board: | Founder or Author of the Trust, Managing Trustees (Treasurer, Auditor, etc.) | Executive Committee (President, Secretary, Vice President, Treasurer), General Body (All members) | Directors |

| Legal right over the property | Held by the trustee | Held in the name of the society | Held in the name of the company |

| Transparency | Low | Low | High |

| Property Management: | The properties of the Trust will be managed by the Trustees; however, the properties cannot be sold by the Trustees without obtaining the permission from the court. | The property of the Society vests in the name of the Society and the same can be sold as per the terms mentioned in the By-laws of the society. (E.g.: Approval from the Executive Committee Member) | The property of the company vests in the name of the Company and the same can be sold as per the rules mentioned under the Companies Act, (E.g.: With the consent of the Board of Directors in the form of a resolution) |

| Revocation/ Dissolution or Winding Up | The trust is usually irrevocable in nature. For reasons like disqualification of trustees, the absence of trustees, mismanagement of the trust, the trust can be merged with another trust having a similar objective with the permission of the court. | Dissolution as per the By-laws of the society, upon dissolution and after settlement of all debts and liabilities, the funds and property of the society may not be distributed among the members of the society; rather, the remaining funds and property must be given or transferred to some other society, preferably one with similar objects. | Dissolution as per the By-laws of the society, upon dissolution and after settlement of all debts and liabilities, the funds and property of the society may not be distributed among the members of the society, rather, the remaining funds and property must be given or transferred to some other society, preferably one with similar objects. |

| Annual Compliance | There is no annual filing but the board of trustee must keep the books and accounts proper. There are no mandatory yearly compliance to be met by a trust | Societies must file annually, with the Registrar of Societies, a list of the names, addresses and occupations of their managing committee members. | There is a requirement of annual compliance by the filing of annual accounts and the return of company with the RoC.(Registrar of the Companies) |

| Cost factor | Low | Medium | High |

| Grants and subsidies from the government | Not much | Not much | Considerable (possible) |

| Preference in registration under FCRA | Low preference | Low preference | Preferred |

| Registration under The Income Tax Act, 1961 | Allowed | Allowed | Allowed |

| Legal right over the property | Held by the trustee | Held in the name of the society | Held in the name of the company |

| Registration period (approximately) | 15-20 days | 20-25 days | 30-45 days |

| Stamp duty | Dependent upon the state stamp duty Act a well as the total worth of the property involved in the matter. | None | None |

Note: Once the payment for the registration is done, it takes about 8 to 10 days for online registration to be completed under the Indian Trust Act – 1882, and about 8 to 10 days for drafting the MoA and By-laws of the Society and similarly for Section 8 Company but thereafter it takes about 2 months for the entire Company registration to be completed whereas it takes 21 to 30 days for the Society to be registered.

In case of trust, before the deed becomes valid throughout the country, the settler has to deliver a presentation at the registrar’s office. On the scheduled date for registration, the Author of the Trust shall be present in the Register Office for registration.

Things to know before starting an NGO in India

NGOs or non-governmental organizations are organizations that involve in a range of welfare activities that help upliftment of the underprivileged people and the society at large. NGOs usually function without depending on the government aids but at times work closely with the government for executing any specific projects.

Any person who has the desire to serve the society is free to join and work in an NGO. But starting one requires a little more than that. Registering an NGO needs funds, hard work, determination and passion to contribute to the society without expecting commercial gains. Some of the causes NGOs in India work for are:

1. Women empowerment

2. Protection of human rights

3. Environmental conservation

4. Wildlife conservation

5. Poverty

6. Children’s education

7. Prevention of sexual harassment

8. Care for the elderly

9. Healthcare and mental healthcare for the impoverished

10. Disease control and so on

Before deciding on NGO registration, here are some pointers to get through the process

What is the total cost of registering an NGO?

- The total cost of registering a section 8 company, including government and professional fees, would be around 14,999.

- The total cost of trust registration, including government and professional fees, would be around .

- The total cost of society registration, including government and professional fees, would be around .

Management Differences between Trust, Society and Section-8 Company

The varying kinds of NGOs that we have require a variety of administrative styles as their formation is different and hence the management styles for such organizations are different as well. A trust is managed by a group of trustees, a society is managed by a committee or a managing council and on the other a section-8 company is managed by a board of directors.

Jurisdiction and Law

The governance of trust is under the Registrar of Trusts. This means that all trust deeds need to be registered with this registrar of Trusts. On the other hand, societies are governed by a Registration of Societies hence all administrative and registration purposes work with regards to societies goes through the registrar of Societies. Section 8 Companies are corporate entities which come under the governance of the Registrar of Companies and have to comply with all ROC Compliances set out by the Ministry of Corporate Affairs such companies are subject to an audit every year.

Purposes

Trusts, Societies and Section 8 companies, under the NGO registration procedure are subject to stricter scrutiny from the authorizing/governing bodies. In general, even though the procedures are streamlined and filing of companies can be done via One Day Company Incorporation. Governing bodies need to be convinced of the authenticity of the intention/ purposes for which the organization has been set up. In accordance with the same, even though formalities might be done beforehand, it takes over 20 days to register a trust, 45 days to incorporate a society and up to 75 days to set up a section-8 company

Forms for NGO Registration

- Form INC 1: Name registration of NGO/ Name Approval

- Form INC 12: Form should be submitted to acquire license to run an NGO (is now merged in SPICe Form Part B)

- Form INC 13: Memorandum of Association;

- Form INC-14: Declaration from a practicing CA/CWA/CS/Advocate

- Form INC-15: Declaration by each subscriber to the Memorandum

- Form INC 7: Application for Incorporation of the NGO.

- FORM INC 22: Details of the Registered Address

- Form DIR 12: To appoint directors of the NGO

- Form DIR 2: Consent of Directors to act as directors for the company/NGO

- Form DIR 3: Application to ROC to get DIN

- Form INC 9: An affidavit from each director and subscriber or first director regarding no conviction or offence registered under Companies Act, 2013

Things to Do – Before Applying for NGO Registration

Decide on the cause

- The above-mentioned causes are just a few and there are a lot more NGOs working towards major developments in the country. For example, a group of social welfare activists in a north Indian state has been working on recycling old materials as a potential source for enhancing the infrastructure of the rural areas. They empower women to build bamboo ridges, irrigation canals, wells, drainage systems and more. Create a well-structured plan of the idea, goals, target group, etc.

Know the legalities of starting an NGO

- An NGO can be registered as a legal entity in three ways - Trust, Society, and Section 8 Company. All three differ in terms of registration, formation and management, and it is essential to decide on which entity suits the best.

- Trusts are formed when the settler of the property transfers any property and offers its benefits for the well-being of recipients or for the practice of public purposes. The main aim of the person who registers a trust in India is to make use of the assets of the trust to attain welfare of the public at large and promote a charitable cause called a Public Charitable trust. It takes nearly two days to one week to form a Trust.

- A Society possesses the Memorandum of Association (MoA) and Rules and Regulation or bylaws. It has the privilege to alter its MoA and increase or decrease its objectives from time to time. Any change made must be duly informed to the Registrar annually. A Society can be merged with another Society working for a similar cause. It takes one to two months to register a Society.

- Section 8 Company is the same as a Trust or Society but needs to be registered under the Central Government through the Registrar of Companies. The process is similar to that of forming a Public Limited and Private Limited. A Section 8 company that takes nearly three to six months has to mandatorily file the annual compliances.

Register NGO online

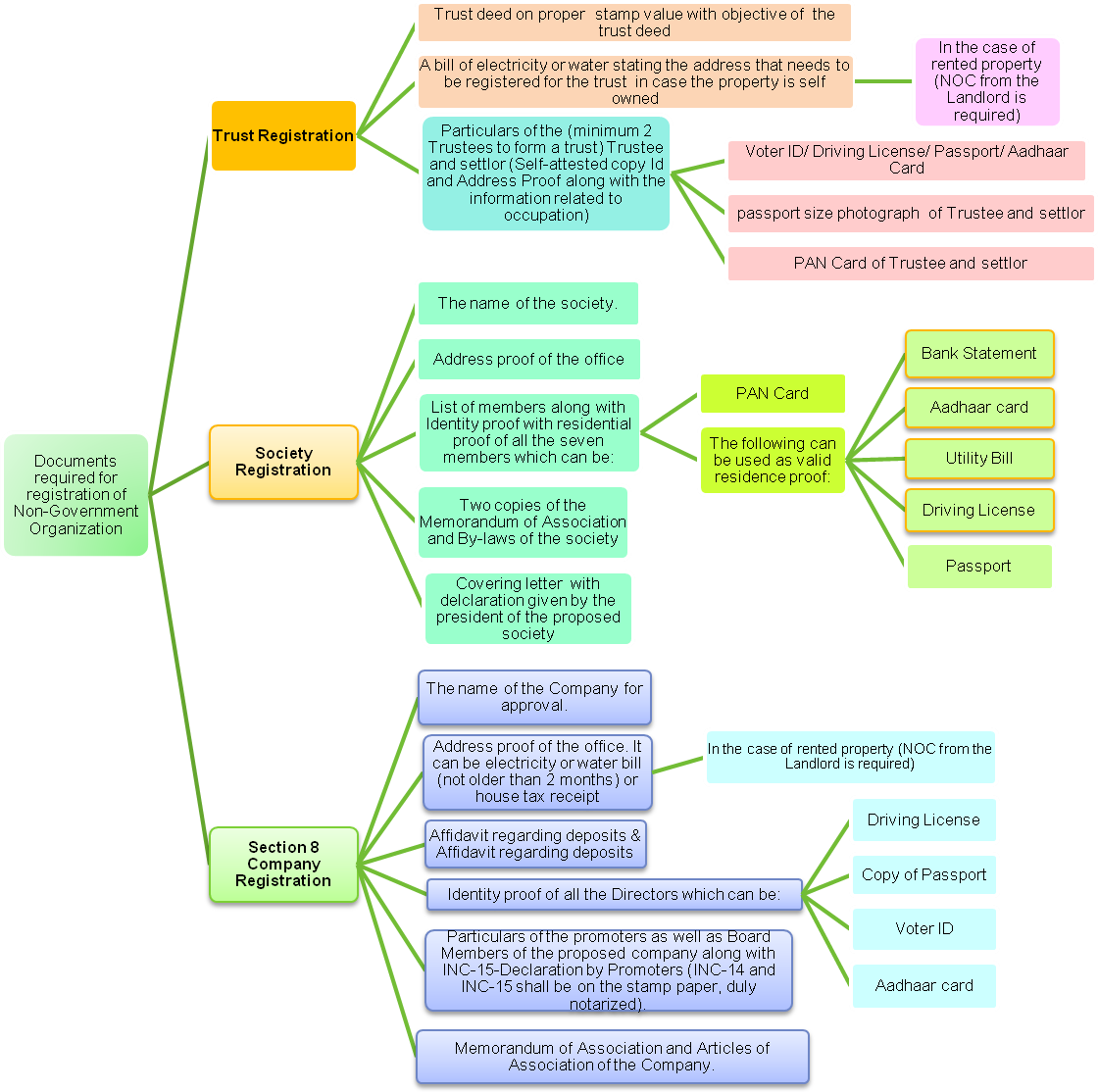

- For online registration of Trust, the essential documents required are water or electricity bill stating the address that needs to be registered, the ID proofs like Voter ID, driving license, passport, Aadhar card. It takes about 8 to 10 days for online registration to be completed with the help of professionals.

- To register a Society, two copies of MoA, copies of valid ID proofs like Voter ID, driving license, passport, Aadhar card. When done with the assistance of expert service providers, it takes about 8 to 10 days for drafting the MoA and By-laws of the Society. Thereafter it takes 21 to 30 days for the Society to be registered

- For registration of Section 8 Company, the Company’s name has to be approved, water or electricity bill stating the address of Section 8 that needs to be registered, ID proofs, and the Memorandum of Association and Articles of Association of the Company. It takes 8 to 10 days for drafting the MoA and AoA of the Society. Thereafter it takes about 2 months for the entire Company registration to be completed by seeking the help of professionals.

Make a financial assessment

- Once the type of entity has been decided and registered, estimate the initial amount required and start collecting the funds to operate. Try in different possible sources like fees, subscription charges, donations, government aids, sponsorships, foreign sources, etc.

Involve in networking

- Socializing as much as possible is a clear cut way to attract people’s attention towards your NGO. Participate in common meetings and social events online and offline to get connected with different types of professionals, including media agencies, corporate and government bodies. It is also best to look for prospective partnership opportunities that help build and support your organization.

Develop a website

- The Internet is a powerful medium to rightly communicate your cause and message to the audience. Hence, it is important to craft an intuitive website where people who want to volunteer, sponsor or partner can check the credibility of your NGO, the activities you do and all other details. It is also a wise idea to have social media handles that help make it more popular

Mandatory documents required for registration of an NGO

- A requesting letter for registration signed by founding members stating purpose of formation

- Certified copy of MoA [Memorandum of Association]/ Articles of association [AOA]

- Copy of the rules and regulations members will abide by

- Name, Address, Occupation & complete details of the members with signatures

- Minutes of meeting

- Declaration by President of Society

- Sworn affidavit from the President or Secretary, declaring the relationship between subscribers

- Address Proof of Registered office and No-Objection Certificate (NOC) from the landlord Address proof [if rented, then NOC from landlord]

- Donation receipts [if any received in the past]

The various tax deductions available under legal compliances of NGO

The various tax deductions available under legal compliances of NGO are as follows:

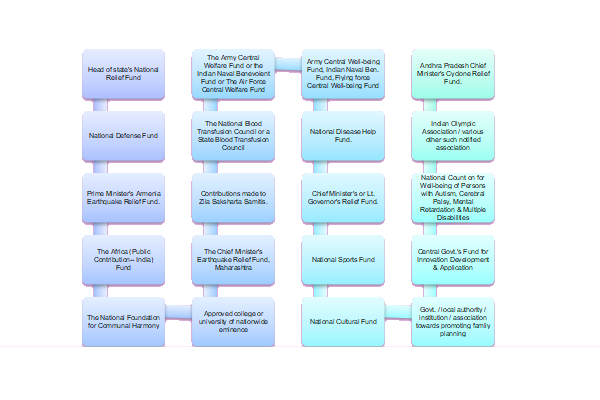

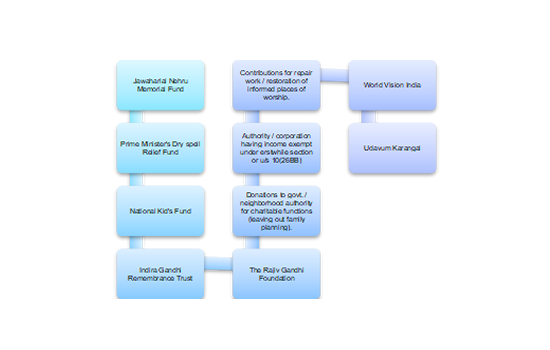

- Deductions under 80 G- Here donations are deductable. The section permits donors to deduct contributions for trusts, societies, and companies registered under section 8. They are entitled to the deduction of 100% if they are government funds or 50% if they are donations to non-government entities. It is a required condition for NGO to get registration under Section 80G- to be eligible for a deduction of 80G.

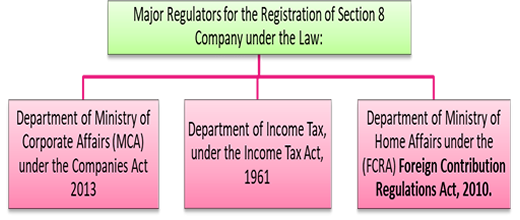

- Reporting foreign contributions- It is under Foreign Contribution (Regulation) Act, 2010. All non-profit organizations in India i.e. public charitable trusts, societies, and Section 8 companies, accepting any foreign contribution requires to secure registration. They have to register themselves with the Central government.

- Registration under section 12A- As per the Income Tax Act, 1961 such registration helps you get the exemption on the income of the Trust. Such registration is not compulsory. The registration is valid only for 5 years, and it has to be renewed after every 5 years.

- Custom Duty- A non-profit organization is involved in any relief work then there is an exemption. The exemption is 100 % on importing items such as food, medicine, clothing, and blankets. The other exemption which is available is on the research equipment and components intended for research institutes.

- FCRA Return- This return can be filed annually or quarterly to the Ministry of Home Affairs. The return has to be filed mandatorily, even if there is no foreign contribution received. The return has to be filed in the Form FC-4, which incorporates the charitable activities run by the organization. The return shall include the FCRA registration and the CA certificate.

Conclusion

It can be concluded that legal compliance of NGOs are mandatory. The NGO, such as registered as the Company has to follow the Section 8 Annual Compliance. Section 8 companies have to follow annual compliance. Legislations like the Income Tax Act play a significant role, as it provides deductions to the donors. The donations from foreign contributions are necessary to be registered, as foreign incomes/donations for Non-Governmental Organizations. Other registrations related to PAN and TAN are mandatory. Under the Income Tax Act, 1961 the definition of income states that ‘no income is exempt unless provided’, so donations are not always 100 % exempted.

NGO Legal Compliances

PAN Application

- It is categorically essential to mention the PAN number in the accompanying archives all the banking and money transactions for income-tax assesses, including NGOs under the current Income Tax Act.

Section 12A Registration under Income Tax Act

- The primary reason for getting this registration under section 12A is to get the benefit of exemption if all the rules and regulations laid down in this section are fulfilled from the Income Tax on the Income/revenue

- 12A registration applicant needs to submit the necessary documents/Legal Compliances for NGOs along with Form 10A

Section 80G Registration under Income Tax Act

- The registration under this section is not compulsory under its Legal Compliances for NGOs. However, to give the benefit of ‘50% or 100%’ exemption over the donations to the donors, it is needed to get the registration under section 80G of Income Tax Act. It is indirectly a huge benefit to NGOs to raise funds.

- 80G registration applicant needs to submit the necessary documents/Legal Compliances for NGOs along with Form 10G

FCRA Registration under Income Tax Act

- The newly registered entity shall apply for prior permission as per its Legal Compliances, if willing to receive a foreign contribution or foreign grants will get itself registered will FCRA Registration under Ministry of Home Affairs. It shall give the details relating to a foreign owner who is contributing the fund during applying for the sameThe fund received shall be employed only for the specified/identified purpose.

- The applicant must be operating for a minimum of 5 years and shall be a registered entity. An applicant entity must have spent at least 10 Lakhs in the previous three years for the entity submitted with last three years audited financial statement.

- Form FC-3A (Application for FCRA Registration) or Form FC-3B (Application for FCRA Prior permission) needs to filled along with all relevant documents

TAN under Income Tax Act

- NGO has to first apply for TAN for its Legal Compliances, if NGOs become liable to remove the tax from a source during the functioning of NGOs at any point of time.

- No specific document or proof of identity is needed for TAN registration. Form 49 B needs to be filled and submitted for obtaining TAN.

GST Registration

- NGO has to firstly apply for the GST registration as a Legal Compliance if the gross revenue from works crosses the basic exemption limit of GST and if the NGO is providing services like research activity or consultancy work etc.

- GST could be applicable for some of the services and goods supplied by a Charitable Trust or NGO unless exempt or NIL rated by the GST Council.

- In order to register under GST, one needs to ensure that the requisite form, i.e. GST REG-01 is filled with the correct information

Professional Tax Registration

- Professional Tax is an accountability of NGO to deposit to the Government and deduct from the pay of employee. Different states of India have different Legal Compliances & rules and regulations for Professional Tax under State Government.

- If NGO develops and the size of employees are more than the prescribed limit in this acts, in that case the Retirement benefits like Provident Fund, Gratuity, ESIC,etc. gets pertinent under its Legal Compliances.

Shops and Establishment License

- NGO must fetch a License under the Shops and Establishments Act, if an NGO employs any person in their office to carry out any work pertaining to the NGO according to the NGO laws in India.

CSR Funding

- The Form CSR-1 is termed as Form for “Registration of Entities for undertaking CSR Activities”. The Form mainly consists of two parts, first part is relating to the information about the entity who intends to undertake CSR activities. Second part of Form CSR-1 is certification by practicing professional. On successful submission of Form CSR-1, a unique CSR Registration Number shall be generated by system automatically to applying organization

- Form CSR-1 is a registration form for getting CSR funding by implementing agencies from the corporate sector.

Compliances that must be done to keep the NGO in active stage

Renewal of Society Registration within the given time Period

- In case of NGO, its registration is given for a specified time period generally 5 Years. Every NGO is required to renew the registration within specified time period. If registration is not renewed then it may create problem for the governing Body.

Mandatory conduct of Board Meeting and General Meeting

- As per bye laws of every NGO, they are bound to conduct Board meeting and general meeting on the regular intervals. If they default in complying with law requirement then governing body is liable for this and they may be penalized for such default.

Conduct of Financial Audit by CA on annual basis and Filing of ITR, audit Report Etc.

- Every NGO is required to get their books of accounts audited on annual basis from a Practicing Chartered Accountant and has to file NGO Income Tax return. If NGO is registered under Section -12A and 80 G of Income Tax Act, 1961 then they are under obligation to file their Tax audit report on or before the specified due date, otherwise their exemption may be withdrawn.

Submission of Audit Report and Annual Governing Body List with Registrar

- Every Society & Section-8 Company is under obligation to submit annual Audit Report and updated Governing body detail with the registrar. In case of delay, Society & Section-8 Company can be penalized which may lead to cancellation of registration also.

Maintaining of proper Records of Event Organized for Social Welfare Activities and expenditure incurred on these events

- NGO must maintain a proper record of all activities done during the year in the form of pictures etc. This step helps in getting Income Tax Benefits and raising more funds from Society and Government.

Penalties to be charged in case of Non-Compliance

In case of encounters of any non-compliance with the procedures, the Ministry of Corporate Affairs has the ability to impose certain penalties.

Penalties to be imposed are as follows:

- If it has been found that the organization is working falsely or in a way violating the object of the organization, then the Central Government may reject the permit allowed to the organization.

- The administration of the Institution will be culpable with fine, which will not be under 10 lakh and can be overextended out to 1 crore.

- Each official along with the chiefs of the organization who is in default will be culpable with detainment for a term which may bounce out to 25 lakh or it can be both.

- Every official in default must be at risk for activity under area 447 if in the event that it is discovered that the issues of the organization were directed falsely.

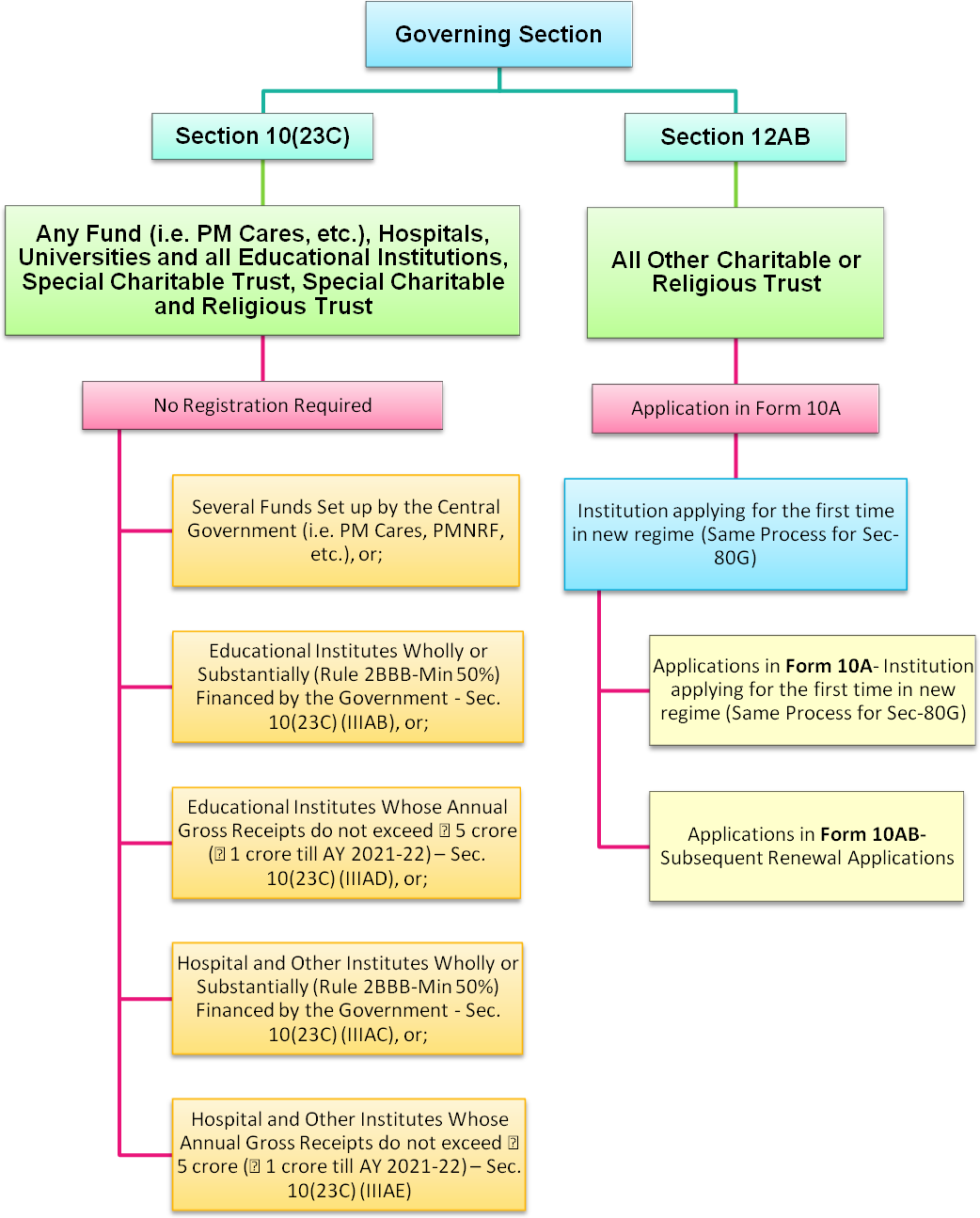

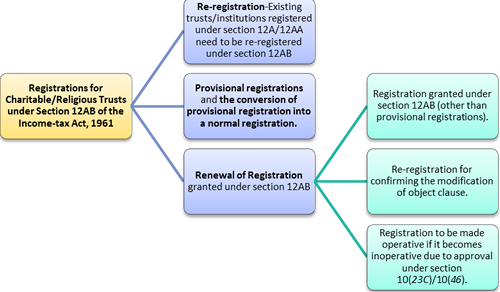

Section 12A and Section 80G for tax exemption- An Introduction

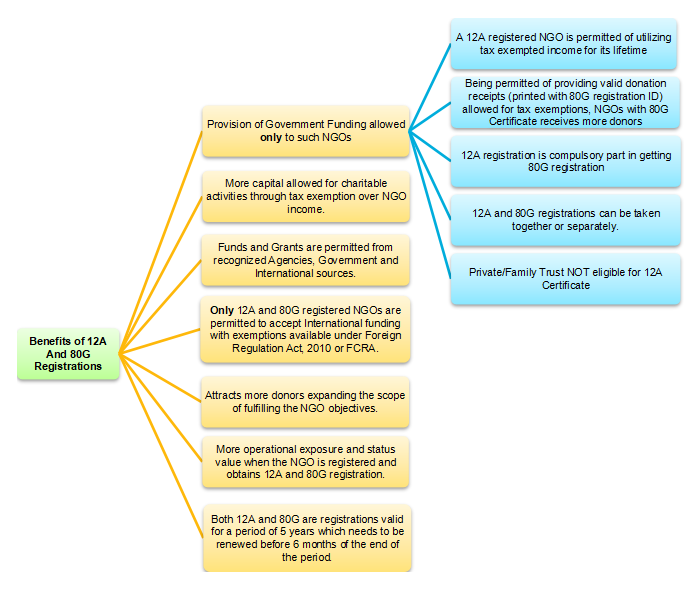

INGOs have multiple options to select the form of constitution, like trust, society and section 8 companies. In order to claim exemptions under section 11 & 12 of Income Tax Act, 1961, it is mandatory for all NGOs to get registration under section 12A of the act. “It is important to note here that notwithstanding the fact that trust, society and section 8 companies are registered as per their respective acts, the registration under section 12A is necessary to claim exemption under Income Tax Act.”

Earlier registration under 12A was given as one time registration and once the registration is granted it will hold good till cancellation. From 1st April 2021, all new registration will be given for 5 years only and organization has to apply for renewal after each 5 years.

An NGO can avail income tax exemption by getting itself registered and complying with certain other formalities, but such registration does not provide any benefit to the persons making donations. The Income Tax Act 1961 has certain provisions which offer tax benefits to the "donors". All NGO's should avail the advantage of these provisions to attract potential donors. Section 80G is one of such sections. If an NGO gets itself registered under section 80G, then the person or the organization making a donation to the NGO will get a deduction of 50% from his/its taxable income. If an NGO gets registered under 12A and 80G, then only it is applicable for any government funding. A newly registered NGO can also apply for 80G registration. The following documents are required for 80G registration. Section 12A and 80G is of a great relief. NGOs do not have to pay tax for the entire period for which it gets registered under section 12A. Besides, the corporate and the ministries prefer to give donations to those who are having 12A and 80G registration. By doing such, their taxes are deducted by 50% of the donation given.

The website of a NGO is essential which speaks about the NGO profile, activates, their members, its history, address and the social work done by it. They should maintain their balance sheets, annual reports, accounts, records, bills, vouchers, photographs for proof of their social activities. This is of a real great help especially during the investigation by the IB officers during FCRA Registration or verification by the government officials applicable for government funding or any corporate officials applicable for corporate social responsibility funding.

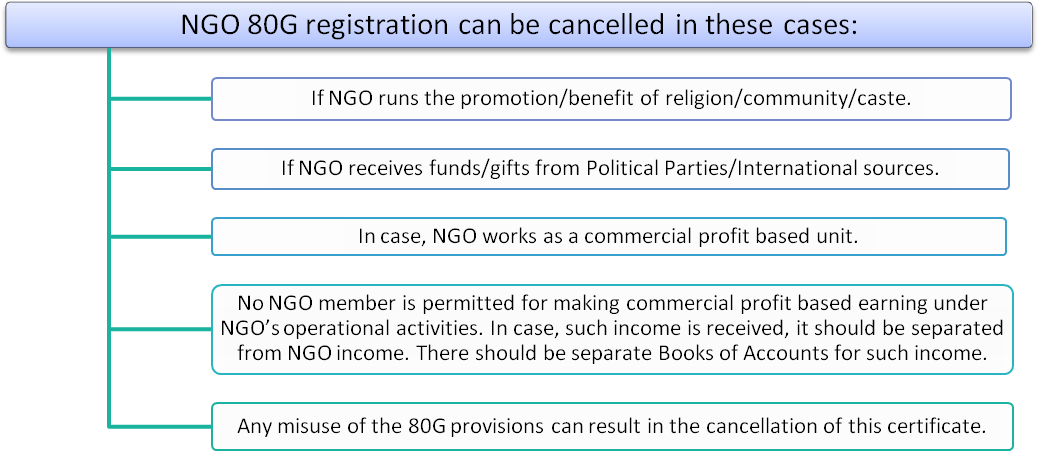

Condition for registration u/s 80G

- The NGO must not have any incomes which are not exempted, such as company income. If the NGO has business income, then it ought to preserve separate books of accounts and need not divert donations got for the purpose of such business if.

- The bye laws or goals of the NGOs must not contain any regulation for investing the income or possessions of the NGO for purposes aside from charitable activities.

- The NGO is not working for the advantage of particular religious community or caste.

- The NGO maintains routine accounts of its expenditures & receipts.

- The NGO is appropriately signed up under the Societies Registration Act 1860 or under any law corresponding to that act or is signed up under section 8 of the Companies Act, 2013.

There is a ceiling limitation up to which the benefit is allowable to the donor. If the quantity of reduction to a charitable organization is more than 10 % of the Gross Total amount income calculated under the Act (as lowered by earnings on which income tax is not payable under any arrangement of this Act and by any quantity in respect of which the assessee is entitled to a reduction under any other arrangement of this Chapter), then the quantity in excess of 10 % of Gross Total Earnings shall not get deduction under section 80G. While computing the overall income of an assessee and for arriving at the deductible quantity under section 80G, first the aggregate of the sums donated needs to be discovered. 50 % of such contributions have actually to be found out and it must be limited to 10 % of the gross total income. The unwanted will have to be ignored if such quantity is even more than 10 % of the gross overall earnings. The persons or company who donate under section 80G gets a deduction of 50 % from their taxable income.

Documents required for filing application u/s 12AB & 80G

Application Procedure

In order to claim exemption, an NGO should make an application to the Principle Commissioner or Commissioner of Income Tax in Form 10A. It has also been provided that the Form No. 10A shall be furnished electronically under digital signature (DSC), if the return of income is required to be furnished under digital signature or through electronic verification code (EVC) the following documents are required to be submitted:

- Copy of Registration certificate of the NGO (i.e. Certificate of Incorporation) and its bye-laws (i.e. Memorandum of Association/Articles of Association/Trust Deed)

- Copies of Detail of activities since its inception or last three years whichever is less

- Copies of audited accounts of the institution/NGO since its inception or last 3 years whichever is less.

- Copies of audited accounts of the institution/NGO since its inception or last 3 years whichever is less.

- Copy of Pan Card of the NGO.

- Details of the members of the NGO

- For an entity, created or established under an instrument, self-certified copy of such instrument creating or establishing the entity.

- For an entity, created or established otherwise than under an instrument, self-certified copy of such of the document evidencing creation or establishment of the entity.

- Self-certified copy of the registration with Registrar of Companies or Registrar of Firms and Societies or Registrar of Public Trusts, as the case may be.

- Self-certified copy of registration under Foreign Contribution (Regulation) Act, 2010 (42 of 2010), if the applicant is registered under such Act;

- Self-certified copy of existing order granting approval under clause (23C) of section 10/12A/12A/12AB;

- Self-certified copy of the order of rejection of application for grant of approval under clause (23C) of section 10/12A/12AA/12AB, if any;

- For existing entities, self-certified copies of the annual accounts of three years immediately preceding the year in which the said application is made;

- Where an undertaken is by the entity as per the provisions of sub-section (4) of section 11 and/ or where the income of the entity includes profits and gains of business as per the provisions of sub-section (4A) of section 11, self-certified copies of the annual accounts and report of audit as per the provisions of section 44AB of three years immediately preceding the year in which the said application is made;

- Note on the activities of the applicant.

Amendments by Finance Act, 2020

New Registration (As amended by Finance Act, 2020)

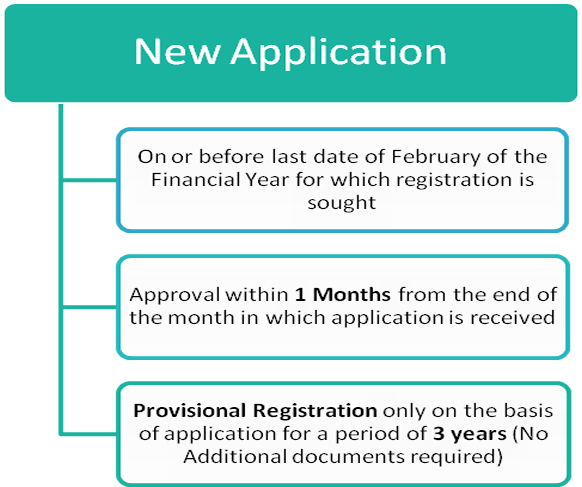

An application for fresh registration under section 12A will be given to Principal Commissioner or Commissioner, as per provisions of section 12AB. A provisional registration for 3 years will be given to organizations. The registration once granted shall be valid for three years from the Assessment Year from which the registration is sought. Application for renewal of such new registration needs to be submitted

- at least six months prior to the expiry of validity period or

- within 6 months from commencement if activities,

Whichever is earlier.

The registration so granted shall be valid for 5 years and further needs to be renewed after each 5 years of time.

Important Note: In cases of new registration, application shall be submitted; at least one month prior to the commencement of the previous year relevant to the assessment year for which registration is meaning thereby new NGO will not be entitled to have the benefit of registration of section 12AB in the first year of operation.

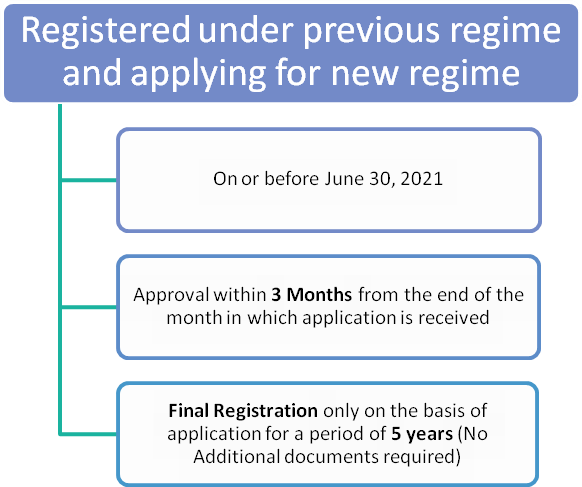

Migration of existing registrations (As amended by Finance Act, 2020)

All registered NGOs are required to apply for re-validation within three months from 1st April 2021. Registration so re-validated shall be valid only for 5 years. The application for the renewal of registration (after five years) needs to be submitted at least six months prior to the expiry of validity period.

No Simultaneous benefits for NGOs (As amended by Finance Act, 2020)

Where any organization’s registration has become non-operative due to simultaneous exemptions in various other sections [10(23C)] in that case it has to reapply under section 12AB. The registration will be given for 5 years, has to be renewed in every five year. The application should be submitted at least 60 months prior to expiry of registration.

Change or Modification of objects clause of NGOs (As amended by Finance Act, 2020)

Where an organization has been granted registration and subsequently there is change or modification of objectives of that organization then in this case it has to re-apply for registration with modified or changed objectives under section 12AB. The registration will be given for 5 years, has to be renewed in every five year. The application for registration shall be submitted within 30 days from such change in objectives.

Changes in compliance and registration procedure of religious or Charitable Trusts/ Institutions etc u/s 12AB & 80G for tax exemption

NNew rules for Trusts & NPO’s Registration u/s 12AB & 80G- Notification no. 19/2021 dated 26/03/2021 issued by CBDT, pertaining to procedure for registration of fund/trust/charitable institutions etc. Substitutes/Amends/Inserts rules related to registration of fund/trust/charitable institutions.

- All NGOs that are already approved under Section 12A/12AA and Section 80G as of this date & all such NGOs who shall be seeking Provisional Registrations with the Department shall file their Applications on Form-10A.

- All NGOs having provisional registrations shall at the time of seeking Final Registrations + All NGOs in the future at the time of applying and obtaining subsequent registrations shall file their applications on Form-10AB.

- Form-10G (for applying Registration u/s 80G) has been done away with & Form-10A or Form-10AB is a common Form for both types of Registrations applied either Section 12AB and/or Section 80G Registrations.

- Under the amended process, approval shall be granted for a period of 5 years, and the Non-profitable entities will be required to re-apply for registration in the manner and the period as prescribed the provision of the Act.

- Existing Non-profitable entity which is already approved under the erstwhile provisions of the Act is also required to make an application for registration in the prescribed form within 3 months from 1 April 2021.

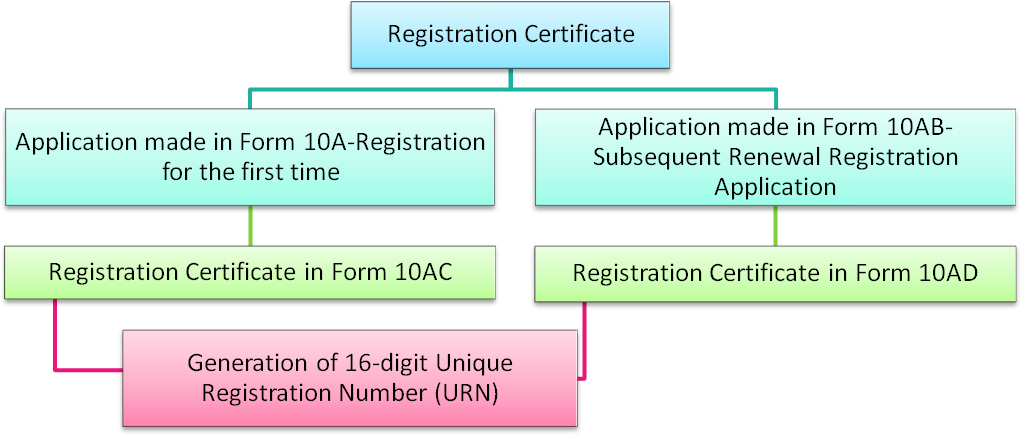

- Income Tax Department shall grant Registrations (order for registration or provisional registration or approval or provisional approval) on Form-10AC and Form-10AD shall carry a 16-digit alphanumeric Unique Registration Number (URN).For section 12AB and Section 80G on Form No. 10AC & in case of application on Form-10AB then on Form-10AD(order for registration or approval or rejection or cancellation).

- All Trust/ Societies/ Not-Profit Making Section-8 Companies granted Section 80G and Section 35(1) Registrations shall be required to file Online on Form-10BD; an “Annual Statement of Donations received” latest by May-31 immediately following the financial year in which the donation is received.

- The first such return/statement shall be applicable for the FY 2021-2022.

- The NGO shall be required to issue a “Certificate of Donation” to the Donor on Form-10BE for the amount of Donation given; (just like a TDS Certificate is issued to the payee).

- All Research Association, Universities, Colleges or other institutions or companies which are approved under section 35(1) as of this date shall be required to intimate under the fifth proviso to Section 35(1) to the Income Tax Department on Form No. 10A latest by June-30-2021.

- 11. All Research Associations, Universities, Colleges, or other institution or Company shall apply for approval of their projects under

- Scientific Research;

- Social Science Research or

- Statistical Research

- Existing Non-profitable entities already approved under existing rules shall apply within 3 months from 1 April 2021 in Form 10A. Approval shall be effective from the financial year in which approval was originally granted and the order shall be passed before the expiry of the period of 3 months from the end of the month in which the application was received.

- Non-profitable entities approved under newly inserted Rules through notification 19/2021 dated 26 March 2021 shall apply at least 6 months prior to the expiry of the period of approval in Form 10AB. Approval shall be effective from the financial year in which registration application is made and the order shall be passed before expiry of the period of 6 months from the end of the month in which the application was received.

- Provisionally approved Non-profitable entities shall apply at least 6 months prior to the expiry of the period of approval in Form 10AB. Approval shall be effective from the financial years for which provisional approval was received & the order shall be passed before the expiry of the period of 6 months from the end of the month in which the application was received.

- All applications made under the existing rules and are pending before the Principal Commissioner or Commissioner, on which no order has been passed before the 1st day of April 2021, shall be deemed to be an application made under clause (iv)/any other case shall apply at least one month prior to the commencement of the Financial year for which approval is sought in Form 10A. Approval shall be effective from the financial year in which registration application is made & order shall be passed before expiry of the period of 1 month from the end of the month in which the application was received.

In case of an application made under sub-clause (vi) of clause (ac) of sub-section (1) of section 12A during previous year beginning on 1st day of April, 2021, the provisional registration shall be effective from the assessment year beginning on 1st day of April, 2022.

Substituted, inserted or amended Forms

| S. No | Form No. | Rules | Purpose |

|---|---|---|---|

| 1 | Form No. 3CF | Rules 5C, 5D, 5E and 5F | Application for registration or approval |

| 2 | Form No. 10A | Rules 2C or 5CA or 11AA or 17A | Application for registration or provisional registration or intimation or approval or provisional approval |

| 3 | Form No. 10AB | Rule 2C or 11AA or 17A | Application for registration or approval |

| 4 | Form No. 10AC | Rule 2C or 11AA or 17A | Order for registration or provisional registration or approval or provisional approval |

| 5 | Form No. 10AD | Rule2C or 11AA or 17A | Order for registration or approval or rejection or cancellation |

| 6 | Form No. 10BD | Rule 18AB | e-Form for Statement of particulars to be filed by reporting person under clause (viii) of sub-section (5) of section 80G and clause (i) to sub-section (1A) of section 35 of the Income-tax Act, 1961 |

| 7 | Form No.10BE | Rule 18AB | Certificate of donation under clause (ix) of sub-section (5) of section 80G and under clause (ii) to sub-section (1A) of section 35 of the Income-tax Act, 1961 |

| Section | Amended Provisions | Amendments & Effective Date | Remarks |

|---|---|---|---|

| Sec. 12A | Clause (ac) of Sub-section (1) | Omitted w.e.f. 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission, clause (ac) was inserted by the Act No. 12 of 2020, w.e.f. 1-6-2020. |

| Inserted w.e.f. 01-04-2021 | Re-introduced from 01-04-2021 | ||

| “First Proviso” to sub-section (2) | Omitted w.e.f 01-06-2020 | “First Proviso” omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission, first proviso was amended by the Act No. 12 of 2020 w.e.f. 1-6-2020. | |

| “Second Proviso” to sub-section (2) | Amended w.e.f. 01-06-2020 | This now becomes the first proviso of section 12A (2). Reference to section 12AB omitted. | |

| “Third Proviso” to sub-section (2) | Amended w.e.f. 01-06-2020 | The existing third proviso has now become the second proviso and hence ‘"provided also" is substituted with "provided further". | |

| “Fourth Proviso” to sub-section (2) | Amended w.e.f. 01-06-2020 | Reference to section 12AB omitted. | |

| “First Proviso” to sub-section (2), after the amendment by this Act | Amended w.e.f. 01-04-2021 | Time-limit for applicability of exemption upon migration to new registration regime. | |

| “Second Proviso” to sub-section (2) | Amended w.e.f. 01-04-2021 | The existing second proviso will become the third proviso and hence "provided further" is substituted with ‘"provided also". | |

| “Fourth Proviso” to sub-section (2) | Amended w.e.f. 01-04-2021 | Reference to section 12AB inserted. | |

| Sec. 12AA | Sub-Section (5) | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission sub-section (5) was inserted by the Act No. 12 of 2020 w.e.f. 1-6-2020. |

| Inserted w.e.f. 01-04-2021 | This relates to Non-applicability of provisions of section 12AA. Earlier it was amended that the provisions of section 12AA would not apply from 01.06.2020. Now it has been amended to make it applicable from 01.04.2021. Thus, provisions of section 12AA will apply from 01-04-2021 and not from 01-06.2020. | ||

| Sec. 12AB | Entire Provisions | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission section 12AB was inserted by the Act No. 12 of 2020 |

| Inserted w.e.f. 01-04-2021 | This relates to procedure for fresh/new registration of a trust or institution. Earlier it was amended that the provisions of section 12AB would apply from 01.06.2020. Now it has been amended to make it applicable from 01.04.2021. Thus, provisions of section 12AB will apply from 01-04-2021 and not from 01-06.2020. | ||

| Sec. 56 | Clause (v), Clause (vi), Clause (vii) and Clause (x) of Sub-Section (2) | Omitted w.e.f 01-06-2020 | Reference to section 12AB omitted. |

| Inserted w.e.f. 01-04-2021 | Reference to section 12AB inserted. | ||

| Sec. 80G | In sub-section (2), in clause (a), in sub-clause (iiia) | Inserted w.e.f. 01-04-2020Inserted w.e.f. 01-04-2020 | PM CARES FUND included for 100% deduction without any limit |

| Clauses (vi) of sub-section (5) | Amended w.e.f. 01-06-2020 | Approval procedure amended and the provision as it stood prior to 01.06.2020 reintroduced. | |

| Clauses (vi) of sub-section (5) | Amended w.e.f. 01-04-2021 | Approval procedure amended and the provision as it stood as on 01.06.2020 introduced. | |

| Clauses (viii) and (ix) of sub-section (5) | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to their omission clauses (viii) and (ix) were inserted by the Act No. 12 of 2020 w.e.f. 1-6-2020. | |

| Clauses (viii) and (ix) of sub-section (5) | Inserted w.e.f. 01-04-2021 | Clause (viii) relates to furnishing of a statement of donation received from donors. Clause (ix) relates to furnishing certificates of donation to donors. Earlier these provisions were introduced by FA, 2020 to apply from 01.06.2020. Now it has been amended to make it applicable from 01.04.2021. Thus, these provisions will apply from 01-04-2021 and not from 01-06.2020. Further, the procedure for obtaining approval in case of an approved fund is deferred to 01.04.2021. These provisions related to fresh approval will now be applicable from 01.04.2021 instead of 01.06.2020 introduced earlier vide Finance Act, 2020. |

|

| Sub-section (5E) | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission sub-section (5E) was inserted by the Act No. 12 of 2020 w.e.f. 1-6-2020. | |

| Inserted w.e.f. 01-04-2021 | This relates to applicability of new approval provisions for pending approval application as on 01.04.2021. | ||

| Explanation 2A | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission sub-section (5E) was inserted by the Act No. 12 of 2020 w.e.f. 1-6-2020. | |

| Inserted w.e.f. 01-04-2021 | This relates to allowability of deduction for donation to donors on the basis of information furnished to income tax authority. | ||

| Sec. 115BBDA | Omitted w.e.f 01-06-2020 | Reference to section 12AB omitted. | |

| Inserted w.e.f. 01-04-2021 | Reference to section 12AB inserted. | ||

| Sec. 271K | Entire Provisions | Omitted w.e.f 01-06-2020 | Omitted by the Act No. 38 of 2020, w.e.f. 1-6-2020. Prior to its omission section 271K was inserted by the Act No. 12 of 2020 w.e.f. 1-6-2020. |

| Inserted w.e.f. 01-04-2021 | This relates to imposition of penalty for failure to furnish statement of donations u/s 80G(5)(viii) or failure to furnish certificate u/s 80G(5)(ix), section 35, etc. |

Certain Forms for Income Tax Deduction scrapped w.e.f. 1st April 2021

The Central Board of Direct Taxes (CBDT) has notified that Form 10G, 56, 3CF-I, 3CF-II and 3CF-III ceased to be effective on or after the 1 April, 2021.

| S. No | Forms | Particulars |

|---|---|---|

| 1 | Form 10G |

Application for grant of approval to fund or institution under clause (vi) of sub-section (5) of section 80G of the Income-tax Act, 1961. Earlier 10G form for 80G registration has been withdrawn; the same can be applied now with Form 10A or 10AB as the case may be. The application from 10A or 10AB as the case may be shall be accompanied by the various documents, as required by Form Nos. 10A or 10AB, as the case may be, namely where

It is noteworthy that similar amendment has been done in section 80G, where existing registration or new registration can be renewed/ applied by filing application 10A or 10AB as the case may be. Moreover trust or institutions who have been granted 80G registration needs to file a statement containing details of donations received in Form No. 10BD and a certificate in Form 10BE needs to be issued to donors. Cancellation of the approval granted in Form No. 10AC and Unique Registration Number(URN): If, at any point of time, it is noticed that Form No. 10A |

| 2 | Form 56 | The application for grant of exemption or continuance under section 10(23C) (iv) and (v) for the year has been omitted by the CBDT, instead Form 3CF can be used. |

| 3 | Form 3CF-I, 3CF-II and 3CF-III | Form No. 3CF-I/II and Form No. 3CF-III has been substituted by ‘Form No. 3CF’ under Rules 5C , 5D, 5E and 5F respectively of the Income-Tax Rules, 1962 and manner of furnishing the same has been introduced with regard to deductions of expenditure on scientific research. Form No 3CF is required to be furnished online electronically. Form 3CF shall be verified by the person who is authorized to verify the return of income under section 140 of the Act with digital signature (DSC) or EVC. If the return of income of the applicant is required to be furnished under digital signature, then furnishing Form 3CF with DSC is compulsory else the forms can be furnished with EVC. |

Application for fresh registration by charitable Trust, Society and Section-8 Company or institutions registered

- All the existing charitable Trust, Society and Section-8 Company or institutions registered/approved on and after 01-04-2016 u/s 12A, 12AA,10 (23C),80 G need not apply for renewal immediately. They have to calculate the period of registration and are required to apply 6 months before the end of 5 years from the date of registration/approval.

- 2. All the existing charitable Trust, Society and Section-8 Company or institutions registered:

- Under the sections 12A & 12AA need to be re-registered under the new section 12AB as and when due.

- Under section 10 (23C) need to apply again for fresh approval as and when due

- Under section 80 G needs to apply again for fresh approval as and when due

- The registration will be granted for a period of 5 years.

- Application has to be made in Form-10A for the purpose of Section 12AB.

- Provisional registration will be valid for maximum period of three years.

- On Commencement of Activities: Application has to be made for converting provisional to final registration in Form-10AB for the purpose of section 12AB.

- Documents required for registration are-

- 12A, 12AA,10 (23C),80G Certificate,

- Darpan Unique ID

- FCRA Registration Certificate, if any.

- Copy of Trust Deed or Bye Laws, MOA etc

- Copy of PAN of Organization

- PAN, AADHAR, Mobile No. & e-mail ID of members/trustee/Directors

- Rent Agreement & Electricity Bill

- Audited financial Statements and ITR for last 3 years, if any

- Annual/Activity Report for last 3 years, if any

- Digital Signature of Authorized Person

- If application is not made, existing Registration/Approval will lapse.

Why all the trust/NGOs needs to get register under Income Tax again?

The Finance Bill 2020 wants to consolidate all trust data to provide an electronic database. There are many old registered trusts, who might have misplaced their registration number and neither the Income Tax Department has any record of the same.

Appropriate Authority for Application

Form for application under section 12AB of Income Tax Act shall be made online by Filing Form 10A along with the required documents to the Commissioner or Principle Commissioner who shall pass an order granting approval or rejection within three months from date of commencement of new provisions, i.e., by 30th June 2021.

Section 12AB of Income Tax Act- From 1st April 2021, the new provisions will come into effect, as a result of which every trust or institution which are already in existence will have to mandatory renew the certificate granted under section 12A, 12AA, 80G, or section 35 with the time limit of 3 months which is 30th June 2021 and In the case of new Trusts or Institutions, they will have to apply for registration under section 12AB of the Income Tax Act, 1961.

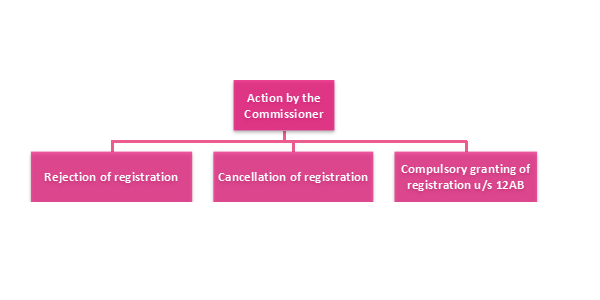

Further, in case where Commissioner or Principle Commissioner is satisfied that the charitable/religious trusts institution etc. have not complied with the objects mentioned or any other law, shall cancel the registration of charitable/religious trusts institution etc. after providing the reasonable opportunity of being heard.

Similarly there are different time limits under different categories which can be summarized below:-

| Category | Time Limits |

|---|---|

| Institutes already registered under section 12A or 12AA or having certificate under section 80G | By 30th June 2021 |

| Institutes who have obtained registration under section 12AB | 6 months prior to the expiry of tenure of 5 years (refer the Validity Period of Registration Paragraph) |

| Institutions that have provisionally obtained registrations under section 12AB | 6 months prior to the expiry date of the provisional registration; or

Within 6 months of the commencement of its activities; Whichever is earlier. |

| Where institutions have modified the objectives | Within 30 days from the date of such modifications. |

| In any other case | At least one month prior to the commencement of the previous year. |

Validity period of Registration:-

In case of trusts or institutions which are having existing registration u/s 12AA shall apply for registration u/s 12AB online by 30-06-2021 in Form 10A. The validity of registration u/s 12AB shall be for 5 years. However, provisional registration shall be granted for a period of 3 years.

It is mandatory for all the trusts/ societies/institutions registered under section 12A and 80G to obtain fresh registration.

Time limit for registration under section 12A (1) (ac) and section 12(AB)

| Sub-clause of clause (ac) of section 12A(1) | Category of Entity | Time limit for filing application for registration | Applicable Form | Time limit for passing order |

|---|---|---|---|---|

| 1 | Trusts or institutions which are having existing registration u/s 12A or 12AA (Migration from section 12A/12AA to section 12AB) | Within 3 months from 1st April, 2021 i.e. up to 30th June, 2021 | Form 10A | Within 3 months from the end of the month in which the application is received |

| 2 | Trusts or institutions which are registered under section 12AB and the period of the said registration is due to expire | Atleast 6 months before the expiry of the said period | Form 10AB | Within 6 months from the end of the month in which the application was received |

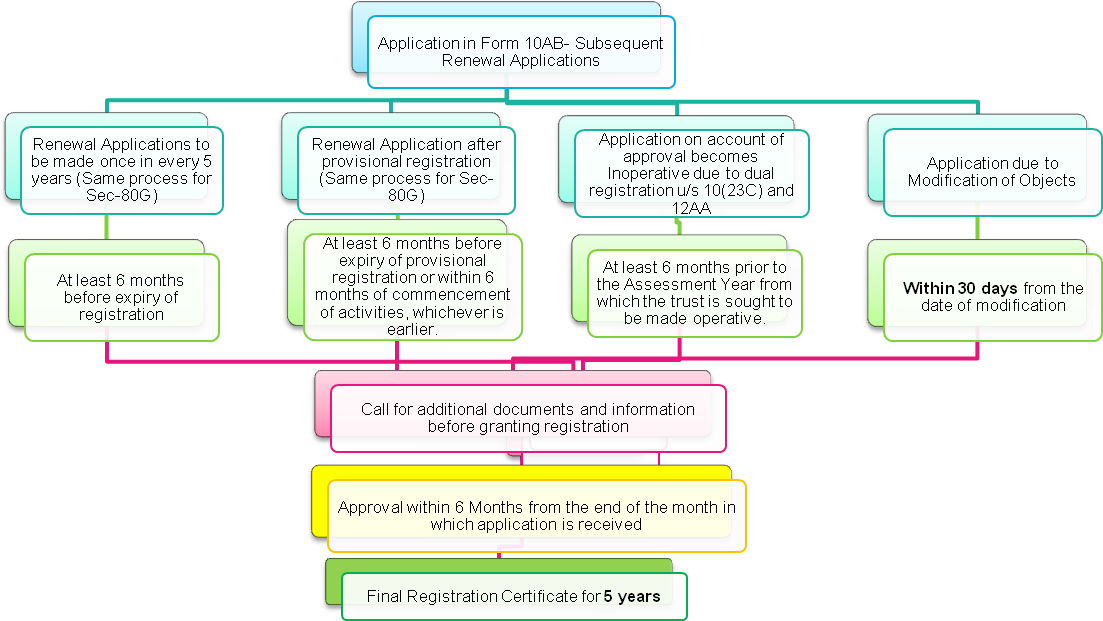

| 3 | New trusts or institutions which have been granted provisional registration under section 12AB (Trusts opting for provisional to final registration for 5 years) | Atleast 6 months before the expiry of the provisional registration or within 6 months of commencement of its activities, whichever is earlier | Form 10AB | Within 6 months from the end of the month in which the application was received |

| 4 | Trusts or institutions whose registration has become inoperative due to first proviso to section 11(7) of the Act. Registration u/s 12A or 12AA shall become inoperative from the date on which the trust or institution is granted registration u/s 10(23C) | Atleast 6months before the commencement of the assessment year from which the said registration is sought to be made operative | Form 10AB | Within 6 months from the end of the month in which the application was received |

| 5 | Trusts or institutions who has adopted or undertaken modifications of the objects which do not conform the conditions of registration | Within a period of 30 days from the date of adoption or modification | Form 10AB | Within 6 months from the end of the month in which the application was received |

| 6 | In any other case (including fresh provisional registration) | Atleast 1 month before commencement of the previous year relevant to assessment year from which the said registration is sought | Form 10A | Within 1 month from the end of the month in which the application is received |

Pre-Registration Preparation

The application can be made by filing form 10A online on the income tax site incometaxindiaefiling.gov.in

The form is available on the income tax website under Income Tax Forms Section under e-file menu which is visible after login on the website.

Contents required to be furnished in Form 10A:-

- Name of the Trust, Society or Institution.

- PAN details of the Trust, Society or Institution.

- Registered Address of the Trust, Society or Institution.

- Select the type of Trust:- Religious/ Charitable/ Religious-cum-Charitable

- E-Mail and Mobile number of the Managing Trustee/Chairman/Managing Director/Any authorized person by whatever name called

- Legal Status of the Trust

- Objects of the Trust whether it is religious/relief of poor/yoga/preservation of environment/advancement of other objects of general public utility/education/medical relief/preservation of monuments or places or objects of artistic or historic interest.

- Date of Modification of Objects, if any.

- Whether the application granted in the past is rejected or the registration is cancelled? If yes, details of the order cancelling the same.

- If the applicant is registered under FCRA, 2010? If yes, then details of the same.

Documents required for Registration:-

Following is the list of documents as mentioned on the Income Tax Website:-

- Where the trust is created, or the institution is established, under an instrument, self-certified copy of the instrument creating the trust or establishing the institution;

- Where the trust is created, or the institution is established, otherwise than under an instrument, self-certified copy of the document evidencing the creation of the trust, or establishment of the institution;

- Self-certified copy of registration with Registrar of Companies or Registrar of Firms and Societies or Registrar of Public Trusts, as the case may be;

- self-certified copy of registration under Foreign Contribution (Regulation) Act, 2010 (42 of 2010), if the applicant is registered under such Act;

- self-certified copy of the documents evidencing adoption or modification of the objects, if any;

- where the trust or institution has been in existence during any year or years prior to the financial year in which the application for registration is made, self certified copies of the annual accounts of the trust or institution relating to such prior year or years (not being more than three years immediately preceding the year in which the said application is made) for which such accounts have been made up;

- note on the activities of the trust or institution;

- self-certified copy of existing order granting registration under section 12A or section 12AB, as the case may be; and

- Self-certified copy of order of rejection of application for grant of registration under section 12A or section 12AB, as the case may be, if any.

- where a business undertaking is held by the applicant as per the provisions of sub-section (4) of section 11 and the applicant has been in existence during any year or years prior to the financial year in which the application for registration is made, self-certified copies of the annual accounts of such business undertaking relating to such prior year or years (not being more than three years immediately preceding the year in which the said application is made) for which such accounts have been made up and self-certified copy of the report of audit as per the provisions of section 44AB for such period;

- where the income of the applicant includes profits and gains of business as per the provisions of sub-section (4A) of section 11 and the applicant has been in existence during any year or years prior to the financial year in which the application for registration is made, self-certified copies of the annual accounts of such business relating to such prior year or years (not being more than three years immediately preceding the year in which the said application is made) for which such accounts have been made up and self-certified copy of the report of audit as per the provisions of section 44AB for such period;

In simple words, we can say the following is required for registration

Following documents are required from the client and annexed to FORM 10A while registration:-

- Registration Certificate and MOA / Trust Deed (two copies- self attested by the Managing Trustee)

- NOC from the Landlord where registered office is situated (if place is rented)

- Copy of PAN card of Trust.

- Electricity Bill/ House Tax/ Water Bill.

- Evidence of welfare activities carried out and progress report of the same since 3 years or since inception.

- Books of Accounts, Balance Sheet, ITR (if any) since inception or last 3 years

- List of Donors with their PAN and address

- List of Governing body or members of the trust/ Institution in the following format

S.No Name Address Adhaar No. PAN Mobile No. Email id - Trust Deed for verification of Original Registration Certificate and MOA

- 10. Any other information / document as may be asked by the Income Tax Department.

Conclusion:-

From 1st October 2020, the new provisions will come into effect, as a result of which every trust or Institution which are already in existence will have to mandatorily renew the certificate granted under section 12A, 12AA, 80G or section 35 within the time limit prescribed which is latest by 30th June 2021.

In case of new Trusts or Institutions, have to apply for registration under section 12AB within the time limit prescribed.

New Registration or Renewal process for Trusts- Section 12AB of Income Tax Act

Procedure of registration under section 12AB

Step-1: Log in to Income Tax India E-Filing Portal using to login credentials and password

Step-2: Navigate to “Income Tax Forms” under E-File tab and select Form 10A/ 10AB, as the case may be

Step-3: Select the option “Prepare and submit online” to fill requisite details in the form

Step-4: Attach the requisite document along with Form 10A/10AB

Step-5: Submit the form using digital signatures or EVC

Step-6: On receipt of application in Form No. 10A or 10AB, as the case may be, the PCIT or CIT shall process the application within the prescribed time limit: -

- In case the applicant is already registered u/s 12AA or in case of provisional registration, where Form No. 10A has been submitted by the applicant: - Order granting registration shall be granted in writing in Form No. 10AC. A 16-digit alphanumeric Unique Registration Number (URN) shall be allotted on successful registration.

- In cases where Form No. 10AB has been filed, order granting registration or rejection or cancellation shall be in Form No. 10AD.

Similar amendment in registration/ renewal procedure has also been made in section 80G. Thus, the existing trusts/ institutions will now have to apply for fresh registration under section 80G in the same manner as applicable in section 12AB. Such application shall be made through Form No. 10A or 10AB, as the case may be.

An important change which has been made is that trusts or institutions that are registered u/s 80G shall now furnish a statement containing details of donations received during the year in Form No. 10BD in the prescribed manner. Further, the trust or institution shall issue a certificate of donation to the donor in Form No. 10BE.

Renewal of registration u/s 12A or section 12AA, as well as renewal of approval under section 80G, is being deferred to 1st April, 2021. The new registration procedure prescribed under section 12AB was supposed to be made applicable from 01/06/2020 and was supposed to be completed by 31/08/2020, which was firstly deferred and extended to 01/10/2020 and end by 31/12/2020 but considering the current pandemic situation, it has been extended to 01/04/2021 and hence now all existing trust have to re-register themselves under section 12AB from 01/04/2021 and before end of three months from the 1st day of April, 2021.

For trusts/institutions which intend to get themselves registered for the first time have to follow the new procedure which is as under –

Step no 1: Getting Provisional Registration

Step no 2: Converting Provisional registration into Final Registration

The old regime of registration procedure will continue till 31-03-2021.

New Registration U/S 12AB for the First Time

For trusts/institutions which intend to get themselves registered for the first time have to follow the new procedure which is as under –

Step no 1: Getting Provisional Registration

Step no 2: Converting Provisional registration into Final Registration

For Seeking Provisional registration- Form No. 10A

The time limit for filing application is at least one month prior to the commencement of the previous year relevant to assessment year from which the said registration is sought. Those trusts/ institutions which intend to seek registration from FY 2021-22 (i.e. AY 2022-23) Since the corresponding rules and forms were not available before 01.03.2021 such application could not be made. Considering this situation, an exception is being provided under rule 17A of the Income-tax rules, 1962- In case of an application made under sub-clause (vi) of clause (ac) of sub-section (1) of section 12A during previous year beginning on 1st day of April, 2021, the provisional registration shall be effective from the assessment year beginning on 1st day of April, 2022.

Accordingly, an application made during the FY 2021-22 for registration under [Section 12(1)(ac)(vi) i.e. Registration for the first time] then the provisional registration granted will be effective from same Financial year (i.e. relevant assessment year). It be kindly noted this exception is provided for covering the year of transition and not applicable for subsequent Assessment years i.e. from AY 2023-24. For those subsequent periods, application has to be made a month prior to the start of previous year relevant to that assessment year in which registration is sought.

Apart from the documents and information as required for filing application under form 10A no other information will be sought for granting provisional registration under section 12AB. Thus, it is very apparent that upon filing application in form 10A (for Provisional registration) the concerned income-tax authority (CIT or PCIT) has to issue provisional registration certificate (in form 10AC with 16 digit unique registration number) without any further verification or examination.

However, it be noted that according to rule 17A(6), of the Rules, if at any point of time it is noticed that Form No. 10A is not furnished properly or correctly, the CIT or PCIT after granting an opportunity of being heard may cancel the registration under form 10AC.

Granting Provisional registration: Within 1 month from the end of the month in which application was received by concerned authority (CIT or PCIT). The Provisional registration will be valid for 3 years from the assessment year from which the registration is sought

For Converting Provisional registration into Final Registration- Form No. 10AB

As mentioned above the first step for getting registered is seeking provisional registration and thereafter converting it to Final registration. Accordingly, the time frame is atleast 6 months prior to the expiry of period of the provisional registration (provisional registration is valid for three years) or within 6 months from the commencement of the activities. Generally trusts immediately after getting formed start their activities but tend to defer seeking funds till they get registered under Income-tax Act so as to plan their taxes (this is the reason behind the idea of introducing Provisional Registration to be granted on fast track basis). Now, since, the registration will be granted on fast track basis, the trusts/institutions can start their activities immediately, and they must apply for Final registration immediately (max time limit is within 6 months from commencement of activities)./p>

After filing form 10AB with requisite documents and information, the procedure is exactly same as it was prevailing immediately before 01.04.2021. That is to say, the CIT or PCIT shall call for such documents or information or make such inquiries as he thinks necessary in order to satisfy himself about genuineness of the activities of the trust or institution and the compliances of other laws [as per section 12AB(1)(b)(i)].