One Person Company (OPC) Registration in India

As per section 2 (62) of the Companies Act, 2013,One Person Company means a company which has only one person has a member.OPC can be formed with just 1 Director and 1 member. It is a form of a company where the compliance requirements are lesser than that of a private company and entrepreneurs who on their own are capable of starting a venture by allowing them to create a single person economic entity.

A single person company can work as a company without the complexity of having partners. This encourages more people to come forward to commence a business. The OPC is fit for small businesses where the turnover is not likely to cross ₹2 crores. In OPC Registration it’s important to note that the nominee or the director should be Indian Resident.

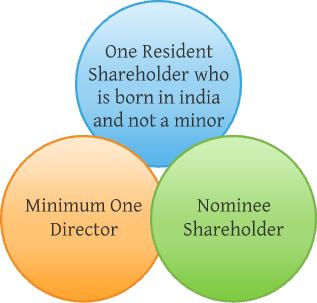

Only a natural person who is an Indian citizen and resident in India shall be eligible to act as a member and nominee of an OPC where the term "resident in India" means a person who has stayed in India for a period of not less than 182 days during the immediately preceding one financial year.

No person shall be eligible to incorporate more than one OPC, that is, no person shall be eligible to become member in more than one OPC. So a natural person shall not be a member and nominee of more than a One Person Company at any point of time. Where a natural person, being member in One Person Company becomes a member in another OPC by virtue of his being a nominee in that OPC, then such person shall meet the eligibility criteria of being a member in only one OPC within a period of 180 days, i.e., he/she shall withdraw his membership from either of the OPCs within 180 days. Form INC-4 shall be filed in case of withdrawal of consent by the nominee or in case of intimation of change in nominee by the member.

Following persons shall not be eligible to become member of OPC:

- Minor

- Foreign Citizen

- Non –Resident

- A person incompetent to enter into a contract

- Person other than Natural Person

Characteristics of One Person Company (OPC)

OPC can have Minimum One and Maximum Fifteen Directors. They can appoint more than 15 directors after passing of special resolution. The restriction is on number of memebers and not Directors. The shareholders/members are the owners of the company and shall be entitled to share in the profits of the company at the ratio of their shareholding. In contrast, the directors shall be responsible for the day to day management of the companyand compliance.

There is no specific tax advantage to an OPC over any other form. The tax rate is flat 30%, other tax provisions like MAT & Dividend Distribution Tax applies as they apply to any other form of company.

The company shall file form INC-4 in case of cessation of member of OPC on account of death, incapacity to contract or change in ownership. In the same form, user needs to provide details of the new member of the OPC. The company shall be having one member and shall appoint one nominee to act as member in case of death or incapacity of the member at the time of conversion into OPC.

In case the paid-up share capital of an OPC exceeds ₹ 50 lakh or its average annual turnover of immediately preceding three consecutive financial years exceeds ₹2 crore, then the OPC has to mandatorily convert itself into a private or public company. The OPC shall inform RoC in form INC-5 within 60 days of exceeding threshold limits and is required to be converted into private or public company within a period of six months. Form INC-6 shall be filed by an OPC for conversion of an OPC into private or public company.

When a One Person Company gets incorporated, it cannot convert itself voluntary to Private or Public company before two years from the date of incorporation. Form INC-6 shall be filed within 30 days in case of voluntary conversion and within six months of mandatory conversion.

The OPC and the member at any time can change the name of the nominee of the OPC. However, it is important to note that even the nominee can withdraw his consent at any time.

If a situation arises that the nominee becomes member of the OPC when the member dies and along with it he is also the member of his own OPC then a single person becomes member of two OPCs at the same time by virtue of circumstances and not voluntarily. In such a case, he shall meet the criteria as specified in the law within a period of 180 days and withdraw his membership from either of the OPCs.

One Person Company shall file a copy of the financial statements duly adopted by its member, along with all the documents which are required to be attached to such financial statements, within 180 days from the closure of the financial year.

The provision of holding of Annual General Meeting is not applicable to OPC.

The OPC is required to hold minimum two Board meeting during a calendar year and one meeting in each half of the calendar year and gap between two meetings is not more than 90 days.

For the purposes of quorum, in case of a single Director, it shall be sufficient if the passed resolutions is entered in the minutes book and signed and dated by such director.

No minor shall become member or nominee of the One Person Company or can hold share with beneficial interest in such OPC.

Such Company cannot be incorporated or converted into a company under section 8 (Company with Charitable Objects) of the Act.

No such company can convert voluntarily into any kind of company unless two years is expired from the date of incorporation of One Person Company except in the case if its falls under the mandatory conversion criteria.

Company shall state word ‘OPC’ in the bracket after the name of the Company, like XYZ (OPC) Private Limited.

One director of the OPC must be resident in India. A person is said to be resident if he or she stays in India for at least 182 days during the preceding financial year irrespective of their citizenship. The days of stay can be in phases.

Such Company cannot carry out Non-Banking Financial Investment activities including investment in securities of any other body corporate

There is no minimum capital requirement as such to be maintained in the company and investment can be done as per the requirement of the business. However, the government fee for one person company registration is calculated on the capital. The least capital demand is ₹ 1 Lakh but this amount varies from investment. Authorised capital and investment are not the same in OPC Company. One can invest as much as they want to but when they need to incorporate a company professionally, it has to be begun with ₹1 Lakh as capital.

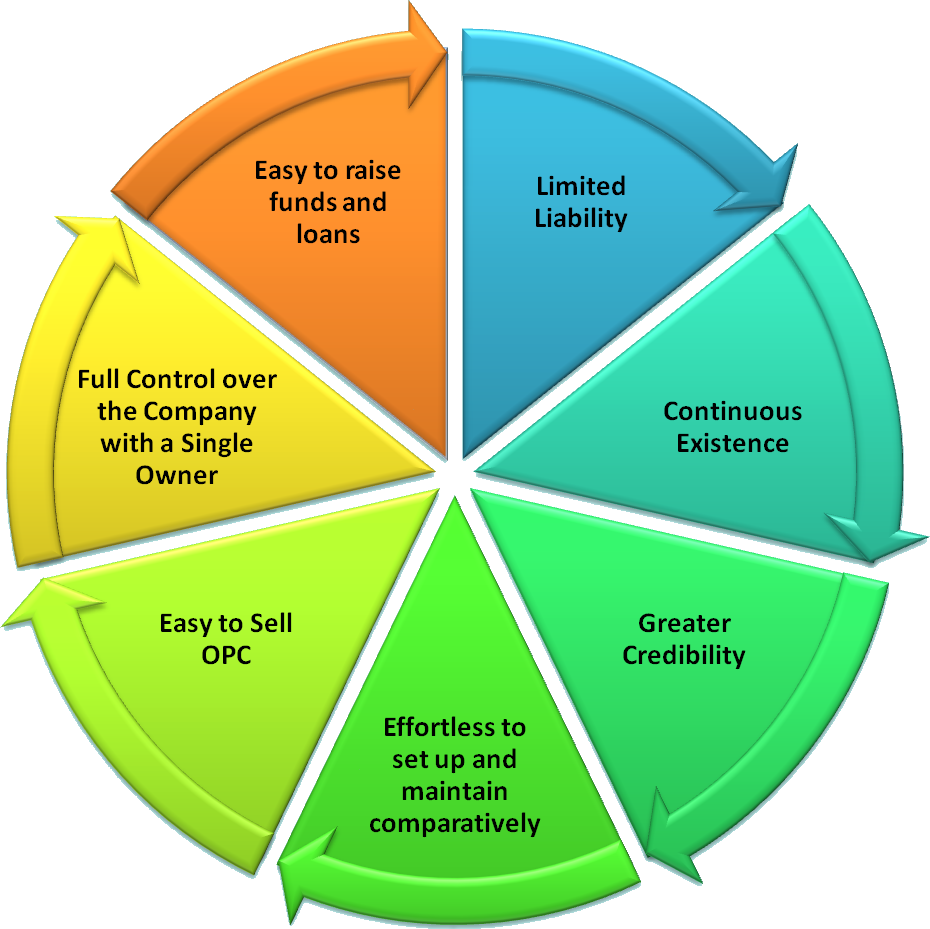

Limited Liability implies that the owner or shareholder of the One Person Company is not personally liable to pay debts of the business. They are only responsible for the unpaid shares of the capital of the company. To qualify, the shareholder needs to comply with all laws and pay taxes on time.

The company will continue to exist, no matter how many directors, officers, and shareholders join or leave.

A Company can Sue and be Sued in its name.

A legal entity like a company has a separate identity from its owners or shareholders.

The private limited companies receive financial assistance from banks and financial institutions, but it receives the preferred rate of interest.

Like a person a private limited company can purchase, sell, own, possess, enjoy and transfer property rights to anyone in its name.

An OPC is prohibited from giving any invitations to public to subscribe for the securities of the company.

If a One Person Company or an officer of such Company is not compliant with the specified regulations, the entity or the officer will incur penalties which could be as high as ₹10,000. Further, the penalty will be increased by a fine of ₹1,000/- for each day of default.

An OPC must inform the Registrar about every contract entered into by the company with the sole member of the company within a period of 15 days from the date of approval.

Benefits of One Person Company (OPC)

Exemptions for an OPC

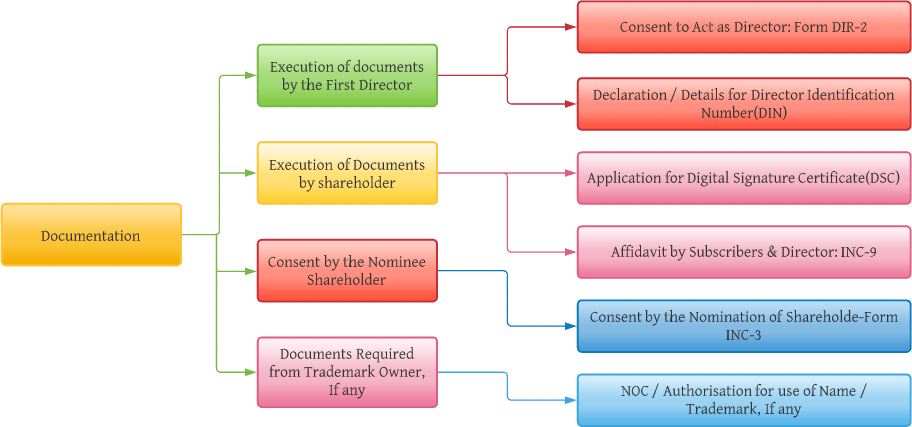

Pre-Requisites of One Person Company

Section-8 Company Incorporation Process

Obtain a DSC-Digital Signature Certificate in electronic format from Government Recognized Certifying Agencies

Register your director by applying for DIN-Director Identification Number (in Form DIN 3 in existing company or directly with SPICe INC 32 upto 3 directors)

Enlist the Company's constitution in Memorandum of Association(MOA) in e-(MOA) and Articles of Association (AOA) in e-(AOA) directly with SPICe INC 32

Obtain Name Approval Certificate in RUN Form(Reserve Unique Name) or directly apply with SPICe INC 32 -in both cases 2 chances are given with one Resubmission (RSUB). The name approved by CRC will be valid for 20 days. The name of a One Person Company shall end with the words (OPC) Private Limited.

To get the company Identification Nember-(CIN) address for the Registered Office and NOC from the landlord is required.

Form INC-20A

Form in respect of commencement of Business within 180 days of incorporation

Current Bank Account to be Opened in Company's Name

GEt the Certificate of Incorporation-(COI) issued by ROC with the PAN & TAN

Application for Goods and Services Tax Identification Number (GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration (AGILE-PRO) in Form INC 35

Apply for PAN and TAN with SPICe INC 32

Apply for PAN and TAN with SPICe INC 32

GEt the Certificate of Incorporation-(COI) issued by ROC with the PAN & TAN

Application for Goods and Services Tax Identification Number (GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration (AGILE-PRO) in Form INC 35

Current Bank Account to be Opened in Company's Name

Form INC-20A

Form in respect of commencement of Business within 180 days of incorporation

Post incorporation procedures of One Person Company

Opening a Company Bank Account

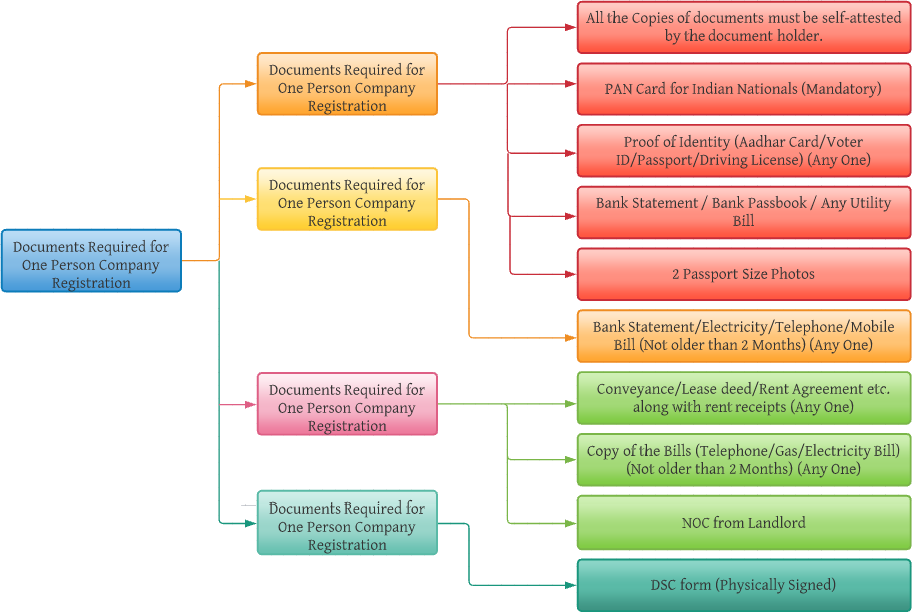

Documents Required

- Company PAN Card

- Board Resolution for opening and operating company bank account

Depositing of Share Capital money into Bank Account

Within 60 days of the Incorporation of the company, the shareholder must deposit the capital into company bank account

Issue of Share Certificates to Shareholders

- The company must issue Share Certificates to its shareholders within 2 months of its Incorporation

- A share certificate is a documentary evidence of a number of shares held by an individual in the Company.

- For non-compliance the Penalty is heavy. Fine to the Company range from ₹ 25,000 to ₹ 500,000. To Individual directors, penalty from ₹10,000 to ₹ 100,000.

Disclosure of interest by Directors

- Every Director of the Company in its First Board meeting after incorporation will disclose his or her interest (ownership or shareholding or directorship) in any other company/LLP/Firm.

- This is a very important compliance, which helps board of directors to take transparent decisions in the interest of the Company and to take up related party transaction compliances.

GST Registration

- If the current supply of goods or service is over ₹ 20 lakh, you need to get a GST Registration (if your business operates exclusively in the North Eastern states, ₹ 10 lakh) within 30 days of business incorporation.

- Anyone supplying goods or services to another state, need to apply for GST regardless of turnover.

- Even online service provider serving customers in another State will instantly attract GST registration.

- Once a One Person Company gets registered under GST, it becomes necessary to file GST returns monthly, quarterly or yearly depending upon the types of GST returns .

MSME /SSI Registration

MSME registration is the procedure to get your company registered under MSME development Act for SME benefits.

Trademark Registration

Many brands in the world value their trademark more than their any other physical assets and want to protect it through Trademark Registration.

Accounting Process

Get your Invoicing, book keeping and cash flow management set right from the beginning. Every One Person company shall maintain proper books of accounts which shall represent an accurate and fair view of the state of affairs of the company. Accounting is necessary for the statutory audit, Annual filing and IT return filing which is mandatory once you start your Company. These books of accounts shall be audited by the auditor appointed by the company.

Company Minutes Book & Statutory Registers

- An OPC Company with multiple directors has to maintain and update from time to time 7 to 8 mandatory registers like Register of shares, Register of Member, Register of Directors etc, besides Minutes of the Board Meetings and Annual General Meeting.

- Statutory Registers and Minutes book are documentary evidence of decisions of the Company.

- For non-compliance the Penalty is heavy. Fine to the Company range from ₹ 50,000 to ₹ 300,000. In addition to ₹ 1,000 per day for continuing default

Board of Directors Meeting

- The First Board meeting of multiple director OPC Company shall be conducted within 30 days of Incorporation.

- Further, minimum 2 Board Meetings shall be held in a calendar year (one meeting in every 6 months). Directors Meeting or Board meetings are very important events in decision making process and management of the company.

- In case of a OPC Company which has 1 Director, Board of Directors meeting is not Applicable.

- Following the legal procedure is very important for compliance purpose, non-compliance may lead to legal problems in case of disputes among the Directors

Income Tax Return Filing

- Income Tax return is a statement of Company's earnings from various sources of income, tax liability thereon, details of tax paid and any refunds that have to be given by the government.

- Filing of Income Tax return is an annual event and need to done once in a year.

- Non-filing of Income Tax Return attracts interest, penalty, prosecution and scrutiny from the Income Tax Department.

- IT return is mandatory even if the company does not make any income during the year.

Income Tax Audit

Irrespective of turnover every One Person Company requires to get the tax audits under section 44AB done.The Tax audit under section 44AB aims to ascertain the compliance of various provisions of the Income-tax Law and the fulfillment of other requirements of the Income-tax Law.The tax audit limit under section 44AB is ₹ 1 Crores( ₹ 5 crores where at least 95 % turnover is made on digital transactions)

Statutory Audit

Every One Person Company registered under the Companies Act, 2013, irrespective of its sales turnover or nature of business or capital must have its book of accounts audited each financial year. Thus, the Board of Directors of a One Person Company are required by law to appoint an Auditor within 30 days of incorporation of the company and thereafter conduct an audit of its financial statements each Financial Year.

MAT Audit

It is mandatory for the One Person Company to get their accounts audited under MAT i.e. Minimum Alternate Tax. The objective of the introduction of MAT was to bring into the tax net “zero tax companies” which in spite of having earned substantial book profits and having paid handsome dividends, do not pay any tax due to various tax concessions and incentives provided under the Income-tax Law.

OPC ROC Filing of Annual Return

- A One Person Company is mandatorily required to file 3 forms every year. Filing has to be done regarding submission of documents of financial statement, i.e. balance sheet, P&L account in ROC form AOC 4 and annual return in ROC form MGT-7. Company report about auditor’s appointment to ROC in Form ADT 1.

- Every OPC is required to file its Annual Return (MGT-7) with the ROC within 60 days of the event date. The Financials including Balance Sheet, Profit and loss account (AOC-4) to be filed within 180 days from end of the Financial Year. The Auditor Appointment (ADT-1) to be filed within 15 days from the AGM.

- TheROC Annual Filing is an annual event giving details of Management, Financial performance and Governance to the ROC under whose jurisdiction the Company registered office is located.

IEC Registration

All the One Person Company which are engaged in Import and Export of goods require to register the Import Export Code. IE code has lifetime validity. Importers are not allowed to proceed without this code and exporters can’t take benefit of exports from DGFT, customs, Export Promotion Council, if they don’t have this code.

Compliance checklist for one person company

| S.No | Particulars | Section & Rules | Status |

|---|---|---|---|

| 1 | Form INC-20A | Form in respect of commencement of Business within 180 days of incorporation | |

| 2 | Stamp duty on Share Certificates | Payment of stamp duty is to be made within 30 days from the issue of share certificates | |

| 3 | Board Meeting | Minimum Two Board Meetings Atleast one Board Meeting in each half of calendar year and gap between two meetings is not less than 90 days | |

| 4 | Annual General Meeting | No such requirement to hold AGM as OPC is exempted from holding Annual General Meeting | |

| 5 | MBP-1 | 184(1) | Disclosure of interest is required to be given in the first Board Meeting or where ever there is any change by every Director of Company. Fresh MBP-1 is required to be submitted whenever there is change in director interest from the earlier. |

| 6 | DIR-8 | 164(2), 143(3)(g) | Declaration in form DIR-8 that director is not disqualified is required to be given in every financial year. Disclosure of non-disqualification in each financial year by every director. |

| 7 | Statutory Registers, Minutes Books and Records | Maintenance of mandatory statutory registers, minutes Book and other secretarial records is required to be done | |

| 8 | Form AOC-4 (Financial Statements) | Section 137 | Company is required to file its Balance sheet along with Statement of Profit and Loss Account, Director Report and Auditor report within 180 days from end of financial year i.e. 31st March |

| 9 | Form MGT-7 * (Annual Return) | Section 92 | within 180 days from end of financial year i.e. 31st March |

| 10 | Income Tax Return of Company | 30th of September of each financial year | |

| 11 | DIR- 3 KYC (Directors KYC) | Rule 12A | By all the Directors of the company shall file DIR-3 on/before 30th of September of next financial year |

| 12 | ADT-1 (Auditor’s Appointment) | Section 139 | Auditor will be appointed for 5 years in form ADT-1 within 15 days of Annual General Meeting. |

| 13 | E-Form MSME-I (Half Yearly Return) | Section 405 | Every Company having outstanding payments dues to micro and small enterprises and in case the payment of the same is pending beyond 45 days, then the Company has to furnish details as per the following timeline:

|

| 14 | E-Form DPT-3 (Return of Deposits) | Section 73,Rule 16 | All the Company having any outstanding loan/amount as on 31st March of every financial year has to furnish details and bifurcation of such outstanding amount irrespective of the fact whether such amount is falling under the definition of deposit or not by 30th June |

*In respect of filing of Annual Return of OPC, unlike other companies there is no such requirement of filing Annual Return within sixty days of AGM as the provisions of AGM doesn’t apply to One Person Company.

Nature of OPC at a Glance

| S.No | Particulars | OPC Company |

|---|---|---|

| 1 | Eligibility | Only an individual who is an Indian citizen and resident in India is eligible to incorporate an OPC |

| 2 | Minimum Requirement | Member – 1, Director – 1, Nominee of Sole Member – 1 |

| 3 | Procedure | Get DSC, DIN, MoA & AoA along with INC-32 Incorporation Filing, PAN, TAN Applications |

| 4 | Existence | Existence of an OPC is never dependent on the Nominee or Director. Can be dissolved by Regulatory Authorities. |

| 5 | Credibility | Medium |

| 6 | Time Taken in Registration | 15 – 20 Days |

| 7 | Conversion System | Cannot be converted before 2 years |

| 8 | Compliance Requirements | Annual Return Filing No Board Meetings, if only one director No General Meetings |

| 9 | Statutory Audit | Compulsory |

| 10 | Fund Raising Options | Low |

| 11 | Recommended For | Sole promoters |

| 12 | Foreign Investment | Not Allowed |

Frequently Asked Questions

- 1. What are the minimum requirements to register a (OPC)? Company?

-

- Minimum 1 Director shall be appointed (Director can be a Member also) who shall be an Indian resident and maximum Directors may be 15.

- There must be only 1 person as a member (Member should be citizen and residence in India

- No company can be registered without having (OPC) Private Limited or limited at the end.

- A nominee who is above the age of 18 years and Indian resident must be appointed as Nominee on registration.

- A place of business in India must be provided as a registered office address.

- 2. What is the concept of nominee in case of OPC?

-

At the time of incorporation of OPC, the sole member of OPC is required to appoint another person as his nominee and his name shall have to be featured in the Memorandum of Association of the OPC.

The nominee so appointed shall:

- in the event of the sole member’s death; or

- in the event of the sole member becoming incapacitated to Contract;

become the member of OPC

- 3. Can the member of the OPC change the nominee?

-

- As per the third proviso to section 3(1) of the Companies Act 2013, the member of the OPC may at any time change the name of the nominee by giving notice in the event of the sole member becoming incapacitated to contract.

- 4. What are the minimum requirements towards Capital?

-

- Authorized Capital (Limit up to which company can allot shares) is prescribed as Minimum Rupees One Lakh, however, since the Stamp duty and fee for Authorised Capital up to Ten Lakhs is same, we recommend it to be kept at Ten Lakhs only

- There is no minimum Paid up capital requirement, however, atleast one share subscription each subscriber is a must, we recommend the paid up capital to be kept as One Lakh since initial expenditure and Bank account opening needs that kind of money.

- 5. Is there any concept for conversion of OPC?

-

- An OPC can be converted into Private or Public Company upon completing 2 years from the date of Incorporation unless it is a mandatory conversion.

- 6. Is there any threshold limits for an OPC to mandatorily get converted into either private or public company?

-

- In case the paid-up share capital of an OPC exceeds fifty lakh rupees or its average annual turnover of immediately preceding three consecutive financial years exceeds two crore rupees, then the OPC has to mandatorily convert itself into a private or public company within a Period of Six Months.

- 7. What is the requirement of DSC (Digital Signature Certificate)?

-

- DSC is provided in the form of token issued by Certified Authorities and is a substitute of Physical Signature and enable the owner to sign documents digitally

Company incorporation is a complete online process and all the forms required to be filed for incorporation of company are required to be signed digitally with the help of DSC of the Directors Company Sarthi helps its clients in the issuance of DSC

- 8. What is the requirement of Documents for DSC issuance?

-

- Self-attested Documents and Details required are:

- Duly filled and Signed Application Form

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Valid and active Mobile Number and e-Mail id

- On submission of above documents with the DSC Authority partner, applicant will receive the OTP on the given Mobile and e-Mail ID and thereafter applicant has to complete Mobile and Video verification.

- 9. What is the eligibility to become a Director in Company?

-

- Any natural person above the age of 18 years can become the director in the company after procuring Director Identification Number (DIN)

- There are no specific criteria provided in terms of citizenship or residency, a foreign national can also become a director.

- 10. What is Director Identification Number (DIN)?

-

- DIN is a unique number assigned by the Ministry of Corporate Affairs to Individuals on whose name the application is made, allowing that individual to become a Director in a Company or Designated Partner in an LLP

- DIN is allowed only once in lifetime and can be used to become a Director in any number of company as per eligibility criteria

- The application of DIN Allotment is now merged with the application for the formation of a company subject to a limit of maximum 3 DIN.

- 11. What is the requirement of Documents for DIN issuance?

-

Self-attested Documents and Details required are

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Valid and active Mobile Number and e-Mail id

- Proof of Identity of Applicant (Any one)

- Valid Passport

- Driving License

- Voter ID Card

- Proof of Residence of Applicant (Any one not older than 2 months having same address as that in the Proof of Identity)

- Bank Statement

- Electricity bill

- Telephone bill

- 12. How to reserve the name of the Company?

-

- Applicant has to give few choices of the name which can be checked at the Company Sarthi for the availability

- On the availability of atleast one name, Company Sarthi inform you of the same and ask you to provide two options of that name and the priority preference

- Company Sarthi also seeks from you the main objects of the company and State in which Registered office will besituated

- Although Company Sarthi follows a rigorous process of checking availability of Name, the registrar may ask to re-submit application with a different name if names applied do not fall under the criteria of uniqueness, relevancy or do not fulfill other requirements

- 13. What documents are required for registered office of Company?

-

- Business address Proof (Any one not older than 2 Months)

- Electricity Bill

- Pipe Lined Gas Bill

- Telephone Bill

- Mobile Bill

- No Objection Certificate to be obtained from the owner(s) of registered office

- Rent Agreement of the registered office should be provided if property is on rent

- 14. Does any subscriber have to be physically present for completing the process of Incorporation of the Company?

-

- No, none of the promoters are required to be physically present for completing the process of Incorporation of the Company

- All the forms are filed on the web portal and are digitally signed

- Also, the required documents can be sent through e-mail or uploaded on our portal for filing.

- 15. What are the minimum requirements for incorporation of OPC?

-

- Minimum 1 Shareholder

- Minimum 1 Director

- The director and shareholder can be same person

- Minimum 1 Nominee

- Minimum Share Capital shall be ₹ 1 Lac (INR One Lac)

- DIN (Director Identification Number) for all the Directors

- DSC (Digital Signature Certificate) for all the Directors

- 16. Who can be a nominee for a One Person Company?

-

Nominee can be anyone, such as your spouse, father, mother, daughter, brothers, sisters etc., but they should hold proper identity proofs such as PAN card, Voter id or Passport or Driving License etc., in order to be appointed as Nominees for One Person Company.

- 17. Can Foreign Direct Investment allowed for One Person Company?

-

No, FDI is not allowed for One Person Company, if it does then it will lose its very nature of One Person Company.

- 18. What are the key advantages of OPC?

-

- Lesser Compliance Burden

- Liability Limited to the value of shareholding

- Distinct identity from its owner

- Personal assets of Owner not affected

- Easy decision making

- No Statutory Requirement of holding AGM

- Compulsory Nomination

- 19. Is Auditor Appointment mandatory in case of OPC?

-

Yes, Every OPC is required to appoint the auditor in company. The power to appoint auditor lies in hand of board of directors.