Incorporation of Partnership Firm

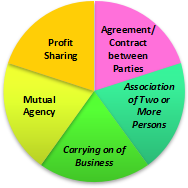

A partnership is a relationship between individuals who have agreed to share the profits of a business carried on by all or any one of them acting for all as stated in Section 4 of the Indian Partnership Act. Therefore, a partnership consists of three essential elements.

- A partnership must be a result of an agreement between two or more individuals.

- The agreement must be built to share the profits obtained from the business.

- The business must be run by all or any of them representing the rest.

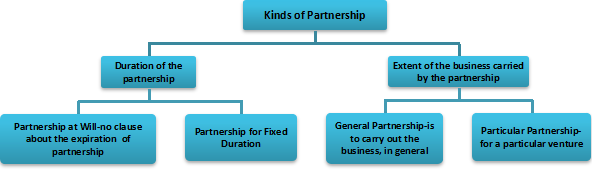

All these conditions must coexist before a partnership can come into existence. Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all. However, there can be various types of partnerships according to their duration or the intent of their creation.

Persons who have entered into partnership with one another to carry on a business are individually called “Partners“; collectively called as a “Partnership Firm”; and the name under which their business is carried on is called the “Firm Name” A partnership firm is not a separate legal entity distinct from its members.

The elements of Partnership Firm-

Partners can determine their mutual rights and duties by a contract called partnership deed, which determines aspects of general administration, such as which partner will do what work, what will be their share in profits, etc. It may be varied by express or implied consent of all the partners. All agreements restraining exercise of a lawful profession, trade or business are invalid.

Nature of Partnership Firm

Definition

A partnership is an association of individuals formed for earning profits from a business run by all or one representing the actions of all.

Relationship

Individuals forming a partnership are called partners. A partner is an agent for all the other partners.

Interest in the property

A partner has interest in the property owned by the firm. A share in a partnership is transferred only with the consent of the other partners.

Mode of creation

A partnership is created through an agreement or out of a contract.

Extent of Liability

The liability of a partner in a partnership is unlimited. This means that every partner is liable for the debts of a firm incurred during the business of the firm. These debts may be recovered the partner’s private property if the joint estate is insufficient to meet the needs entirely.

Authority to bind

By an act, a partner can bind the firm.

Governing Law

The Partnership Act governs a partnership.

Legal Status

A firm is not a legal entity. Therefore, it has no legal identity distinct from the personalities of its constituent members.

Agency

In a firm, all the partners are an agent for each other, as well as of the firm.

Distribution of Profits

The profits of a firm must be distributed among the partners according to the terms stated in the partnership deed.

Property

The firm’s property is that which is called a “Joint Estate” of all the partners. It does not belong to anybody distinct in law from its members.

Transfer of Shares

A share in a partnership can’t be transferred to another individual or partner without the consent of all the partners

Management

If there is no express agreement formed to the contrary, all the partners of the firm are entitled to participate in the control.

Number of membership

For firms running a business other than banking, the number must not exceed 20. For banks, such a number must not exceed 10.

Duration of existence

If no contracts are existing to the contrary, death, retirement or an insolvency of a partner that results in the dissolution of a firm.

Audit

The audit of the accounts of a firm is not compulsory.

Dissolution

A change in the partners of a firm would affect its existence.

Death of a member

Death of a partner in the firm would lead to the dissolution of the partnership.

Calling for accounts on the closure

A partner can file a suit against the firm for matters related to accounts, provided he also seeks for the dissolution of the firm.

Minor’s capacity

A minor cannot be a part of a partnership. Although, a minor can be admitted to the benefits of the partnership based on the consent of all the partners.

Continuity

A firm gets dissolved by the death or insolvency of a partner subject to a contract between the partners.

Types of Partners

Active Partner/Managing Partner/Ostensible Partner - Partner-active participation for running the business. Acts as an agent of all the other partners & must give a public notice when he/she wishes to retire

Dormant/Sleeping Partner - he does not take an active part in the daily activities but bound by the action of all the other partners.

Nominal Partner - capital contributions & no share in the profits but liable to outsiders /third parties for acts done by any other partners.

Partner by Estoppel - even though such a person is not a partner he has represented himself as such, and so he becomes partner by estoppel or partner by holding out

Partner in Profits Only - only share the profits of the firm, he/she will not be liable for any liabilities

Minor Partner - a partner can be admitted to the benefits of a partnership if all partners gives their consent for the same. He will share profits of the firm but his liability for the losses will be limited to his share in the firm. The minor after attaining 18 years of age within 6 months must then declare his decision via a public notice.

Duties of Partners

General duties

- carrying on the business to the greatest common good

- duty to be just and faithful towards each other

- rendering true accounts, and providing full information of all things affecting the firm. etc

Duty to indemnify for fraud

- Any partner who commits fraud must indemnify other partners for his actions.

- The Act has adopted this principle because the firm is liable for wrongful acts of partners.

- He is liable to indemnify others if his willful neglect causes losses to the firm.

Duty to act diligently

- Every partner must attend to his duties towards the firm as diligently.

Duty to use the firm’s property properly

- Partners can use the firm’s property exclusively for its business, and not for any personal purpose, because they all own it collectively. Hence, they must be careful while using these properties.

Duty to not earn personal profits or to compete

- Each partner must function according to commonly shared goals.

- They should not make any personal profit and must not engage in any competing business venture.

- They should hand over personal profits made to their firm.

Advantages of Partnership

Disadvantages of Partnership

Unlimited Liability

Restriction on Transfer of Interest

Inadequacy of Capital

Mutual Conflicts

Uncertain Continuity

Delay in Decision Making

Risk of Implied Authority

Lack of Public Confidence

Aversion to Risk

Limited Scope for Expansion

Continuation of Responsibilities

No Independent Legal Status

Suitability for Partnership Firms

Partnership form of business might be more suitable for small and medium sized businesses.

- In case of businesses where the capital requirement is medium i.e. it is neither too large nor too small. Business like retail and wholesale trade or small manufacturing units can be successfully started by partners.

- Businesses that need different ability, managerial talent, skill and expertise are best run in Partnership mode. For example, businesses such as Construction, Legal firms etc. prefer Partnerships where each partner contributes the best as per his specialization

- Family Businesses are best organized as partnerships wherein Husband and Wife, Parents and Children, Brothers and Sisters can become partners of a firm but they should also have partnership deed.

- Businesses requiring flexibility of operations, wishing to avoid elaborate compliance requirements will prefer Partnership form of business

Partnership Firms registration procedure under Indian Partnership Act

Indian Partnership Act, 1932 governs the partnerships. Registration of partnership firm is optional and at the discretion of the partners. Registration of partnership firm may be done at any time – before starting a business or anytime during the continuation of partnership. It is always advisable to register the firm since registered firms enjoy special rights which aren’t available to the unregistered firms. An application form along with fees is to be submitted to Registrar of Firms of the State in which firm is situated. The application has to be signed by all partners or their agents.

Documents to be submitted to Registrar are-

- Application for registration of partnership (Form 1)

- Specimen of Affidavit

- Certified original copy of Partnership Deed

- Proof of principal place of business (ownership documents or rental/lease agreement)

- Documents of Firm-PAN card of firm,Address proof of firm

- Documents of Partners-PAN card of partners,Address proof of partners

- Additional Documents in case of Registration

- GST Registration

- Current Bank Account

If the registrar is satisfied with the documents, he will register the firm in Register of Firms and issue Certificate of Registration.

Register of Firms contains up-to-date information on all firms and can be viewed by anybody upon payment of certain fees.

Name of the Partnership firm

- The name shouldn’t be too similar or identical to an existing firm doing the same business,

- The name shouldn’t contain words like emperor, crown, empress, empire or any other words which show sanction or approval of the government

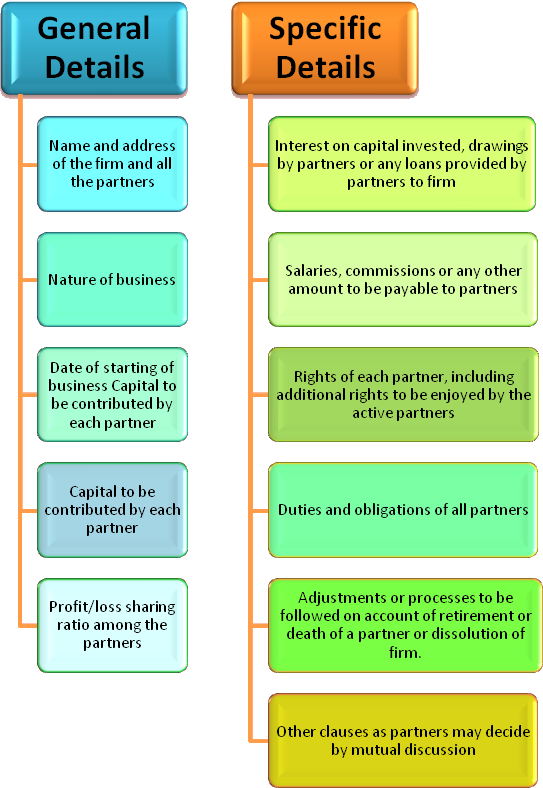

Partnership deed

Partnership deed is an agreement between the partners in which rights, duties, profits shares and other obligations of each partner is mentioned.

Partnership deed can be written or oral, although it is always advisable to write a partnership deed to avoid any conflicts in the future.

details are required in a partnership deed:

Documents of Partners

- PAN card of partners - All partners are required to submit their PAN number as identity proof.

- Address proof of partners - Partners can submit Aadhaar Card, Driving License, passport or Voter ID card as address proof. Name and other details on address proof should match PAN card details

Documents of Firm

- PAN card of firm – Partners need to apply for PAN of the firm. Form 49A has to be filed to apply for a PAN. It should be filled online by visiting https://www.onlineservices.nsdl.com/paam/endUserRegisterContact.html

- It can be filed online if the authorized partner signs the application using a digital signature certificate. Else, the application and requisite documents have to be sent to the nearest PAN processing centers available across the country

- Address Proof of firm – If the registered office place is rented, rent agreement and one utility bill (electricity bill, water bill, property tax bill, gas receipt etc.) have to be submitted. Also, NOC from landlord will be submitted.

If the registered office place is own, utility bill has to be submitted mentioning the name of the owner. Also, a NOC from the owner (owner as mentioned in utility bill) has to be submitted.

Additional Documents in case of Registration

In case partners wish to register the partnership firm, they need to submit partnership deed, ID and address proofs of the firm as well as the partners to the Registrar of Partnerships. With it, an affidavit is also required to be submitted certifying that all the details mentioned in deed and documents are correct.

GST Registration

For obtaining a GST registration, a firm needs to submit PAN number, address proof and identity & address proofs of partner. Authorized signatory will sign the application either using a digital signature certificate or E-Aadhaar verification.

Current Bank Account

For opening a current bank account, a firm needs to submit following documents :

- Partnership deed

- Partnership firm PAN card

- Address Proof of the partnership firm

- Identity proofs of all the partners, Partners KYC, Mobile No. & Mail ID, Passport size photo of Partners,Partnership Firm address proof

- Copy of resolution for bank account opening

- Partnership registration certificate (if partnership has been registered)

- Any registration document issued by central or state government (normally GST certificate is submitted)

- Copy of electricity bill, telephone bill or water bill (not more than 3 months old)

- Authorization letter on the letterhead of the firm authorizing a partner as authorized signatory for the bank account.

Benefits of partnership deed registration

Post Registration Compliances for Partnership Firm

File Partnership Agreement to ROF

- Partnership firm get registered when Firm deed get executed between partners. There are two type of Partnership firm , one is registered Firm and second is unregistered firm. Key difference between registered and unregistered firm is submission of firm deed to Registrar of Firm (ROF).

Apply PAN & TAN of Partnership Firm

- Every Partnership firm need to apply for PAN & TAN after partnership registration. Procedure to apply PAN & TAN of firm is online and manual. On behalf of firm partner shall make application to NDSL department. Along with PAN & TAN Application , firm need to submit photo copy of Partnership Deed. PAN Number is important for Partnership firm annual Tax return filing , GST Registration etc.

Partnership Firm stationery

- Partnership Firm Seal with Name of firm and Firm Name with Partner. This Stamp/seal is required post Partnership registration for bank account opening, affix on legal documents , agreements etc.

- Partnership Firm stationery like letterhead, invoice, official documents, etc., with the Partnership Firm name and registered office of the Partnership Firm.

Deposit Partners Capital

- Post Partnership Firm registration, compliance is partners shall deposit there monetary contribution in Firm. At time of registration of firm, partners decide about capital contribution to start firm. For keeping such capital contribution transactions transparent between partners, should deposit from their personal saving account via electronic / cheque transfer. Capital deposited in firm get recorded in firms annual balance sheet.

Bookkeeping of Partnership Firm

- For Annual Partnership Firm compliances & Income Tax Return filing, Firm need to maintain books of account. As per Income Tax Act firm can choose to maintain accounting in cash / accrual basis. Firm can maintain books of account manually or in computerized software. Some Common types of books of account of Partnership Firm are as -Cash book

Apply Shop Act Registration

- Business need to have Shop Act license Registration it is a primary proof of existence of business which is also known as Gumastadhara. Shop means a premises where goods or services or both are sold which includes offices, store room, warehouse. No child labor is allowed to work. Hence as per state Government Law its mandatory compliance to apply for Shop Act Registration of firm which may vary from state to state. Partnership Firm having different office within state or out of state firm shall apply separate shop Act registration

MSME Registration

- MSME stands for Micro, Small and Medium Enterprises -MSME development Act for SME benefits. In a developing country like India, MSME industries are the backbone of the economy. Where Partnership firm Apply for any bank loan, MSME registration certificate helps to get bank loan at reduced rate. Even for filing government tenders MSME registration is required.

Professional Tax Registration

- Professional Tax is registration is payment of tax to state government. Partnership firm when hire employees it comes in relation of employer and employee. Under professional tax every firm need to apply for registration as per state government rules and regulation and make timely payment of taxes. If Firm having branches in different states then, this registration need to be applied state wise.

GST Registration

- Every business with annual turnover exceeds ₹ 40 lakhs for manufactures & ₹20 lakhs turnover in case of Service providers is required to GST Registration under Goods and Services Tax (GST). However this registration can be applied suo moto. Where Partnership firm finds that post registration, GST Registration is important for business then can apply for GST registration. For some businesses like Export-Import, E-commerce, and Market Place Aggregator, GST registration is mandatory.

Intellectual Properties

- Business need to get protected them self for brand, product, formula etc. Due to dynamic and aggressive businesses new startups always have risk of losing brand etc. Partnership firm who created it brand, product etc. need to get protection via IP registration. It helps in IP protection and help to business expansion.

Copyrights

- In Case You Want to work of Writing, Artistic, Literature take Copyright Registration.Copyright means a legal right of an author/artist/originator to commercially exploit his original work which has been expressed in a tangible form and prevents such work from being copied or reproduced without his/their consent. The duration of copyright is the lifetime of the author or artist, and 60 years counted from the year following the death of the author/artist/originator.

Patents

- Patent is a monopoly given to the inventor on his invention to commercial use and exploit that invention in the market. In India, the term of the patent is for 20 years. The patent is renewed every year from the date of patent.

Trade Mark Registration

- In Case You Want that no one can use your business Name take Trademark Registration. Trademarks means any words, symbols, logos, slogans, product packaging or design that identify the goods or services from a particular source.If a person is using a similar mark for similar or related goods or services or is using a well-known mark, the other person can file a suit against that person for violation of the IP rights irrespective of the fact that the trademark is registered or not.

Partnership Firm Income Tax Return Filing

- Section 139(1) of Income Tax Act 1961 is applicable for Partnership Firm. Under income tax financial year start from April and ends at March. Annual Income tax filing compliance for Partnership firm is applicable irrespective of its turnover. In annual tax return filing firm submits its annual financial transaction information to Tax department. On basis of these transactions firm pay Income Tax.

- Regular Partnership Firm ITR filing Due date 31 July

- Firm Under audit ITR Filing Due date 30 Sept

Annual Compliances for Partnership Firm

Income Tax Filing

- A Partnership firm needs to file ITR irrespective of the revenue or loss. For partnership firm, the rate of income tax on the whole of the total income will be 30% surcharge on income tax.

Tax Audit

- Partnership Firms having an annual turnover of over ₹ 100 lakhs are required to obtain a tax audit.

TDS Filing

- Partnership firms are also required to file quarterly TDS returns that have TAN and are required to deduct tax at source as per TDS rules.

GST Filing

- GST registration is required for businesses whose annual turnover exceeds ₹ 40 lakhs ( ₹ 20 lakhs for North Eastern states). For some businesses like Export-Import, E-commerce, and Market Place Aggregator, GST registration is mandatory.

- After GST registration firms have to file monthly, quarterly and annual GST returns.

ESI Return

- For all the partnership firms having ESI registration, it is mandatory for them to file ESI return.

Documents Required for Annual Compliance of a Partnership Firm

Invoices of sales and purchase during a financial year.

Invoices of expenses made during a financial year.

Bank statements of the bank accounts of the partners.

Copy of TDS returns filed.

Copy of GST returns filed.

Conclusion

In India, partnerships are governed by the Indian Partnership Act 1932 (the Act). Limited liability partnerships (LLPs) are governed by the Limited Liability Partnership Act 2008 (the LLP Act). In an LLP, the partners have limited liability, whereas in a partnership the liability of the partners is unlimited. There is no overlap between the provisions of the Act and the LLP Act.

An LLP is a separate legal entity distinct from its partners, and all partners in an LLP have limited liability, such as in the case of a company.

While a partnership firm is a body of persons, an LLP is a body corporate.

Partnerships are preferable as they are easy to set up, not requiring formalities or elaborate paperwork. Further, they provide flexibility as the terms and conditions can be easily amended, subject to the consent of the partners.

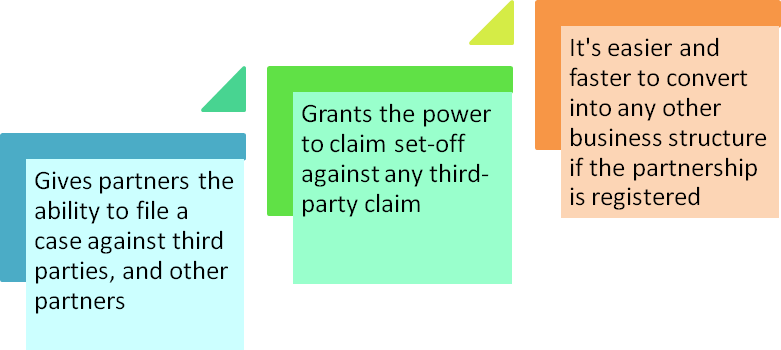

Further, with the advent of the LLP Act, LLPs have become a more popular form of structure owing to the advantage of being separate legal entities with the liability of the partners limited to the extent of capital contributed by them. LLPs have a more regulated framework with all the filings to be made online with the Ministry of Corporate Affairs (MCA), which can be viewed by the public when required.

The biggest drawback for partnerships is that the liability of the partners is unlimited; however, this was addressed with the advent of the LLP Act, with LLPs now being the preferred structure for the Indian partners. However, from a foreign direct investment (FDI) perspective, FDI is only permitted if the LLP is engaged in an activity in which 100 % foreign investment is permitted through the automatic route (that is, where prior approval from the government is not required) and there are no foreign investment-related performance conditions.

Partnership Firms are easy to start, raising funds for these firms is easy, and they have minimal compliance requirements. Apart from the benefits, these firms do have some disadvantages as well as they have limited access to capital; the business has no independent legal status, unlimited liability etc. However, the number of advantages surely outweighs the disadvantages. Since partnership firms have minimal compliance requirements, are easy to set up and come with extra managerial support; therefore, business partnerships will be beneficial for you if you are looking forward to starting a new business.

Frequently Asked Questions

- 1. What are the minimum requirements to register Partnership Firm?

-

- Minimum 2 Partners are required to start a partnership firm

- A place of business in India must be provided as a registered office address

- 2. What are the minimum requirements towards Capital?

-

For Partnership Firm in India, there is no minimum capital requirement, unlike Private Limited Company. You just need capital to maintain a current bank account balance.

- 3. What are Documents required for Partnership Firm Registration?

-

Partnership firm registration is not mandatory in India .However if partner’s wishes to register its firm then the following documents are required:-

- Partnership Firm registration application in Form 1

- Passport size photo of all the partners

- Certified Copy of notarized Partnership Deed on stamp paper

- Specimen of Affidavit

- Ownership documents in case property are owned.

- If the property is on rent then rental agreement as a proof of principal place of Business.

- ID Proof and address proof of all the partners (PAN/ Aadhar Card)

- 4. How are partnerships taxed?

-

A partnership firm and an LLP are taxed at a flat rate of 30 % (excluding applicable surcharge and cess (tax levied for a specific purpose)) on their income. Thereafter, the share of profit that a partner takes out from the partnership firm or an LLP is exempt in the hands of the partner (including the partners based overseas, subject to double taxation avoidance agreements). The income (other than profits) earned by a partner is assessed and taxed as if the partner is self-employed and not an employee of an organization.

- 5. To what extent must partnerships, LLPs and similar structures file accounts and other documents and information with a government agency?

-

The Income Tax Act 1961 provides that partnership firms and LLPs involved in a profession with gross receipts of more than ₹50lakhs and those involved in doing business and having sales turnover exceeding ₹100lakhs are required to have a tax audit. The details of the partners of a registered partnership firm and an LLP are available for the public to inspect.

- 6. What are the benefits of Partnership Firm Registration?

-

The benefits of registering a partnership firm are as follows :

- the firm can file a suit against a third party;

- a partner can file a suit against other partners of the firm

- the firm can file a suit against any partner; and

- a partner can file a suit to enforce against the firm a right arising from the contract or conferred by the Act.

- 7. What are the disqualifications of Partnership firms?

-

Any individual or body corporate can become a partner provided that the individual has:

- not been found to be of unsound mind by a court of competent jurisdiction and the finding is in force;

- not been declared an undischarged bankrupt; or

- not applied to be adjudicated as an insolvent and his or her application is pending.

Further, a foreign entity can be a partner in an LLP and make an investment only in sectors where 100% FDI is allowed in terms of the extent FDI policy

- 8. How partnership firms are voluntarily dissolved?

-

In terms of the Act, a partnership firm may be dissolved with the consent of all the partners or in accordance with the contract between the partners. In terms of the LLP Act, an LLP shall be dissolved as contractually agreed by the partners.

- 9. Can partners sue for loss caused by another partner?

-

The partners are the agents of the firm. Hence, the partnerships can sue a partner for any loss incurred due to willful neglect or fraud of the partner and they are required to indemnify the partnerships.

In terms of the Act, the partners are jointly and severally liable for all acts of the firm. In terms of the LLP Act, if a partner has acted fraudulently without the knowledge of the LLP, then, without prejudice to any criminal proceedings that may arise under any law for the time being in force, the LLP and any such partner or designated partner is liable to pay compensation to any person (including the partners of the LLP) who has suffered any loss or damage by reason of such conduct.

- 10. How much time does it take to register a partnership?

-

The time taken to issue a certificate of incorporation may vary as per the regulations of the concerned state. The registration of Partnership Firm is subject to Government processing time which varies for each State.

- 11. Are there any grounds on which partnership can be invalid?

-

Often, if the partnership agreement is not registered, the court may deem a partnership invalid. If the object of the business is illegal, the court may consider the partnership invalid and dissolve the partnership.

- 12. If all partners wish to end the partnership, how can they do so?

-

If the partners of a firm wish to end the partnership, they can do so by dissolving the partnership by notice, if it is a partnership of will. A partnership can be dissolved in accordance with the terms laid out in the Partnership Deed, or they can do so creating a separate agreement.

- 13. Can the certificate of registration be cancelled?

-

In a certain sense, a partnership certification of incorporation can be revoked, this often termed as dissolution. Dissolution can be brought upon automatically when all partners or all partners except one partner are declared insolvent or if the firm is carrying unlawful activities, i.e. like trading in drugs or other illegal products, corporate malpractice or making business engagements with countries that may harm the interest of India.

- 14. What is the scope of liability when it comes to partnerships?

-

Every partner is jointly liable with all the other partners and also individually, for all acts/activities of the firm, during the course of business while he/she is a partner. This means that if a loss or injury is caused to any third party or a penalty is levied during the course of business all partners will be held liable even if the injury or loss was caused by one of the partners.