Incorporation of a Public Limited Company

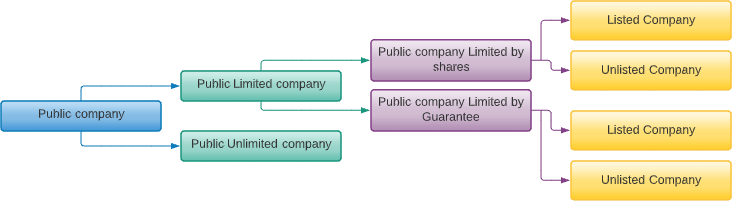

As per Companies Act 2013, a Public Limited Company is a company that has limited liability and may offer shares to the general public by Initial Public Offer (IPO). Where the company is listed, an individual can also acquire the shares of such company via stock market. A Public Limited Company has stringent regulatory requirements and has no exemption allowed under the Companies Act 2013. A private company which is Subsidiary of a Public company shall also be deemed to be Public Company.

A Public Company must have at least seven shareholder and minimum three directors. There is not limit for maximum shareholder in a public company.

Its shares are freely transferable and that too without the prior consent of other shareholders. It is independent legal person; its existence is not affected by the death, retirement or insolvency of any of its shareholders. These companies can invite capital and deposits from the public. These Companies can be listed or unlisted.

A public company can only be listed on stock exchanges and can issue securities to general public through an initial public offering (IPO). Shares of only public company can be traded on stock exchanges. Public companies are subject to higher levels of reporting, regulations, and public scrutiny. A listed Public company must meet stringent reporting requirements set out by Securities and Exchange Board of India (SEBI).

The Company Incorporation rules, requirements, process, and procedures vary more or less depending particularly on the type of company to be incorporated.

Characteristics of Public Limited Company

- Paid-up Capital: Minimum paid-up capital of Rs.5,00,000/-, but now no mandatory obligation for limit

- No. of Members: Minimum 7 members, no maximum limit

- Name of Company: Name must end in "Public limited"

- No. of Directors: Minimum 3 directors, and if listed company one-third must be independent

- Managerial Remuneration: Restricted to 11% of the Net profit of the company

- Quorum of Meetings: Quorum will depend on the total number of members of the company

- Public Offer: Public offers must be in the demat form only It can bring initial Public offer(IPO) to raise funds and can become the listed company

- Accepting Deposits: If paid capital exceeds 100 crores, or turnover exceeds 500 crores, the company can accept public deposits

- Compliance Requirement: Public company shall comply with all most all provisions of companies Act as this type of company is for large business with public interest

- Transfer of Shares: Shares of a public company is freely transferable. Board of directors cannot impose restrictions on share transfer.

- Issue of Shares: A public company can issue shares subject to regulation of SEBI and other compliance requirements.

Minimum Requirements for Public Limited Company

- Minimum seven shareholders;

- Minimum three Directors (Directors and shareholders can be same person);

- At least one Director shall be resident in India;

- No Minimum capital required for public limited company incorporation in India. Earlier, it was ₹5 lakh, however to provide ease of doing business in India, the requirement of minimum capital for Public company is withdrawn;

- Income-tax PAN is a mandatory requirement in case of Indian nationals;

- Any one of the Identity Proof (Voter ID /Aadhaar Card/Driving License/Passport); Passport is mandatory requirement for proof of identity in case of foreign nationals;

- Any one Proof of Residence (Electricity Bill/Telephone Bill/Mobile Bill/Bank Statement);

- Registered Office address proof (rent agreement along with latest rent receipt and copy of latest utility bill in the name of landlord and a no objection certificate from the owner of the premises, in case the premises are rented);

- In case the premises are owned by a Director and Promoters, any documents establishing the ownership such as Sale Deed/House Tax receipt etc along with the no objection certificate.

Features of Public Limited Company

Limited Liability

Shareholders of the company are not liable to pay any amount over and above the unpaid amount on shares hold by them at the time of liquidation.

Directors

A Public Limited company shall have a minimum of 3 directors. Further, a company can have a maximum number of 15 directors. However, through a special resolution a company may appoint more than the prescribed limit.

Paid up capital

A public limited company shall have a minimum paid-up capital of ₹5 Lacs or such higher amount as may be prescribed under the act. However, there is no prescribed limit for maximum capital amount.

Name

As per Companies Act 2013, any company which has registered as Public Ltd. A company is required to add the word limited after their name. For example XYZ Limited.

Prospectus

A prospectus means any documents including red-herring and shelf prospectus or any notices, circular, advertisement, or other documents that are issued by the company for inviting offer from the public for the subscription of shares or debentures.

Criteria for Public Limited Company Registration

Minimum Seven People: Minimum seven people are required to start the public limited company in India. These companies shall have minimum three directors. The same seven people can become shareholder and director of the company. However, maximum any number of people can become shareholder in the public limited company.

No Minimum Capital: Capital of the business is depending on the need of the business and statutory no minimum capital is required to start the public limited company. However, minimum authorized and subscribed share capital required for public company is Rupees five lakh.

One Resident Director: Among director, one person must be resident Indian.

Unique Name: The name of the public limited company should be unique and should not be similar to the any existing company name or trademark.

Disadvantages of Public Limited Company

High Compliance cost, high cose of registration and maintenance is high

Stringent penalties on any non compliance

More compliances applicable than any other form of business

Benefits of Public limited company

Separate Legal Entity

Capacity to Sue and to be Sued

Easy Transferability of Shares

Perpetual Succession

Larger Borrowing Capacity

Ownership of Property

Increase in Attraction Rate of mutual funds owner and other stock traders

More Development Opportunities

Spreading risk

Larger amount of capital

Efficient management

Limited Liability of shareholder

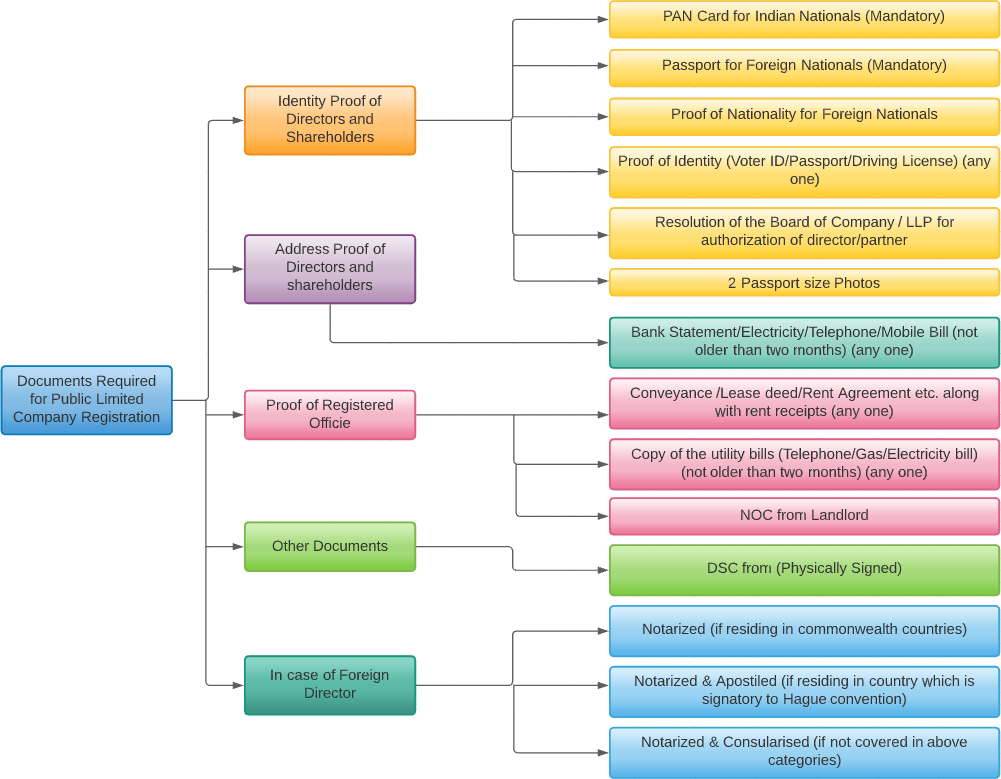

Documents Required for Public Limited Company Registration

Public Company Incorporation Process

Obtain DSC in electronic Format from Government Recognized Certifying Agencies for the directors and shareholder of the company, who is required to sign the e-form for registration before filing incorporation application for th company. Photo, ID and Address Proof is required along with DSC application form for issuance of DSC.

Obtain Director Identification Number(DIN) issued by ROC by applying for DIN-(in Form DIN 3 in existing company or directly with SPICe INC 32 upto 3 directors) An application is filed along with ID and address proof duly attested by CS/CMA/CA.

Obtain Name Approval Certificate in RUN Form(Reserve Unique Name) or directly apply with SPICe INC 32 -in both cases 2 chances are given with one Resubmission (RSUB) The proposed name selected should do not contain any word which is prohibited under Companies Act, 2013. An approved name by CRC is valid for a period of 20 days.

The Registrar of companies may require the applicant to furnish the Approval of other authorities of any department, regulatory body, appropriate authority, or Ministry of the Central or State Government(s) in relation to the work to be done.

Obtaining approval from FIPB (Foreign Investment Promotion Board), if required : If the activities of the indian wholly owned subsidiary fall under Government approval route, then the approval from FIPB has to be obtained.

Current Bank Account to be Opened in Company's Name & Issue of Prospectus and Declaration of Commencement of Business in Form 20A.

Get the Certificate of Incorporation - (COI) issued by ROC with the PAN & TAN - Application for Goods and Services Tax Identification Number(GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration(AGILE-PRO) in Form INC 35

To get the Company Identification Number-(CIN) address for the Registered Office and NOC from the landlord is required & Apply for PAN ad TAN with SPICe INC 32.

Enlist the company's constitution in Memorandum of Association(MOA) in e-(MOA) and Articles of Association (AOA) in e-(AOA) directly with SPICe INC 32. application for registration/incorporation of public limited company is made to registrar of companies(ROC) along memorandum and Articles of Association, declarations, affidavits etc. Minimum seven persons are required for incorporation of public limited company.

Enlist the company's constitution in Memorandum of Association(MOA) in e-(MOA) and Articles of Association (AOA) in e-(AOA) directly with SPICe INC 32. application for registration/incorporation of public limited company is made to registrar of companies(ROC) along memorandum and Articles of Association, declarations, affidavits etc. Minimum seven persons are required for incorporation of public limited company.

To get the Company Identification Number-(CIN) address for the Registered Office and NOC from the landlord is required & Apply for PAN ad TAN with SPICe INC 32.

Get the Certificate of Incorporation - (COI) issued by ROC with the PAN & TAN - Application for Goods and Services Tax Identification Number(GSTIN), Employees State Insurance Corporation Registration(ESIC) plus Employees Provident Fund Organization(EPFO) registration(AGILE-PRO) in Form INC 35

Current Bank Account to be Opened in Company's Name & Issue of Prospectus and Declaration of Commencement of Business in Form 20A.

Issue of Prospectus

Every Public Company is under obligation to issue prospectus either after formation of the company or in case of existing company. A prospectus means any documents including red-herring and shelf prospectus or any notices, circular, advertisement, or other documents that are issued by the company for inviting offer from the public for the subscription of shares or debentures. The rules and penal provisions with regards to issue of prospectus are very strict in nature. A prospectus must include the following information as per sec 26 of the Companies Act, 2013-

- Names and addresses of the Registered Office of the Company, Company Secretary, Chief Financial Officer, auditors, legal advisers, bankers, trustees, if any, underwriters and such other persons as may be prescribed;

- dates of the opening and closing of the issue, and declaration about the issue of allotment letters and refunds within the prescribed time;

- a statement by the Board of Directors about the separate bank account where all monies received out of the issue are to be transferred and disclosure of details of all monies including utilized and unutilized monies out of the previous issue in the prescribed manner;

- details about underwriting of the issue;

- consent of the directors, auditors, bankers to the issue, expert’s opinion, if any, and of such other persons, as may be prescribed;

- the authority for the issue and the details of the resolution passed;

- procedure and time schedule for allotment and issue of securities;

- capital structure of the company in the prescribed manner;

- main objects of public offer, terms of the present issue and such other particulars as may be prescribed;

- main objects and present business of the company and its location, schedule of implementation of the project;

- particulars relating to—

- minimum subscription, amount payable by way of premium, issue of shares otherwise than on cash;

- details of directors including their appointments and remuneration, and such particulars of the nature and extent of their interests in the company as may be prescribed; and

- disclosures in such manner as may be prescribed about sources of promoter’s contribution.

(a). Management perception of risk factors specific to the project;

(b). Gestation period of the project;

(c). Extent of progress made in the project;

(d). Deadlines for completion of the project; and

(e). any litigation or legal action pending or taken by a Government Department or a statutory body during the last five years immediately preceding the year of the issue of prospectus against the promoter of the company;

Post Incorporation Procedures of Public Limited Company

First Board Meeting

- A company shall within 30 days from the date of incorporation conduct first board meeting of the company.

- Directors can attend the meeting either in person or through video conferencing.

- Disclosures of interest by Board of Directors in form MBP-1 and declarations in form DIR-8.

Deposit of Share Capital Money

Once bank account is opened, the next compliance is of depositing the share capital money in the bank account within 60 days from the date of incorporation of the company.

Issue of Share Certificates and payment of stamp duty

The Public Limited Company shall issue share certificates to the shareholders of the company within 60 days from the date of incorporation of the company and pay stamp duty within 30 days from the date of allotment of shares as per the relevant stamp act applicable on the state.

Registered Address

As per Section 12(1) of the Companies Act, 2013 a company should have its registered office within 15 days from the date of incorporation of the company. This address should be used for all types of future communications from various authorities.

Appointment of Auditors

As per Section 139 of the Companies Act, 2013 every company is required to appoint its first auditor within 30 days of incorporation by its board of directors and in case the board of directors fails to appoint the auditor within said period of 30 days then they shall call an extraordinary general meeting of shareholders for appointing an auditor. The appointment of auditor through shareholder must be completed within 90 days.

Affixing Sign

- Once the Public Limited Company is registered, then its required to affix its name board at every place from where it is carrying on business all over india.

- Company need to affix name board at office premises.

Printing of letter heads

- Section 12 mandate a company to print the following information on all its Business Letterhead/Billheads/Letter Papers etc.

- Name of the Company

- Address of Registered Office

- CIN Number

- Telephone Number

- Fax (if any)

- E-mail ID

- Website Address

Disclosure of Interest

- At first board meeting, every director is under obligation to disclose his interest in any company/firm/body corporate/association of individuals as outlined in section 184(1) of the Companies Act 2013. Any changes in the disclosures shall be intimated by the director to Board of Directors in its first meeting held during each financial year. An independent director, if any, must give a declaration that he meets the criteria of independence during the first board meeting as a director.

Maintenance of Statutory Registers

It is mandatory as a post incorportion compliance for Public Limited Company to maintain statutory registers like :

- MGT-1 : Register of Members

- MGT-2 : Register of Debenture holders Register and index of Beneficial Owner

- MGT-3 : Foreign Register of Members, Debenture holders, other security holders or beneficial owners residing outside india

- Form SH-2 : Register of Renewed and Duplicate Share Certificate

- Form SH-3 : Register of Sweat Equity Shares

- Form SH-6 : Register or Employee Stock Options.

- Form SH-10 : Register of Shares or Securities Bought Back Register of Directors and KMPs Register of Deposits

- Form CHG-7 : Register of Charges

- Form MBP-2 : Register of Loans/Guarantee/Security and Acquisition by Company

- Form MBP-3 : Register of Investments not held in its own name

- Form MBP-4 : Register of contacts or Arrangments in which Directors are interested.

Declaration of Commencement of Business

As a post incorporation requirements Public Limited company required to file a declaration of commencement of business within 180 days from the date of incorporation of the company in accordance with the Companies (Amendment) Ordinance 2018, Section 10A, in form INC-20A.

Books of Accounts

As per section 128, every Public Limited Company post registration company shall maintain proper books of accounts which shall represent true and fair view of the financial disclosure of the company.

Obtain Shop Act Registration

As a post Incorporation Compliance for Public Limited Company, the next important step is obtaining shop act license immediately. shop Act Registration The basic documents for obtaining shop act license is MOA,AOA,COI, Directors KYC documents etc.

Obtaining GST Certificate

Every business with annual turnover exceeds ₹ 40 lakhs or Service Providers ₹ 20 lakhs is required to GST Registration under Goods and Services Tax(GST). However Public Company can apply GST Registration suomoto. In most of cases where company dealing with MNC companies they demand GST registration number. As a business need, Company can apply for GST Registration in AGILE-PRO itself at the time of incorporation.

Professional Tax Registration

It is mandatory obtain Professional Tax Registration to company and all directors, and employees. However, all Union Territories including NCT of Delhi and certain states like Haryana, Punjab, Rajasthan, Uttar Pradesh etc. does not have any law to tax professional.

Trade Mark Registration

To protect trade name, Public limited company post registration can apply for Trade Mark Registration. It gives legal right to use name exclusively.

Annual Compliances of Listed Public Limited Company

| S.No | Compliance | Form No | Particulars of Compliances | Section | Due Date |

|---|---|---|---|---|---|

| 1 | Annual General Meeting | Form MGT-15 | Annual General Meeting to be conducted as per the provisions of the Act. | Section 121(1) of the Companies Act,2013 | Within thirty days from date of its incorporation. |

| 2 | Financial Statements | Form AOC-4 | Balance sheet, Director’s Report, Cash Flow Statement Auditor’s Report and the consolidated Financial Statement prepared in Extensible Business Reporting System (XBRL). | As per Section 137 of the Companies Act to be read with Rule 12(2) of the Companies (Accounts) Rules, 2014. | Within thirty days of holding the Annual General Meeting or AGM |

| 3 | Annual Return | MGT-7 | Information about the directors and shareholders is to be filed with relevant Registrar of Companies In case, the total paid-up capital of the public limited company equals to or exceeds ₹10 Crore, or its annual turnover crosses ₹ 50 Crore, then, there will arise the requirement of filing the Form MGT-8 (Certification of Annual Return) also, within Sixty days from the end of the financial year. |

According to section 92 of the Companies Act, 2013 to be read with Rule 11(1) of the Companies (Management and Administration) Rules 2014. | Within sixty days of the Annual General Meeting(AGM) |

| 4 | Financial and Director’s Report | Form MGT-14 | Adoption of Financial and Director’s Report | Section 173 read along with Secretarial Standards 1 | Within thirty days from the Board Meeting |

| 5 | Income Tax Returns | Form ITR-6 | Income Tax Returns must be filed before the Tax Department. Again, tax-audit will be compulsory if the annual turnover of the public limited company gets more than ₹1 Crore. |

On or before 30th September of the financial year | |

| 6 | Secretarial Audit Report | Form MR-3 | Submission of Secretarial Audit Report along with the Board Report when: Its total Paid- up capital is equal to or crosses ₹50 crore or Its annual turnover is equal to or exceeds ₹250 crore. | Section 204 of Companies Act, 2013 to be read with Rule 9 of The companies (Appointment and Remuneration Personnel) Rules, 2014. | Before appointment or reappointment of The Secretarial Auditors. |

| 7 | Compliances under all Rules and Regulations associated with SEBI | Includes the Listing Regulations of 2015 | Listing Regulations of 2015, SEBI | ||

| 8 | Various Annual Compliances under other Laws applicable | Such as the Labor and Employment Law, Corporate and Commercial Laws, Excise and Custom, RBI, FEMA, Intellectual Property Laws, Pollution Control Act, PF and ESI Regulations, Maritime and Admiralty Laws, etc. |

Annual Compliances for Unlisted Public Limited Company

| S.No | Compliance | Form No | Particulars of Compliances | Section | Due Date |

|---|---|---|---|---|---|

| 1 | Board Meeting | Discussions related to appointment or reappointment of auditor or any such related issues. | Section 173 of the Companies Act | At least 4 Board meeting in a year. | |

| 2 | Appointment of Cost Auditor | Form CRA-2 | Issue the Letter of Appointment to Cost Auditor and intimation to be made to Central government about its appointment. | As per Section 148(3) along with Rule 6(2) and Rule 6(3A) of the Companies (Cost Records and Audit) Rules,2014 | Original Appointment to be done within 30 days of Board Meeting or 180 days of Financial year, whichever is earlier Casual Vacancy to be filled within 30 days of Board Meeting. |

| 3 | Return of Deposits(DPT) | Form DPT-3 | The Return of Deposit should be filed before the Registrar of Companies or ROC. | As per Rule 16 of Companies (Acceptance or Deposit) Rules, 2014 | 30th June of every year. |

| 4 | Appointment of CEO or CFO or CS | Form MGT-14 & Form DIR-12 | Appointment of full time or casual CEO or CS or CFO | According to Section 203 read with Rule 8 & 8A of the Companies (Appointment and remuneration of Managerial Personnel) Rules, 2014. | Within 30 days of the Annual General Meeting and in case of casual vacancy within 6 months. |

| 5 | Annual General Meeting | Conducting Annual General Meeting for declaration of dividend. | Section 96 of the Companies Act, 2013 | The first Annual General Meeting is to be held within 9 months of the end of financial year. | |

| 6 | Special Resolution | Special Resolution passed at Annual General Meeting | Section 117 of the Companies Act, 2013 to be read with Rule 24 of the Companies (Management and Administration) Rules, 2014. | Within 30 days of passing the resolution. | |

| 7 | CSR Committee | Hold meeting and approve CSR Activities | Section 135 of the Companies Act, 2013 read with companies(Corporate Social Responsibility Policy) Rules, 2014 & SS-1 | Four Board meetings with a gap of not less than 120 days between two Board meetings. | |

| 8 | Director’s Disclosure | Form MBP-1 | Director’s need to disclose financial interest in the company. | Section 184(1) of the Companies Act, 2013 to be read along with Rule 9(1) of the Companies (Meetings of Board and its Powers) Rules, 2014. | After its appointment in first meeting. |

Conclusion

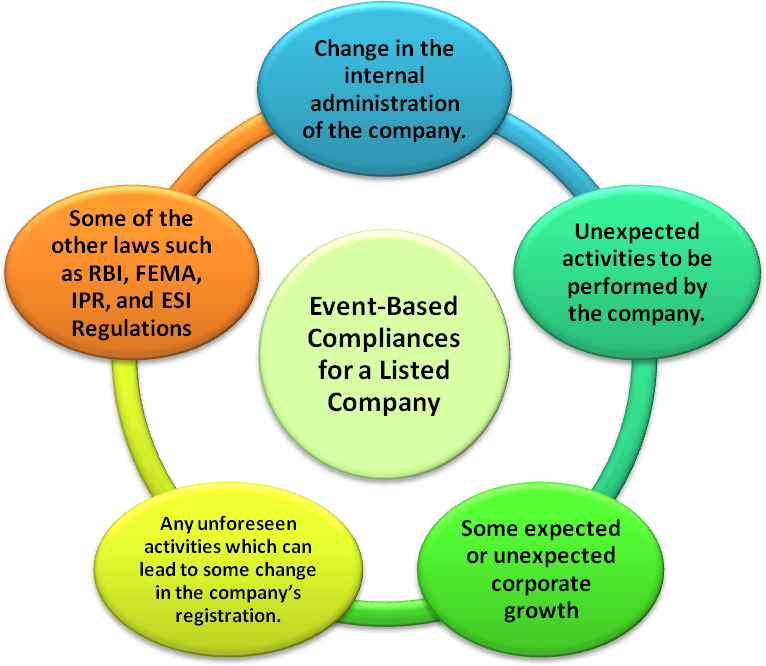

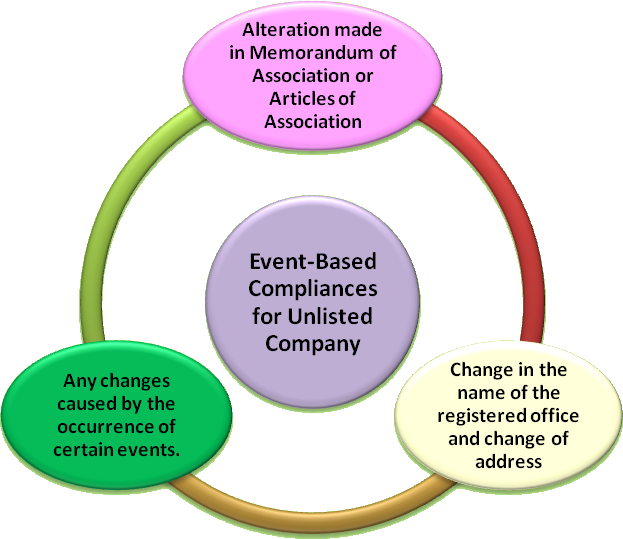

For Public Limited Company there are some post incorporation compliance and some are event based compliances. Non compliance by company may attract to fines and penalties on company and directors. It is therefore important that company and directors should be aware about post incorporation compliances. The Companies will be liable to pay a heavy fine, or additionally, the directors can face the punishment of imprisonment. These regulations bring a better structure, greater Independence, and balanced checks in the functioning of a public Limited Company.

Frequently Asked Questions

- 1. What are the minimum requirements to register a Public Limited Company?

-

- Minimum seven shareholders;

- Minimum three Directors (Directors and shareholders can be same person);

- At least one Director shall be resident in India;

- No Minimum capital required for public limited company incorporation in India. Earlier, it was ₹5 lakh, however to provide ease of doing business in India, the requirement of minimum capital for Public company is withdrawn;

- 2. What are the minimum requirements towards Capital?

-

- No Minimum capital required for public limited company incorporation in India. Earlier, it was ₹5 lakh, however to provide ease of doing business in India, the requirement of minimum capital for Public company is withdrawn.

- 3. What is the requirement of DSC (Digital Signature Certificate)?

-

- DSC is provided in the form of token issued by Certified Authorities and is a substitute of Physical Signature and enable the owner to sign documents digitally

- Company incorporation is a complete online process and all the forms required to be filed for incorporation of company are required to be signed digitally with the help of DSC of the Directors

- Company Sarthi helps its clients in the issuance of DSC

- 4. What is the requirement of Documents for DSC issuance?

-

- Self-attested Documents and Details required are

- Duly filled and Signed Application Form

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Valid and active Mobile Number and e-Mail id

- On submission of above documents with the DSC Authority partner, applicant will receive the OTP on the given Mobile and e-Mail ID and thereafter applicant has to complete Mobile and Video verification.

- 5. What is the eligibility to become a Director in Company?

-

- Any natural person above the age of 18 years can become the director in the company after procuring Director Identification Number (DIN).

- There are no specific criteria provided in terms of citizenship or residency, a foreign national can also become a director.

- 6. What is Director Identification Number (DIN)?

-

- DIN is a unique number assigned by the Ministry of Corporate Affairs to Individuals on whose name the application is made, allowing that individual to become a Director in a Company or Designated Partner in an LLP

- DIN is allowed only once in lifetime and can be used to become a Director in any number of company as per eligibility criteria

- The application of DIN Allotment is now merged with the application for the formation of a company subject to a limit of maximum 3 DIN.

- 7. What is the requirement of Documents for DIN issuance?

-

- Self-attested Documents and Details required are

- Copy of PAN Card

- Copy of Aadhaar Card

- Passport size Photograph

- Valid and active Mobile Number and e-Mail id

- Proof of Identity of Applicant (Any one)

- Valid Passport

- Driving License

- Voter ID Card

- Proof of Residence of Applicant (Any one not older than 2 months having same address as that in the Proof of Identity):

- Bank Statement

- Electricity bill

- Telephone bill

- Mobile bill

- 8. How to reserve the name of the Company?

-

- Applicant has to give few choices of the name which can be checked at the Company Sarthi for the availability

- On the availability of atleast one name, Company Sarthi inform you of the same and ask you to provide two options of that name and the priority preference

- Company Sarthi also seeks from you the main objects of the company and State in which Registered office will be situated

- Although Company Sarthi follows a rigorous process of checking availability of Name, the registrar may ask to re-submit application with a different name if names applied do not fall under the criteria of uniqueness, relevancy or do not fulfill other requirements

- 9. Does any subscriber have to be physically present for completing the process of Incorporation of the Company?

-

- No, none of the promoters are required to be physically present for completing the process of Incorporation of the Company

- All the forms are filed on the web portal and are digitally signed.

- Also, the required documents can be sent through e-mail or uploaded on our portal for filing.

- 10. What documents are required for Registered Office of Company?

-

- Business address Proof (Any one not older than 2 Months)

- Electricity Bill

- Pipe Lined Gas Bill

- Telephone Bill

- Mobile Bill

- No Objection Certificate to be obtained from the owner(s) of registered office.

- Company Sarthi also seeks from you the main objects of the company and State in which Registered office will be situated

- Rent Agreement of the registered office should be provided if property is on rent

- 11. What is the Annual Return of the Public Limited Company?

-

The annual return is filed every year along with the Balance Sheet, P&L Account and other documents. It is different from the income tax department and it’s governed by the Ministry of Corporate Affairs. Annual Return consists of the Balance Sheet, P&L account, Directors Report, Details of the Members, Details of Directors and Secretarial Certificate (if applicable) The Annual Return must be signed by two directors of the company on or before the due date i.e. 30th September of each year. Annual compliance means the requirements which have to be followed yearly in order to avoid any form of penalties.

- 12. Can the company file the Annual Return itself?

-

- No, Certification by CAs or CSs is required.

- 13. Who is the main Regulatory Authority for Annual Compliance?

-

The primary regulatory authority for Annual Compliance for a public limited company is the Ministry of Corporate Affairs and the Registrar of Companies.

- 14. What is a Listed and Unlisted Company?

-

Listed Company

- A listed Company is explained in Section 2(52) of the Companies Act, 2013.

- A listed company means a company has its securities listed on any recognized Stock Exchange.

- A listed Companies shares can be traded in the stock exchange.

- A listed Company is recognized as a Public Limited Company because it makes an Initial Public Offering or IPO to sell its shares to the public and to get capital in return.

Unlisted Company

- An unlisted Company has not been explained in the Companies Act, 2013.

- An unlisted Company can be a Public Limited Company or a Private Limited Company.

- The shares of the unlisted companies are not available for the general public.

- An unlisted Company is not listed in any stock exchange

- An unlisted Company can have an unlimited number of shareholders for raising capital for any commercial venture.