Public Private Partnerships (PPP) - Introduction

In a public-private partnership (PPP), companies and government bodies or civil society organizations work together. The partnership may be solely financial (donations and sponsorship), but may also involve a more concrete collaboration. PPP is based on two main principles:

- Both parties invest in the project. In a financial sense (manpower, materials budget) and in an expertise-related sense (knowledge, networks).

- The parties contribute to a societal and often also commercial purpose.

PPP involves a contract between a public sector and a private party, in which a government service or private business venture is funded by both the parties and executed through a partnership of public authority and private sector companies. A public- private partnership covers all types of collaborations between the public and private sectors, where public sector delivers policies, infrastructure etc. Hence, Public Private Partnership means an arrangement between a government/ statutory entity/ government owned entity on one side and a private sector entity on the other. It is often done for the provision of public assets or public services, through investments being made and/or management being undertaken by the private sector entity, for a specified period of time. There is well defined allocation of risk between the private sector and the public entity. The private entity who is chosen on the basis of open competitive bidding, receives performance linked payments that conform (or are benchmarked) to specified and pre-determined performance standards, measurable by the public entity or its representative.

- Public Ownership and operation

- Quasi public agency

- Operations assistance

- Contract operations and maintenance

- Contracts operations and financing

- Design/ Build/ Operate

- Lease and Operate

- Joint Ownership

- Private Ownership

India has systematically rolled out a PPP program for the delivery of high-priority public utilities and infrastructure and, over the last decade or so, developed what is perhaps one of the largest PPP Programs in the world. With close to 2000 PPP projects in various stages of implementation, according to the World Bank. India is one of the leading countries in terms of readiness for PPPs.

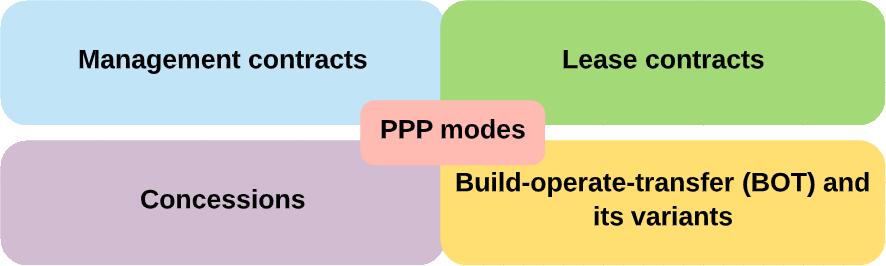

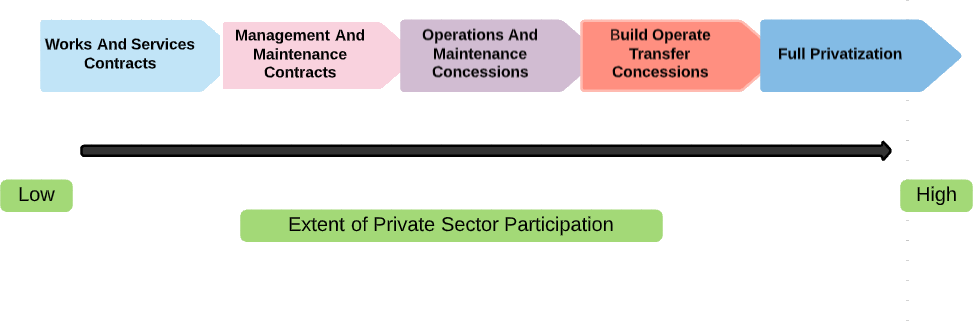

Types of PPP modesThe four major “families” of PPP modes are

PPPs have given rise to an array of acronyms for the names that describe the variations in each modal family. Different PPP modes can be compared on a spectrum ranging between low and high levels of private participation and involvement.

Brief history about public–private partnership Brief history about public–private partnership

A public–private partnership (PPP, 3P, or P3) is an arrangement between two or more public and private sectors of a long-term nature. Typically, it involves private capital financing government projects and services up-front, and then drawing profits from taxpayers and/or users over the course of the PPP contract. Public–private partnerships have been implemented in multiple countries and are primarily used for infrastructure projects. They have been used for building, equipping, operating and maintaining schools, hospitals, transport systems, and water and sewerage systems.

Cooperation between private actors, corporations and governments has existed since the inception of sovereign states, notably for the purpose of tax collection and colonization. However, contemporary "public-private partnerships" came into being around the end of the 20th century. They were associated with neoliberal policies to increase the private sector's involvement in public administration. Originally, they were seen by governments around the world as a method of financing new or refurbished public-sector assets outside their balance sheet. At the dawn of the millennium, this vision of PPPs came under heavy criticism as taxpayers or users still had to pay for those PPP projects, with high interest. PPPs initiated after 2010 are generally included in the public balance sheet.

PPPs continue to be highly controversial as funding tools, largely over concerns that public return on investment is lower than returns for the private funder. PPPs are closely related to concepts such as privatization and the contracting out of government services. The lack of a shared understanding of what a PPP is and the secrecy surrounding their financial details makes the process of evaluating whether PPPs have been successful, complex. P3 advocates highlight the sharing of risk and the development of innovation, while critics decry their higher costs and issues of accountability. Evidence of PPP performance in terms of value for money and efficiency, for example, is mixed and often unavailable.

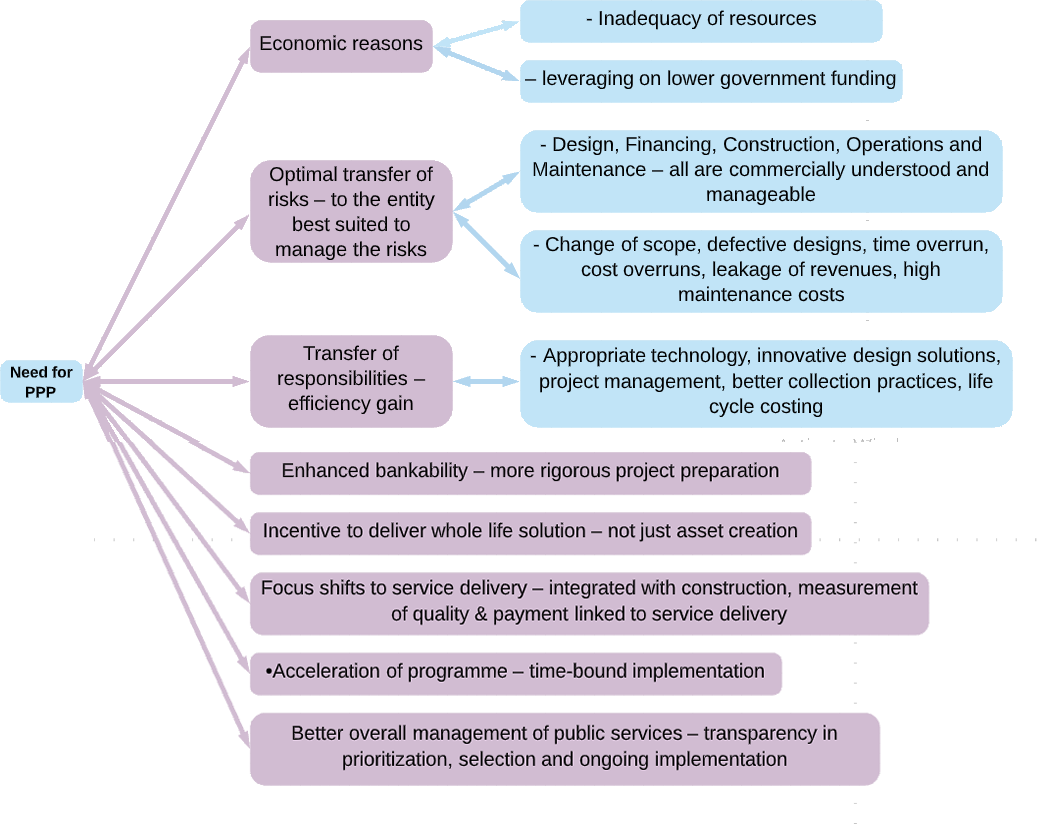

Government of India is committed to improving the level and the quality of economic and social infrastructure services across the country. In pursuance of this goal, the Government envisages a substantive role for Public Private Partnership (PPPs) as a means for harnessing private sector investment and operational efficiencies in the provision of public assets and services. India has already witnessed considerable growth in PPPs in the last one and half decade. It has emerged as one of the leading PPP markets in the world, due to several policy and institutional initiatives taken by the central as well as many state governments. Government of India has set up Public Private Partnership Appraisal Committee to streamline appraisal and approval of projects. Transparent and competitive bidding processes have been established. To provide a broader cross-sectoral fillip to PPPs, extensive support has been extended through project development funds, viability gap funding, user charge reforms, provision of long tenor financing and refinancing as well as institutional and individual capacity building. PPPs are now seen as the preferred execution mode in many sectors such as highways, ports and airports. Increasingly, PPPs are being adopted in the urban sector and in social sectors. Over the years an elaborate eco-system for PPPs has developed, including institutions, developers, financiers, equity providers, policies and procedures. The growing PPP trends, especially in the last decade, justify the need for a broad policy framework that sets out the principles for implementing a larger number of projects across diverse sectors to complement the inclusive growth aspirations of the nation. The National PPP Policy seeks to facilitate this expansion in the use of PPP approach, where appropriate, in a consistent and effective manner, through:

- Setting out the broad principles for pursuing a project on PPP basis;

- Providing a framework for identifying, structuring, awarding and managing PPP projects;

- Delineating the cross-sectoral institutional architecture and mechanisms for facilitating and implementing PPPs.

Public–private partnerships in India

The Department of Economic Affairs (DEA) defines PPPs as-PPP means an arrangement between a government or statutory entity or government owned entity on one side and a private sector entity on the other, for the provision of public assets and/ or related services for public benefit, through investments being made by and/or management undertaken by the private sector entity for a specified time period, where there is a substantial risk sharing with the private sector and the private sector receives performance linked payments that conform (or are benchmarked) to specified, pre-determined and measurable performance standards. The level of private sector participation in infrastructure can cover a spectrum from short-term service contracts at one end all the way through to full privatization (disinvestment) at the other. Service contracts and disinvestments are generally not considered as PPPs in India. An infrastructure PPP in India is therefore more than just a short-term contract for services with the private sector but does not go so far as to include complete private sector ownership and control. A PPP is an arrangement between a public (government) entity & a private (non-government) entity by which services that have traditionally been delivered by the public entity are provided by the private entity under a set of terms and conditions that are defined at the outset.Public Private Partnership (PPP) is a contract between a public sector institution/municipality and a private party, in which the private party assumes substantial financial, technical and operational risk in the design, financing, building and operation of a project.

Traditionally, private sector participation has been limited to separate planning, design or construction contracts on a fee for service basis – based on the public agency’s specifications. Expanding the private sector role allows the public agencies to tap private sector technical, management and financial resources in new ways to achieve certain public agency objectives such as greater cost and schedule certainty, supplementing in-house staff, innovative technology applications, specialized expertise or access to private capital. The private partner can expand its business opportunities in return for assuming the new or expanded responsibilities and risks. PPPs provide benefits by allocating the responsibilities to the party – either public or private – that is best positioned to control the activity that will produce the desired result. With PPPs, this is accomplished by specifying the roles, risks and rewards contractually, so as to provide incentives for maximum performance and the flexibility necessary to achieve the desired results. The Planning Commission of India has defined the PPP in a generic term as “the PPP is a mode of implementing government programmes / schemes in partnership with the private sector. It provides an opportunity for private sector participation in financing, designing, construction, operation and maintenance of public sector programme and projects”. In addition, greenfield investment1 in the infrastructure development has also been given more encouragement in India. Greenfield investment is defined as an investment in a start-up project, usually for a major capital investment and the investment starts with a bare site in a greenfield.

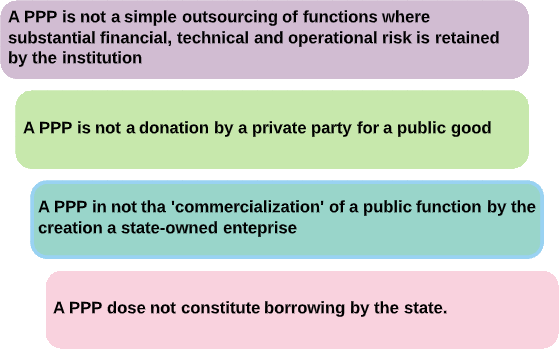

What is not a PPP?

The way a PPP is defined in the regulations makes it clear that:

PPPs can follow a variety of structures and contractual formats. However, all PPPs incorporate

three key characteristics:

- nA contractual agreement defining the roles and responsibilities of the parties,

- Sensible risk-sharing among the public and the private sector partners, and

- Financial rewards to the private party commensurate with the achievement of pre-specified Outputs.

(1).Arrangement with Private Sector Entity: The asset and/or service under an arrangement will be provided by the Private Sector Entity to the public.

(2).Public asset or service for public benefit: Has the element of facilities/ services being provided by the Government as a sovereign to its people. To better reflect this intent, two key concepts are elaborated below:

- ‘Public Services’ are those services that the State is obligated to provide to its citizens (towards meeting the socio-economic objectives) or where the State has traditionally provided the services to its citizens. For example, provision of security, law and order, electricity, water, etc. to the citizens.

- Public Asset’ is that asset the use of which is inextricably linked to the delivery of a Public Service. For example, public road which is linked to public transportation or, those assets that utilize or integrate sovereign assets to deliver Public Services, like right of way on highways or use of river / water bodies, etc.

Features of public–private partnership

PPPs in India have ensures the speedy and cost effective of key projects in sectors such as power, technology and infrastructure. This has great value for taxpayers who are benefiting from the impact of such ventures.

All risks pertaining to design, building, financing and operation transferred to the private entity Transfer of demand risk depends on the extent to which the private sector can influence usage

Public-private partnerships in India have integrated public infrastructure with the superior financing and maintenance provided by private enterprises. The synergistic collaborations between the public sector and private firms and companies have led to the generation of resources and knowledge transfer.

- Contracts specify the service outputs required rather than asset configuration/mode of service delivery Emphasis on type of service & performance standards Private entity incentivized to deliver outputs using innovation in design, construction, operation and financing

PPPs have overcome the capacity constraints of the economy by generating huge productivity through optimal utilization of labor and capital resources.

Whole life asset performance- Private entity takes responsibility & assumes risk for the performance of the asset and delivery of service over a long term

Joint ventures and partnerships between the leading companies and the government have been very successful in generating jobs as well as growth in key economic sectors.

Payment for Performance- Revenue/ Payment to private entity is subject to performance in relation to specific & quantified criteria enshrined in the contract

The public sector has regulated the projects to ensure accountability and delivery of quality products and services.

Innovation and excellence characterize the public-private partnerships that have emerged across the years in India. These PPPs are ensuring the effective utilization of state assets in a manner that is productive as well as profitable.

Infrastructure created using these partnerships is of a superior quality. This has led to the development of many good airports and buildings across India. India needs more basic infrastructure and PPPs are the best way to accomplish this.

PPPs also help the public sector to develop a more commercial approach. This is essential as most parties in India are very oriented towards social welfare and they often do not consider factors such as profit. Any partnership is only successful if it is able to meet the needs of the masses and also generate a profit.

PPPs have also ensured that the Indian public gets value for its money. India is a nation that has to meet the challenges of generating enough resources to meet the needs of the people.

India has one of the fastest growing populations in the world. Using the finances of the private firms to complete the PPP ventures has led to conservation of national and governmental resources.

Significance of Public-Private Partnership

Financial and managerial resources are critically required for successful implementation and more so, the sustainability of e-Governance initiatives. While the normal preference for any reform initiative is through the exclusive use of in-house resources, the merits of inducting the private sector resources into the e-Governance sector have now been appreciated and accepted by policy-makers in Government. Public-Private Partnership has thus become one of the cornerstones of NeGP. PPP, as applied to the e-Governance sector is still in a stage of evolution. While early PPP projects like eSeva had attempted a simple version of PPP, more complex projects like MCA 21 required considerable innovation and experimentation in designing and adoption of an appropriate PPP model. The following is an attempt to examine PPP in light of the significance of the e-Governance sector. New technologies demand new types of implementation models. In the conventional approach, the project ownership lies with the public sector itself along with the responsibility for funding it and bearing the entire risk. The concept of PPP has been in operation for more than a decade, primarily in relation to the construction and operation of public infrastructure projects like bridges, airports, highways, hospitals etc. PPP is a mechanism that attempts to capture the strengths of both – a government organization as well as a private enterprise.

There are many compelling reasons why governments should look at PPP in relation to their e-Governance plans. Some reasons are enumerated below:

The PPP model can combine the accountability mechanisms and domain expertise of the public sector with the efficiency, cost-effectiveness and customer-centric approach of the private sector. As compared to the public sector, the private sector is more efficient and innovative in adopting and applying new technologies. This is also true in the specific case of Information and Communications Technology. Therefore, the PPP approach in the field of e-Governance is well suited in combining the core strengths of the public and private sectors for the delivery of efficient online services.

2.The pace of implementation:New innovations in the field of Information Communication Technology are happening at a fast rate. This applies to all its segments – hardware, software and networks. Newer versions and releases of operating systems, database servers, application servers, and security software are continuously being released at regular intervals. The typical life cycle of a large e-Governance initiative is 18 to 24 months from initiation to completion. It has been observed that the private sector is generally faster than the government in adopting and making use of the latest technology. This is a compelling reason to join hands with the private sector.

3.Resources:The combined effect of the huge size of e-Governance effort and the speed of implementation is that investments required in the e-Governance sector are very large over a continuous period of 5 years. It is estimated that India needs over 45,000 crore of investment in the e-Governance sector over a period of 3-5 years – excluding the cost of communication and access infrastructure. This is sixteen times higher than the current annual IT expenditure of about 3000 crore in the government sector. In addition to this, high quality managerial and human resources are required. It is difficult to mobilize such large amounts of financial and human resources within the government. Tapping the financial, managerial and manpower resources of the private sector is a viable alternative in this regard.

Characteristics of PPP

The private sector is responsible for carrying out or operating the project and takes on a substantial portion of the associated project risks

During the operational life of the project the public sector’s role is to monitor the performance of the private partner and enforce the terms of the contract

The private sector’s costs may be recovered in whole or in part from charges related to the use of the services provided by the project, and may be recovered through payments from the public sector

Public sector payments are based on performance standards set out in the contract

Often the private sector will contribute the majority of the project’s capital costs, although this is not always the case

It will often be necessary to build or add to existing assets in order to meet the infrastructure needs of the economy and users. However, an important part of the infrastructure PPP concept is that:

• A PPP is focused on outputs, and the outputs of the PPP are infrastructure services, not infrastructure assets.

The reason for the focus on outputs and services rather than assets is to encourage efficient use of public resources and improved infrastructure quality.

A PPP brings the public and private sectors together as partners in a contractual agreement, for a pre-defined period (e.g. 30 years) matched to the life of the infrastructure assets used to provide the services. The private partners (investors, contractors and operators) provide specified infrastructure services and, in return, the public sector either pays for those services or grants the private partner the right to generate revenue from the project. For example, the private partner may be allowed to charge user fees or receive revenue from other aspects of the project.

The best PPPs will have the public and private partners working together to build and sustain a long-term relationship that is of benefit to all.

Reasons for direct government involvement

Other than its strategic, financial and economic interest, the government may also like to directly participate in a PPP project. The main reasons for such direct involvement include:

- To address political sensitivity and fulfill social obligations

- To ensure commercial viability

- To provide greater confidence to lenders

- To have better insight to protect public interest.

Government involvement in PPPs

The government has an important stake in infrastructure development. Considering its public good in nature, strategic importance, profound effects on other sectors, and related issues in public safety and security, and utilization of natural resources, governments always take interest in infrastructure development, whether implemented by the public sector or the private sector. There are also other reasons of government's interest which include:

- The network nature of most infrastructures implies that they cannot be considered as isolated projects (road, energy transmission line, telephone line, etc.)

- Can be used as a policy tool for development

- Infrastructure is important and needed but individual projects are not always commercially viable (water supply, rural/local roads, for example)

- Bulky nature and large size of investment requirements

- Long to very long existence with perpetual liability through generations

There are legal, social, economic, political and administrative issues involving PPPs. The government has responsibility in addressing a wide range of issues in PPPs if a country has to run a successful PPP programme. Private participation in infrastructure development requires the government to continue to play a key role in planning, policy formulation and regulatory matters. Further, in order to promote private participation, the government needs to implement a series of economic, financial and legal reforms which only it can initiate. In these respects, the major responsibilities of government are in:

- Formulation of a PPP policy framework

- Creation of an enabling environment

- Establishment of an administrative mechanism

- Promotion of good governance

- Addressing the social and political concern of PPP projects

- Capacity-building of the public sector

These responsibilities are discussed in the following.

Why a policy framework?Formulation of a policy framework is an important step towards building an enabling environment for PPPs. The existence of a clear framework can remove ambiguities and uncertainties about government's intention to PPP development.

Contents: Such a framework may have two parts:

- the first part on common matters to all PPPs such as objectives, principles and general policy issues; and

- the second part on issues specific to each sector

Social objectives can be incorporated in the policy framework as well as in legal and regulatory regimes.

Defining the roles of public and private sectors

The roles of public and private sector should be clearly defined in the framework. Private sector friendly policies can be formulated and their implementation needs to be coordinated across all sectors and at all spatial levels. It is also important to include in the framework (and follow) certain core principles of good governance namely transparency, accountability and participatory approach in decision making to promote PPPs. Formulation of a policy framework is also important in view of the fact that many aspects of it can be turned into legal and regulatory instruments.

The creation of PPP-enabling environment is one of the main responsibilities of the government. Main reasons why the existing environment may not be conducive to PPPs? Deficiencies of the regulatory and legislative framework: laws and regulations will control whether, or how, PPPs can be implemented. At minimum, the legal and regulatory framework should allow the Government to enter in PPP type of contracts with the private sector. In many cases, the existing regulatory environment may also be conservative and too restrictive and may not be favorable for undertaking PPPs. In order to address these issues, governments may consider enacting new legislations or suitably amend the existing ones to address these issues;

- Prevailing unfavorable general perception and understanding of PPP and the absence of clear policies on the role of private and public sectors which should be addressed through the development of a clear policy framework and

- Imperfections in market and sector structure.

More often than not, the existing market and sector structure is not conducive to PPPs. Lack of relevant market regulation leads to monopoly and sector inefficiencies. In fact, sector inefficiencies can be major deterrents to private participation in infrastructure. For example, the existence of barriers such as public monopoly and distortion in the pricing of competing transport modes is a serious problem for the motivation of the private sector to invest in the transport sector in many countries.

It is necessary to formulate rules and clear guidelines defining the administrative process involved in project implementation, in order to overcome the administrative difficulties faced by the bureaucracy. Establishment of procedures for various tasks and administrative approval from competent authorities at different stages of project implementation process are also necessary in running a successful PPP programme. Streamlined administrative procedures reduce uncertainties at different stages of project development and approval and enhance investors' confidence in a PPP programme.

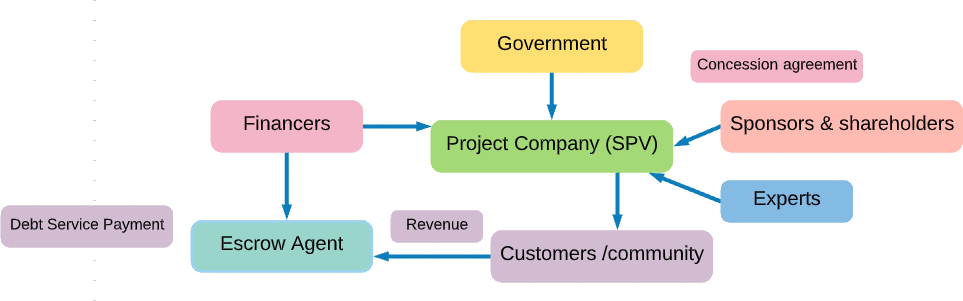

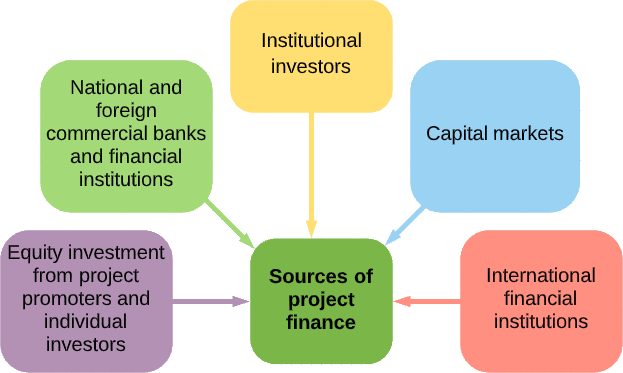

Project financing

PPPs in infrastructure are normally financed on project basis (as opposed to corporate financing). This refers to financing in which lenders look to the cash flows of an investment for repayment, without recourse to either equity sponsors or the public sector to make up any shortfall.

This arrangement has several advantages:

- tors;

- more careful project scrutiny, risk analysis leading to change in project structure, reduction in level of risk and more appropriate allocation of risks between parties

However, project financing also has manydisadvantages which include:

more complex transactions than corporate or public financing;

- higher transaction costs (the due diligence process conducted by parties results in higher development costs, which could be up to 5-10 per cent of project value);

- protracted negotiation between parties;

- Requirement of close monitoring and regulatory oversight (particularly for the potential expostulate guarantees).

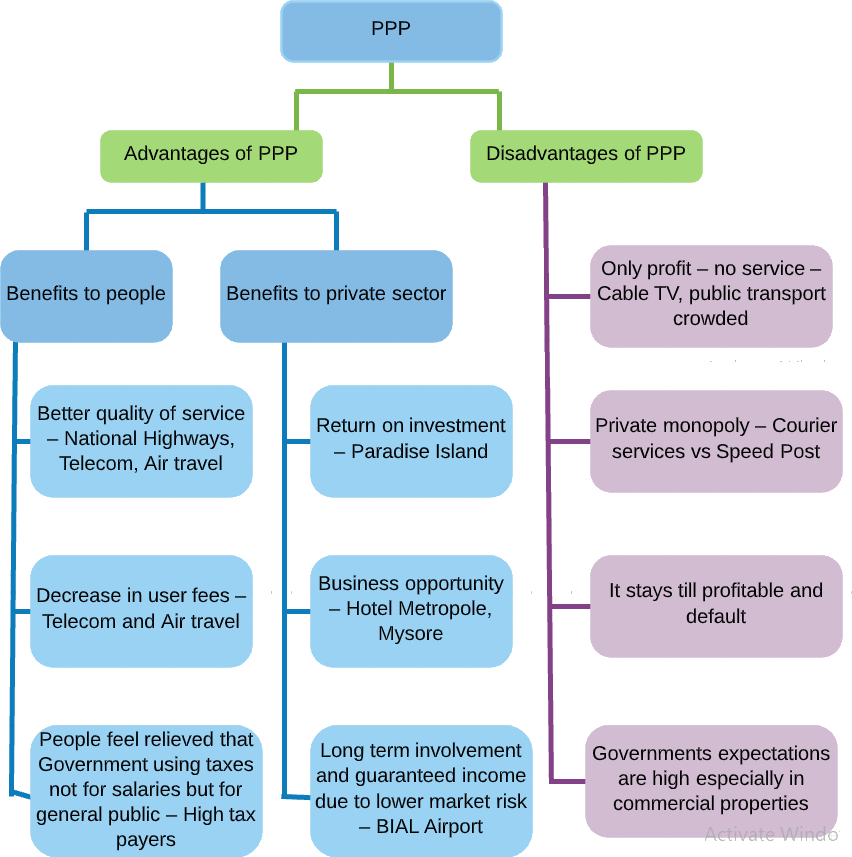

Advantages of PPP

Access to private sector finance

- India has a very large infrastructure need and an associated funding gap. PPPs can help both to meet the need and to fill the funding gap. PPP projects often involve the private sector arranging and providing finance. This frees the public sector from the need to meet financing requirements from its own revenues (taxes) or through borrowing.

Better infrastructure

- They provide better infrastructure solutions than an initiative that is wholly public or wholly private. By shifting the responsibility for finance away from the public sector PPPs can enable more investment in infrastructure and increased access to infrastructure services.

Optimum utilization of skills

- Efficiency advantages from using private sector skills and from transferring risk to the private sector

- Enlargement of focus from only creating an asset to delivery of a service, including maintenance of the infrastructure asset during its operating lifetime

- This broadened focus creates incentives to reduce the full life-cycle costs (ie, construction costs and operating costs)

Increased transparency in the use of funds

- A well-designed PPP process can bring procurement out from behind closed doors. The PPP tender and award process based on open competitive bidding following international best practice procedures lead to transparency.

Less delays

- They result in faster project completion and reduced delays on infrastructure projects by including time-to-completion as a measure of performance and therefore of profit.

Risk distribution

- Transfer of risks is the most important advantage of PPP projects. In PPP projects, there is a possibility to transfer most or all of the risks to the private entity. The private entities explore opportunities, even though they involve risks.

Constant cash flow

- The state budget is formed of fixed budgets for each ministry. Major investments are temporary modifications of the budget of a ministry, and this problem can be difficult to deal with within the budgetary process. Avoiding major investments by having a constant cash flow is an important driver when the state looks at the advantages of PPP.

Implementation Structures

Different organizational structures may be used to implement PPP projects. These include:

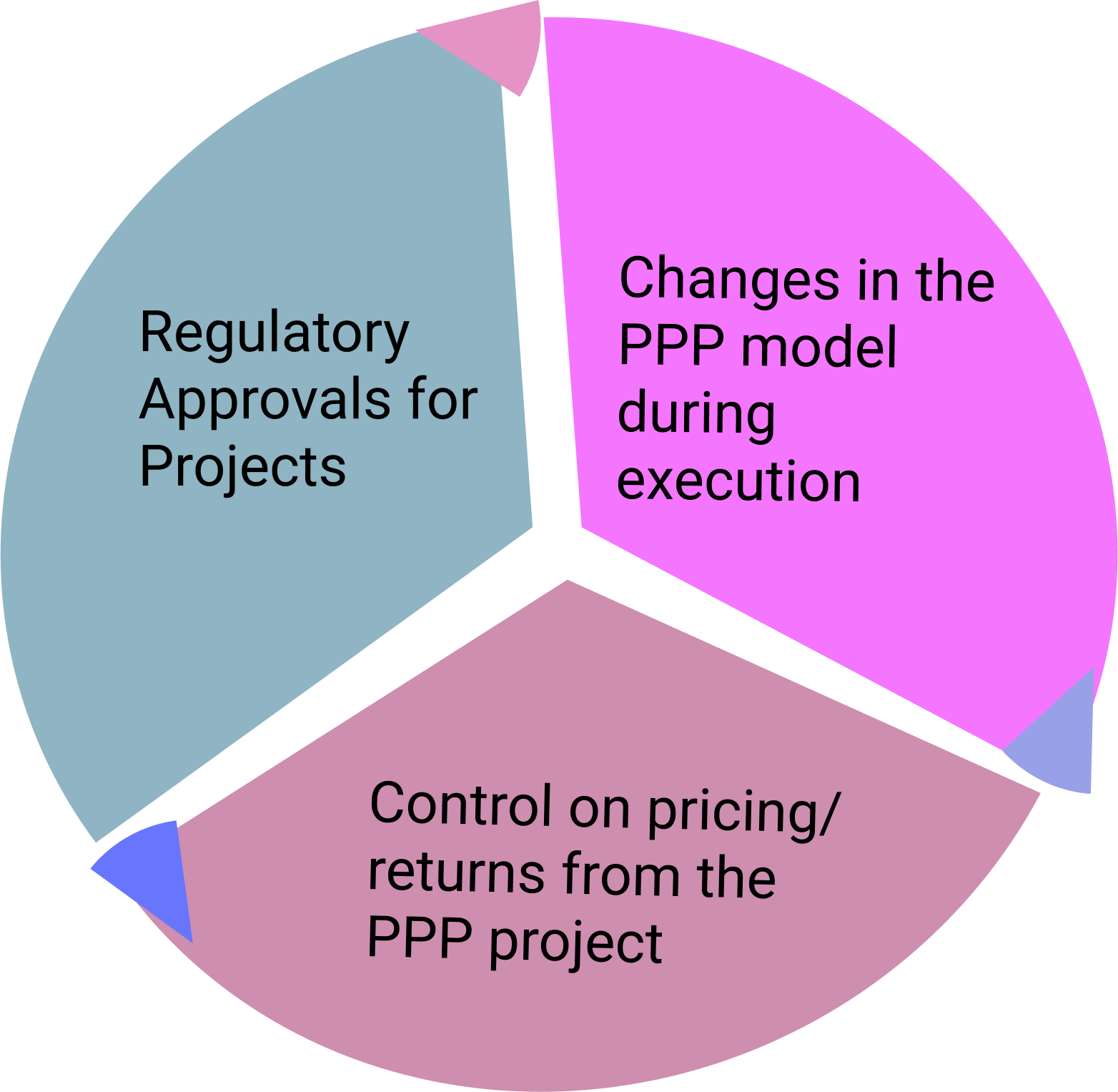

PPPs often cover a long-term period of service provision (e.g. 15-30 years, or life of the asset). Any agreement covering such a long period into the future is naturally subject to uncertainty. If the requirements of the public sponsor or the conditions facing the private sector change during the lifetime of the PPP the contract may need to be modified to reflect the changes. This can entail large costs to the public sector and the benefit of competitive tendering to determine these costs is usually not available. This issue can be mitigated by selecting relatively stable projects as PPPs and by specifying in the original contract terms how future contract variations will be handled and priced.

Difficulty in Demonstrating Value for Money in AdvanceIdeally, a project should be procured as a PPP on the basis of a clear demonstration that it provides value for money (VFM) compared with public sector procurement. However, it is difficult to demonstrate VFM in advance due to uncertainties in predicting what will happen over the life of the project and due to a lack of information about comparable previous projects. However, the standard for VFM is different in India to more economically developed countries such as Australia or the UK. In those countries there is a much smaller funding need. In India, many projects procured in the public sector, experience time and cost over runs, and hence it is likely that well-managed private procurements will deliver savings. Furthermore, the funding gap is far greater than the Public Sponsor can meet by itself. In this case, it may sometimes not be a question of public vs. private procurement, but rather the choice between private procurement or none at all. If this is the case then the focus should be on making a careful assessment of alternative project options to be sure that the projects that are selected are the best ones economically and financially.

- The public sector environment is suited to supporting PPPs

- The project is suitable to being carried out as a PPP –

- The potential barriers to successful project implementation have been identified and can be overcome

Given that these conditions are satisfied, the project must be commercially viable for the private sector and offer value for money (VFM) for the public sector.

Commercial viability

Commercial viability is crucial if the project is to attract a private partner. For a project to be commercially viable does not mean it cannot receive some financial and other support from the public sector. In some cases such support may be necessary, and initiatives such as Viability Gap Funds (VGF) have been established for this purpose.

Careful and appropriate risk allocation between the public and private partners is a critical focus of PPP design to achieve value for money.If private partners do not bear the risks that are under their control, their incentives for efficiency will be weakened and PPP benefits may be reduced. The requirements for effective risk transfer and the ability to harness private sector efficiencies means PPPs are best suited to projects for which:

- It is possible to clearly specify the requirements in terms of service outputs – the idea is to capture as much of the private sector efficiencies as possible by allowing scope for bidders to introduce efficiencies through innovations proposed in their bids

- The requirements can be specified so as to enable monitoring of performance against measurable standards and enforcement of penalties where standards are not met

- The requirements of the public sector sponsor are likely to be stable throughout the life of the PPP – the aim is to avoid the need to renegotiate the contract at a later date due to changes to project scope or requirements

Pre-requisites for Implementing PPP projects

Certain pre-requisite conditions must be fulfilled in order to use PPPs or derive benefits from their use as a tool for project implementation.

Enabling authority: The public entity should unambiguously have the enabling authority (that is, legal power) to transfer (to the private party) its responsibility of providing the service in question. This authority may stem from the enabling legislative and policy framework or from an administrative order. The instrument of transfer is through a legally enforceable contract between the authorized public entity and the private party. For example, the Department of Telecom (DoT) could issue Cellular and Basic Services Licenses only after appropriate amendments to the Indian Telegraph Act, 1884. The National and State Highways legislation needed appropriate amendments to enable private parties to develop and maintain highways and levy and collect tolls / user fees.

To derive benefits from PPPs projects would need to incorporate the following features:

Financial obligations: The transfer of responsibility to the private party should be of significant proportions, usually involving large financial investment obligations on part of the private party. This would bring in efficiencies in the way projects are financed and could bring down costs for users.

Performance-based payment: Payment to the private entity for service provided whether paid maximum benefits. Thus, the tenure of the contract would be for periods always in excess of 5 years and may go to 50-60 years as well, depending on the economic life / life cycle of the underlying assets.

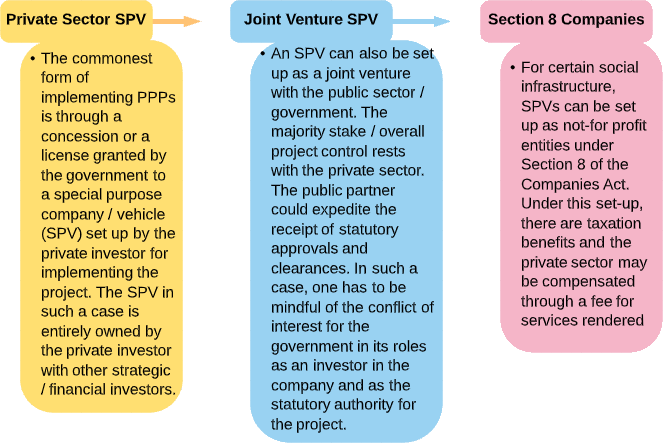

Special Purpose Vehicle

A Special Purpose Vehicle (SPV), a new company, is set up to implement each project. Usually the sponsoring entity (majority-owing private partner) offers no additional balance sheet support except for the initial equity commitment. The majority of the project obligations are usually addressed through separate contractual arrangements for construction. O&M, supply agreements (for instance, waste supply in a MSW project or fuel supply agreement for a power generation project), off take (purchase of compost for a MSW treatment project or purchase of water / power) and financing – which would mirror the obligations passed on to the SPV under the concession agreement.

The benefit of using a SPV structure is that it is a bankruptcy-remove structure. The project and the sponsor are both insulated from each other. The main advantage for the government is that the project is protected from failure of the sponsoring entity.

Implementation of the PPP Model

The PPP model of implementation is more suitable for particular areas of e-Governance and not to all. The criteria for PPP include long-term nature of the demand for a service, profitability and amenability to structuring a commercial framework and business model for PPP. The following is an illustrative list of areas suited for PPP.

Public-Private Partnership projects also pose several challenges which need to be understood and addressed carefully. There is often a lack of congruence in the objectives of the two partners – government and the private sector. The success of PPP depends on the degree to which the public and private sector partners align their efforts in achieving these objectives. Clarity on objectives has to be achieved by both the parties at the outset.

Also, the organizational cultures in the private and public sector differ widely. This may result in conflicting situations since e-Governance involves substantial process reform needing interaction between the partner company and the government agency or agencies in charge of the ‘domain’. It is necessary to create an appropriate coordination and review mechanism that develops mutual trust and confidence. Also, the agreements defining the mutual role and responsibilities should be precisely drafted, following a transparent process of selection of the private partner.

Typical risks in Infrastructure PPP

| S.No. | Risk type | Description |

|---|---|---|

| 1 | Pre-operative task risks | |

| Delays in land acquisition | Refers to the risk that the project site (or sites) will be unavailable or unable to be used within the required time, or in the manner or the cost anticipated or the site will generate unanticipated liabilities due to existing encumbrances and native claims being made on the site. This risk is most relevant to greenfield projects involving treatment and storage facilities | |

| External linkages | Refers to the risk that adequate and timely connectivity to the project site is not available, which may impact the commencement of construction and overall pace of development of the project. | |

| Financing risks | Refers to the risk that sufficient finance will not be available for the project at reasonable cost (e.g., because of changes in market conditions or credit availability) resulting in delays in the financial closure for a project. | |

| Planning risks | Refers to the risk that the pre-development studies (technical, legal, financial and others) conducted are inadequate or not robust enough resulting in possible deviations from the outcomes that were planned or expected in the PPP project development. | |

| 2 | Construction phase risks | |

| Design risk | Refers to the risk that the proposed design will be unable to meet the performance and service requirements in the output specification. It can result in additional costs for modification and redesign. | |

| Construction risk | Refers to the risk that the construction of the assets required for the project will not be completed on time, on budget or to specification. It may lead to additional raw materials and labor costs, additional financing costs, increase in the cost of maintaining existing infrastructure or providing a temporary alternative solution due to a delay in the provision of the service. | |

| Approvals risk | Refers to the risk that delays in approvals to be obtained during the construction phase will result in a delay in the construction of the assets as per the construction schedule. Such delays in obtaining approvals may lead to cost overruns. | |

| 3 | Operation phase risks | |

| Operations and maintenance risk | Refers to the risks associated with the need for increased maintenance of assets or machinery over the term of the project in order to meet performance requirements. In a brownfield PPP, where the private partner takes over operation of existing assets, O&M risk is very sensitive to the starting condition of the assets. In this case the private operator's O&M risk is related to the risk of poor or incomplete information about the quality of the assets that it will take over. | |

| Volume risk | Refers to the risk that demand for water or sanitation services will vary from the initial forecast, such that the total revenue derived from the project over the project life will vary from initial expectations. | |

| Payment risk | Refers to the risk that charges for services are not collected in full or are not set at a level that allows recovery of costs. Who bears the payment risk depends on whether the charges for services are paid directly by users, or are paid by the municipality. If charges are paid by the municipality (via taxes) the public sector bears this risk. | |

| Financial risk | Refers to the risk that the concessionaire introduces too much financial stress on a project by using an inappropriate financial structure for the privately financed components of the project. It can result in additional funding costs for increased margins or unexpected refinancing costs. Currency risk can also impact on financial risk if the project includes funding denominated in foreign currency. | |

| Performance risk | This is a risk that the quality of services delivered will not meet the performance standards agreed in the Concession Agreement. The Concession Agreement should stipulate penalties or compensation terms in this case. | |

| Environmental risk | Refers to the risk of environmental damage in excess of what is planned for in the environmental impact mitigation plan. For example, ground water pollution from sewerage release. |

| S.No. | Risk type | Description |

|---|---|---|

| 4 | Handover risks | |

| Handover risk / Terminal value risk | Refers to the risk that the concessionaire will default in the handover of the asset at the end of the project life, or that it will fail to meet the minimum quality standard or value of the asset that needs to be handed back to the public entity. This risk (and terminal value risk) generally relates to concession and BOT type PPPs. However, it may also be relevant to performance based management contracts in which the private partner is responsible for investing in meters. | |

| 5 | Other risks | |

| Change in law | Refers to the risk that the current legal / regulatory regime will change, having a material adverse impact on the project. | |

| Force Majeure | Refers to the risk that events beyond the control of either entity may occur, resulting in a material adverse impact on either party's ability to perform its obligations under the PPP contract. These events are sometimes also called "Acts of God", to indicate that they are beyond the control of either contracted party. | |

| Concessionaire risk | Refers to the risk that the concessionaire will prove to be inappropriate or unsuitable for delivery of the project, for example due to failure of their company. | |

| Sponsor risk | Refers to the risk that the Sponsor will prove to be an unsuitable partner for the project, for example due to poor project management or a failure to fully recognize the agreed terms of the Concession Agreement. | |

| Concessionaire event of default | Refers to the risk that the concessionaire will not fulfill its contractual obligations and that the public Sponsor will be unable to either enforce those obligations against the concessionaire, or recover some form of compensation or remedy from the concessionaire for any loss sustained by it as a result of the breach. | |

| Government event ofdefault | Refers to the risk that the public Sponsor will not fulfill its contractual obligations and that the concessionaire will be unable to either enforce those obligations against the Sponsor, or recover some form of compensation or remedy from the Sponsor for any loss sustained by it as a result of the breach. |

Problems with PPP Projects

Uncertainties: PPPs often cover a long-term period of service provision (e.g. 15-30 years). Any agreement covering such a long period into the future is naturally subject to uncertainty. If the requirements of the public sponsor or the conditions facing the private sector change during the lifetime of the PPP, the contract may need to be modified to reflect the changes. This can entail large costs to the public sector.

Policy and regulatory gaps: Inadequate regulatory framework and inefficiency in the approval process have been considered as serious disincentives for developers and contractors. Indian government has a poor record in regulating PPPs in practice. For example, more than two years were needed for the Gujarat Pipavav port project to receive the necessary clearances after achieving financial closure. Moreover, most of the large projects involve dealings with various ministries where coordination remains inefficient.

Crony capitalism: In many sectors, PPP projects have turned into conduits of crony capitalism. It is worth noting that a large chunk of politically connected firms in India are in the infrastructure sector, which has used political connections to win contracts in the past. Metro projects become sites of crony capitalism and a means for accumulating land by private companies.

Renegotiation: While private firms accept stringent terms of PPP contracts initially, they lose no opportunity for renegotiating contracts, in effect garnering a larger share of public resources than originally planned. Rather than being an exceptional clause, renegotiation has become the norm in PPP projects in India. PPP firms use every opportunity for renegotiating contracts by citing reasons like lower revenue or rise in costs which becomes a norm in India. Frequent renegotiations also resulted into drain of larger share of public resources. These firms create a moral hazard by their opportunistic behavior.

- PPP projects have been stuck in issues such as disputes in existing contracts, non-availability of capital and regulatory hurdles related to the acquisition of land.

- Across the world PPPs are facing problems, performance of PPPs has been very mixed according to study conducted by various research bodies.

- It is also argued that PPP is mere a ‘’language game” by governments who find it difficult to push privatization, or when politically it is difficult to contracting out.

- Loans for infrastructure projects are believed to comprise a large share of the non-performing asset portfolio of public sector banks in India.

- Checking Viability: PPPs should not be used to evade responsibility for service delivery to citizens. This model should be adopted only after checking its viability for a project, in terms of costs and risks. Further, PPP structures should not be adopted for very small projects, since the benefits are not commensurate with the costs.

- Risk allocation and management: Public-Private Partnership PPP contracts should ensure optimal risk allocation across all stakeholders by ensuring that it is allocated to the entity that is best suited to manage the risk. A generic risk monitoring and evaluation framework should be developed covering all aspects of a project’s life cycle.

- Strengthening governance: The Prevention of Corruption Act, 1988 should be amended to distinguish between genuine errors in decision making and acts of corruption by public servants.

- Strengthening institutional capacity: A national-level institution should be set up to support institutional capacity building activities and encouraging private investments with regard to PPPs. Independent regulators must be set up in sectors that are going for PPPs. An Infrastructure PPP Adjudication Tribunal should also be constituted. A quick, efficient, and enforceable dispute resolution mechanism must be developed for PPP projects.

- Strengthening contracts: The private sector must be protected against such loss of bargaining power. This could be ensured by amending the terms of the Public-Private Partnership PPP contracts to allow for renegotiations.

The success of Public-Private Partnership to a large extent depends on optimal risk allocation among stakeholders, the environment of trust and robust institutional capacity to timely implementation of PPP projects. To foster the successful implementation of a PPP project, a robust PPP enabling ecosystem and sound regulatory framework is essential.

Types of PPP

PPP Options

Types of Investment Models

Public Investment Model: In this model Government requires revenue for investment that mainly comes through taxes.

As the world is facing the prospect of an extended period of weak economic growth, by enhancing public-sector investment large pools of savings can be channelized into productivity.

Properly targeted public investment can do much to boost economic performance, generating aggregate demand quickly, fueling productivity growth by improving human capital, encouraging technological innovation, and spurring private-sector investment by increasing returns.

Though public investment cannot fix a large demand shortfall overnight, it can accelerate the recovery and establish more sustainable growth patterns.

Private Investment Model: For a country to grow and increase its production investment is required. Presently tax revenue of India is not adequate to meet this demand so government requires private investment.

Private investment can be source from domestic or international market.

From abroad private investment comes in the form of FDI or FPI.

Private investment can generate more efficiency by creating more competition, realization of economies of scale and greater flexibility than is available to the public sector.

Public-Private Partnership Model: PPP is an arrangement between government and private sector for the provision of public assets and/or public services. Public-private partnerships allow large-scale government projects, such as roads, bridges, or hospitals, to be completed with private funding.

In this type of partnership, investments are undertaken by the private sector entity, for a specified period of time.

These partnerships work well when private sector technology and innovation combine with public sector incentives to complete work on time and within budget.

As PPP involves full retention of responsibility by the government for providing the services, it doesn’t amount to privatization.

There is a well defined allocation of risk between the private sector and the public entity.

Private entity is chosen on the basis of open competitive bidding and receives performance linked payments.

PPP route can be alternative in developing countries where governments face various constraints on borrowing money for important projects.

It can also give required expertise in planning or executing large projects.

Models of Public Private Partnership

These models are different on level of investment, ownership control, risk sharing, technical collaboration, duration, financing etc. Commonly adopted model of PPPs include

Build-Operate-Transfer (BOT)

- It is conventional PPP model in which private partner is responsible to design, build, operate (during the contracted period) and transfer back the facility to the public sector.

- Private sector partner has to bring the finance for the project and take the responsibility to construct and maintain it.

- Public sector will allow private sector partner to collect revenue from the users. The national highway projects contracted out by NHAI under PPP mode is a major example for the BOT model.

Build-Own-Operate (BOO)

- In this model ownership of the newly built facility will rest with the private party.

- On mutually agreed terms and conditions public sector partner agrees to ‘purchase’ the goods and services produced by the project.

- A BOO transaction may qualify for tax exempt status and is often used for water treatment or power plants.

Build – Own – Operate – Transfer (BOOT)

- In this variant of BOT, after the negotiated period of time, project is transferred to the government or to the private operator.

- BOOT model is used for the development of highways and ports.

- The private sector builds and owns the facility for the duration of the contract, with the primary goal of recouping construction costs (and more) during the operational phase. At the end of the contract the facility is handed back to the government. This structure is suitable when the government has a large infrastructure financing gap as the equity and commercial risk stays with the private sector for the length of the contract. This model is often used for school and hospital contracts.

Build-Operate-Lease-Transfer (BOLT)

- In this approach, the government gives a concession to a private entity to build a facility (and possibly design it as well), own the facility, lease the facility to the public sector and then at the end of the lease period transfer the ownership of the facility to the government.

Design-Build-Operate-Transfer (DBFOT)

- In this model, entire responsibility for the design, construction, finance, and operation of the project for the period of concession lies with the private party.

- The private sector designs, builds, finances, operates an asset, then leases it back to the government, typically over a 25 – 30 year period. Public sector long-term risk is reduced and the regular payments make it an attractive option to the private sector.

Lease-Develop-Operate (LDO)

- In this type of investment model either the government or the public sector entity retains ownership of the newly created infrastructure facility and receives payments in terms of a lease agreement with the private promoter.

- It is mostly followed in the development of airport facilities.

Design–build–operate–transfer (DBOT)

- This funding option is common when the client has no knowledge of what the project entails. Hence they contracts the project to a company to design, build, operate, and then transfer it. Examples of such projects are refinery constructions.

Design – Construct – Maintain – Finance (DCMF)

- Design, Construct, Maintain and Finance is very similar to DBFM. The private entity creates the facility based on specifications from the government body and leases it back to them. This is generally the convention for PPP prison projects.

- A private entity is entrusted to design, construct, manage, and finance a facility, based on the specifications of the government. Project cash flows result from the government's payment for the rent of the facility. Some examples of the DCMF model are prisons or public hospitals.

O & M (Operation & Maintenance)

- In an O&M contract, a private operator operates and maintains the asset for the public partner, usually to an agreed level with specified obligations. The work is often sub-contracted to specialist maintenance companies. The payment for this contract is either via a fixed fee, where a lump sum is given to the private partner, or more commonly a performance-based fee. In this situation, performance is incentivized using a pain share / gain share mechanism, which rewards the private partner for over-performance (according to the agreed SLAs) or induces a penalty payment for work which has fallen short.

Design–build–finance–maintain (DBFM)

- The private sector designs, builds and finances an asset and provides hard facility management or maintenance services under a long-term agreement." The owner (usually the public sector) operates the facility. This model is in the middle of the spectrum for private sector risk and involvement.

Design–build–finance–maintain–operate (DBFMO)

- Design–build–finance–operate is a project delivery method very similar to BOOT except that there is no actual ownership transfer. Moreover, the contractor assumes the risk of financing until the end of the contract period. The owner then assumes the responsibility for maintenance and operation. This model is extensively used in specific infrastructure projects such as toll roads. The private construction company is responsible for the design and construction of a piece of infrastructure for the government, which is the true owner. Moreover, the private entity has the responsibility to raise finance during the construction and the exploitation period. Usually, the public sector begins payments to the private sector for use of the asset post-construction.

Different Levels of Private sector engagement in PPP contracts

| Model | Identify Infrastructure Need | Propose solution | Project design | Project financing | Construction | Operation | Maintenance | Ownership | Whether Concession? |

|---|---|---|---|---|---|---|---|---|---|

| Bid–build | Public sector | Private sector | Public sector | No | |||||

| Design–bid–build | Public sector | Private sector | Public sector | Private sector | Public sector | No | |||

| Design–build | Public sector | Private sector | Public sector | Private sector | Public sector | No | |||

| Design–build–finance | Public sector | Private sector | Public sector | No | |||||

| Design–build–finance–maintain | Public sector | Private sector | Public sector | Private sector | Public sector | No | |||

| Design–build–finance–operate | Public sector | Private sector | Public sector | No | |||||

| Design–build–finance–maintain–operate | Public sector | Private sector | Public sector | No | |||||

| Build–finance | Public sector | Private sector | Public sector | No | |||||

| Operation & maintenance contract | Private sector | Public sector | No | ||||||

| Build-operate-transfer | Public sector | Private sector | Public sector | Temporary | |||||

| Build–lease–transfer | Public sector | Private sector | Public sector | Private sector | Temporary | ||||

| Build–own–operate–transfer | Public sector | Private sector | Temporary | ||||||

| Build–own–operate | Public sector | Private sector | Yes | ||||||

| Market-led proposals | Private sector | Public sector | no |

Typical modes and characteristics

| Model | Asset ownership | Duration | Capital investment focus & responsibility | Private partner risks | Private partner roles | Features |

|---|---|---|---|---|---|---|

| Management Contract | Public | Short – medium (e.g. 3-5yrs) | Not the focus Public | Low (Pre-determined fee, possibly with performance incentive | Management of all aspects of operation and maintenance. | This involves contracting to the private sector most or all of the operations and maintenance of a public facility or service. Although the ultimate obligation of service provision remains with the public authority, the day-to-day management control is vested with the private sector. Usually the private sector is not required to make capital investments. These are prevalent in India across sectors. e.g., Karnataka Urban Water Supply and Improvement Project, performance based maintenance contracts in highways. |

| Management Contract | Public | Medium – long | Limited Focus Brownfield (Rehabilitation / expansion) Private | Medium (Tariff / Revenue share) | Minimum Capex, Management, Maintenance | This is similar to management contracts but include limited investments for rehabilitation or expansion of the facility. This mode has been adopted in the power distribution and water supply sectors e.g. Bhiwandi Distribution Franchise, Latur Water Supply Project. |

| Lease Contracts - Asset is leased, either by the public entity to the private partner or vice-versa. | ||||||

| Lease Contracts | Public | Medium (e.g., 10-15yrs) | Not the focus Public | High Revenue from Operations | Management and maintenance | e.g. Leasing of retail outlets at railway stations by Indian Railways |

| Build Lease Transfer (BLT) or Build-Own-Lease-Transfer (BOLT) | Private (Leased to the government) | Medium (e.g. 10-15yrs) | Greenfield Private | Low-medium Pre-set lease from the government. | Capex | Involves building a facility, leasing it to the Govt. and transferring the facility after recovery of investment. Primarily taken up for railway projects such as gauge conversion in India in the past, with limited success. |

| Build-Transfer-Lease (BTL) | Public | Medium (e.g., 10-15yrs) | Greenfield Private | High Revenue from User Charges | Capex and Operations | Involves building an asset, transferring it to the Govt, and leasing it back. Here the private sector delivers the service and collects user charges. |

| Concessions - Responsibility for construction (typically brownfield / expansions) and operations with the private partner while ownership is retained by the public sector. | ||||||

| Area Concessions | Public | Long (e.g. 20-30 yrs) | Brownfield/ Expansions Private | High Tariff revenue | Design, finance, construct, manage, maintain | Private sector is responsible for the full delivery of services in a specified area, including operation, maintenance, collection, management, and |

| Model | Asset ownership | Duration | Capital investment focus & responsibility | Private partner risks | Private partner roles | Features |

|---|---|---|---|---|---|---|

| construction and rehabilitation of the system. Operator is now responsible for all capital investment while the assets are publicly owned even during the concession period. The public sector’s role shifts from being the service provider to regulating the price and quality of service. e.g water distribution concession for a city or area within the city. | ||||||

| Build-Operate-Transfer Contracts - Responsibility for construction (typically Greenfield) and operations with the private partner while ownership is retained by the public sector. | ||||||

| Design-build-operate (DBO) | Public | Short-medium (e.g. 3-5 yrs) | Greenfield Public | Medium-High Tariff revenue | Design, construct, manage, maintain | Not very common in India. Typically financing obligation is not retained by the public sector. |

| Build-operate-transfer (BOT)/ Design-Build-Finance-Operate-Transfer (DBFOT) | Public | Long (e.g. 20-30 yrs) | Greenfield Private | High Tariff revenue | Design, finance, construct, manage, maintain | Most common form of BOT concession in India. e.g. Nhava Sheva International Container Terminal, Amritsar Interstate Bus Terminal, Delhi Gurgaon Expressway, Hyderabad Metro, Salt Lake Water Supply and Sewage Disposal System. |

| Build-operate-transfer (BOT) Annuity | Public | Long (e.g. 20-30 yrs) | Greenfield Private | Low Annuity revenue / unitary charge | Design, finance, construct, manage, maintain | This has been adopted for NHAI highway projects in the past. More recently, it is the preferred approach for socially relevant projects where revenue potential is limited. e.g. Tuni Anakapalli Project, Alandur Underground Sewerage Project |

| Build-own-operate Transfer (BOOT) Contracts - Private partner has the responsibility for construction and operations. Ownership is with the private partner for the duration of the concession. | ||||||

| Build-own-operate-transfer (BOOT) or DBOOT | Private | Long (e.g. 20-30 yrs) | Greenfield Private | High Tariff revenue | Design, construct, own, manage, maintain, transfer | Most common form of BOOT concession in India. For example, Greenfield minor port concessions in Gujarat are on a BOOT basis. |

| BBuild-own-operate (BOO) | Private | Perpetual | Greenfield Private | High Tariff revenue | Design, finance, construct, own, manage, maintain | Under this structure the asset ownership is with the private sector and the service / facility provision responsibility is also with the private sector. Not common in India. |

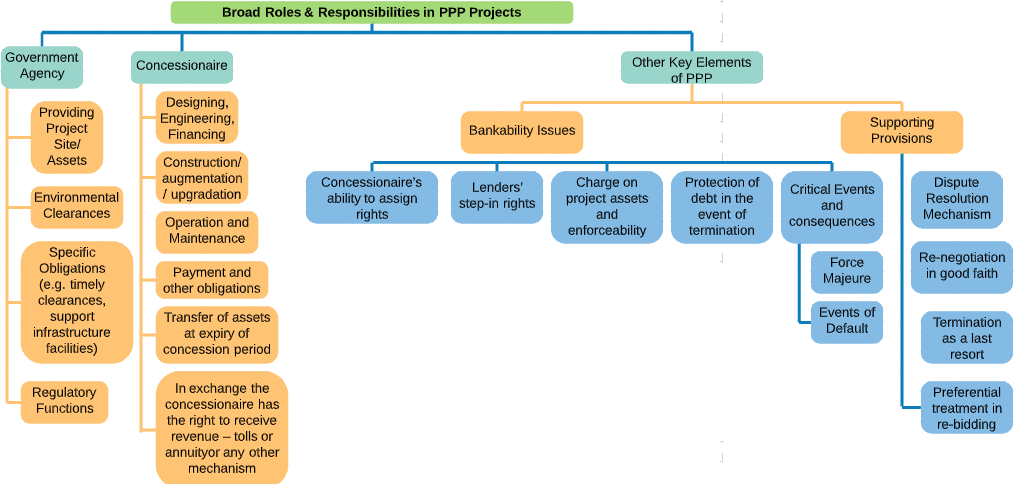

Contractual Framework

A PPP project operates under a contractual framework, where the intended outcomes are explicitly set out. This contract is called the Concession Agreement. The concession agreement lays out the rights and obligations of both the private party and the public entity, and the consequences in case of non-fulfillment of any obligation.

The importance of the contract lies in the fact that it is usually the only tangible security available to both parties in case of non-performance.

The contracting parties are usually the government agency (concessioning authority) which is procuring the service, and the private party (concessionaire) that is providing the service. The other parties may include the state government, lenders, and supplies of services. It is important to remember that a concession is a license, wherein certain rights are enjoyed by the private party in return for performing certain obligations.

- All intentions need to be set out in a contract

- Concession Agreement - bundle of rights & obligations and consequences in case of non fulfillment

- Usually the only tangible security available

- Contracting parties: Government Agency – Concessioning Authority and Private Party – Concessionaire

- Other parties – state government, Lenders, Suppliers of services

- A concession is a license – rights enjoyed for obligations performed.

- Striking a balance between differing concerns & objectives of parties

- Legislative Back up

- Rights and obligations of parties

- Identification and allocation of risks

- Penalties and rewards which would ensure performance

The different modes and variants of them will be appropriate to different projects. This will depend in particular on the nature of the service or output required, which in turn depends on the sector and subsector, and the political and economic climate in which the PPP will be carried out.

New (“Greenfield”) or existing assets – Greenfield developments, which include major capital expenditure to build new infrastructure, have different requirements to the rehabilitation or management of existing assets in Brownfield developments. The scope of potential private sector roles is broader in greenfield projects. The chosen PPP mode will reflect whether the private sector will be responsible for the design, finance and construction of the project (e.g.: DBO agreement or a variation) or only some of these roles.

Ownership flexibility – There may be legal restrictions on public ownership (as is the case in India for highways or port frontages). Other practical issues need to be taken into account in deciding ownership, such as political acceptability (e.g. due to resistance to public ownership of certain facilities that are seen as providing strategic or ‘vital’ services, such as may be the case in electricity).

Restrictions on ownership rule out PPP modes that specifically contain ownership aspects, such as Build-own-operate (BOO) and its variants (e.g. BOOT). In this case other options such as lease management contracts, BOT, BTL, could be considered.

Lifetime of the asset and scale of capital costs – infrastructure assets that involve large upfront capital costs, such as roads, require long timeframes for cost recovery. Such assets may be suited to long-term contracts (e.g. BOT, BLT etc). However, long timeframes also bring greater risk of future unknowns. The public sector may be required to take on some of these risks by providing some guarantee to cost recovery in order to attract private sector project finance. For example, for a road project where future traffic volumes are uncertain the PPP might be structured with annuity payments rather than being toll-based, to reduce the revenue risk to the private operator. Alternatively, if long-tenor finance from the private sector is not available public sector financing may need to step into the gap (e.g., IIFCL). The willingness or ability of the public sector partner to meet these risks is a further factor to be considered in determining the length of contract. For example, if facilities to support long-tenor debt are not available shorter term contracts with renewal clauses may be appropriate.

The nature of the service to be provided and the supporting infrastructure assets – More broadly, the nature of the end-user service itself will tend to favor a type of contracting structure. This is related to the capital cost structure (scale and timing) and the nature of the assets (physically fixed to their location or transportable). Large capital-intensive network infrastructure assets tend to be natural monopolies and require some form of institutional price and quality regulation, either within the terms of contract or by a dedicated regulatory agency. By contrast, some services such as those that are provided on the network (e.g. municipal buses, electric energy) or solid waste collection can be subject to market competition. A different contracting structure is possible in this case, including greater opportunity for shorter contracts and periodic competitive re-bidding to maintain pressure on costs.

Cost recovery options – Whether the revenue from the PPP will be from a user-charge or a management fee or annuity paid by the public sector has important implications for the nature of the risk sharing.

Stability of demand for the services required – long-term PPP contracts are best suited to the provision of infrastructure services which are not expected to change much through time. These projects have lower risk of unforeseeable outcomes compared with projects whose services are subject to change, for example in sectors that are subject to rapid technological change.

Role of Different Stakeholders in the PPP Process

| Stakeholder | Role |

|---|---|

| Political decision makers | Establish and prioritize goals and objectives of PPP and communicate these to the public Approve decision criteria for selecting preferred PPP option Approve recommended PPP option Approve regulatory and legal frameworks |

| Company management and staff | Identify company-specific needs and goals of PPP Provide company-specific data Assist in marketing and due diligence process Implement change |

| Consumers | Communicate ability and willingness to pay for service Express priorities for quality and level of service Identify existing strengths and weaknesses in service |

| Investors | Provide feedback on attractiveness of various PPP options Follow rules and procedures of competitive bidding process Perform thorough due diligence resulting in competitive and realistic bidding |

| Strategic consultants | Provide unbiased evaluation of options for PPP Review existing framework and propose reforms Act as facilitator for cooperation among stakeholders |

Why does India need a new public-private partnership policy?

Public-Private Partnership has a mixed track record of failures and successes but the government is confident about it, given its success in airports, railways and many highways, and wants a new policy that will facilitate private investment. The central government announced on June 28 that it would formulate a new public-private partnership (PPP) policy to improve the ease of doing business by cutting red tape and reduce the number of clearances.

In the 2021-22 Budget speech, Finance Minister Nirmala Sitharaman had announced that monetizing operating public infrastructure assets is a very important financing option for new construction.

The PPP model has delivered mixed results in India on account of overextended balance sheets, contract disputes, land acquisition problems, and lack of a dispute-resolution mechanism.

However, the government is extremely confident about the PPP model because of its success in the airports, roads, and railway sectors.

change.

But what are the issues the government will need to address in its new PPP policy?

India is a federal state where land is a common subject for the central and state governments.

While most PPP projects in India are awarded by the central government or by a regulatory body under the central government, projects are implemented in the jurisdiction of state governments.

The key execution challenges during construction project developers’ face include acquisition of land and right of way, securing necessary clearances, and financial closure. The two biggest issues the government currently faces are land acquisition-related challenges because of the procedural delays involved and the compensation involved in buying the land. In many road PPP projects, the delay between the project being awarded and the actual date for construction to start ranges 9 to 15 months.

As per most PPP concession agreements in India, it is the responsibility of the government authority to hand over the required land and right of way to the concessionaire, failure of which resulted in the time and cost overrun of the projects. But there have been cases where state authorities did not act proactively to make available land or resolved land-related issues. As observed in the case of Mumbai metro rail and national highway projects, the concessionaire received delayed Right of Way to complete the construction work. Further, most PPP projects in India are still awarded after two layers of approvals from a Standing Finance Committee and the Public-Private Partnership Appraisal Committee.

Projects that are bigger than 1,000 crore also require the approval of the Union Cabinet, which delays them further. PPP projects that involve government funding in the form of viability gap funding are further delayed due to regulatory approvals.

If viability-gap funding is needed, then the projects go through an additional layer of scrutiny, as the government needs to invest in the project, these causes a delay in awarding projects.

Environment and social considerations are also important but more critical in these projects. In certain cases, these issues can become very complicated and politically challenging.

For instance, in the development of the Mumbai Metro, about 800 acres of land in Mumbai's Aarey was declared a reserve forest, and the project developer, Reliance Infra, was forced to shift their plans to construct a car shed elsewhere.

Given the long-term nature of these projects, it is difficult to identify all possible contingencies and issues that may come up during project development but were not anticipated by the parties when the contract was signed. It is also possible that some of the projects may fail or may be terminated prior to the projected term of the project, for reasons including changes in government policy, failure by the private operator or the government to perform their obligations, or due to external circumstances. A number of road operators in India have found actual traffic lower than the government’s projection. The major risk observed in the case of most of the failed road projects is lower-than-expected traffic growth and in turn, subdued toll/fee collections during the operation phase. The unrealistic traffic projections during the pre-bid stage phase of the project were the cause of this debacle. The GMR Ambala Chandigarh Expressways Pvt Ltd and L&T Halol Shamlaji Tollway Ltd are examples of such projects where actual traffic has been much lower than the government's projected traffic.

PPP projects have usually been a success in economic infrastructure projects in India, such as airports and toll roads. However, they have faced problems in social infrastructure such as water supply, solid waste management, health, and education; these projects have taken a hit. Private firms will also want to know that the rules of the game are to be respected by the government as regards undertakings to increase tariffs/fair regulation, etc. The private sector will also expect a significant level of control over operations if it is to accept significant risks. The electricity tariffs in Delhi and Mumbai are examples of such cases where private partners are subject to tariffs set by the respective state governments. In most PPP projects citizens will continue to hold the government accountable for the quality of utility services and the government will also need to retain sufficient expertise, to be able to understand the PPP arrangements, to carry out its own obligations under the PPP agreement and to monitor the performance of the private sector and enforce its obligations. Private sector will do what it is paid to do and no more than that – therefore incentives and performance requirements need to be clearly set out in the contract.

Public-Private Partnerships (PPP) – Recent Developments

Public-Private Partnership in India – As of November 2020, around 1100 PPP projects were launched in the country, representing a total of $274,959,000,000 of committed investments

Health Sector

- NITI (National Institution for Transforming India) Aayog has come out with Public-Private Partnership (PPP) Model to bring changes in the Health Sector. As per this PPP model developed by NITI (National Institution for Transforming India) Aayog, the gap in medical education will be addressed and the shortage of qualified doctors will be addressed. As per this model, existing or new private medical colleges will be linked with functional district hospitals.

Power Sector

- Government of India is planning to launch the Atal Distribution Transformation Yojana (ADITYA) Scheme. As per this scheme, if states will involve private sectors to improve the efficiency of state distribution companies (discoms), then the Central Government will provide incentives to the States. Such a scheme did not exist earlier. If Indian needs to become a $ 5 trillion economy then it requires a healthy power sector. The 3 important segments of the power sector are distribution, transmission and power generation. If progress needs to be done in desired pace and direction, then the distribution segment needs to be established as the strongest link hence the Central Government is focussing on increasing efficiency of the Distribution segment through ADITYA Scheme. Most of the developed countries have privatised their power distribution segment. The Public-Private Partnership model in Delhi was introduced in 2002, has proven to be a success. Delhi Vidyut Board was privatised by selling its majority stake (51%).

Railways

- Tejas Express is the 1st private train in India. Under the Public-Private Partnership (PPP) model, the services in the Tejas Express will be provided by private players. Services will include housekeeping, catering, ticketing, refunds, parcels. The Physical infrastructure for the Tejas Express will be Indian Railways. It includes coaches, locomotives, guards, loco pilots, guards.

Urban Housing