Professional Tax Registration- An introduction

Professional Tax is a tax collected by State Governments from the professionally occupied business entities. A person earning income from salary or professions such as Chartered Accountants, Company Secretaries, Lawyers, etc. is required to pay professional tax. For the purpose of this registration, the employers, professionals, traders, etc. come under the purview of registration.

This tax is deducted from the salary of the employer, which is later eligible for deduction from the computation of taxable income. The registration is obtained by the employers and business owners with the respect Municipal Corporation. Being it State based registration, the rate of tax and method of registration is different. Further, there are two types of registrations being – PTEC and PTRC registrations.

Professional tax is tax on income earned by employees or self employed people. Professional tax is a state level tax and currently applies in only few states in India.

The respective state governments in India levy the professional tax on income from profession or employment. The professionals earning an income from salary or other practices such as a lawyer, teacher, doctor, chartered accountant, etc. are required to pay professional tax. In case of salaried and wage earners, the professional tax is liable to be deducted by the employer from the salary/wages and the same is to be deposited to the state government. In case of other class of individuals, this tax is liable to be paid by the employee himself. The tax calculation and amount collected may vary from one state to another, but it has a maximum limit of 2500/- per year. Total amount of Professional Tax paid during the year is allowed as deduction under the Income Tax Act. The Professional Tax is a source of revenue for the state governments which helps in implementing schemes for the welfare and development of the region. Professional Tax is deducted by the employers from the salary of the salaried employees, and is deposited with the state government. Other individuals pay it directly to the government or through the local bodies appointed to do so.

Professional Tax registration is a tax registration applied on professionals and trades in India. This type of tax is state-level tax and has to be compulsorily paid by every member of staff employed in private companies. The owner of a business is responsible to deduct professional tax from the salaries of his employees and pay the amount so collected to the appropriate government department.

Professional tax registration is usually a slab-amount based on the gross income of the professional. It is deducted from his income every month. Some of the state governments that have levied this type of tax are Karnataka, West Bengal, Andhra Pradesh, Maharashtra, Tamil Nadu, Gujarat, Assam, Chhattisgarh, Kerala, Meghalaya, Orissa, Tripura and Madhya Pradesh. In case of salaried employees and wage earners, Employer is liable to deduct this type of tax with the State Government. In case of other class of Individuals, this tax is liable to be paid by the person himself.

Professional tax is collected by the Commercial Tax Department. The commercial tax department of the respective states collects it which ultimately reaches the fund of Municipality Corporation.

The employer is responsible for deducting professional tax from the salaries of his employees and paying the amount so collected to the appropriate state government. An employer has to furnish a return to the tax department in the prescribed form within the specified time along with proof of tax payment.

Professional tax is levied by Municipal Corporations of particular state and majority of the Indian states impose this duty. The professional tax is a source of revenue for the State Government which helps them in implementing schemes for the welfare and development of the region. It is also payable by members of staff employed in private companies. It is mandatory to pay professional tax. The rate of professional tax charged is based on the Income Slabs set by the respective State Governments. The tax amount of professional tax paid during the year is allowed as Deduction under the Income Tax Act.

Overview of Professional Tax Registration

Professional Tax is a tax that is levied by the state government, it is levied on the income that is earned by the trade and is remitted by the employer. A person has to pay a professional tax of around 2500 every year to the state or any local authority by the way of the tax on the profession, trades, callings, and the employments. Professional tax in India is not just levied on the professionals but it is levied on all employees, a person carrying business, freelancers and professionals, etc and it is subject to the income exceeding the monetary threshold if there is any. Professional tax is a kind of tax that is levied by the state government. The state government is also empowered to make laws with to the professional tax though being a tax on income under Article 276 of the constitution of India which deals with the taxes on profession, trades and callings, and employment. It may be noted that the professional tax is a deductible amount and can be deducted from the taxable income. Professional tax is just like income tax, but the central government and the professional tax collect the income tax managed by the state government. At the time of the introduction, the maximum limit on the tax to be collected as the professional tax was 250. There has been an upward revision of the professional tax to 2500 and has allowed the government to raise the additional resources.

Thus the ‘Professional tax’ is a tax which is levied on all kinds of professions, trades, and employment, and its applicability is based on the income of such-

- Profession,

- Trade, and

- Employment.

Professional tax is levied by the State Government and it varies from state to state. To govern the professional tax of the particular state, every state has its laws and regulations. However, all the states do follow a slab system based on the income to levy professional tax. Further, Individuals carrying on freelancing business without any employees are required to obtain Professional tax certificate subject to the pecuniary threshold if any, provided by the respective State Authorities.

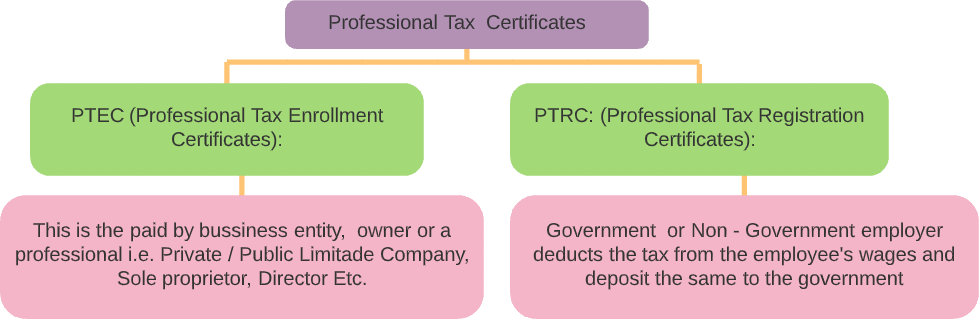

There Are Two Types Professional Tax Certificates:-

Note- A professional tax imposed is subject to the exemption provided by the respective State to particular categories. If the employer has different offices in different states of India, they will need to take Professional Tax Registration in those particular states.

Which states levy Professional tax in India?

The maximum amount an individual needs to pay as professional tax is 2500. The tax amount is based on the gross income of the professional. It happens to be deducted from his or her income every month by the employer. Here is the list of states where the professional tax is levied.

1.Andhra Pradesh

2.Telangana

3.Sikkim

4.Assam

5.Bihar

6.Chattisgarh

7.Gujarat

8.Karnataka

9.Kerala

10.Madhya Pradesh

11.Maharashtra

12.Meghalaya

13.Orissa

14.Tamil Nadu

15.Tripura

16.West Bengal

Here is the list of states where the professional tax is not applicable are

1. Union territories Controlled by the Central Government

2.Arunachal Pradesh

3.Delhi

4.Goa

5.Haryana

6.Himachal Pradesh

7.Jammu & Kashmir

8.Jharkhand

9.Nagaland

10.Punjab

11.Rajasthan

12.Manipur

13.Uttar Pradesh

14.Uttaranchal

15.Andaman & Nicobar

16.Chandigarh

17.Daman & Diu

18.Dadra & Nagar Haveli

19.Lakshadweep

20.Puducherry

21.Mizoram

As the state government levies the professional tax, it differs in each state. Each state declares a slab, and the professional tax is deducted based on these slabs. Many states and union territories do not charge any professional tax too. The professional tax is paid in 12 equal installments; in such situations where the source of income is falling under the sectors they will be liable for separate tax. As each state has its regulations and laws on the professional tax, the professional tax varies from state to state. However, a slab system is followed by all the states. The slab system is based on the income of the individual. Hence, the state government levies the tax based on income.

Benefits of Professional Tax Registration

Here are the reasons why one should never miss a professional tax payment

Imposes Minimal Restriction

- Professional tax is simple to comply with and the compliances relating to professional tax impose very few restrictions.

Avoid Penalty

- Professional tax payment is a legal requirement, and hence ignoring it can result in any penalty or prosecution. To avoid this penalty and prosecution, the self-employed person and employer pay their professional tax without any delay, as per the rates prescribed by their concerned state.

Easy Registered

- Professional tax is easy to get registered with simplified annual or monthly compliances.

Implementing Welfare & Development Programs

- The Professional Tax ia a source of revenue for the state governments which help in implementing schemes for the various welfare and development of the region.

can claim Deduction

- Deduction can be claimed in the salary on the basis of the professional tax paid. the deductions will be allowed in the year corresponding to which the taxpayer made the payments i.e. the deduction can be claimed of earlier paid professional tax on salary.

Judicial requirement

- Employers in many states of india are strictly bound by the judiciary to obtain the registration of professional tax. After the registration, they have to make the deductions and pay the service taxes of all the employees who work under them.

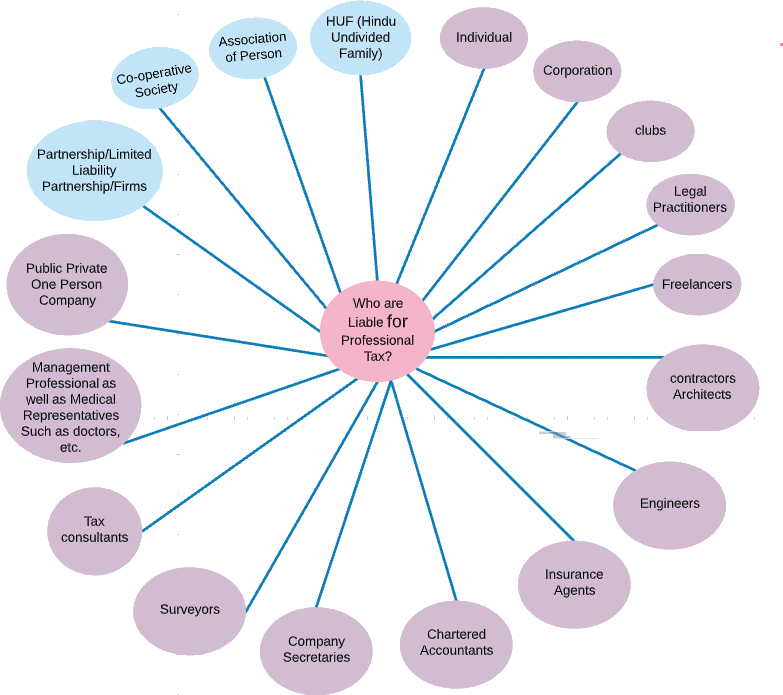

Who are Liable for Professional Tax?

The Below-mentioned class of persons is liable for Professional tax. Professional Tax is payable by the following ‘PERSONS’ (Individuals and Business Entities) engaged in any Profession, trade, callings or employment .However, it depends on the state where it is applicable-

Who is exempted from paying the professional tax in India?

Ex-servicemen

Individuals, above 65 years of age.

Individuals serving in the Central Para Military Force (CPMF)

People who run educational Institutions teaching up to class 12

Handicaps with at least 40% disability. A relevant Certificate must be submitted.

Any person who has a permit for a single three-wheeler or a single taxi to carry goods.

Individuals who are deaf, dumb, and blind are earning a salary.

Civilians as well as non-civilian members from the armed forces.

Technicians from foreign countries who are employed by the state

Foreign employees are exempt from paying professional tax.

Indians employed by the Foreign office and consultant are excluded from taking the certificate of registration.

Parents of children suffering from mental or permanent disability

Individuals with permanent physical disability

Badli workers engaged in the textile industry

Women engaged exclusively as an agent under the directorate of small savings or Mahila Pradhan Kshetriya Bachat Yojana

Guardians or parents of mentally challenged individuals.

Members of the armed forces. The age differs state wise

Understanding the Professional Tax Registration Applicability

Firms/Companies/LLPs

- In the case of professional tax, firms, LLPs, corporations, societies, HUFs, associations, clubs, and companies are considered taxable entities. All the branches involved in these will also be considered separate individuals under professional tax.

Individuals (Professional)

- Legal practitioners such as notaries and solicitors, medical representatives such as dentists, medical consultants, doctors, and other professionals such as management consultants, tax consultants, surveyors, company secretaries, chartered accountants, insurance agents, engineers, architects, and contractors are all considered professional individuals who need to pay professional tax.

Partners and Directors

- People who act as company directors, firm partners, LLP partners, and designated partners should pay professional tax. They should register under the professional tax act within 30 days of getting appointed in these roles.

Employers

- Within 30 days of the company's incorporation, the company/firm must get a professional tax enrollment certificate (PTEC) by registering on the government portal.

- The company/firm must have a professional tax registration certificate (PTRC) within 30 days of employing a staff member. The employers are supposed to deduct professional tax from the salary of the people employed under them and submit it at the professional tax department during the time of filing returns.

- The employers are supposed to deduct professional tax from the salary of the people employed under them and submit it at the professional tax department during the time of filing returns. The employer will have to register at the professional tax department before 30 days of its applicability.

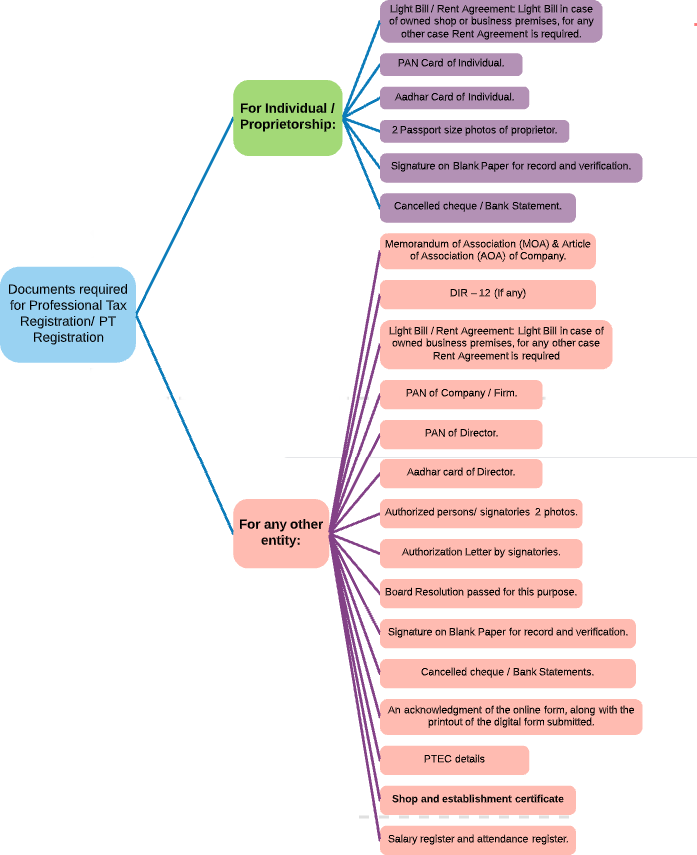

Documents required for Professional Tax Registration/ PT Registration

Online Professional Tax Registration - an Overview

Employers are required to obtain the registration when employees are appointed. This makes the employee eligible to deduct the professional tax from his employee’s salaries. Registration should be obtained within the 30 days of employing staff.

The procedure for the registration of professional tax varies from state to state, the slab rates can vary from one state to another, where the business owner has employees that are employed in different states then one has to get a professional tax registration for all the states.

The application for the registration under professional tax is to be submitted to the state tax department within 30 days of employing the staff in the business. If there is more than one place of work then an application is to be made separately to each authority considering the place of work that comes under the authority's jurisdiction.

In case there is a delay in the payment of the professional tax, there is a penalty of 5 per day, there is also a penalty of nonpayment there is a penalty of 10% of the tax.

The penalties on professional Tax vary in each state. Also, there is a penalty for Non-Registration. Along with the penalty for non-payment, there is also a penalty for late return filing.

Frequency of filing the returns: The frequency with which one has to file the returns are also dependent on the state the person is residing in, so before filing the returns it is very important to know the rules of the particular state.

Professional tax is a tax that is imposed by state governments on all salaried individuals. Professional tax is applicable to all working professionals, such as chartered accountants, lawyers, and doctors. It is levied based on the individual’s employment, trade or profession. The tax rates differ across all states; however, the maximum amount that can be levied as professional tax is 2,500 per annum.

How is HUF taxed?

- Professional tax applicability: Professional tax is levied on all types of trades and professions in India. It has to be paid compulsorily by every staff member who is employed in any private firm operating in India. Professional tax registration is the onus of every business owner, who must take up responsibility for deduction of professional tax and payment for the same.

- Professional tax for self-employed: Any professional who obtains a monthly regular income will need to pay the professional tax. By the word professional, we mean people employed in specialized fields such as accountancy, media, etc.

Though the actual penal interest or penalty can change according to each state’s legislation board, all states will be charged a penalty if they have not registered after the professional tax legislation is made applicable. Also, penalties will be charged if the payments are not made within the due date or if the return is not filed within the due date specified.

- 1. Fails to Get Registration- He will be liable to a penalty for the period during which he remains unregistered.

- 2. Fails to Deposit to the Government/ Late Deposition- He will be liable to a penalty for the period during which he remains unregistered.

- 3. Non-Deposition of Amount- The officials have power to recover such amount along with applicable penalty and interest from the assets of such defaulter. Moreover, they can attach his bank account also. In serious cases, prosecution case also can be filed.

Professional Tax Registration in Delhi

Professional tax is levied by the state government of that particular state. Professional tax in Delhi is the tax that is levied on the income that is earned by any trade and is remitted by the employer. Every year has to pay around 2500 to the state or the local authorities in the manner of tax on the profession, trades, callings, and employment. The professional tax is just like the income tax but the professional tax in Delhi is managed by the state government. The upward revision of professional tax 2500 has allowed the government to raise the additional resources.

Who had to pay professional tax in Delhi?Professional tax in Delhi is applicable for the individuals and the entities that are mentioned below:Companies, Firms, Limited Liability Partnerships, Corporations, societies, Hindu undivided families, associations, clubs, legal practitioners, contractors, architects, engineers, tax consultants, management professionals as well as medical representatives such as doctors.

Professional tax registration in DelhiAn application for registering under the professional tax in Delhi has to be made with the State Tax Department within 30 days of employing staff in a business. If in case there is more than one place of work the application has to be made separately to each of the authorities considering the place of work that is coming under the authority's jurisdiction.Delay in the payment of professional tax can lead to a penalty of 5 per day. On non-payment or the late payment there is a penalty of 10% of the tax if the filing of the returns is done late there is a penalty of three hundred rupees.

What is the professional tax rate in Delhi?The maximum amount an individual has to pay as professional tax is 2500. The slab amount is based on the gross income of the individual. The professional tax in Delhi is deducted from the salary of the employee by the employer every month.This deducted amount has to be deposited with the state government every month. It is mandatory to pay the professional tax as there are penalties in case of non-compliance.

Professional Tax Registration and Returns

Professional Tax Registration is mandatory within 30 days of employing staff in a business or, in the case of professionals, 30 days from the start of the practice. Professional tax needs to be deducted from the salary or wages paid amount. Application for the Registration Certificate should be made to the assesse's state tax department within 30 days of employing staff for his business. If the assesse's has more than one place of work, then application should be made separately to each authority with respect to the place of work under the jurisdiction of that authority.

If an employer has employed more than 20 employees, he is required to make the payment within 15 days from the end of the month. However, if an employer has less than 20 employees, he is required to pay quarterly (i.e. by the 15th of next month from the end of the quarter).

Employer Needs To Obtain 2 Registrations:-Profession Tax Enrolment Certificate (PTEC) – To deduct tax from the employee’s salary and pay Professional Tax Registration Certificate (PTRC) – To deduct tax for himself and pay Self-employed people need to obtain only 1 registration - PTRC

State-wise Professional Tax Slab FY 21 – 22

Professional tax is levied by the state and it is considered as state revenue. Not only by the government entity but the tax is also payable by the member of a private company. The tax rate is based on income slabs of each state.However, the professional tax is not imposed by all the states. It is imposed on people of only a few states, those are:

| States | Monthly Salary | Tax per Month |

| Karnataka | Up to 15,000 Above 15,000 | NIL 200 |

| Bihar | Up to 3, 00,000 From 3, 00,001 to 5, 00,000 From 5, 00,001 to 10, 00,000 Above 10, 00,000 | NIL 1,000 2,000 2,500 |

| West Bengal | Up to 8,500 From 8,501 to 10,000 From 10,001 to 15,000 From 15,001 to 25,000 From 25,001 to 40,000 Above 40,000 | NIL 90 110 130 150 200 |

| Andhra Pradesh | Up to 15,000 From 15,001 to 20,000 Above 20,000 | NIL 150 200 |

| Telangana | Up to 15,000 From 15,001 to 20,000 Above 20,000 | NIL 150 200 |

| Maharashtra | Up to 7,500 for men Up to 10,000 for women From 7,500 to 10,000 10,000 and above | NIL NIL 175 200 ( 300/- for February) |

| Maharashtra | Up to 7,500 for men Up to 10,000 for women From 7,500 to 10,000 10,000 and above | NIL NIL 175 200 ( 300/- for February) |

| Tamil Nadu | Up to 21,000 From 21,001 to 30,000 From 30,001 to 45,000 From 45,001 to 60,000 From 60,001 to 75,000 Above 75,000 | NIL 100 235 510 760 1095 |

| Gujarat | Up to 5,999 From 6,000 to 8,999 From 9,000 to 11,999 12,000 and Above | NIL 80 150 200 |

| Gujarat | Up to 5,999 From 6,000 to 8,999 From 9,000 to 11,999 12,000 and Above | NIL 80 150 200 |

| Assam | Up to 10,000 From 10,001 to 15,000 From 15,001 to 25,000 Above 25,000 | NIL 150 180 208, ( 212 for the February) |

| Kerala | Up to 1,999 From 2,000 to 2,999 From 3,000 to 4,999 From 5,000 to 7,499 From 7,500 to 9,999 From 10,000 to 12,499 From 12,500 to 16,666 From 16,667to 20,833 Above 20,834 | NIL 20 30 50 75 100 125 166 208/- (212 for February) |

| Meghalaya | Up to 4,166 | NIL |

| States | Monthly Salary | Tax per Month |

| From 4,167 to 6,250 From 6,251 to 8,333 From 8,334to 12,500 From 12,501 to 16,666 From 16,667 to 20,833 From 20,834 to 25,000 From 25,001 to 29,166 From 29,167 to 33,333 From 33,334 to 37,500 From 37,501 to 41,666 Above 41,666 | 16.50 25 41.50 62.50 83.33 104.16 125 150 175 200 208 ( 212 for February). | |

| Odisha | Up to 5,000 From 5,001 to 6,000 From 6,001 to 8,000 From 8,001 to 10,000 From 10,001 to 15,000 From 15,001 to 20,000 Above 20,000 | NIL 30 50 75 100 150 200 |

| Tripura | Up to 5,000 From 5,001 to 7,000 From 7,001 to 9,000 From 9,001 to 12,000 From 12,001 to 15,000 Above 15,000 | NIL 70 120 140 190 208 (212 for February) |

| Madhya Pradesh | Up to 1,50,000 From 1,50,001 to 1,80,000 Above 1,80,000 | NIL 125 212 |

| Sikkim | Up to 20,000 From 20,001 to 30,000 From 30,001 to 40,000 Above 40,000 | NIL 125 150 200 |

| Chhattisgarh | Up to 1,50,000 From 1,50,001 to 2,00,000 From 2,00,000 to 2,50,000 From 2,50,001 to 3,00,000 Above 3,00,000 | NIL 150 180 190 200 |

The owner of businesses is responsible to deduct the salaries of his employees and deposit the amount collected to the relevant government department. Depending on the nature of the business, the tax may be paid monthly, semi-annually or annual basis.Next, professional tax returns must be filed to the tax department at the end of every financial year. It must be filed in the pre-described form (with the proof of the tax payment) within a specified time.If the tax payment proof is not included, the application will be deemed to be incomplete or invalid.It may be noted that professional tax is a deductible amount for the purpose of Income-tax Act, 1961 and can be deducted from taxable income.

Penalty

The tax has to be paid within the time period specified by the respective State Government. The due dates will be provided within the act. In the uneventful case of failing to pay the tax, penalty and late fee would be penalized by the Government.

- In case of breach of the rules, a penalty of 2% per month is imposed

- In case of non-payment, 10% of additional payment is imposed

- In case of delay in obtaining the certificate of enrollment, a penalty of 5 per day is imposed

- In case of misrepresentation, 3 times the amount due is payable as the penalty.

- Interest @ 1.25% per month of delay in payment.

Profession Tax Enrolment Certificate number (PTEC)

Professional Tax Employee Registration is a must for all employers; who employ people with salary or wages. Certificate of Enrolment (EC) is a must for obtaining the Certificate of Registration (RC). The person is subject to pay the tax if he/she is exceeding the monetary threshold income provided by the State’s legislation.In the case of salary earners, the tax is deducted by the employer directly from the wages/salary amount of an employee. He is solely responsible for depositing the amount in the respective government department.In the case of other class individuals, the tax must be paid by the person himself.The calculation of tax varies from state to state, however, the maximum being set as 2500 per year.

Visit to e-PRERANA website

For Enrollment Certificate (EC), click on Enrollment Application from left panel of e-Service and the details On the left side bar of the application, the application would have to click on Enrollment of Application if the application is enrolling for payment of professional tax for this time then the enrollmentfor professional tax must be considered. if the application is new, then click and Select the new category for enrollment.

Select the Business Application to the Enrollment- In the next step, the application has to select the suitable business for enrollment for the professional tax. Here information related to the application must be provided by the employer. With this, the application has to enter the financial year for which professional tax has to be paid. If the application is already enrolled for the payment of professional tax in the respective State, then following Enrolled must be Selected by the application. Then the application has to input the 9 digit alphanumerical enrollment certificate for professional tax in respective State. When choosing the business type and status, personal information related to the business must be mentioned. if the business has multiple branches to carry out activities, than the same must be mentioned in the drop down menu of the form.

Click on Relevant Tax Application on the Schedule- In the next Step, the employer has to click on the relevant tax which is application on the respective business. For this the professional tax schedule of respective state must be considered.

Payment- In the last step the application must select the mode of payment of professional tax. The applicant can either pay online or offline. There is a method for e-payment option for the applicant. If this is not possible then application can either pay through cash, cheque or DD.

Then make payment online, then take a point of enrollment application and after that you will get enrollment certificate

For New Registration Certificate (RC), click on New RC Request fill the entire mandatory field, Sent OTP to Mobile and Verify the number, then you will receive a Acknowledgement No Through this you can get a RC certificate. After this the applicant would be provided with a PTN no or a Professional Tax Number. After this the applicant has to enter the professional tax number along with the professional tax data. Than the procedure for registration of professional tax is complete

Procedure of Professional Tax Registration Certificate (PTRC)

Step-1- Filing The Application Online

- The applicant can apply online through the Commercial Tax Department (CTD) portal of specific state.

Step-2-Filing The Form Along With The Requisite Documents

- The applicant shall file the form along with the requisite document.

Applying In Offline Mode

- One can also apply offline by submitting the application form along with the requisite documents and prescribed fee to the concerned State Government.

Step-3-Submit Hard Copy

- Once the applicant applied for registration, he/she should submit the physical copy to the concerned tax department.

Step-4- Scrutinization By The Tax Authority

- On receipt of an application, the tax authority shall scrutinize it for its correctness.

Step-5- Issuance Of Registration Certificate

- After scrutinization, if the authority gets satisfied, it shall approve the same and issue the registration certificate to the applicant. In case if the department found a flaw in the application, it can definitely raise a queries that shall be responded on time.

Cancellation procedures under the Professional Tax Act

1. Online login into the account make the cancellation Application. An application for cancellation of registration under sub-section 8 shall be made to be registering authority in Form III.

2. Take the print out of Acknowledgement

3. Submit the following document in department

- Application of cancellation with affix of 5 Court fees Stamp

- Original Professional tax Certificate

- Original Challan Copy

- Letter of Authority in favors of person attending department

- Closure proof (bank statement, previous year financial, Salary Register etc)

4. If the registering authority is satisfied that the application is in order, and falls within the provisions of sub-section (6) of section 8, it shall by order in writing, after giving the dealer a reasonable opportunity of being heard, cancel the registration with effect from a date fixed in accordance with sub-rule (3) and shall, by a notice placed on the notice board if its office publish the name, address and registration number of the dealer and the date from which the cancellation takes effect. A copy of such order shall be served on the dealer.

5. Where the registration is to be cancelled on the ground

- of discontinuance, transfer or otherwise disposal of the dealer's activity of execution of works contract, the date of cancellation of registration shall be the date on which the activity has been discontinued or transferred or otherwise disposed of;

- that the turnover either of all purchase or all sales of the registered dealer has during any year not exceeded the limit as specified in section 3 of the Act, the date of cancellation of registration shall not be later than the first day of the month next following the day on which the notice is published under sub-rule 2.

6. Where a registration of the dealer is to be cancelled under sub-section 7 of section 8,the Commissioner shall, after giving the dealer a reasonable opportunity of being heard, cancel the registration by an order in writing with effect from such date as the Commissioner may fix to be the date on which the activity of execution of works contract has been discontinued or transferred or disposed of, as the case may be and the Commissioner shall by a notice placed on the notice board of his office, publish the name; address and registration number of the dealer and the date from which the cancellation takes effect. A copy of the cancellation order shall be served on the dealer.

7. if the registration of a dealer is cancelled either on his application or under sub-section (7) of section 8, the dealer shall surrender the certificate of registration and the copies thereof, if any, granted to him, to the registering authority within fifteen days from the date of receipt by him of the order cancelling the registration.

8. After submitting all the documents, the department will cancel the certificate in 30 days; you can check the status online.

Digital Facility for Payment and Filing

The State Government has facilitated its taxpayers with the option of paying tax dues and filing the returns through the e-PRERANA portal of the Commercial Taxes Department. The online portal facilitates the taxpayer with various e-services such as filing enrollment application, e-payment of taxes, filing of returns, etc.Tax may be paid in online or offline mode and a challan be generated for each such successful payment. Employers must also file a Professional Tax Return in a prescribed form at regular intervals, where such time limits vary in each state.

Professional tax employer registration requires for all businesses, regardless of the number of workforces deployed in it. Upon registration, the employer will receive a Certificate of Enrollment from the Profession Tax Office. The document will include details of the tax payable by the employer and the stipulated date of payment. Failure to remit the tax within the specified date may lead to penal consequences.For example, for the awareness of the employers, the tax rate for businesses established under the Karnataka Shops and Commercial Establishments Act, 1961, is herewith specified. The Government declares the tax rate based on the strength of employees:

No employees – No tax implications.

One to five employees – 1000.

Five to ten employees – 1,500.

More than ten employees – 2,500.

Professional Tax Employee Registration

This kind of registration deals with an employee’s obligation, which is to be met by an employer. As previewed before, employers require doing the employee’s gloves by remitting their professional tax dues, which can be deducted from the salary of the latter. As employees earning more than 20,000 in a month qualify for the payment, businesses employing such personnel must obtain the Professional Tax Employee Registration. This registration is certified with a Certificate of Registration, which can be obtained by the employers who have the Certificate of Registration.

Once you will get registered with the Professional Tax registration department, Id Password will be issued in order to file a professional tax return. By using such Id password you can file a professional tax return on the website of the State government. For professional tax return filing you need to login to your account and on the basis of requirements such as monthly filing or quarterly filing, payment should be made.

Monthly Payment and Return

Employers, whose workforces earn a salary scaling to 20,000 or above must remit professional taxes on behalf of the employees; the contribution towards the same is stipulated to be 200 per month. These employers, who must have the certificate of registration, must file a return within twenty days of the succeeding month depicting the salary/wages remitted and the tax deducted from the employee’s monthly salary during the previous month. Non-payment of tax or failure to file returns will result in a penalty of 250 for every month of default.

Annual Payment and Return

A business holding an enrollment certificate requires paying their taxes at the stipulated rates before the 30th of April every year. Also, all employers must file an annual return within 60 days of the expiry of the given year. The return must comprise of the salaries/wages remitted to the employees and the tax deducted during the previous year.

Basic guidelines for making Tax Payments under the Profession Tax Act

- Every employer who is liable to deduct tax from the salary of wages of the employees and pay the tax to the Department on behalf of the employees shall get himself “registered”,(except officers of the State Government and the Central Government )Prescribed form of application is Form I

- Every assessee other than a person earning salary or wages in respect of whom tax is payable by his employer, liable to pay tax under the Act shall obtain a certificate of enrolment. The following persons are liable to get enrolled.

- Employees falling under Entry 1 of the First Schedule; and

- also covered by any other entry or entries and the rate of tax under any such other entry is more than the rate of tax under Entry 1 and have furnished certificate in Form III; and

- are simultaneously engaged in employment under more than one employer, and have furnished certificate in Form IV; and

Persons falling under any of the entries 2 to 21. Prescribed form of application is Form II.

Deposit of tax| Employer has employed | Make payment within |

|---|---|

| More than 20 Employees | 15 days from end of the month |

| 20 employees or less | 15th of next month from the end of each quarter |

While each state has the ability to fix penalty based on its own tax laws, the regime is generally centered on the following penalties:

| Delay in | Non-compliance | Penalty levied by most states |

|---|---|---|

| Registration | Non-registration when the employer was liable to be registered | 5 / day |

| Payment | Non-payment of tax or payment after the due date. | 10 % of the amount of tax |

| Filing of Return | Non-filing of Tax Returns or delay in filing | 1000/ return delayed by 1 month 2000/return for a further delay. |

Consequences of Default

Taxpayers failing to meet the compliance requirements will be dealt with the respective provisions. Here’s an overview of the various defaults and the consequences resulting from it:

Failure to obtain the Certificate of Enrollment

- A penalty of 1,000 is payable by the taxpayer, apart from that additionally annual tax payments pending is also payble.

Failure to obtain the Certificate of Registration

- Non-Compliance with this obligation or in deducting and remmitting the taxpayers quotient will force the employer to take it upon his stride to remit the tax liability by the employee. the remittance will include a simple intrest of 1.25% for each month or part threre of, as well as a penalty which is equivalentto the actual liability. these penel provisions will be in place until he/she fulfils the final obligation.

Non-Payment of tax

- In Case of delay in payment of tax the original tax amount along with the interest of 1.25% is applicable for each month of delay. Forthermore, the professional Tax Officer may levy an additional amount, which will not exceed fifty percent of the amount of tax due.

Failure to file returns

- A Penalty of 250 is Applicable for the employer for every month of delay.

Conclusion

Entry 60 in List II (State List) of the Seventh Schedule to the constitution empowers the State Legislatures to make law relating to levy of tax on Professions, Trades, Callings and Employments. Accordingly the State Legislature empowered the local authorities to tax on professions, trades, callings and employments by incorporating that power in the statutes relating to local authorities.Professional tax is a tax levied by the State Government. All states do not impose this tax, only some of them collect the tax. This tax is a source of revenue for the states that impose it.The individual state governments of India impose the professional tax on trade, calling, profession or employment of a person based on their income. Only salaried class employees bear the professional tax. It can be either salary or money earned from other practices like Doctor, Lawyer, CA, etc. The person is subject to pay the tax if he/she is exceeding the monetary threshold income provided by the State’s legislation.

- In the case of salary earners, the tax is deducted by the employer directly from the wages/salary amount of an employee. He is solely responsible for depositing the amount in the respective government department.

- In the case of other class individuals, the tax must be paid by the person himself.

The calculation of tax varies from state to state, however, the maximum being set as 2500 per year. Every state conducts its own laws and regulations in governing the professional tax. However, there is a slab system that is followed based on the income of its residents.In certain states there is concept of composition scheme. For e.g. in case of Maharashtra, the government announced composition scheme under which any person liable to make payment to government at rate of 2500 may make a lump sum payment in advance of 10,000 and his liability to pay for 5 years will be discharged.Also no tax is payable for holding any Profession for less than 120 days in the year.

Frequently Asked Questions

- 1. What is a professional tax and when is it levied?

-

The professional tax is a state-level tax that is imposed on the income that is earned through profession, trade, calling, or employment. The tax is based on the slab that is dependent on the income o the individual who may be self-employed or working as an employee of an entity.

- 2. Who deducts the tax and deposits the same with the government?

-

- In the case of self-employed individuals, the tax has to be paid by the individual himself. In the case of the individuals, the liability of deducting the tax is on the employer.

- 3. Who has to pay professional tax in India?

-

Every person that is engaged actively or otherwise in any profession, trades, callings, or employment and falls under one or the other class that is mentioned in the second column of the Schedule I appended to the profession tax act is liable to pay the professional tax.

- 4. What is the difference between a professional tax and income tax?

-

Income tax is a direct tax collected by the central government from all taxpayers. It is charged on a certain percentage of their income whereas, professional tax is an indirect tax collected by the state government. It is charged based on a slab for people engaged in business, occupation, or employment.

- 5. What is the slab of professional tax?

-

Each Indian state prescribes its slab for professional tax. For example: In Maharashtra, if your monthly income is between 7,500 to 10,000, then the professional tax levied is 175. Similarly, for monthly incomes above 10,001, the tax levied is 200 for 11 months and 300 on the 12th month. Finally, when the monthly salary is less than 7500, there is no professional tax imposed.

- 6.Is professional tax registration mandatory?

-

Employers in some states are required to deduct and deposit taxes from employees whose pay exceeds the minimum slab limit. That entity must get a registration certificate as well as an enrollment certificate.

- 7. How do I know my professional tax is paid?

-

Once the payment has been made, download the payment acknowledgement receipt. The receipt indicates that the payment has been made successfully.

- 8. How can I get my PTEC & PTRC number?

-

Each individual who registers for a professional tax certificate will receive a certificate which will have the TIN number mentioned as enrollment number or registration number.

- 9. How much professional tax is deducted from my salary?

-

Professional tax appears at the top of the salary slip as it is deducted even before calculating income tax. The employer deducts it from the salary of the employee and deposits it with the state government. Professional tax is calculated on the earned gross based on the tax levied by the statement government in the respective states.

- 10. Is it mandatory to pay professional tax?

-

Professional tax is a mandatory tax paid by every individual, firm, and company. There are penalties in case of non-compliance.

- 11. Why is professional tax different in every state?

-

The professional tax rules vary from state to state. As the rules vary from state to state, each state can set limits and rates. But the maximum amount limit has been developed to 2500 per year. The salary slab structures for levying professional tax differ from state to state.

- 12. Who is liable to professional tax in Delhi?

-

An individual who is engaged in any activity or any profession, trade, or employment has to pay professional tax in Delhi.

- 13. Who shall obtain the Professional Tax Registration?

-

The responsibility to obtain a registration lies with the owner of the business or profession. The business owner/employer is required to deduct the professional tax based on the professional tax slab from the salaries of employees and pay the same to Government before the 15th day of each month or quarter as applicable.

- 14. What is enrolment certificate?

-

Enrolment Certificate also known as the Professional Tax Enrolment Certificate (PTEC), this registration is obtained for the payment of taxes by the employers.

- 15. What is the registration certificate?

-

The employers are required to obtain the registration when employees are appointed. This makes the employees eligible to deduct the professional tax from his employee’s salaries. Registration should be obtained within the 30 days of employing staff.

- 16. In which States is Professional Tax applicable?

-

The State Governments of the following states have levied professional tax:

Punjab, Bihar, Karnataka, West Bengal, Andhra Pradesh, Telangana, Maharashtra, Tamil Nadu, Gujarat, Assam, Sikkim, Kerala, Meghalaya, Orissa, Tripura and Madhya Pradesh.

- 17. Whether the separate application is required for additional place of work?

-

Yes, if you have more than one place of work, you have to make a separate application for professional tax registration to the concerned authority.

- 18. What are the penalties of non-compliance of Professional tax payment?

-

For delays in obtaining Registration Certificate, a penalty of 5/- per day is levied. In case of non/late payment of profession tax, the penalty will amount to 10% of the amount of tax. In case of late filing of returns, a penalty of 300 per return will be imposed.

- 19. What are the due dates to file and pay Professional Tax?

-

The due date for the payment of Profession Tax is 30th June for the employees enrolled before 31st May of the year. The people enrolled after 31st May of a year are requested to pay Profession Tax within one month from the date of enrolment. Employers are requested to file monthly return along with due payment of tax.

- 20. Whether Shop & Establishment registration is also required for this registration?

-

In cities like Ahmedabad, both the registration must be obtained simultaneously. In a few places, Shop & establishment registration is a requirement for this application. Hence, it depends on the law of where the jurisdiction of the premise is situated.

- 21. Who is responsible for deducting the tax and depositing the same with the Government?

-

- In case of self-employed individuals, the tax has to be paid by the individual himself.

- In the case of employed individuals, the liability to pay the tax is on the employer.

- 22. Is Professional tax imposed in every state in India?

-

- No

- 23. Is a freelance professional is liable to pay Professional Tax?

-

Yes, Professional Tax is applicable even for freelance professionals if income exceeds the specified limit as per the Professional Tax Laws applicable in the state where the freelancer resides.

- 24. What is the enrollment certificate that is obtained by self-employed persons?

-

An employer who deducts the tax from the salary of the employee and pays to the government, such entity shall obtain registration certificate while employer if not deduct professional tax then the individual shall get enrolment certificate from necessary authority.

- 25. Can the liability of professional tax amount is paid in lump sum?

-

The Certain state allows the concept of a composition scheme under which any individual liable to make payment to the state government may make a lump sum payment in advance of 10,000(at a rate of 2500 *4).

- 26. On which date an employer becomes liable to pay Professional tax?

-

The liability will arise on the date on which the employer disburses salary to any of his employees in the taxable limit for the first time.

- 27. When is Professional Tax registration required?

-

- Professional tax enrollment certificate (PTEC) is mandatory in the case of professionals/ business and has to be applied within 30 days of commencement of practice/business.

- Professional tax registration certificate (PTRC) is mandatory within 30 days of employing staff in the business.

- 28. What is the penalty for furnishing wrong information’s?

-

The penalty prescribed as per section 5(6) for giving false information in application for Registration Certificate or Enrolment Certificate is equal to three times the tax payable under the Profession Tax Act.

- 29. What is the rate of interest for late payment?

-

The rate of interest is 1.25 percent per month of the amount of such belatedly paid tax.

- 30. Why Do I need Professional Tax registration Certificate (PTRC)?

-

This registration need to be taken by an employer. This is for payment of Profession tax deducted from salary of employees. Hence Professional Tax registration Certificate (PTRC) is needed.

- 31. Why Do I need Professional Tax enrollment Certificate (PTEC)?

-

This registration is required for businesses that are liable for PTEC registration. For example Doctors, CA etc. need to apply for PTEC. PTEC is the corporate liability of the company.

- 32. Is there different type of Professional Tax?

-

The professional tax is classified in to two types- Professional Tax -Employer and Professional Tax - Employee.

- 33. What is the Compliance under the Professional Tax Regulations?

-

Every registered business with Enrollment Certificate shall pay tax every year before 30th of April at the specified rates.

- 34. Who are responsible to pay professional tax?

-

In case of employees, an employer is a person responsible to deduct and pay professional tax to the State Government subject to the monetary threshold if any provided by respective state’s legislation, employer (corporate, partnership firms, sole proprietorship etc) also being a person carrying on trade/profession is also required to pay professional tax on his/her trade/ profession again subject to the monetary threshold if any provided by respective State’s legislation.

- 35. What is the Applicability of Profession Tax?

-

Company/Firms/LLP: Company, firms, LLP, Corporation, societies, HUF, Associations, clubs are taxable entity.

Professionals(Individuals): Legal Practitioners like solicitors, Notaries, medical representatives like dentist, medical consultants, doctors and other professionals like management consultants, tax consultants, surveyors, CS, CA, Insurance agents, engineers, architects and contractors are all considered as professional individuals who need to pay professional tax. - 36. What is the professional tax Registration Process?

-

The professional tax registration procedure varies according to state : The tax slab rates can vary from one state to another, where the business owner have employees under different states , then one have to get a professional tax registration for all the states. Frequency of filing returns: The frequency with which one needs to file returns will depend on the state the person resides in. Therefore before filing a return it’s important to know the rules of the state.

Get registered as a payee of professional tax in a local professional tax office at that specified state. It is imperative for all the individuals and businesses that are liable for the tax payment. Calculate the pay of professional tax in the prescription form. The payment and calculations done must be audited by the chartered Accountant. When it comes to employees, the employer has to deduct the salaries of employees for the professional tax. Once the person gets registered, he is then responsible to pay Professional Tax; different professions are specified with different PT rates.

- 37. What are the Documents required for professional tax Registration?

-

- Acknowledgement of the online form, along with the print out of the digital form submitted.

- Copy of PAN Card.

- Residence proof of Partner, Director, Proprietor.

- Proof of Constitution of business like Certificate of Incorporation.

- Address proof of Business place.

- Blank Cancelled Cheque.

- Establishment Certificate.

- PAN& PTEC details.

All these documents are required to be self-attested

- 38. I am a freelancer. Is profession tax applicable to me?

-

Yes, freelancers are also required to register and pay professional tax because professional tax is levied if the income exceeds the limit as specified in the state./p>

- 39. I am a director in 3 different companies. Am I required to pay profession tax in each company?

-

If all the 3 companies are in the same state, then you can make the payment from only one company of your choice.

- 40. What If An Employer Has Different Offices In Different States Of India?

-

If the employer has different offices in different states of India, they will need to take Professional Tax Registration in those particular states.

- 41. When Does The Employer Have To Pay The Professional Tax?

-

- If the employer has less than 20 employees, they need to make the payment of professional tax quarterly of the financial year.

- If the employer has more than 20 employees, they need to make the payment of professional tax within 15 days from the end of the month.

- 42. What If The Employer Does Not Get PTR Or Pay Professional Tax On Time?

-

- Delay in Registration of professional tax penalty levied by most states 5 per day.

- Delay in payment of professional tax penalty levied by most states 10% of the amount of tax

- Delay in filing of return of professional tax 1000 per return delay by 1 month and 2000 per return for further delay.

- 43. I am a doctor should I also required to register for PT?

-

Yes if you are a registered doctor with medical council of India or any other council dealing in allopathic, homeopathy, naturopathy or any other discipline of treatment , then it is required for you to take registration and pay PT.

- 44. If I have taken GST Registration, should I also need to take Profession tax registration?

-

Yes, any Business, Profession , Trade or calling operating for profit motive in Specified state need to take profession tax number and pay PT every year by filing appropriate challan and return. Now Maharashtra Profession tax department has started sending notice for all GST registered dealer who has taken GST but not registered for PT.

- 45. If I have taken GST Registration, should I also need to take Profession tax registration?

-

Yes. If your Registration application is approved, a Tax Payer Identification Number will be issued. The P TIN is an 11 digit number with the first two digits indicating the State code. You will have to use this TIN for all Tax Purposes. In case you are already a GST dealer and are in possession of a valid TIN, the same number will be allotted for you under the Enrolment Category. Please note that separate TINS will be issued for “Registration” and “Enrolment”

- 46. How will I get my Registration Certificate?

-

- 1. Once you registration application is approved, the RC certificate will be scanned & Uploaded to the dealer login.

- 2. The dealer can initiate all his business activities on receipt of the scanned certificate.

- 3. The Original certificate shall be couriered/ sent by RPAD to the premises of the dealer by the Registering Authority.

- 47. What happens if my Registration Application is found to be incomplete?

-

- In case of any gap found in the registration application, the Registering authority may return the application to the dealer by recording the reasons in writing and provide the dealer 7 days of time to respond to the query. The dealer may resubmit the application after rectifying the defects noted.

- In case of rejection of a registration application, the Registering Authority should issue a rejection order, by recoding the reasons for such rejection in writing.

- 48. Is there any annual renewal process for registration?

-

No. You need not approach any office for annual renewal of the P tax registration. Once issued, the certificate is considered to be valid until cancelled.

- 49. How we can file Professional Tax Return?

-

Once you will get registered with the Professional Tax registration department, Id Password will be issued in order to file a professional tax return. By using such Id password you can file a professional tax return on the website of the Karnataka government. For professional tax return filing you need to login to your account and on the basis of requirements such as monthly filing or quarterly filing, payment should be made.