GST Return Filing– An Introduction

The businesses registered under GST have to file returns monthly, quarterly and annually based on the category of business through the Government of India's GST portal. They have to provide the details of the sales and purchases of goods and services along with the tax collected and paid.Implementation of a comprehensive Income Tax system like GST in India will ensure that taxpayer services such as registration, returns, and compliance are transparent and straightforward. Individual taxpayers will be using 4 forms for filing their GST returns such as the return for supplies, return for purchases, monthly returns, and annual return. Small taxpayers who have opted for a composition scheme will have to file quarterly returns. All filing of returns will be done online.All registered businesses have to file monthly or quarterly and an annual GST return based on the type of business. All these GSTR filings are done online on the GST portal.

What is GST Return?GST return is an official document that furnishes all the purchases, sales, tax paid on purchases, and tax collected on sales-related details. The GST returns is required to be filed, following which the taxpayer has to pay off the tax liability.A GST return is a document containing details of all income/sales and/or expense/purchase which a taxpayer (every GSTIN) is required to file with the tax administrative authorities. This is used by tax authorities to calculate net tax liability.

Under GST, a registered dealer has to file GST returns that broadly include:

- Purchases

- Sales

- Output GST (On sales)

- Input tax credit (GST paid on purchases)

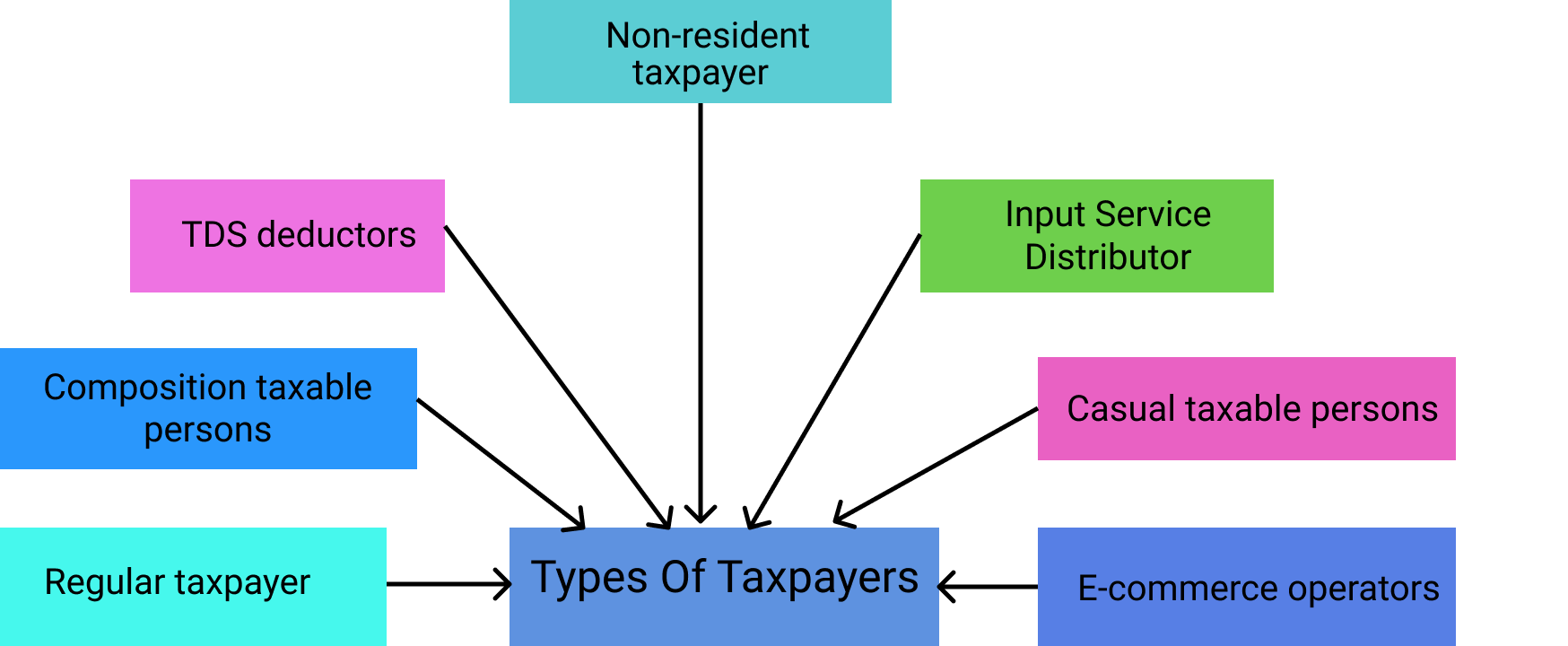

GST returns are different forms that a taxpayer has to file for every GSTIN to which he is registered. There are around 22 types of GST forms available. From these 22 GST forms, there are 11 that are active, 8 view-only and 3 suspended. So the number and type of GST you have to file is based on the type of taxpayer you have registered.There are 7 types of taxpayers. These are:

GST Returns are filed quarterly, monthly, or annually. In the GST regime, any regular business having more than 5 crore as annual aggregate turnovers has to file two monthly returns and one annual return. This amounts to 26 returns in a year.The number of GSTR filings varies for quarterly GSTR-1 filers under QRMP scheme. The number of GSTR filings online for them is 9 in a year, including the GSTR-3B and annual return.There are separate returns required to be filed by special cases such as composition dealers whose

All business owners and dealers who have registered under the GST system must file GST returns according to the nature of their business or transactions.

- Regular Businesses.

- Businesses registered under the Composition Scheme.

- Other types of business owners and dealers.

- Amendments.

- Auto-drafted Returns.

- Tax Notice.

So ideally, who should file GST? Every business that has an annual turnover of 40 lakhs and 20 lakhs in Hilly and North-Eastern States will have to register under GST and file the returns accordingly.Here is a summary of who should file an annual return under GST.

| S No. | Form No. | Form to be used for |

| 1. | Form GSTR-1 | Details of outwards supplies of goods or services (monthly or quarterly) Every registered person should file this form |

| 2. | Form GSTR-2A | Details of supplies auto drafted from GSTR-1 or GSTR-5 to recipient. Auto fill form that is view-only |

| GSTR 2B | View only form | |

| 3. | Form GSTR-3 | Details of sales and purchases (monthly or quarterly) |

| 4. | Form GSTR-3A | Notice to return defaulter u/s 46 |

| GSTR 3B | Needs to be filled by the normal taxpayer | |

| 5. | Form GSTR-4 | Annual return for registered persons opting composition levy. Needs to be filled by a composition dealer who has opted for a composition scheme |

| 6. | Form GSTR-4A | Auto drafted details for registered persons opting composition levy |

| 7. | Form GSTR-5 | Return for Non-Resident Taxable Persons. Needs to be paid by those non-resident foreigners who have businesses in India |

| 8. | Form GSTR-5A | Details of supplies of Online Information and Database Access or Retrieval (OIDAR) services by a person located outside India made to non-taxable persons in India. Non-resident OIDAR service providers |

| 9. | Form GSTR-6 | Return for input service distributors. Needs to be filed by an Input Service Distributor (ISD) |

| 10. | Form GSTR-6A | Details of supplies auto drafted from GSTR-1 or GSTR-5 to ISD. |

| 11. | Form GSTR-7 | Return for Tax Deduction at Source. Filed by those persons who need to deduct TDS under GST |

| 12. | Form GSTR-7A | Tax Deduction at Source Certificate |

| 13. | Form GSTR-8 | Statement for Tax Collection at Source. Filed by e-commerce operators |

| 14. | Form GSTR-9 | Annual return by Taxpayers registered under GST |

| 15. | Form GSTR-9A | Annual return by Compounding taxable persons registered under section 10 |

| 16. | Form GSTR-9B | Annual Return by E-Commerce operator |

| 17. | Form GSTR-9C | Reconciliation Statement by Taxpayers registered under GST |

| 18. | Form GSTR-10 | Final return Paid by those persons whose GST registration was cancelled or surrendered |

| 19. | Form GSTR-11 | Inward supplies statement for persons having Unique Identification Number (UIN) For refund claims by foreign diplomatic missions and embassies |

Different Types of GST Returns at a glance

| S No. | Types of GSTR | Purpose |

| 1. | GSTR-1 | GSTR-1 has to be filed against all goods and services rendered by a company. This includes all the invoices raised as well as credit-debit notes against sales for a tax period. |

| 2. | GSTR-2A | GSTR 2A is a view-only GST return for buying goods and services. It contains the details of all purchases made by the recipient in any month. All kinds of inward supplies to the recipient can be viewed as purchases made from other GST registered suppliers. |

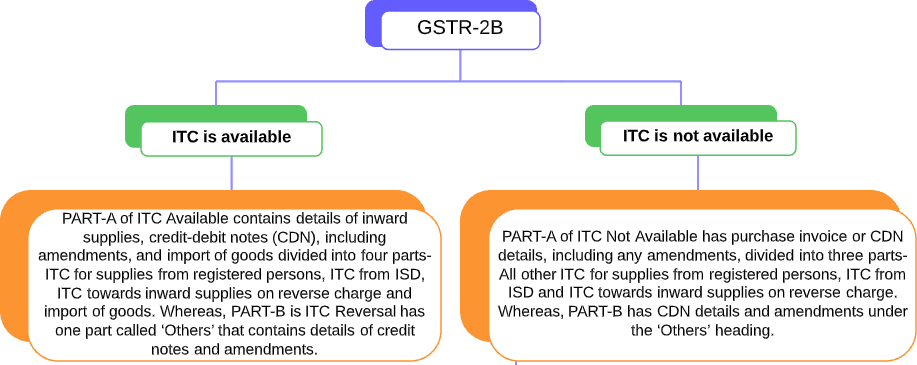

| 3. | GSTR-2B | This is also a static, view-only GST return. It is important for buyers of goods and services. GSTR-2B is available every month from August 2020 and contains ITC data of any period when it is checked back. |

| 4. | GSTR-3B |

GSTR 3B is a monthly self-declaration. It furnishes the summarized details of:

|

| 5. | GSTR-4 | GSTR-4 is an annual return to be filed by composition taxable persons. It is to be filed by April 30th following the relevant financial year. This return replaced GSTR-9A. |

| 6. | GSTR-5 |

GSTR-5 is for those non-resident foreign taxpayers who carry out transactions in India. They contain details of the following:

|

| 7. | GSTR-5A | GSTR-5A summarizes all the outward taxable supplies and tax payable by OIDAR, which stands for the Online Information and Database Access or Retrieval Services provider. You have to file this return by the 20th of every month. |

| 8. | GSTR-6 |

GSTR-6 must be filed by an Input Service Distributor (ISD) every month. Its composition details are:

The due date of the GSTR-6 is the 13th of every month. |

| 9. | GSTR-7 |

GSTR-7 is to be filed by the persons who are required to deduct the TDS under GST. TDS stands for “Tax deducted at source.” Here’s what the GSTR-7 entails:

The due date of the GSTR-7 is the 10th of every month. |

| 10. | GSTR-8 | This form is required to be filed by the e-commerce operators registered under GST. They are usually required to collect tax at the source. All the details of supplies made through the e-commerce platform and the TCS on the same are recorded. It is to be filed by the 10th of every month. |

| 11. | GSTR-9 |

This is an annual return to be filed by taxpayers who are registered under GST. It is due by December 31st for the year following the specific financial year. It consists of the following:

|

| 12. | GSTR-9C | It is a statement filed by all the taxpayers registered under GST whose turnover exceeds 2 crores in a financial year. This is a unique form in that it has to be certified by a Chartered Accountant or a Cost Management Accountant after a GST audit and looking over the GST-9.It is to be filed by December 31st of the year that follows the relevant financial year. However, as per the Union Budget 2021, the mandate for the GST audit by CAs and CMAs has been removed. |

| 13. | GSTR-10 | The GSTR-10 form is to be filled by a person whose registration was surrendered or cancelled. It is also called a final return which needs to be filed within three months of the cancellation order or the date of cancellation, whichever comes first. |

| 14. | GSTR-11 | GSTR-11 is for foreign diplomatic missions and embassies that do not pay tax in India but require a refund of taxes. It is filed by those persons who have been issued a Unique Identity Number (UIN) to get a refund for the goods and services incurred by them in India. These returns have details of the inward supplies received and refunds claimed.These were the different types of GST returns and who should file them. |

How to File GST Returns with GSTN?

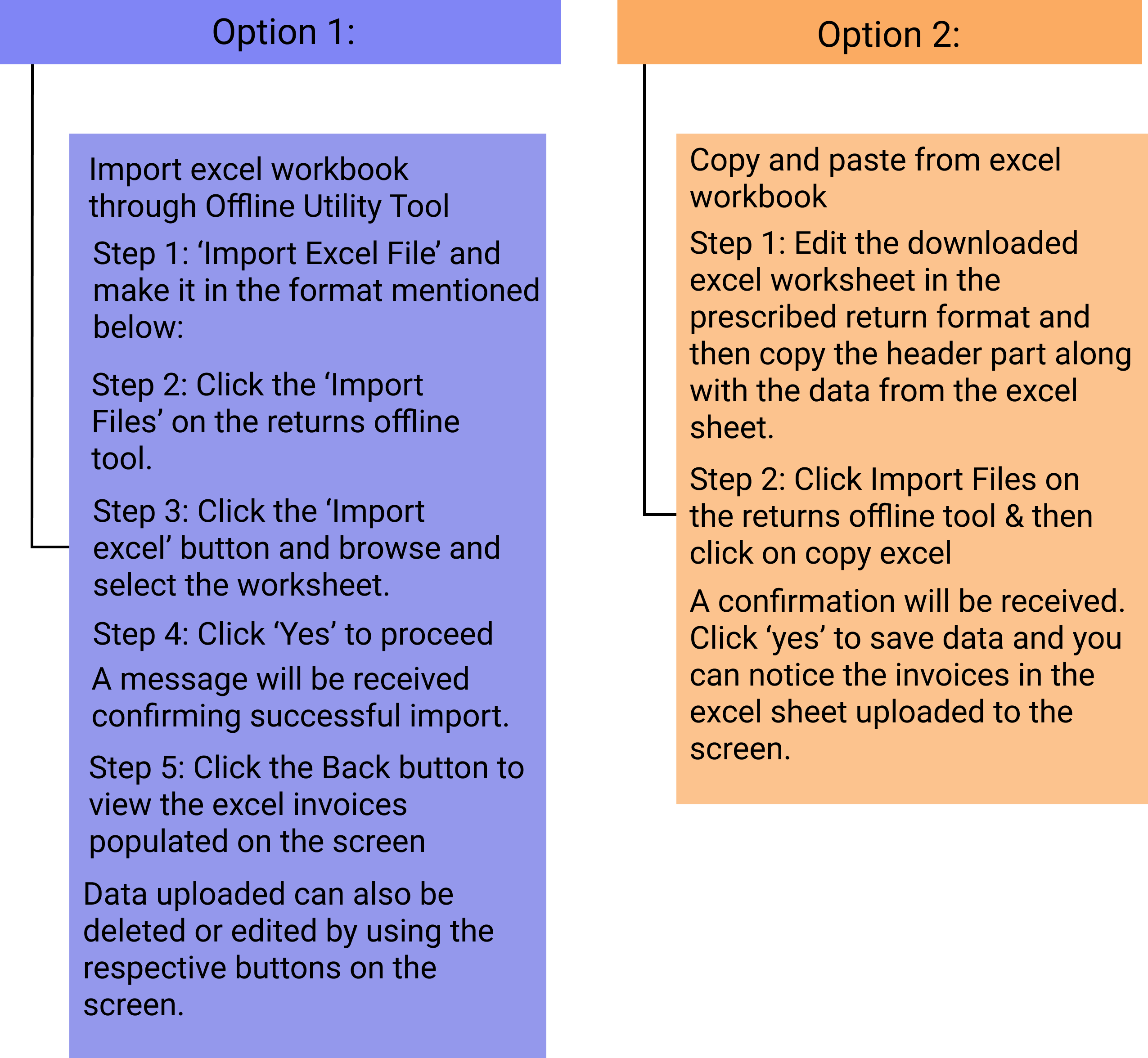

GST returns can be filed with the software provided by the Goods and Services Tax Network (GSTN), which will auto-populate the forms. The Goods and Service Tax Network (GSTN) stores information about all GST registered sellers and buyers to ensure a streamlined and simple process. The data is then combined and maintained for future reference. Business entities can simply download the excel workbook that is available on the common GST portal free of charge. The template can be used to collate all the necessary information offline smoothly. Once done, the file must be uploaded to the GST portal.

(1). GST return online filing processThe GST return online filing process can be completed in the following steps.

Step 1: Use the GST portal that is www.gst.gov.in.

Step 2: Based on your state code and PAN number, a 15 digit number will be issued.

Step 3: Each invoice that you have needs to be uploaded. Against each invoice, a reference number will be issued.

Step 4: After this, the next step is to file the outward returns, inward returns, and cumulative monthly returns. All errors can be rectified.

Step 5: File the outward supply returns of GSTR-1 using the information section at the GST Common Portal on or before the 10th of the month.

Step 6: The outward supplies furnished by the supplier will be gotten from the GSTR-2A.

Step 7: After this, the recipient has to verify the details of the outward supplies and file details of credit or debit notes.

Step 8: Next, supply details of the inward supplies of goods and services in the GSTR-2 form.

Step 9: Supplier can accept or reject the details provided by the inward supplies made apparent in the GSTR-1A.

To file your GST returns in the offline mode, you need to visit and download the following offline tool, Website Link. Once you have downloaded this tool, you can easily fill in the GSTR-1 and GSTR-2 forms. All you have to do is follow the steps in the link provided above.

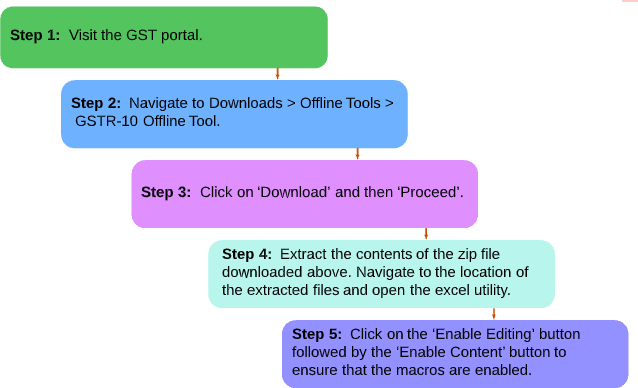

How to download GST returns form?Here’s how to download GST returns from the government portal.Follow these steps one after the other.

Step 1: Login to the GST portal.

Step 2: From there, go to the Service→ Returns→ Returns Dashboard.

Step 3: Choose the month and year from the drop-down.

Step 4: Hit PREPARE OFFLINE.

Step 5: Navigate to “Download” and click on “GENERATE FILE.

Step 6: Click on the “Click Here” link and download the link. You should get a ZIP file.

Step 7: Open this file using the GST offline tool by clicking on “Open” under the Open Downloaded Return file from the GST portal.

How to Check Status of GST Returns?

To check GST return status online, just follow these steps.

- Open the portal https://www.gst.gov.in/.

- Enter the details on the login page.

- Choose and click Service > Returns > Track Returns Status.

- From the drop-down, select “Status of Return.

- Click the Search button.

- The status may show up as ‘TO BE FILED / SUBMITTED BUT NOT FILLED / FILED- VALID / FILED-INVALID’.

This is how to track GST return filing. GST returns filing used to be a tedious and laborious job. It has now become simplified by the process of online filling of the various forms. Once you have an idea of the various GST returns forms you have to fill, the process can become significantly simplified.

Revision of Returns:The mechanism of filing revised returns for any correction of errors/ omissions has been done away with. The rectification of errors/ omissions is allowed in the subsequent returns. However, no rectification is allowed after furnishing the return for the month of September following the end of the financial year to which, such details pertain, or furnishing of the relevant annual return, whichever is earlier.

What is the penalty for the late filing of GST returns?If you have failed to pay the GST returns, there is an interest and late fee to be paid. The interest is at 18% per annum to be calculated on the amount of outstanding tax. And under the CGST and SGST, there is a late fee of 100 to be paid each day, so the total comes to 200 per day.

Penal Provisions Relating to Returns:Any registered person, who fails to furnish form GSTR-1, GSTR-2, GSTR-3 or Final Return within the due dates, shall be liable to pay a late fee of 100 per day, subject to a maximum of 5,000.ITC Matching and Auto-Reversal:

- It is a mechanism to prevent revenue leakage.

- The process of ITC Matching begins after the due date for filing of the return (20

th of every month). This is carried out by GSTN.

- The details of every inward supply furnished by the taxable person (i.e. the “recipient” of goods and/or services) in form GSTR-2 shall be matched with the corresponding details of outward supply furnished by the corresponding taxable person (i.e. the “supplier” of goods and/or services) in his valid return. A return may be considered to be a valid return only when the appropriate GST has been paid in full by the taxable person, as shown in such return for a given tax period.

- In case the details match, then the ITC claimed by the recipient in his valid returns shall be considered as finally accepted and such acceptance shall be communicated to the recipient. Failure to file valid return by the supplier may lead to denial of ITC in the hands of the recipient.

- In case the ITC claimed by the recipient is in excess of the tax declared by the supplier or where the details of outward supply are not declared by the supplier in his valid returns, the discrepancy shall be communicated to both the supplier and the recipient. Similarly, in case, there is duplication of claim of ITC, the same shall be communicated to the recipient.

- The recipient will be asked to rectify the discrepancy of excess claim of ITC and in case the supplier has not rectified the discrepancy communicated in his valid returns for the month in which, the discrepancy is communicated, then such excess ITC as claimed by the recipient shall be added to the output tax liability of the recipient in the succeeding month.

- Similarly, duplication of ITC claimed by the recipient shall be added to the output tax liability of the recipient in the month in which, such duplication is communicated.

- The recipient shall be liable to pay interest on the excess or duplicate ITC added back to the output tax liability of the recipient from the date of availing of ITC till the corresponding additions are made in their returns.

- Re-claim of ITC refers to taking back the ITC reversed in the Electronic Credit Ledger of the recipient by way of reducing the output tax liability. Such re-claim can be made by the recipient only in case the supplier declares the details of the Invoice and/or Debit Notes in his valid return within the prescribed timeframe. In such case, the interest paid by the recipient shall be refunded to him by way of crediting the amount to his Electronic Cash Ledger.

Types of GST returns and their purposes

| GST Returns | Purpose |

| GSTR1 |

Tax return for outward supplies made (contains the details of interstate as well as intrastate B2B and B2C sales including purchases under reverse charge and inter-state stock transfers made during the tax period). If Form GSTR-1 is filed late (post the due date), the late fee will be auto-populated and collected in the next open return in Form GSTR-3B. From January 1, 2022, taxpayers will not be permitted to file Form GSTR-1 if they have not filed Form GSTR-3B in the preceding month.GSTR-1 form has to be filed by a registered taxable supplier with details of the outward supplies of goods and services. This form is filled by the supplier. The buyer has to confirm the auto-populated buy information on the form and make modifications if required. The form will contain the following details:

GSTR-1 has to be filed by 10th of the following month. |

| GSTR2 |

Monthly return for inward supplies received (contains tax payer info, period of return and final invoice-level purchase information related to the tax period, listed separately for goods and services).GSTR-2 form has to be filed by a registered taxable recipient with details of the inward supplies of goods and services. The form will contain the following details:

GSTR-2 has to be filed by 15th of the following month. (Suspended from September 2017 onwards) |

| GSTR2B | GSTR 2B is an auto-drafted document that will act as an Input Tax Credit (ITC) statement for taxpayers. The GST Council states that GSTR 2B will help in cutting down the time taken to file returns, minimize errors, ease reconciliation and simplify compliance. |

| GSTR3 |

Consolidated monthly tax return (contains The taxpayer’s basic information (name, GSTIN, etc), period to which the return pertains, turnover details, final aggregate-level inward and outward supply details, tax liability under CGST, SGST, IGST, and additional tax (+1% tax), details about your ITC, cash, and liability ledgers, details of other payments such as interests, penalties, and fees).GSTR-3 form has to be filed by a registered taxpayer with details that are automatically populated by from GSTR-1 and GSTR-2 returns forms. The taxpayer has to verify and make modifications, if any. GSTR-3 return form will contain the following details:

GSTR-3 has to be filed by 20th of the following month. (Suspended from September 2017 onwards) |

| GSTR3B | Temporary consolidated summary return of inward and outward supplies that the Government of India has introduced as a relaxation for businesses that have recently transitioned to GST. Hence, in the months of July and August 2017, the tax payments will be based on a simple return called the GSTR-3B instead. |

| GSTR9 | Annual consolidated tax return (It contains the taxpayer’s income and expenditure in detail. These are then regrouped according to the monthly returns filed by the tax payer).GSTR-9 form is filed by normal taxpayers with details of all income and expenditure for the year. This detail will be regrouped in accordance with the monthly returns. The taxpayer will have the opportunity to make modifications in the information provided if required. GSTR-9 has to be filed by 31st December of the following financial year along with the audited copies of the annual accounts. |

| GSTR9C | Audit form that needs to be filed by every taxpayer who is liable to get their annual reports audited when their aggregate turnover exceeds 2 crores in a financial year. |

| Businesses registered under the Composition Scheme | |

| GSTR4 |

Quarterly return for compounding vendors (It contains the total value of supply made during the period covered by the return, along with the details of the tax paid at the compounding rate (not more than 1% of aggregate turnover) for the period along with invoice-wise details for inward supplies if they are either imports or purchased from normal taxpayers).GSTR-4 form has to be filed by taxpayers who have opted for the Composition Scheme. Taxpayers with small business or a turnover of up to 75 lakh can opt for the Composition Scheme wherein he or she has to pay tax at a fixed rate based on the type of business. Taxpayers under this scheme will not have input tax credit facility. GSTR-4 quarterly return form will contain the following details:

GSTR-4 has to be filed by 18th of the following month. |

| GSTR9A | Annual composition returns form that has to be filed by every taxpayer who is enrolled in the composition scheme. (Suspended) |

| GST Returns | Purpose |

| GSTR 5 |

Variable return for Non-resident foreign taxpayers (It contains the details of the taxpayer, period of return and invoice details of all goods and services sold and purchased (this also includes imports) by the tax payer on Indian soil for the registered period/month).GSTR-5 form has to be filed by all registered non-resident taxpayers. This form will contain the following:

GSTR-5 has to be filed by 20th of the following month. |

| GSTR 6 |

Monthly return for ISDs (This return contains the details of the taxpayer’s basic information (name, GSTIN, etc), period to which the return pertains, invoice-level supply details from the GSTR-1 of counter-parties, invoice details, including the GSTIN of the taxpayer receiving the credit, separate ISD ledger containing the opening ITC balance for the period, credit for ITC services received, debit for ITC reversed or distributed, and closing balance).GSTR-6 form has to be filed by all taxpayers who are registered as an Input Service Distributor. This form will contain the following:

GSTR-6 has to be filed by 13th of the following month. |

| GSTR 7 |

Monthly return for TDS transactions (This return contains the taxpayer’s basic information (name, GSTIN, etc), period to which the return pertains, supplier’s GSTIN, invoices against which the tax has been deducted (categorized under the major tax heads - SGST, CGST, and IGST), and details of any other payments such as interests and penalties).GSTR-7 form has to be filed by all registered taxpayers who are required to deduct tax at source under the GST rule. This form will contain the following:

GSTR-7 has to be filed by 10 of the following month. |

| GSTR 8 |

Monthly return for ecommerce operators (It contains the taxpayer’s basic information (name, GSTIN, etc), the period to which the return pertains, details of supplies made to customers through the e-commerce portal by both registered taxable persons and unregistered persons, customers’ basic information (whether or not they are registered taxpayers), the amount of tax collected at source, tax payable, and tax paid).GSTR-8 form has to be filed by all e-Commerce operators who are required to collect tax at source under the GST rule. This form will contain details of supplies effected and the amount of tax collected under Sub-section (1) of Section 43C of Model GST Law. Other details include:

GSTR-8 has to be filed by 10th of the following month. |

| GSTR 9B | Annual return form that has to be filed by ecommerce operators who collect tax at the source. |

| GSTR 10 |

Final GST return before cancelling GST registration (This final return is to be filed when terminating business activities permanently/cancelling GST registration. It will contain the details of all supplies, liabilities, tax collected, tax payable, etc).GSTR-10 form has to be filed by any taxpayer who opts for cancellation of GST registration. This form will contain the following:

GSTR-10 final return form has to be filed within 3 months of the date of cancellation or date of cancellation order, whichever is later. |

| GSTR 11 |

Variable tax return for taxpayers with UIN (It contains the details of purchases made by foreign embassies and diplomatic missions for self consumption during a particular month).GSTR-11 form has to be filed by everyone who has been issued a Unique Identity Number (UIN) and claims a refund of the taxes paid on inward supplies. This form will contain the following details:

Based on the above mentioned details, the tax refund will be made. GSTR-11 form has to be filed on 28th of the month, following the month for which supply was received. |

| GST Returns | Purpose |

| GSTR 1A | An amendment form that is used to correct the GSTR-1 document including any mismatches between the GSTR-1 of a taxpayer and the GSTR-2 of his/her customers. This can be filed between 15th and 17th of the following month. |

| Auto-drafted Returns | |

| GSTR 2A | An auto drafted tax return for purchases and inward supplies made by a taxpayer that is automatically compiled by the GSTN based on the information present within the GSTR-1 of his/her suppliers. |

| GSTR 4A | Quarterly purchase-related tax return for composition dealers. It’s automatically generated by the GSTN portal based on the information furnished in the GSTR-1, GSTR-5, and GSTR-7 of your suppliers. |

| Tax Notice | |

| GSTR 3A | Tax notice issued by the tax authority to a defaulter who has failed to file monthly GST returns on time. |

Different types of GST Returns with due dates

Here is a list of all the returns to be filed as prescribed under the GST Law along with the due dates.

GST filings as per the CGST Act subject to changes by CBIC Notifications| Return Form | Description | Frequency | Due Date |

| GSTR-1 | Details of outward supplies of taxable goods and/or services affected. | Monthly | 11th of the next month with effect from October 2018 until September 2020. *Previously, the due date was 10th of the next month. |

| Quarterly (If opted under the QRMP scheme) | 13th of the month succeeding the quarter. Was end of the month succeeding the quarter until December 2020) | ||

| GSTR-2 Suspended from September 2017 onwards |

Details of inward supplies of taxable goods and/or services effected claiming the input tax credit. | Monthly | 15th of the next month. |

| GSTR-3 Suspended |

Monthly return on the basis of finalization of details of outward supplies and inward | Monthly | 20th of the next month. |

| from September 2017 onwards | supplies along with the payment of tax. | ||

| GSTR-3B | Simple return in which summary of outward supplies along with input tax credit is declared and payment of tax is affected by the taxpayer. | Monthly | 20th of the next month from the month of January 2021 onwards^ Staggered^^ from the month of January 2020 onwards upto December 2020. **Previously 20th of the next month for all taxpayers. |

| Quarterly | 22nd or 24th of the month next to the quarter*** | ||

| ^20th of next month for taxpayers with an aggregate turnover in the previous financial year more than 5 crore or otherwise eligible but still opting out of the QRMP scheme. 20th of next month for taxpayers with an aggregate turnover in the previous financial year more than 5 crore.For the taxpayers with aggregate turnover equal to or below 5 crore, 22nd of next month for taxpayers in category X states/UTs and 24th of next month for taxpayers in category Y states/UTs ***For the taxpayers with aggregate turnover equal to or below 5 crore, eligible and remain opted into the QRMP scheme, 22nd of month next to the quarter for taxpayers in category X states/UTs and 24th of month next to the quarter for taxpayers in category Y states/UTs | |||

| Category X: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana or Andhra Pradesh or the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands and Lakshadweep.Category Y: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha or the Union Territories of Jammu and Kashmir, Ladakh, Chandigarh and New Delhi. | |||

| CMP-08 | Statement-cum-challan to make a tax payment by a taxpayer registered under the composition scheme under section 10 of the CGST Act (supplier of goods) and CGST (Rate) notification no. 02/2019 dated 7th March 2020 (Supplier of services) | Quarterly | 18th of the month succeeding the quarter. |

| GSTR-4 | Return for a taxpayer registered under the composition scheme under section 10 of the CGST Act (supplier of goods) and CGST (Rate) notification no. 02/2019 dated 7 March 2020 (Supplier of services). | Annually | 30th of the month succeeding a financial year. |

| GSTR-5 | Return for a non-resident foreign taxable person. | Monthly | 20th of the next month |

| GSTR-6 | Return for an input service distributor to distribute the eligible input tax credit to its branches. | Monthly | 13th of the next month. |

| GSTR-7 | Return for government authorities deducting tax at source (TDS). | Monthly | 10th of the next month. |

| GSTR-8 | Details of supplies effected through e-commerce operators and the amount of tax collected at source by them. | Monthly | 10th of the next month. |

| GSTR-9 | Annual return for a normal taxpayer. | Annually | 31st December of next financial year. |

| GSTR-9A (Suspended) |

Annual return optional for filing by a taxpayer registered under the composition levy anytime during the year. | Annually until FY 2017-18 and FY 2018-19 | 31st December of next financial year, only up to FY 2018-19. |

| GSTR-9C | Certified reconciliation statement | Annually | 31st December of next financial year. |

| GSTR-10 | Final return to be filed by a taxpayer whose GST registration is cancelled. | Once, when GST registration is cancelled or surrendered. | Within three months of the date of cancellation or date of cancellation order, whichever is later. |

| GSTR-11 | Details of inward supplies to be furnished by a person having UIN and claiming a refund | Monthly | 28th of the month following the month for which statement is filed. |

Types of GST Returns under New GST Law

The list of all types of GST returns in India along with frequency and the due date for filing returns.

| Return form | Who should file the return and what should be filed? | Frequency | Due date for filing |

| GSTR-1 | Registered taxable supplier should file details of outward supplies of taxable goods and services as effected. | Monthly | 11th of the subsequent month. |

| GSTR-2 | Registered taxable recipient should file details of inward supplies of taxable goods and services claiming input tax credit. | Monthly | 15th of the subsequent month. |

| GSTR-3 | Registered taxable person should file monthly return on the basis of finalization of details of outward supplies and inward supplies plus the payment of amount of tax. | Monthly | 20th of the subsequent month. |

| GSTR-4 | Composition supplier should file quarterly return. | Quarterly | 18th of the month succeeding quarter. |

| GSTR-5 | Return for non-resident taxable person. | Monthly | 20th of the subsequent month. |

| GSTR-6 | Return for input service distributor. | Monthly | 13th of the subsequent month. |

| GSTR-7 | Return for authorities carrying out tax deduction at source. | Monthly | 10th of the subsequent month. |

| GSTR-8 | E-commerce operator or tax collector should file details of supplies effected and the amount of tax collected. | Monthly | 10th of the subsequent month. |

| GSTR-9 | Registered taxable person should file annual return. | Annual | 31st December of the next fiscal year. |

| GSTR-10 | Taxable person whose registration has been cancelled or surrendered should file final return. | Once, after the registration of GST is cancelled | Within 3 months of date of cancellation or date of cancellation order, whichever is later. |

| GSTR-11 | Person having UIN claiming refund should file details of inward supplies. | Monthly | 28th of the month, following the month for which the statement was filed. |

How to File GST Returns Online?

From manufacturers and suppliers to dealers and consumers, all taxpayers have to file their tax returns with the GST department every year. Under the new GST regime, filing tax returns has become automated. GST returns can be filed online using the software or apps provided by Goods and Service Tax Network (GSTN) which will auto-populate the details on each GSTR forms. The Goods and Service Tax Network will store information of all GST registered sellers and buyers, combine the submitted details, and maintain registers for future reference. Companies have to file 3 monthly returns every 3 months and one annual return in a financial year (37 returns in total). GSTN has launched a simple excel based template to make the filing of returns easier for businesses. This excel workbook can be downloaded from the GST common portal free of charge. Taxpayers can use this template to collate invoice data regularly. The details of inward and outward supplies can be uploaded on the GST portal on or before the due date. The data preparation can be done offline. Only while uploading the prepared file on the GST portal will the taxpayer need the Internet.

Listed below are the steps for filing GST return online:

Step: 1 Visit the GST portal (www.gst.gov.in).

Step: 2 A 15 digit GST identification number will be issued based on your state code and PAN number.

Step: 3 Upload invoices on the on the GST portal or the software. An invoices reference number will be issued againts each invoice.

Step: 4 After Uploading invoices, outward return, inward return, and cumulative monthly return have to be filed online, if there are any errors, you have the option to correct it and re-file the return.

Step: 5 File the outward supply returns in GSTR-1 form through the in information section at the GST Common Portal (GSTN) on or before 10th of the following month.

Step: 6 Details of outward supplies furnished by the supplier will be made available in GSTR-2A to the recipient.

Step: 7 Recipient has to verify, validate, and modify the details of outward supplies, and also file details of credit or debit notes.

Step: 8 Recipient has to furnish the details of inward supplies of taxable goods and service in GSTR-2 form.

Step: 9 The supplier can either accept or reject the modifications of the details of inward supplies made available by the recipient in GSTR-1A.

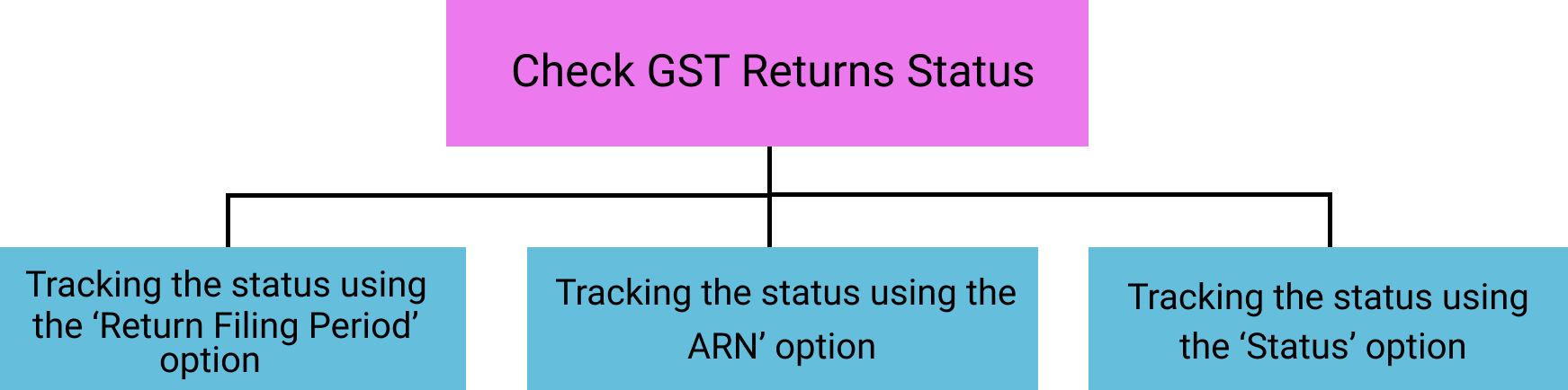

How to check GST Returns Status?

The official GST Login Portal allows you to check the status of your GST Returns. There are 3 different methods for the same. The methods are as follows:

- Step 1: Use your credentials to log in to the online GST portal at https://www.gst.gov.in/.

- Step 2: Click on the ‘Services’ tab from the top menu.

- Step 3: Navigate to ‘Track Return Status’ under the ‘Returns’ option.

- Step 4: Select the ’Return Filing Period’ option.

- Step 5: In the next page, select the financial year and the return filing period from the respective drop-down boxes.

- Step 6: Click on the ‘Search’ button and the status of the GST Return will be displayed on your screen.

- Step 1: Use your credentials to log in to the online GST portal at https://www.gst.gov.in/.

- Step 2: Click on the ‘Services’ tab from the top menu.

- Step 3: Navigate to ‘Track Return Status’ under the ‘Returns’ option.

- Step 4: Select the ’ARN’ option.

- Step 5: Enter the ARN in the field provided.

- Step 6: Click on the ‘Search’ button and the status of the GST Return will be displayed on your screen

- Step 1: Use your credentials to log in to the online GST portal at https://www.gst.gov.in/.

- Step 2: Click on the ‘Services’ tab from the top menu.

- Step 3: Navigate to ‘Track Return Status’ under the ‘Returns’ option.

- Step 4: Select the ’Status’ option.

- Step 5: Select the Status of Return that you are looking for from the drop-down box.

- Step 6: Click on the ‘Search’ button and the status of the GST Return will be displayed on your screen.

How to Download GST Returns?

You can download your GST Returns from the official GST Portal. You can follow the steps mentioned below to download your GST Returns:

Step 1:

- Use tour credentials to log in to the online GST portal at https://www.gst.gov.in/.

Step 2:

- Click on the Services tab from the top menu.

Step 3:

- Navigate to Returns Dashboard under the Returns option.

Step 4:

- In the next page, select the financial year and the return filing period from the respective drop-down boxes.

Step 5:

- Click on the Search button and select the GTR that you want to download.

Step 6:

- Click on the Prepare Offline button under the selected GSTR.

Step 7:

- Navigate to the Download option and click on Generate File.

Step 8:

- In general the request for the generation of the file takes around 20 minutes.

Step 9:

- Once the file is generated, a download link will be generated. Click on the Click Hereoption to download the ZIP file containing your GST Returns

Penalty for late filing of GST Returns

A penalty will be levied on the taxpayer in case he/she fails to file the returns on time. This penalty is called the late fee. As per the GST Law, the late fee is 100 for each day for each Central Goods and Services Tax (CGST) and State Goods and Services Tax (SGST). Thus, the total fine amount will be 200 per day. However, this rate is subject to changes which will be announced through notifications. The maximum amount of fine that can be levied is 5,000. Integrated GST or IGST does not attract any late fee in case the return filing is delayed. The taxpayer will also be required to pay an interest at the rate of 18% p.a. in addition to the late fee. This interest has to be calculated by the taxpayer on the amount of tax that is to be paid. The time period will be calculated from the day following the filing deadline till the date when the actual payment is made.

If GST Returns are not filed within time, you will be liable to pay interest and a late fee.Interest is 18% per annum. It has to be calculated by the taxpayer on the amount of outstanding tax to be paid. The time period will be from the next day of filing to the date of payment.A late fee is 100 per day per Act.So it is 100 under CGST & 100 under SGST. Total will be 200/day. Maximum is 5,000. There is no late fee on IGST. However, currently, a reduced late fees of 50 per day of delay ( 20 for NIL return) is applicable for those who file GSTR-1 and GSTR-3B.

New Functionalities made available for Taxpayers

The GSTN has issued update to inform all the taxpayers and stakeholders about the details of new functionalities made available on GST Portal in November 2021. The new functions enabled are facility of withdrawal of application of cancellation of registration, enabling EVC for all taxpayers, providing effective date of suspension in taxpayer's profile etc.Goods And Services Tax Network -New Functionalities made available for Taxpayers for the Month of November, 2021 on GST Portal related to GST Registration, Refunds, Registration, Returns and Payments, Refunds, Appeals, Enforcement and Recovery.

| Sr. No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Withdrawal of application for cancellation of registration in FORM REG-16 by taxpayers | Functionality has been introduced for taxpayers to withdraw their application for cancellation of registration, filed in Form REG-16, provided no action has been initiated by the tax officer against their application. |

| 2. | Providing effective date of Suspension in Taxpayer Profile | Now the effective date of suspension of a taxpayer is also displayed on the Portal when his/her profile is accessed using “Search Taxpayer” functionality. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Enabling EVC for all taxpayers |

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Change in the undertaking to be submitted by taxpayer for issuance of Form PMT 03 by Tax Officer | To enable Tax Officers to issue PMT03, an undertaking has to be filed by the submitted by taxpayer for taxpayers. The text in the undertaking form to be submitted by the taxpayer has been altered to include both credit and cash ledgers for enabling re-credit of inadmissible ITC to respective ledgers. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Removal of validation for all minor head except Tax/Cess in Forms GST APL-01, for Refund Module | To allow the applicant to file Appeal for interest on delayed grant of refund, the earlier validation on value of the Interest and Penalty amounts to not exceed the claimed amount/amount in the original order, has been removed from the Appeal form APL-01. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Updating the description in Ledgers for MOV-11, rectified MOV-09/MOV-11 | In case an order/ rectification order is issued in Form GST MOV09/11, the description in the liability ledger has now been updated to indicate the Demand Type. |

| 2. | Rectification of Order (DRC-08) functionality in Enforcement Module (for MOV-09/11 orders) |

For cases where the Tax Officer rectifies the demand order (Form GST DRC-07) or issues Rectification/ Withdrawal order (Form GST DRC-08) in transit cases, following functionality has been enabled for the Tax-payers:

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Filing of Application in Form GST DRC-20 by Taxpayer for Payment of recovery amount in installments or seeking extension of time |

|

List of Latest Features on Official GST Portal for Taxpayers

The timely updation leads to the maintenance of compliance. The taxpayers are required to stay up-todate to keep pace with the compliance which abolishes notice being issued to the taxpayers.

GSTN New Feature for Stopping to File GSTR 1The recent notification no. 35/2021 in the central tax mentioned the clause (a) of the sub-rule (6) of Rule 59 of CGST Rules, 2017 amendments, in which the preceding two months’ words are being substituted by 1th January 2022. The utility will be barring taxpayers from filing GSTR 1 if the filing is not done for GSTR 3B for the recent month. The utility will be soon live on the GSTN portal making it mandatory for the taxpayers to file the GSTR 1 and 3B.

New Feature to Check Last 5 GST ReturnsUpon the GST portal the Goods and Service Tax Networks (GSTN) has given a latest feature in which the assessee can now see their returns for the last five return periods. This return calendar will assist every enrolled business and professionals to check the past five return periods which assist in avoiding any interest or late fees.

GST Portal: New Features Added in GST Search Taxpayer TabThe Goods and Service Tax Network (GSTN) has incorporated additional features at the GST Portal.The changes have been made in the “GST Search Taxpayer tab”. The two pieces of information added in the GST Search Taxpayer tab at GST Portal are Profile and Place of Business (PoB). The PoB shows the Mobile Number and Email of the Principal Signatory. The aforesaid tab comprises features of the constitution of business, administrative office, gross total income, annual aggregate turnover, the status of e-KYC verification, and the status of Aadhaar Authentication.

The Goods and Service Tax Network (GSTN) has approved the unique characteristic to select Core Business Activity enabled on GST Portal. Today if you open the GST portal you will watch the new popup in which you will have to examine the main business as either a trader or service provider etc.Only post choosing any one of the choices stated above, you will be entitled to login into the GST account or furnish the GST return, and so on. It is to be noted that you can opt for only one major business activity. For the event where all the activities are applied to you, please choose the main business activity. Others will engage the work Contract and Other Miscellaneous Items.So to acknowledge the destination of the Manufacturer / Trader / Service Provider, you can click on the “Information Button” Moreover, if you need to amend it in the future then you can do it by navigating MY PROFILE COREBUSINESS ACTIVITY STATUS.

Enabled Feature for Filing LUT on GST Portal(LUT) Letter of undertaking for the financial year 2021-2022 can now be furnished in the GSTN portal as the new functionality has been activated for all the taxpayers and this has done for the facilitation of taxpayers.

New Communication Facility for Taxpayers on the GST PortalThe GST Portal now features a new facility of ‘Communication between Taxpayers’. This facility has been provided to send notifications, concerning missing documents or any deficiencies in documents or any other issue, by recipient taxpayers to their supplier and vice-versa.The facility is open for all registered persons, excluding people registered as TDS, TCS, or NRTP. After log in to the portal a registered person can use this facility to send a notification, view notification, send a reply, and view replies.

- Registered taxpayers can send notifications (Check procedure below).

- Registered taxpayers can view notifications by navigating to Services User Services Communication between Taxpayers > and select the Compose option.

- Registered taxpayers can view notification sent or reply sent by checking Outbox (Notification & Reply Sent) option.

- After Log in to the portal Navigating to – Services> User Services

- Then select Communication Between Taxpayers > and select the Compose option

- Choose the Supplier option to send a notification to a Supplier, otherwise, go with Recipient

- From the Document, Details section choose the Action Required by Supplier/ Recipient from the drop-down list and fillup all the required details

- The facility provides the facility to attach Up to fifty documents in a notification

- The Sender also has the option to add Remarks of up to 200 characters in the remark box

- The receiving party will get notifications about all the notifications received on their registered email and mobile number.

- The receiving party will also get a notification on GST Portal logging into the GST portal.

- Up to 100 notifications can be sent to a single GSTIN for a particular tax period.

- The recipient can send details of missing documents (not uploaded by their supplier in their Form GSTR-1) using this facility and send a notification to their supplier.

- Suppliers can add such documents directly to their Form GSTR-1, if not previously reported

- The document upload and download facilities will be available soon.

The Goods & Service Tax Network (GSTN) has lately added two new features to the portal with the aim to make it more user-friendly. Now, the taxpayers can get GSTR-3B monthly statements auto-populated on the portal. Another facility that has been added to the website is “Communication between Taxpayers”. To access this feature, log-in to your GSTN account and find the option under services > user services. This feature aims to enable seamless, peer-to-peer communication between the users, increasing user experience, security, and scalability.

GST Refund Application Status Track on GST & PFMS PortalIn the recent time, the government of India has offered an utility for the tracking of Refund Application Status from the GST portal. The given utility is said to provide the comprehensive details on the ‘Refund Application Status’ of the GST portal. However, the PFMS will validate the account detail first in the two stages through the RFD-01, and in RFD-05. Still, there is no extensive details that are provided by the government on the GST portal.

E-way Bill Data required to be imported to File GSTR-1In order to provide the taxpayers with the facility of seamless importing of data, the GST Portal got integrated to the E-way bill (EWB) portal. Now, the users are facilitated to get the B2B and B2C (large) invoices sections imported. They could also import the HSN-wise-summary of outward supplies section and both automatically. With the help of this update, the taxpayers could verify the data first and then could proceed and thus are exempted from unnecessary data-entry.

As a result of the new functionality released by the GST portal, the tax filers get assisted and find it’s easy in comparing their GSTR-3B tax liabilities with the GSTR-1 which have been filed. Just like this,the users of this portal could also compare their input tax credit claimed in GSTR-3B with the credits available in GSTR-2A. Along with this Comparison could also be made by them in their ITC claimed in the form GSTR-3B with the credits available in GSTR-2A

We would now be discussing the four different tabs under which the comparison of data could be carried out:-

- Liability other than export/reverse charge

- Liability due to reverse charge

- Liability due to export and SEZ supplies

- ITC credit claimed and due

The above-mentioned functionality would be proved to be very effective and would largely help in the reconciling of the GST returns filed and also in the preparation of the Annual returns.

A Taxpayer’s GSTIN can be entered while Filing a Refund ApplicationIn effect of the inverted duty structure under GST, a registered taxpayer could file a refund application for accumulated ITC. This portal has made the entry of a taxpayer’s own GSTIN possible in the inward supply detail statement by filing it on the same GST portal. This is a new facility which was not available earlier

Preferred Banks List Introduced for PaymentsDuring the payment process, a list of 6 banks would emerge on the portal among which, one bank needs to be selected by just one click and after that, we can proceed with the payment. The user is exempted from filling the complete Bank details time and again for making payment.Suppose you do not find your Bank’s name on the portal, what you just need to do is that you can add the Bank name in the list and the Banks’ name which is least preferable would itself get omitted thus, axiomatically maintaining the list of six.

The Credit of TDS/TCS Credit Can be UtilizedA new window has been introduced in the Portal which offers with an option to accept or reject the TDS/TCS credits available. So here the taxpayers could select the option and get the GST returns filed. Following this, the credits get relocated to the cash ledger and could be used for the GST payments. The window assists the taxpayers to recognize such credits and acts as per.

The tax filers till now were supposed to file their returns on a quarterly basis but now due to an update, it would not be required to wait for the quarterly filing of refund applications. As per the update, the portal has enabled the monthly filing option of the same. However, the clause now is that to file the refund application the taxpayer is required to make sure that the GSTR-1 for the quarter has been filed. Well, the facility is also there for the Businesses especially SMEs, which they could mobilize their cash flows if they are not willing to wait till the quarter end.

Responding to Show-cause Notices for Compulsory WithdrawalThe Portal has now been updated to make it easy for the Composition taxpayers to respond/reply to show-cause notices that have been issued for compulsory withdrawal from the composition scheme. In the case where a show-cause notice has been issued and the proceedings have been initiated the option there is just to reply to the same on the Portal. This is a time savior and simplifies responses for composition taxpayers.

Now File Online Appeals & Receive System-generated AcknowledgementsGST portal now offers an option where a taxpayer could file an appeal against an order passed by an appellate authority or against an advanced ruling by an appellate authority. The taxpayer has the same choice in the case of rectification of a mistake in the order passed. If an appellate authority fails to issue a final acknowledgement within the specified time, then a system generated final acknowledgement will be issued with the remark “subject to validation of certified copies”. This has made the process of filing appeals & tracking its status very easy & simple.

Get Compulsory Withdrawal through SCN Online Via Reply by Composition TaxpayersFollowing the updation, the composition taxpayer under GST now has the opportunity to Show Cause Notices (SCN) on the portal when the SCN is being issued for compulsory withdrawal from the composition scheme, also if the proceedings are originated against the composition taxpayer.

No Need of Bank Account Details at the Time of RegistrationIt is now not required to furnish the complete bank account details at the time of registration for Normal, OIDAR and NRTP taxpayers. The GST registration number should be obtained first and then the Bank details should be furnished at the time of the first login. This scheme would be most profitable for new businesses who are in the process of obtaining bank accounts. They have the benefit of saving time by simultaneously initiating GST registration.

New Features Introduced on GST Portal

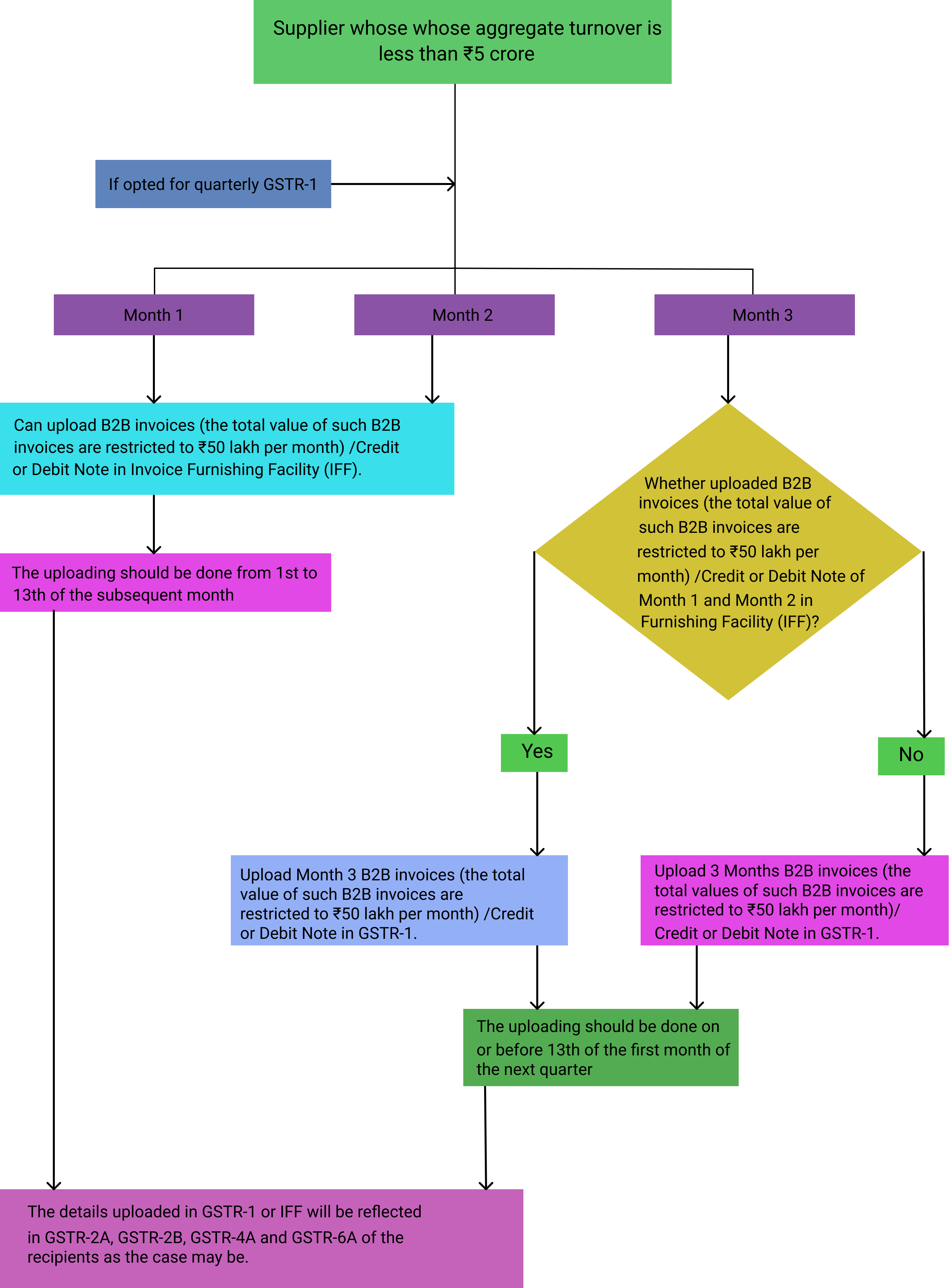

- The taxpayers under QRMP Scheme have been given an optional IFF, to furnish subtleties of their B2B Invoices and corrections thereto, for the initial 2 months of a quarter. Following amendments can be made in IFF:

- Taxpayers would now be able to move the records saved in their IFF of 1st month of a quarter to the IFF of the 2nd month of the quarter.

- Taxpayers can likewise move the records saved in IFF of the 1st and 2nd month of the quarter to their quarterly GSTR-1 (of a similar quarter).

- While getting ready IFF/GSTR-1 (of later long stretches of the same quarter) on the web, if there should arise an occurrence of saved records, taxpayers will get a pop-up message asking them to either move the records by choosing YES or erase them by choosing NO. Note: Records under the submitted (or documented) stage cannot be moved by above usefulness.

- Moreover, the GSTR-3B (Quarterly) of the taxpayer under the QRMP scheme will get autopopulated based on the file IFF and GSTR-1 of that particular Quarter.

As per this new feature introduced on the GST portal the taxpayer can now file GST RFD-01 without a LUT number for claiming the accumulated input tax credit (ITC) on exempt and nil-rated supplies. However, for claiming accumulated input tax credit (ITC) on exports of goods or/and service without GST payment and supply of goods or/and services to SEZ without GST payment, the taxpayer needs to mention the valid LUT number.

GST RegistrationTimelines for filing of Application for Revocation of Cancellation of Registration in Form GST REG-21 that was due on 15th April 2021 is extended till 30th June 2021 on the GST Portal. However, these extensions of date have now ceased to be effective from 1st July 2021. Moreover, the period for filing of GST REG-21 (an application for revocation of canceled GST registration) is now amended to 90 days on the GST Portal. This 90 days period will start from the order date of Cancellation of GST Registration in Form GST REG-19.

Ledgers- As per this new feature introduced on the GST portal, the taxpayer will be able to view the ledger for 12 months instead of 6 months. Moreover, the taxpayer details can now download the ledgers for 12 months in pdf and Excel formats.

- Temporary ID holders and unregistered applicants can now transfer the amount available in the cash ledger between major or/and minor heads using the GST PMT-09 Form.

- Now the taxpayers registered under the composition scheme will be able to see the negative liability statement on GST Portal. Moreover, the negative balance showing in the negative liability statement will get auto-adjusted against the tax liabilities of the subsequent tax period(s).

The CBIC has updated the current available HSN Master on the GST portal. As per this new feature introduced on GST Portal, HSN masters now include product names commonly used in Trade against the particular HSN code. In addition, the taxpayer can Search for HSN functionality on the GST Portal, available both in Pre and Post Login. Moreover, now the taxpayer can download the download HSN in Excel Format.

New Functionalities made available for Taxpayers on GST Portal between January-March, 2021

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Aadhaar Authentication enabled for Persons/ applicants applying for GST registration through MCA portal in SPICe -AGILE Form | Persons/ applicants applying for new registration in GST, through MCA portal in SPICe-AGILE Form, can now opt for Aadhaar Authentication (while applying for registration). |

| 2. | Disabling entering Aadhaar number by Taxpayers/ Applicants in registration application |

The field for entering Aadhaar number has been disabled for

|

| 3. | Selection of Core Business Activity by existing Taxpayers on the GST Portal |

The existing taxpayers have been provided with functionality on the GST portal to select their core business activity. They can select one of the following categories as their core business activity, based on their turnover:

|

| 4. | Post TRN Login, Tracking of Registration Application Status | The Search ARN Functionality for Registration, post TRN Login (i.e. after TRN is generated by taxpayer/ applicant but has not completed the filing of registration application), has been enhanced for the taxpayers. They will now be displayed various stages of Registration, with the current status of their application in green color and remaining pending stages being grayed out. |

| 5. | Deemed approval of Registration Application in Form GST REG-01 |

|

| 6. | Field for capturing validity period, in case of SEZ unit and SEZ developers, in Form GST REG-01 |

|

| 7. | Facility to upload documents in Form GST REG-13 |

|

| 8. | Aadhaar Authentication and eKYC changes for Existing Taxpayers |

Note: In this case, the process of e-KYC authentication would be subject to approval of uploaded e-KYC documents by Tax Official.

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | RESET button enabled on GST Portal for Form GSTR-1/ IFF (Invoice Furnishing Facility) | Normal taxpayers, irrespective of their filing profile (of quarterly or monthly), have now been provided with a RESET button on the GST Portal, in Form GSTR-1/IFF. This will enable them to delete the entire saved data, for the specific return period, but not yet submitted or filed their Form GSTR-1/IFF. |

| 2. | Reporting and paying interest & other amounts, in Form GSTR- 5A by OIDAR registrants | A person registered as OIDAR can now declare interest and any other liabilities in Table 6 - Interest or any other amount of their Form GSTR 5A and discharge it through Electronic Cash Ledger. |

| 3. | Download of Table 5 data, after filing, enabled for Form GST ITC-04 | Registered manufacturers who are required to file quarterly Form GST ITC-04 (to furnish details of inputs or capital goods, sent to a job worker without payment of tax), can now download the data of Table 5 of Form GST ITC-04 (on the GST Portal), after filing the Form, when there is change in the state code, due to merger or creation of a State/ UT. This is to download data, when there is change in State/ UT code, before the goods are received back. |

| 4. | Issuance of Form GSTR 3A, for Non Filing of GSTR-3B Returns to taxpayers, under QRMP scheme | Functionality has been deployed on GST Portal for issuance of system generated notice in Form GSTR-3A, to the taxpayers who have opted for/ assigned to QRMP Scheme and fail to file their GSTR-3B return on quarterly frequency, by due date. |

| 5. | Discontinuation of filing of Form GSTR-9A, for FY 2019-20 & onwards | The facility of filing Annual Returns in Form GSTR-9A by taxpayers in Composition Scheme, as per proviso to sub-section (1) Section 44 has been done away with on GST Portal, from FY 2019-20 & onwards. Thus, now taxpayers will not be able to view/save/file Form GSTR-9A for FY 2019-20 & onwards. Filing of the said return for the FY 2017-18 and 2018-19 is available (& is optional). |

| 6. | Facility to file NIL Form GST ITC-03 by the taxpayers opting in to Composition scheme | Existing taxpayers while opting for composition scheme are required to file details of stock in Form GST ITC-03 and pay tax on the stock (on which ITC has been claimed by them). Now a facility has been provided on the GST Portal to such taxpayers to file NIL Form GST ITC-03. |

| 7. | Validation of date on entry of invoices of cancelled suppliers and date of registration, in Form GSTR-6 and showing of tax period and filing status in Excel download of Form GSTR 6A |

|

| 8. | Implementation of 35% Challan in QRMP Scheme in Form GST PMT-06 for making payment |

|

| 9. | Editing the Auto-population of some data in Form GSTR-3B |

|

| 10. | Allowing reporting of GSTINs and tax deducted of OIDARs, in Form GSTR-7, by TDS deductors | Earlier, reporting of GSTINs of OIDAR registrants was not allowed in Form GSTR-7, for reporting of tax deduction made by the Deductor. The same has now been enabled on the GST Portal. The TDS deducted will be credited to the cash ledger of the OIDAR supplier on acceptance. |

| 11. | Notice in Form GSTR-3A for Non Filing of GSTR-3B Returns |

|

| 12. | Invoice Furnishing Facility (IFF) facility for taxpayers under Quarterly Returns Monthly Payment (QRMP) Scheme |

An Invoice Furnishing Facility (IFF) facility has been provided to taxpayers under QRMP Scheme (Quarterly filers of Form GSTR-1 and also of Form GSTR-3B returns), as per sub-rule (2) of Rule59 of the CGST Rules, 2017. Taxpayers who have opted for quarterly filing frequency under the scheme can file their details of outward supplies (B2B invoices only) for first two months of a quarter (M1 and M2 respectively of a Quarter) in IFF. For e.g. for Apr-June qtr., B2B invoices only for the months of April (M1) and May (M2) can be filed in IFF by a taxpayer.

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Filing of refund application in Form GST RFD-01, by exporter of services (with payment of tax), in cases of Foreign exchange fluctuations | The system earlier validated the refund amount claimed by the exporter of services (with payment of tax), against the proceeds realized (against exports, as submitted by the claimant in form of FIRC). If the value realized mentioned in BRC/FIRC column, was less than the refund amount claimed, then such taxpayers were not allowed to file their refund application on GST Portal. This validation has now been removed and taxpayer will be able to file refund application now in such cases (As the value realized in BRC/FIRC may fluctuate due to foreign exchange fluctuations and net realization may be less than the refund amount). |

| 2. | Pre login Tracking of Refund Application Status | Now taxpayers can navigate to Services > Track Application Status Select the Refund option > Enter ARN to track their refund application, without logging into the GST Portal. This will display various stages of Refund application filed by them, with the current status of their application in green color and remaining pending stages being grayed out. |

| 3. | Enabling taxpayers/ applicants with (only) TRN, to manually enter bank account details in Refund Application in Form GST RFD-01 | So far the taxpayers/applicants having (only) TRN were unable to file an application for refund, as they were not allowed to enter or add bank account details in the Registration Module. To enable filing of Refund Application by such taxpayers/applicants, a facility has been made available to them for manual entry of bank account details in Form GST RFD-01, while filing an application for refund. |

| 4. | Filing of Refund application by taxpayers under QRMP scheme |

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Audit related functionalities made available to taxpayers |

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Selection of two more reasons for voluntary payment in Form GST DRC-03 |

Following two reasons have been included for selection in drop down list for Form GST DRC-03, for the taxpayers to make voluntary payment:

|

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Status of Aadhaar authentication or E-KYC verification of a GSTIN | In the Search Taxpayer functionality (both pre-login and post login), the user will now be shown status of Aadhaar authentication or E-KYC verification of the searched GSTIN. |

| 2. | Change in label and functionality of HSN / Service Classification Code Tax Rate search | The label for “Search HSN / Service Classification Code Tax Rate” has now been changed to “Search HSN Code”. The functionality also has been enhanced wherein if the user searches for an item or a HSN code, the output is displayed systematically under the associated Chapter head, the description of the keyed in HSN code and also other associated HSN codes (all hyperlinked) along with it. (Services> User Services > Search HSN Code). |

| 3. | Additional information about taxpayers under Search Taxpayer functionality | In the “Search Taxpayer” functionality (Search Taxpayer> Search by GSTIN/UIN) available on the GST Portal, Post Login, users can now view certain additional details like Aadhar Authentication, e-KYC Verification, Compliance Rating, GSTIN/UIN status update, Annual Aggregate Turnover, Gross Taxable Income etc of the taxpayer. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Auto-generation of Form GST DRC-01 and its availability to the taxpayer on the GST Portal | As per Rule 142(1) of the CGST/SGST Rules, summary in Form GST DRC-01 is required to be served to the taxpayer along with the notice issued by the tax official under Section 73, 74, 129, 130 etc. The auto-generation of Form GST DRC- 01 (upon issuance of SCN/MOV-07/MOV-10 in Enforcement Module) has been enabled on the GST Portal and the same is now made available to the taxpayer under Additional Notices & Orders sub menu (Services> User Services > Additional Notices & Orders). |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Saving Advance Ruling/Advance Ruling Appeal applications by applicants | Applicants can now save Advance Ruling/Advance Ruling Appeal applications upto 15 days, before editing and filing it on GST Portal. These applications in saved stage will be automatically purged after 15 days. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Filing appeal against Refund order in Form GST APL 01 |

|

New Functionalities made available for Taxpayers on GST Portal in December, 2021

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Changes made in Form GSTR-1/IFF |

To improve the taxpayer experience some enhancements have been done in GSTR-1/IFF user interface wherein taxpayers are provided with

For more details, please click https://www.gst.gov.in/newsandupdates/read/513 |

| 2. | Creation of My Masters facility in Form GSTR-1/ IFF |

|

| 3. | Allowing entry of suspended GSTINs as recipients in Form GSTR 1/ IFF (B2B Tables) | The system used to return an error message if a supplier entered GSTIN of a suspended taxpayer in the B2B, B2BA, CDNR and CDNRA tables of Form GSTR1/IFF. This validation has now been removed and taxpayer would be able to enter a suspended GSTIN as a recipient of taxable supplies in respective tables of Form GSTR-1/IFF. |

| Sr.No. | Form/Functionality | Functionality made available for Taxpayers |

| 1. | Integration of Appeal Module with Enforcement Module | The Enforcement module has now been integrated with Appeal module. The taxpayers will now be able to file an online appeal against orders passed by an Enforcement Officer. |

| 2. | Integration of Appeal Module with Assessment Module | The Assessment module has now been integrated with Appeal module. The taxpayers will now be able to file an online appeal against orders passed by a Tax Officer. |

Applicability of Form GSTR-9C from FY 2020-21 onwards

Businesses registered under the GST law having more than 2 crore as annual aggregate turnovers in a financial year had to get their books, represented by the annual financial statements, audited under Section 35(5) of the CGST Act.

After the conclusion of the GST audit by CA/CMA, the auditor had to sort out any deviations with the management, prepare a reconciliation statement between the audited financial statements and Form GSTR-9 (GST annual returns) filed by the business for a particular financial year. The Form was known as GSTR-9C provided by Section 44 of the CGST Act, read with CGST Rule 80, and this form had to be certified by the same auditor or a CA/CMA eligible to do so. It had to be prepared for every GSTIN registered under a particular PAN. Once the certification was complete, the business had to file both Form GSTR-9 and Form GSTR-9C on the GST portal on or before the due date of 31st December of the year following that financial year. The taxpayers can pay any additional liability reported in this form through Form DRC-03. They must select ― ’Reconciliation Statement’ from the drop-down provided in Form DRC-03 and pay towards such liability only through the electronic cash ledger. The GST department considers the information reported in Form GSTR-9C to check for significant discrepancies in the taxpayer’s reporting and compliance. In turn, if it finds any such discrepancy that the taxpayer does not resolve, it can issue notice to the taxpayer. The format of the erstwhile Form GSTR-9C was divided into two parts. Part-A contained the reconciliation statement with the mention of any differences. Part-B contained the certification by the auditor or CA/CMA.

Part-A was further divided into five parts as follows:

| Part No. | Particulars |

| Part-I | Basic details such as GSTIN, FY, Trade name and legal name, and any requirement of audit under any other law. |

| Part-II | Reconciliation between the turnover derived from the audited annual financial statement for a particular GSTIN and the turnover mentioned in Form GSTR-9 (GST annual returns). |

| Part-III | Reconciliation and differences, if any, between the GST-rate wise tax liability and payment as reported in Form GSTR-9 and derived from the audited financial statements for a particular GSTIN. |

| Part-IV | Reconciliation and differences, if any, between the input tax credit availed and used as reported in Form GSTR-9 and derived from the audited financial statements for a particular GSTIN. |

| Part-V | Auditor’s recommendation regarding any additional un-reconciled liabilities. |

Part-B had two varieties for use. The auditor could use the first type or format for certifying the Form GSTR-9C himself. The second type or format could be used by a CA/CMA who did not perform the audit but certifies the Form GSTR-9C based on the auditor’s observations.

Changes introduced by the Union Budget 2021 and notificationsThe Union Budget 2021 introduced two key changes in Sections 35 and 44 of the CGST Act. The government has removed Section 35(5) of the CGST Act. Further, Section 44 of the CGST Act stands amended. The changes in the Act were approved with the passing of the Finance Act, 2021. Following are the changes in the CGST Act

- The need for a GST audit by CA/CMA stands removed for FY 2020-21 and any later financial years.

- Every applicable taxpayer must submit a self-certified reconciliation statement by reconciling values between the audited financial statements and the annual returns.

- Some taxpayers may be exempted from complying with the annual return and reconciliation statement requirement through the CBIC notification.

- Section 44 shall not apply to any central government or state government departments already subject to audit by the Comptroller and Auditor-General of India (CAG).

The GST Council reaffirmed these changes at the 43rd GST Council meeting held on 28th May 2021. The CBIC notified these changes on 30th July 2021 vide Central Tax notifications 29/2021 and 30/2021. It notified the applicability of Sections 110 and 111 of the Finance Act, 2021 that contained these amendments. Further, Rule 80(3) and Part-B of the CGST Rules have been amended to specify the threshold limit for applicability and bring changes to the format. Accordingly, Form GSTR-9C applies to a taxpayer if the annual aggregate turnover limit for the relevant financial year is more than 5 crore. The format of Form GSTR-9C has been modified to include FY 2020-21 and to support self-certification.

Applicability of Form GSTR-9C from FY 2020-21 onwardsForm GSTR-9C continues to be exempted for input service distributors, taxpayers subject to TDS and TCS provisions, casual taxable persons and non-resident taxable persons. In addition to these, government departments and taxpayers with a total turnover less than or equal to 5 crore are added to the exemption category.

Accordingly, Form GSTR-9C becomes applicable to taxpayers with an annual aggregate turnover for the relevant financial year being more than 5 crore. These taxpayers are required to self certify or carry out a voluntary reconciliation statement without the need for audit and file it with the tax authority on or before 31st December of the year following the relevant financial year. The following table summarizes the threshold applicability of both annual returns and the reconciliation statement for FY 2020-21.

| Name of the Form A | Applicability- AATO* limit for FY 2020-21 | The due date for FY 2020-21 |

| GSTR-9 | > 2 crore | >31st December 2021 |

| GSTR-9C | > 5 crore |

Annual aggregate turnover during FY 2020-21.

(Changes applicable for FY 2020-21 and onwards)

Changes in Part-A: Reconciliation statement is as follows:

| Reference to part and/or table no. | Particulars | Changes made |

| Part-II – Tables 5B to 5N | Reconciliation of the annual turnover as per the audited annual financial statement with the turnover as declared in Form GSTR-9 | These tables are optional while filing GSTR-9C for FY 2020-21. If there are any adjustments, those can be done in Table 5O. |

| Part-III and Table no. 9 | Reconciliation of GST rate-wise liability and the amount payable | A new row is inserted below ‘K’ -0.10% to now have ‘K-1’ for other GST rates not listed above it. |

| Part-III and Table no. 11 | Any additional amount to be paid but not paid (on account of the reasons specified under Tables 6,8 and 10) | A new row ‘others’ is inserted below 0.10% to now have other GST rates not listed above it. |

| Part-IV- Tables 12B, 12C, and 14 | Reconciliation of Input Tax Credit (ITC) | These tables are optional while filing GSTR-9C for FY 2020-21. |

| Part-V | Auditor’s recommendation on any additional Liability due to non reconciliation | Heading changed to “Additional Liability due to non reconciliation” A new row ‘others’ is inserted below 0.10% to now have other GST rates not listed above it. |

| Verification | Verification of the registered person | Replaced by the following lines: I hereby solemnly affirm and declare that the information given herein above is true and correct, and nothing has been concealed therefrom. I am uploading the self-certified reconciliation statement in Form GSTR-9C. As applicable, I am also uploading other statements, including financial statements, profit and loss account and balance sheet, etc. |

| Instruction -serial no. 7 | Part V – Additional Liability due to non-reconciliation | The wordings of the instruction are revised to remove references to the auditor and their recommendations, as follows: Part-V consists of the additional liability to be discharged by the taxpayer due to non-reconciliation of turnover or non-reconciliation of the input tax credit. Any refund that has been mistakenly considered and paid back to the government must also be declared in this table. Lastly, any other pending demand to be settled by the taxpayer has to be declared in this Table. |

CFO or Finance Head’s responsibility towards self-certified GSTR-9C

No doubt that with the removal of the GST audit and certification by CA/CMA, compliance seems to have been simplified for taxpayers. On the flip side, the Finance Head’s of the taxpayer business will have added responsibility on their shoulders to report the figures in Forms GSTR-9 and GSTR-9C accurately.With this move being notified for FY 2020-21, every CFO or Finance Head of the applicable company must first ensure that their teams are aligned with the changes in the format of GSTR-9 and GSTR-9C. They should arrange for awareness sessions for their teams to understand the implications of removing the requirement of GST audit and certification by a CA/CMA.The government does not intend to reduce its verification measures with the removal of the GST audit. It may even increase the scrutiny procedures and impose penalties where it identifies any non-compliance or lapse in reporting. Businesses must notify any un-reconciled figures as it is in Form GSTR-9C, without any omissions. Companies may refer to the opinions and observations made by the statutory auditors regarding GST compliance while preparing GSTR-9C.